Well it’s more of a “lurch” than a “shamble”, but I’m going to stick with the traditional naming convention.

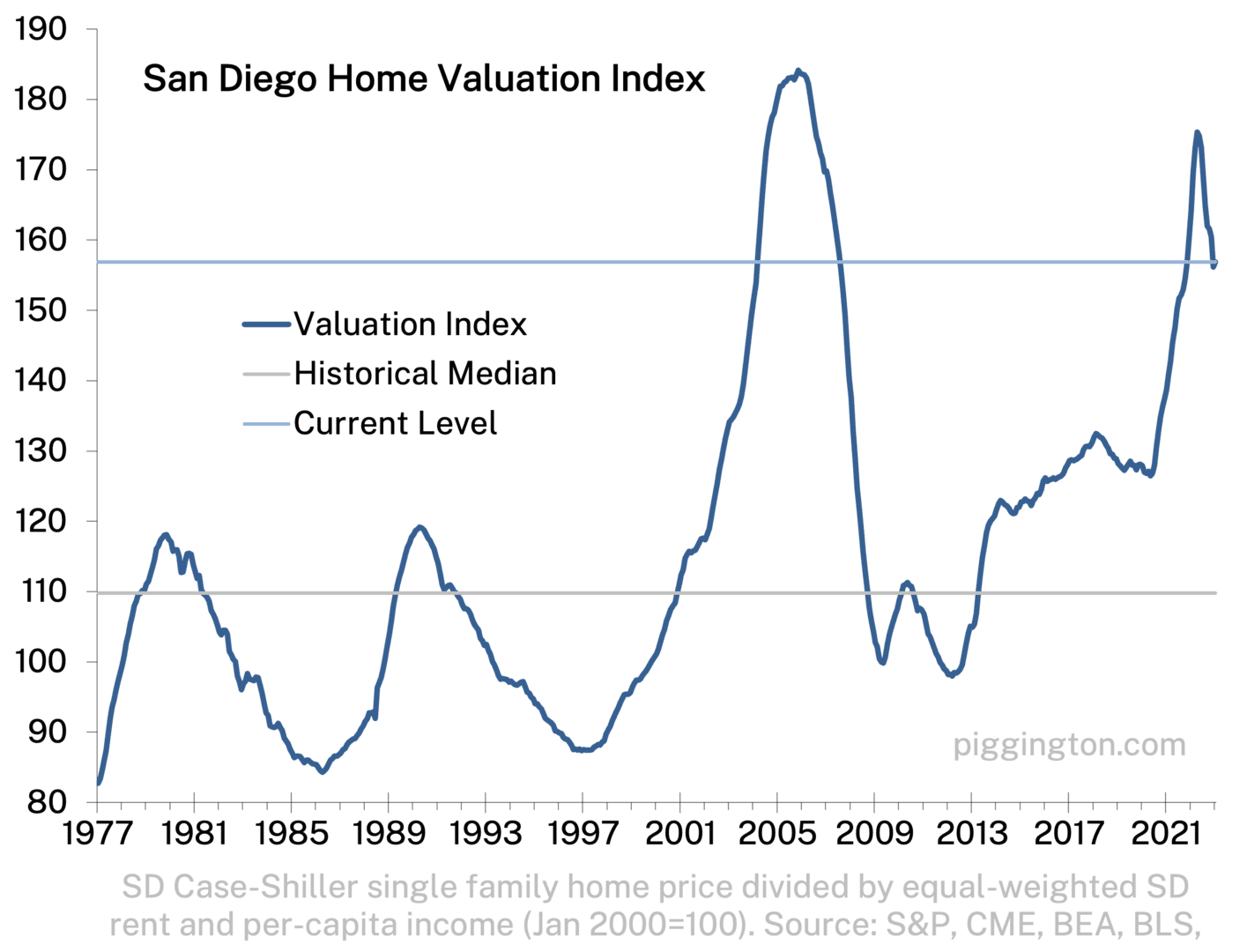

This first chart shows the ratio of home purchase prices to a combination of rents and incomes. That boost in valuation has made a very rapid turnaround since it peaked last spring, but it has only retraced about 40% of its post-Covid surge.

