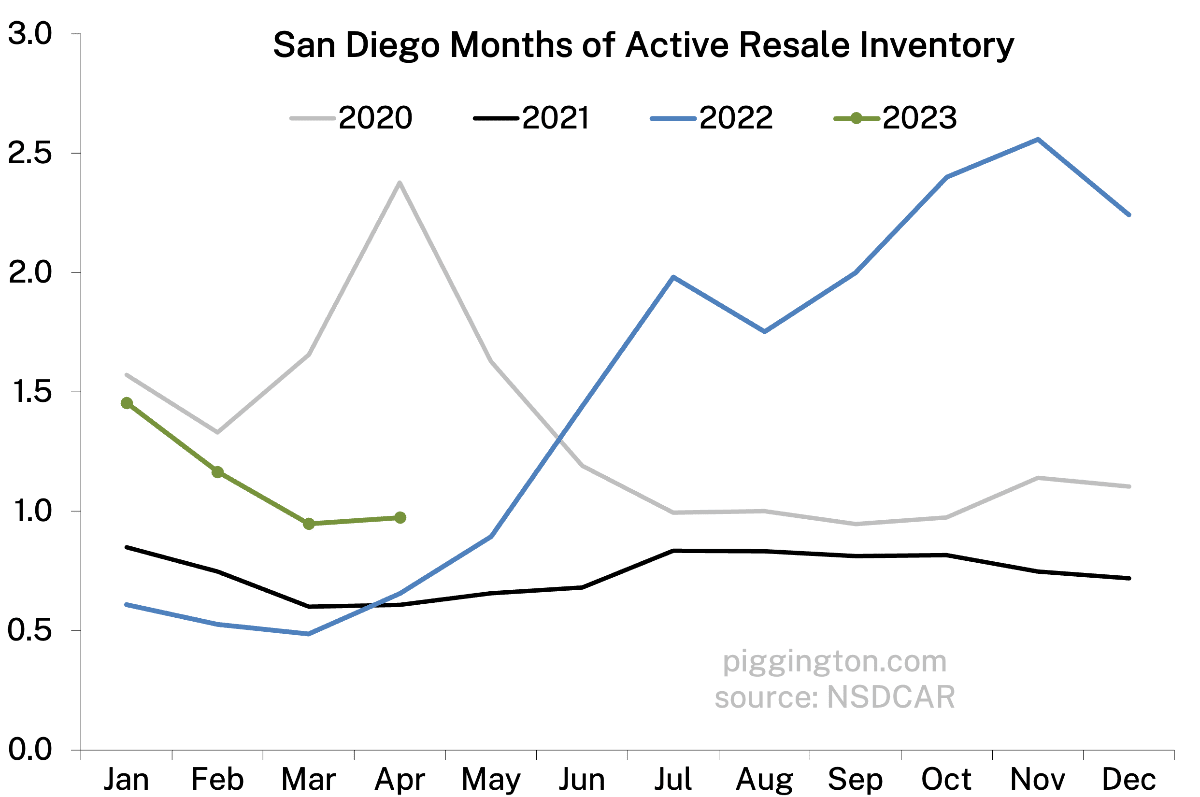

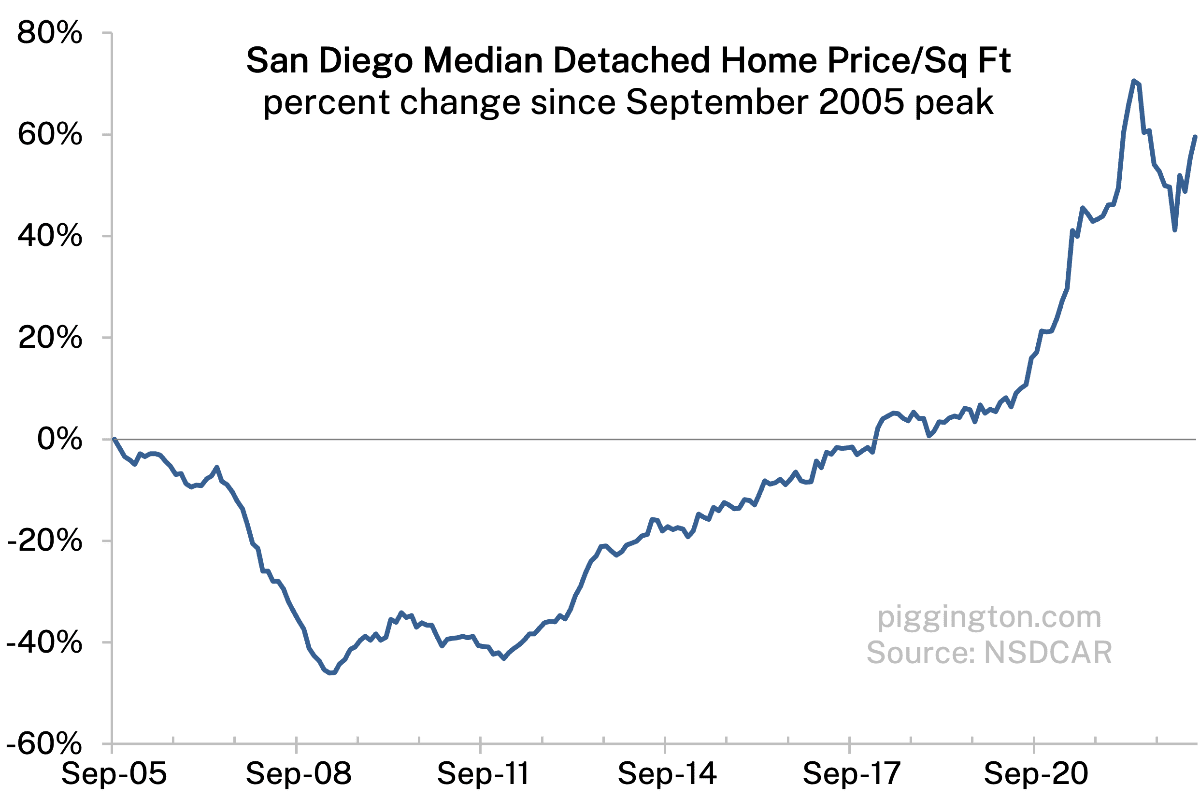