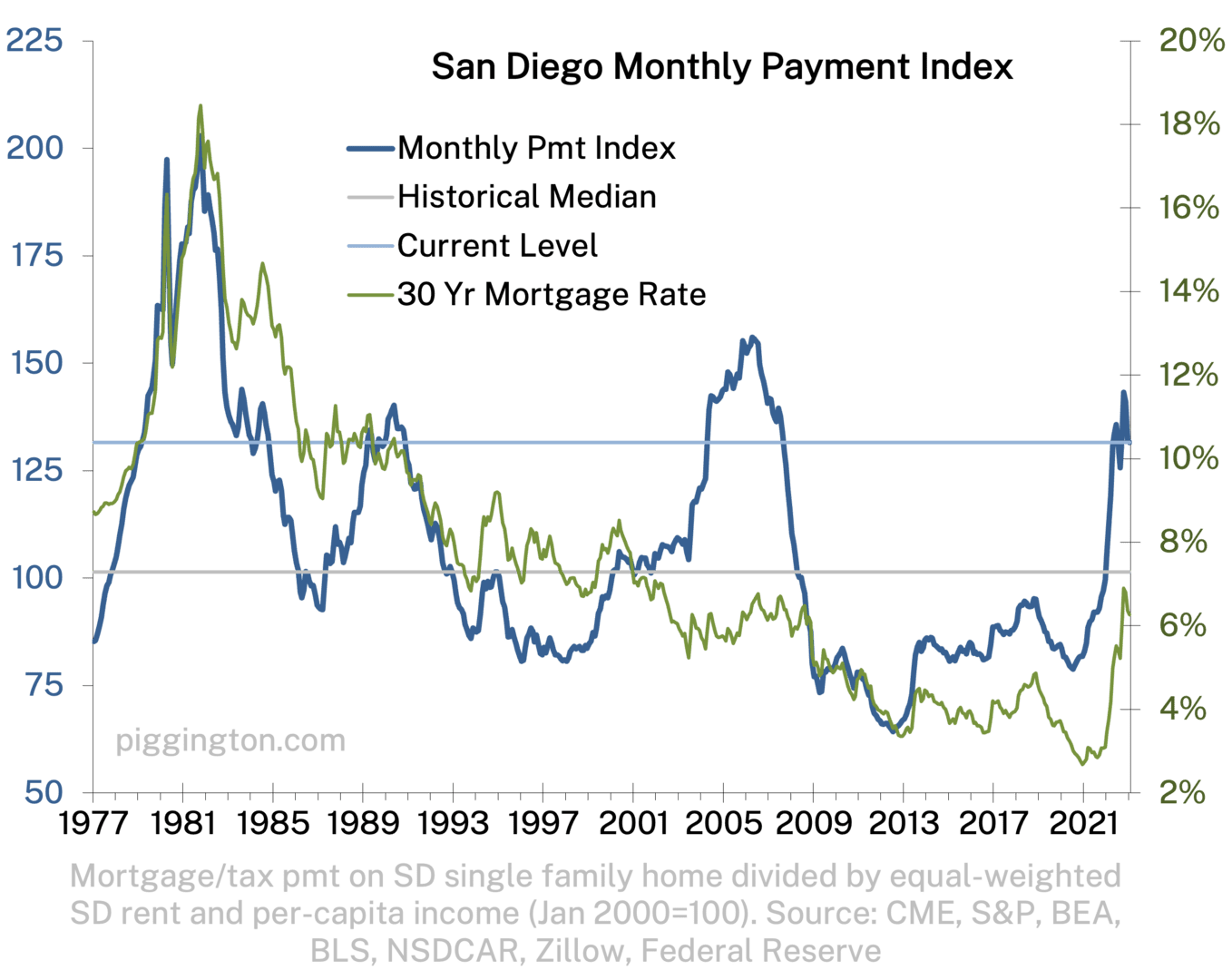

The second chart shows the ratio of home monthly payments to rents and incomes. While off the recent highs, this proxy for monthly payment affordability remains quite uncomfortably on the “unaffordable” side of things. (Un-fun fact: this ratio has increased by 67% since the post-Covid lockdown low point in July 2020).

Here are some potential outcomes, in descending order of how likely I think they are to happen:

- The monthly payment index will decline. This seems pretty likely, because I just don’t think this level of monthly payment affordability is sustainable.

However, this is not a particularly useful forecast, because this could happen via any or all of the following: rising incomes/rents, declining prices, or declining mortgage rates. We’ve already seen a decent amount of the first two, and now, a tiny bit of the third. All three are likely to continue playing a role, but the proportion of each is, I think, highly dependent on economic developments (which I believe to be very hard to predict with any reliability).

- The valuation index will decline further. I also see this as pretty likely, but I’m less confident of this one than the prior one.

I think it’s likely to happen because the only times valuations got to this level, there was something “special” happening. The first time was a huge speculative bubble, and affordability doesn’t matter during bubbles, at least for as long as the party keeps going. The second was a dramatic decline in interest rates that kept monthly payments reasonably affordable despite the high purchase price valuations. Without a special factor like that, I would expect valuations to return to more normal territory over time.

I am less confident about this outcome than the prior one because I’m allowing for the possibility that rates drop substantially enough that monthly payments become affordable again. (That’s not my base case, but I don’t want to rule it out, either… see above about predicting such things. And this uncertainty cuts both ways: If mortgage rates were to stay here or even go higher — also not my base case, but also not unthinkable — valuations would have to decline even more than I am expecting to get payments back into line).

- Nominal home prices will decline further. This seems likely to some degree, but the extent of it is highly uncertain in my view. This is because it could be headed off not only by much lower rates (as in the last bullet), but also by an increase in rents/incomes that is large enough to allow valuations to normalize without prices coming down too much.