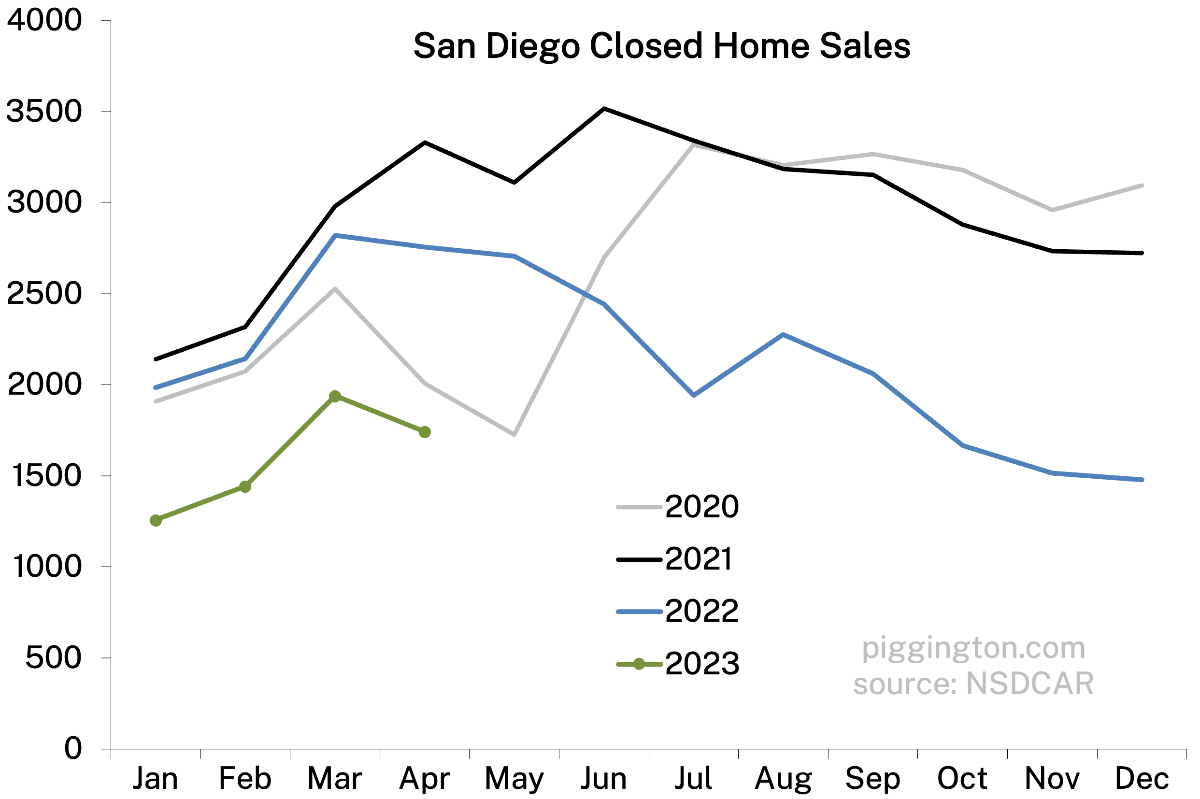

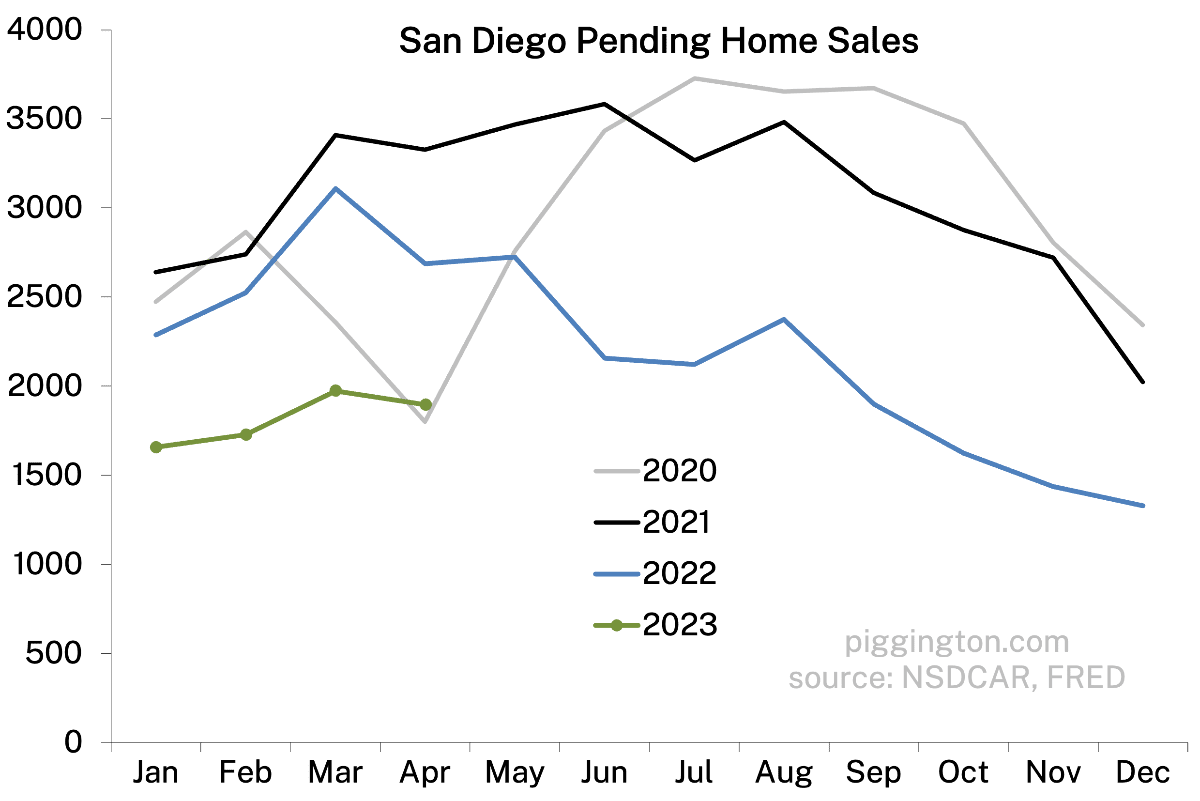

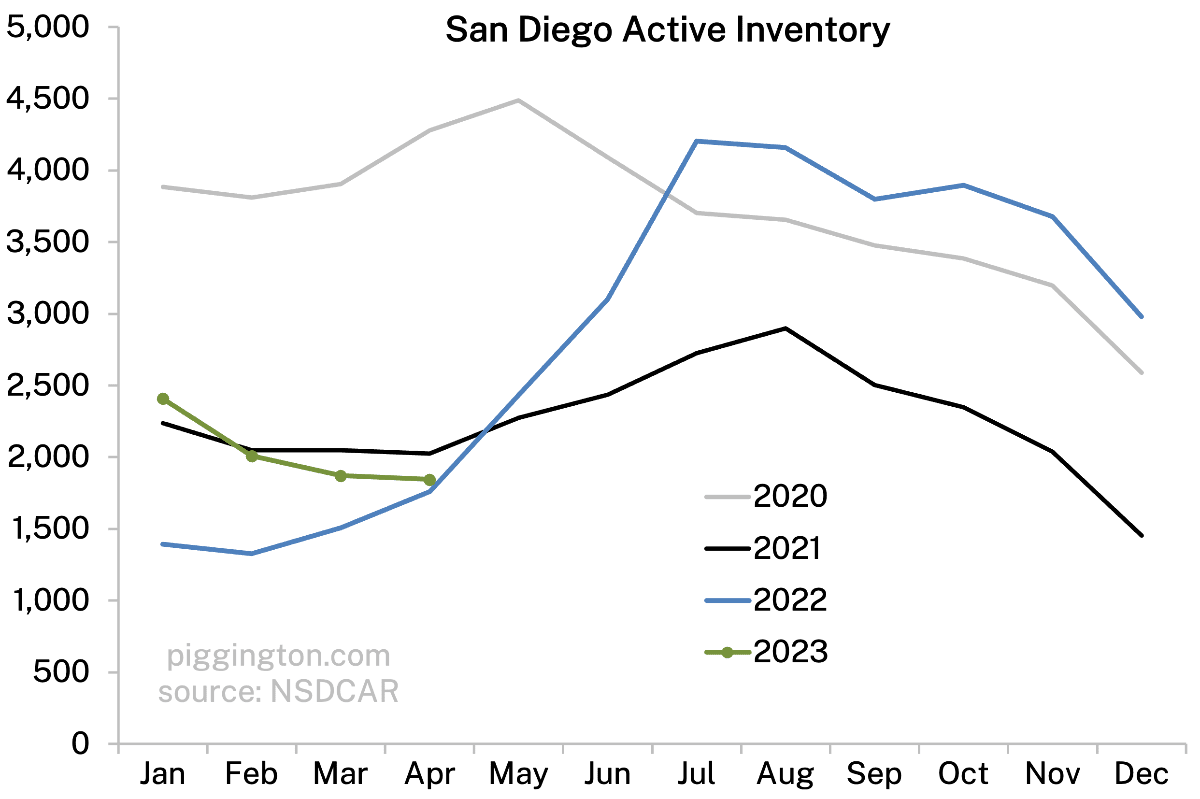

Hey folks. I would consider last month as a bit of a stalemate, based on the non-movement in months of inventory:

But the previous level of inventory was quite low.