Duration becomes fairly important here… given sufficient time, the inexorable rise of rents and incomes could lower valuations quite a bit without prices moving at all. But if the adjustment is to take place more quickly, it seems likely that price declines would have to do some of the work. Which of these paths is taken is anyone’s guess. But I do think that a recession in the near term would increase the likelihood of nominal price declines.

My view that price declines are “likely to some degree” is based on the fact that mortgage rates are still high, and the move towards greater affordability has happened pretty quickly so far. That implies some degree of downward price pressure, but that could change (and based on the lack of inventory hitting the market, it may already have started to change) — so it is a weakly-held view.

And so the shambling, or lurching, towards affordability seems likely to continue… but how this might be accomplished is much less certain.

Thanks, Rich! I was thinking about asking for an updated valuation post after unemployment unexpectedly dropped in January. Saw a few news articles predicting more fed rate increases this year, which will pull mortgage rates up with it. It’s looking more like wages and nominal prices will meet somewhere in the middle.

Question for Rich. What period does the historical median represent and why was that period chosen? Was it for some specific resaon or just because that is how far the data goes back? It would seem that the way the market behaved before and after around 2000 is very different when one looks at the historical data.

That’s how far back the Case-Shiller data goes, 1977. The median is just the median over that entire history. It’s just there for reference, not to suggest that it’s the “right” level or anything.

Thanks for clarifying that

What is the “right” level? I wonder if there is a blended average of price/interest rates where we see the market come into balance. Of course you’d have to make an assumption of what that is, 2 months inventory, 6.

Josh

“What is the “right” level?”

I’ll let you know in 30 years…

My bearishness is growing daily.

Like most owners with locked in low rates and property tax, I would never sell. But I still like my zestimates to go up.

California’s Prop 13, high construction costs, and state level cap gains really holds back supply. But when I look at other sunbelt areas like Austin, inventory is surging and looks like some serious additional price declines are in the cards.

Can we have 7% mortgage rates and 11% car loans and not have a recession? Probably not. The tardy and long awaited China Reopening is good for demand but will fuel inflation.

I added to my RE shorts. Reshorted BXP after covering a while ago, added to AVB.

As general recession shorts, I shorted TSLA, WING, WMT, and TR. Also SPY puts.

I am not a fan of all these new suburban infill state laws. But they always seem to be more scary in theory than practice. Anti-developer city govs and zoning definitely do hurt supply. However, high construction costs and now high finance costs are bigger problems. Construction employment is just not going to go up enough to significantly increase new RE supply. And the YIMBYs can’t help themselves, they put burdensome affordable housing mandates in their “deregulation” laws.

I think the old assumption 6 months of inventory is a stable market is no longer valid. The invention and access to web search tools has lowered the friction in the market and decreased search times. When a buyer can drill down to an area and neighborhood in 1 hour versus 4 months of house tours and scouting the friction is less. You can additionally research schools, restaurants, activities with the internet and understand the area much better than when that 6 month metric was coined 30 year ago. I would estimate stable supply for San Diego is around 2.5 months and anything over is a glut and prices will drop. This market is going to get crushed. It takes 3 doctor salaries to afford the median priced home with 20% down. Sell sell sell, buy back at 50% off when it gets foreclosed on in 3 years.

The problem is there are not and won’t be excessive selling. If i sold and bought back at 50% peak values my taxes would still be nearly double what they are. Id have to pay taxes on a capital gain of more than $1m. I’d have to move and I hate moving. I’d have to rent some place not as nice. There are so many problems with your suggestion. I’ll just stay here, that’s fine takes. And stay off my lawn!!!

The math doesn’t work this way. Just because people can spend less time finding a home doesn’t mean that there will be more homebuyers per month coming into the picture, or more sales per month. it just shifts the the sales to an earlier month.

I agree that 6 months of inventory is not correct any more… over the past decade, the equilibrium level seems to have been about 2.5 months of inventory (whatever the mechanism for that shift may be). See chart below.

However, the leap from that fact to making a bearish forecast is inexplicable to me. If indeed equilibrium supply is 2.5 months of inventory, that is neither bearish nor bullish… it is just a statement how the market functions. (If anything, the fact that Jan inventory was below equilibrium is short-term bullish).

Maybe it does work that way because houses don’t linger as long. My intuition has always told me that the change in months of inventory coincide with price changes more than the absolute months of inventory. Meaning – if prices are stable, months of inventory could be stable at 2.5 months of inventory or 6.0 months. Seems like Rich ran those numbers once and proved my intuition wrong. I wonder if you include the times when 6.0 months meant “stable” and now when 2.5 months means stable then it would come out differently.

And the bottom line is so few are selling that it doesn’t matter. Ok prices drop. Good luck being the guy to get the one house that is for sale

March, April and May are traditionally the peak listing counts each year. Not looking that way. So very quiet

[…] More charts below, and for some thoughts on the longer-term outlook, please see the recent valuation update. […]

[…] further immediately ahead. But inventory is weather, not climate (see the second graph). FWIW my long term view continues to be that this level of affordability is not […]