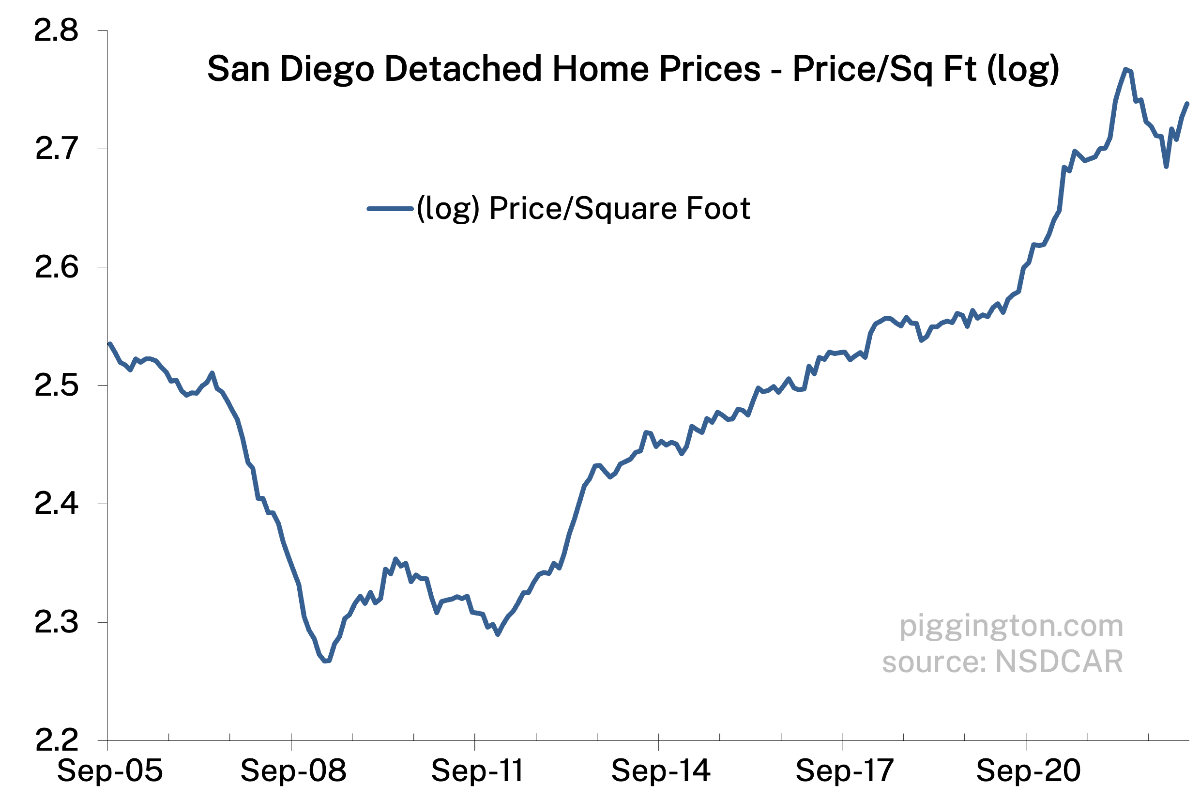

Not many people are buying, but even fewer are selling. And so prices are being supported, and rose further last month.

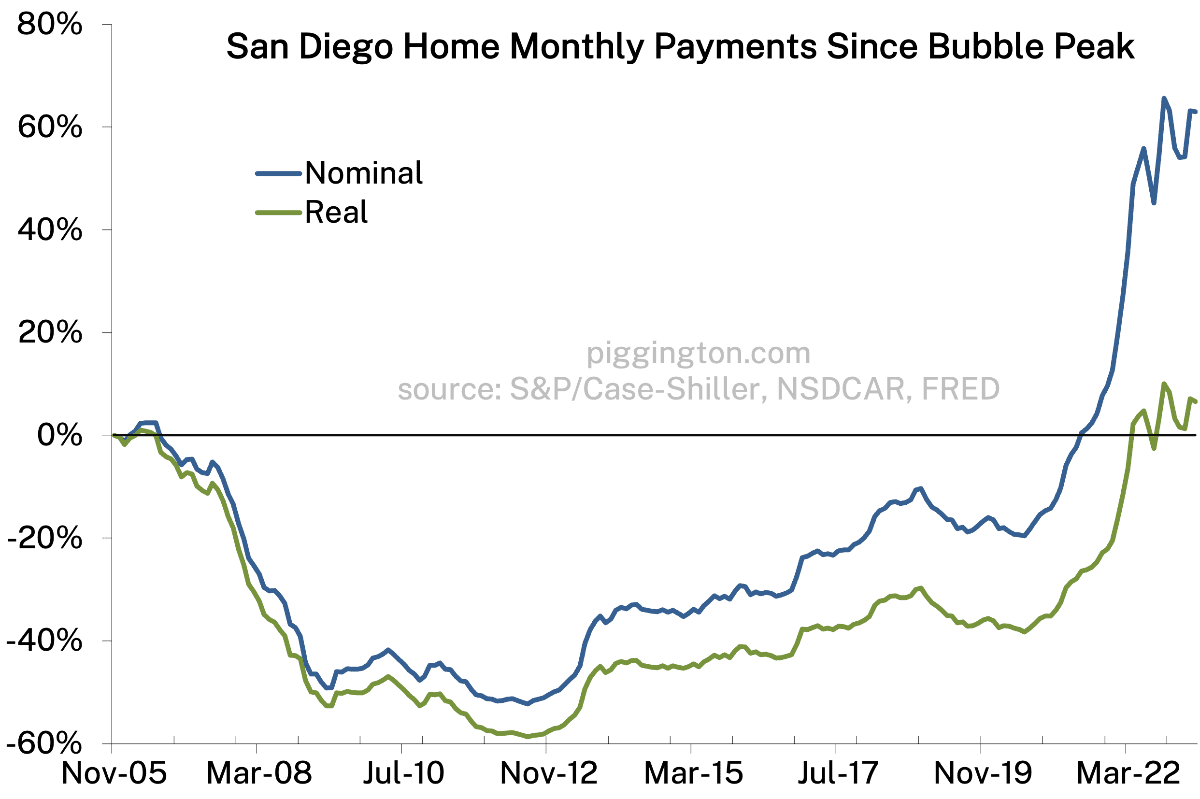

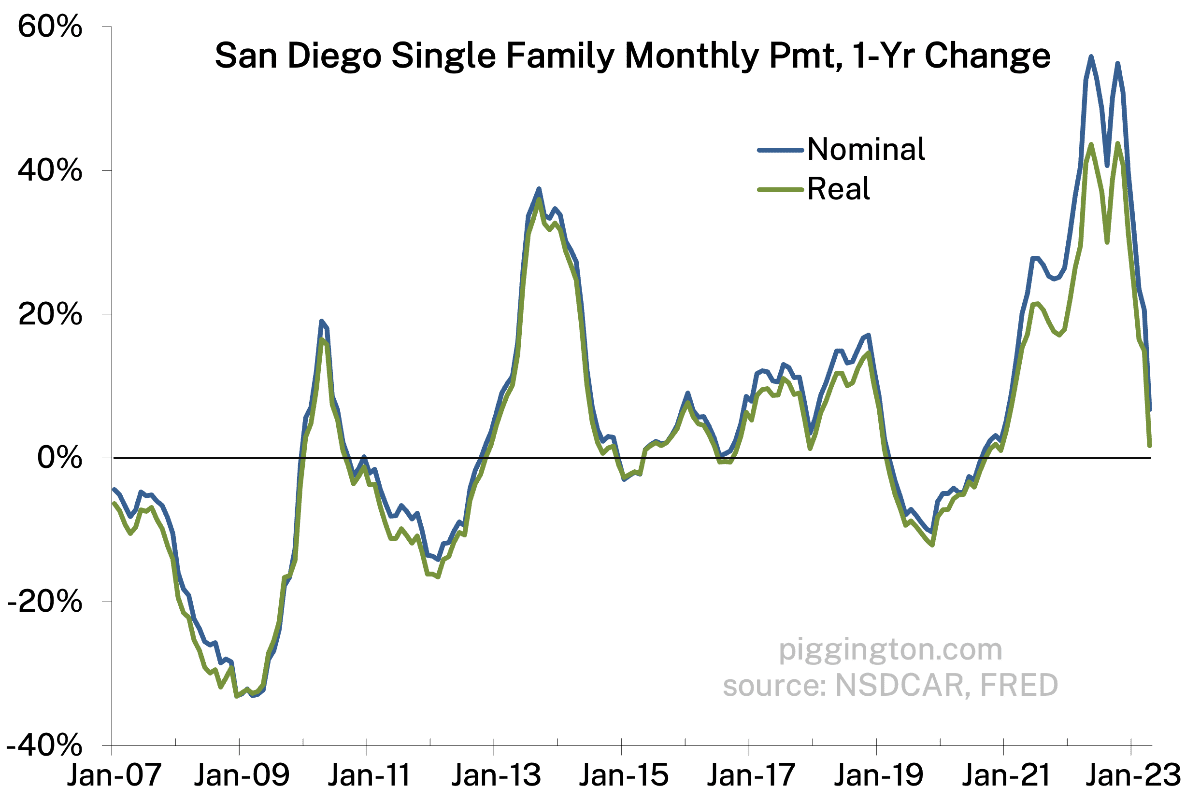

This is despite the fact that inflation-adjusted monthly payments are actually higher than they were at the bubble peak!

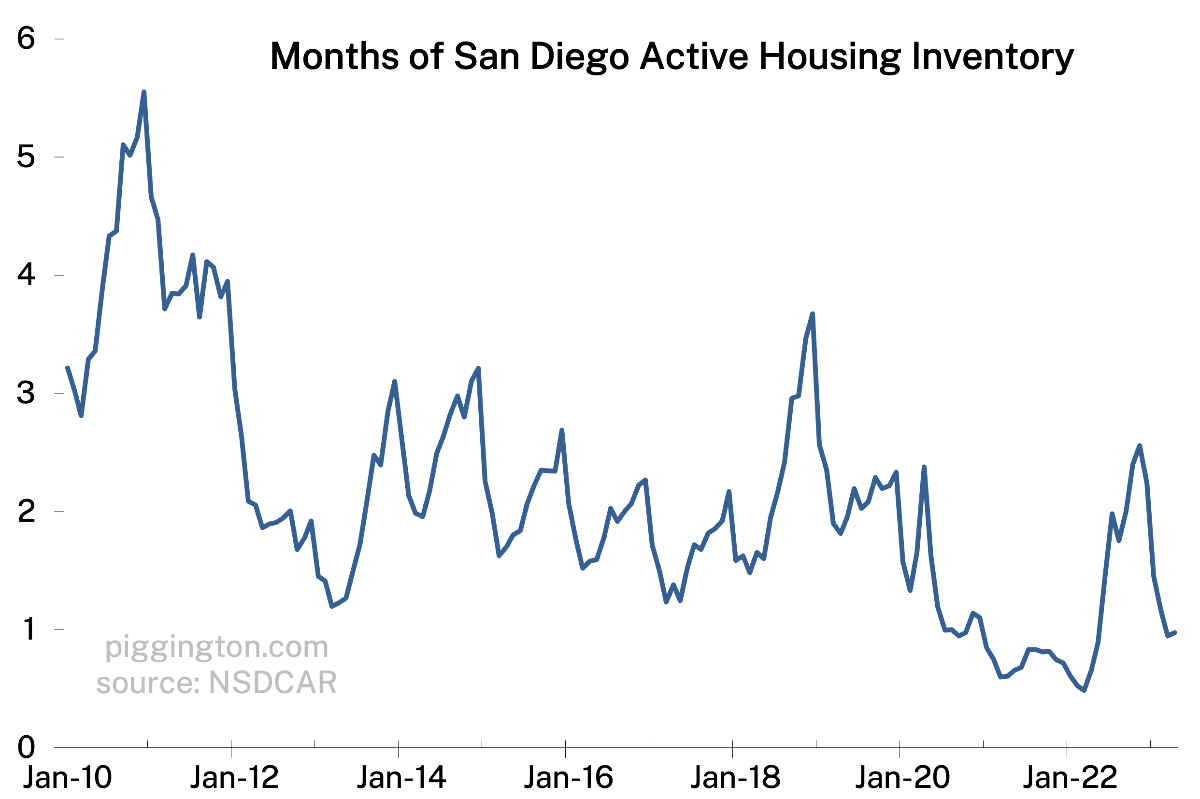

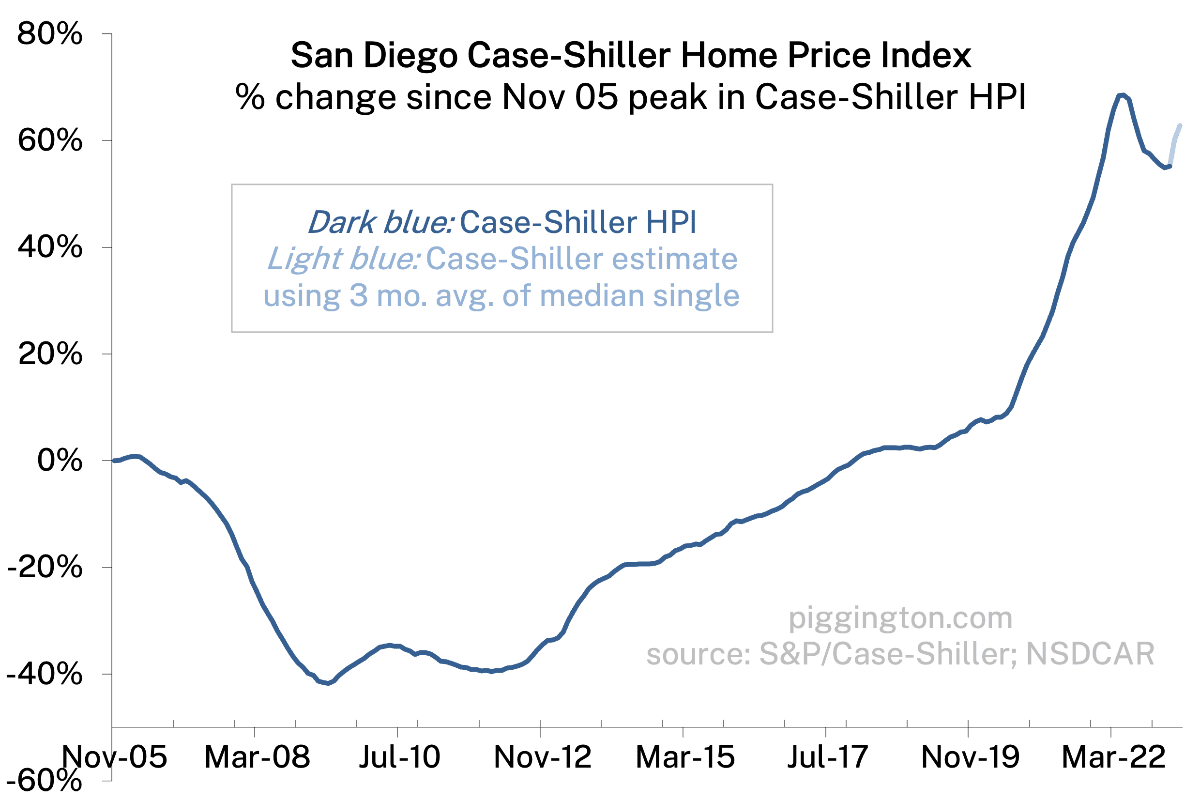

Inventory at this level is very supportive of prices in the short run, so I’d expect prices to rise further immediately ahead. But inventory is weather, not climate (see the second graph). FWIW my long term view continues to be that this level of affordability is not sustainable.

More graphs below…

Agree with every single part of that. The data is showing what I’ve been talking about for months. The only solution is continued albeit slower inflation and passage of time

Wait until the May and June data comes out. Inventory y-o-y is about to go deeply negative

“ This is despite the fact that inflation-adjusted monthly payments are actually higher than they were at the bubble peak! ”

Combine the fact that real incomes increased by about 30%, and the strong secular trend of WFH increasing residential demand, and the secular trend of increased real construction costs…

I think our fundamentals are a lot stronger than 2006.

I was helping someone look for a 2 bedroom to rent in suburban east county recently.

Lots of Zillow listings of places around $2000 now that were 1200-1400 in 2019-2020. The average listing age was also short, there were tons of contacts on them, and landlords almost all said up front how picky they are. Good credit, no pets, verified income.

Just one example:

8551 Graham Ter APT 6, Santee, CA 92071

Listed at 1400 in 2019, 2000 in a new listing today, 9 contacts and 1 application already.

I hear people in their 20s and 30s who rent talk about the specifics of the 10% annual rent increase law a lot too. There’s an expectation of regular large increases. They want to buy to avoid them.

Fair point on real income increases, income is a the better denominator than inflation. However, even using incomes/rents (which basically say the same thing)… we’re still not too far below bubble peak levels for monthly pmt affordability: https://piggington.com/shambling-towards-affordability-january-2023/

(PS 30% real income growth since 06 seems high but the point is directionally correct)

Hey Rich,

Thank you for the insight! My housing thesis aligns to what your long-term thesis is – affordability will be a limiter over the long run.

What befuddles me is that I am looking at two condos right now to rent and the economics from an owners perspective makes no sense. One condo in Carlsbad was purchased May 2023 for $825K and seeking $3,500/month in rent. Assuming 20% down payment, a very generous interest rate buydown at 5%, include HOA, prop tax, and insurance the monthly payment comes out to over $5,000/month. That does not include maintenance, Capex, or any other miscellaneous expenses you would typically UW in a rental property.

Same thing with another condo in Carmel Valley that was listed on the market for over 6 months and finally sold. The numbers still don’t make sense unless these are all cash purchases, but even then the unlevered yield is less than 3%, which is not good. Money markets are paying 5% and all you have to do is click a button and have instant liquidity.

What am I missing?

I think there are still buyers out there making suboptimal “investment” decisions which is helping stabilize home prices in the short run, but this is not a sustainable creation of value.

Curious to hear your thoughts and if you are seeing similar activity and if this stuff was happening during the last housing bubble?

Thanks,

Dan

There can be many explanations. Here are two. They did a 1031 exchange and brought lots of cash to purchase. They are buying as retirement home for future and looking to hedge against further increases in prices. There are more but the point is you are looking at it through your lens and they may have a very different one

Looking at the big picture, here is something to consider about real estate (as an investment class)

basically the “boomer generation” are entering their retirement era (so they are pulling out their money from the stock market, and putting their money into real estate in warm sun belt climates like the San Diego area)

https://zeihan.com/a-bungle-of-boomers/

To start at the end, no, I don’t think this is much like the bubble. Back then there was a lot of overconfidence/delusion and yolo mortgage underwriting to fuel the whole party, this doesn’t feel like that to me.

But I do share your sense that SD housing is very expensive, and to me it doesn’t seem like a very compelling investment unless you believe in continually rising valuations. But a lot of people do believe in that (even if only implicitly), so that could account for a chunk of demand, along with people who maybe don’t have a view but are price-insensitive because they just need a place to live.

My disclaimer here is that I haven’t gone out and run the numbers on individual properties (and I don’t know how to interpret your numbers — eg, did you back out principal repayment and tax benefits?). It’s more based on the valuation charts and the generally inverse relationship between valuations and long term returns.