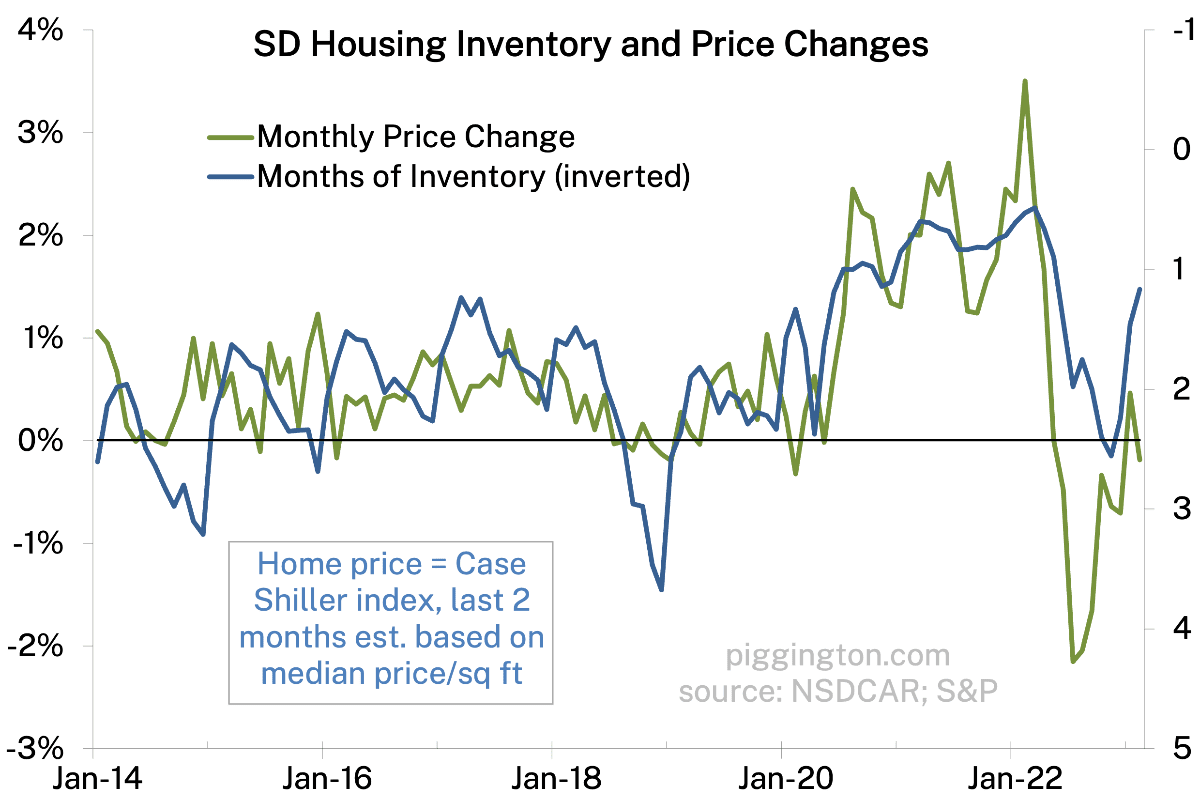

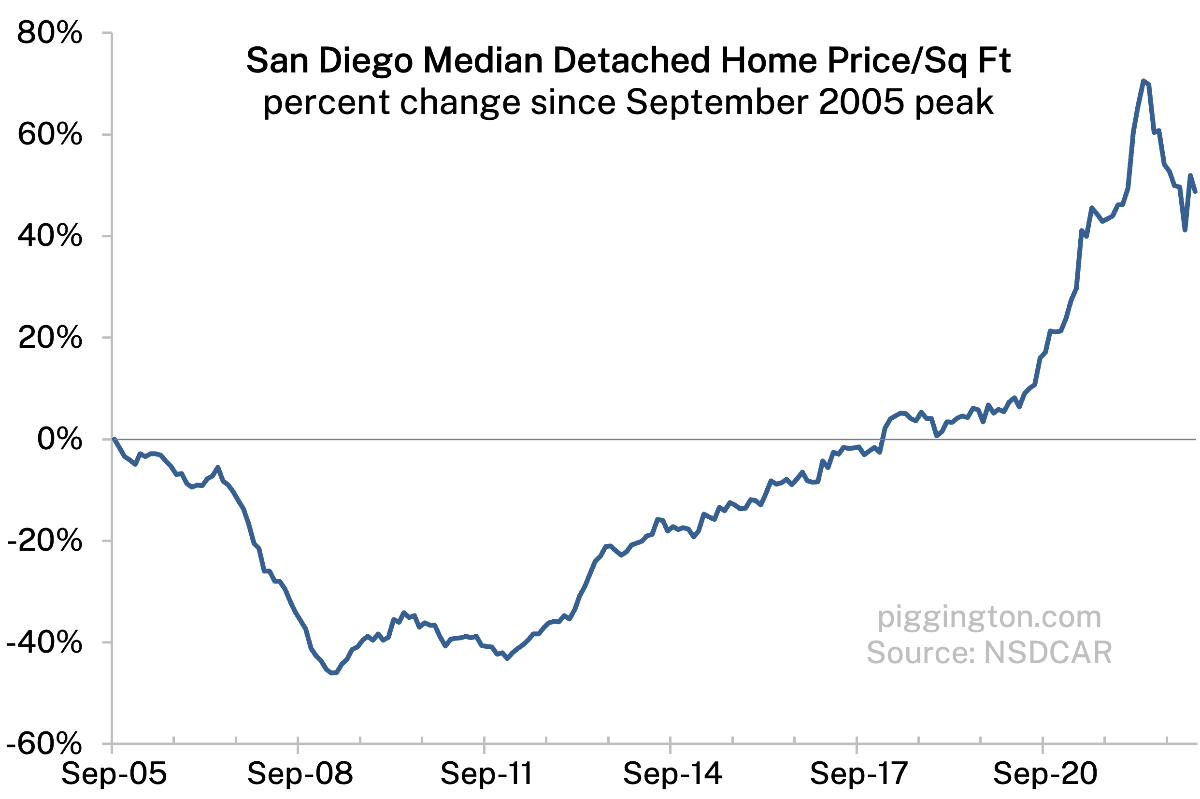

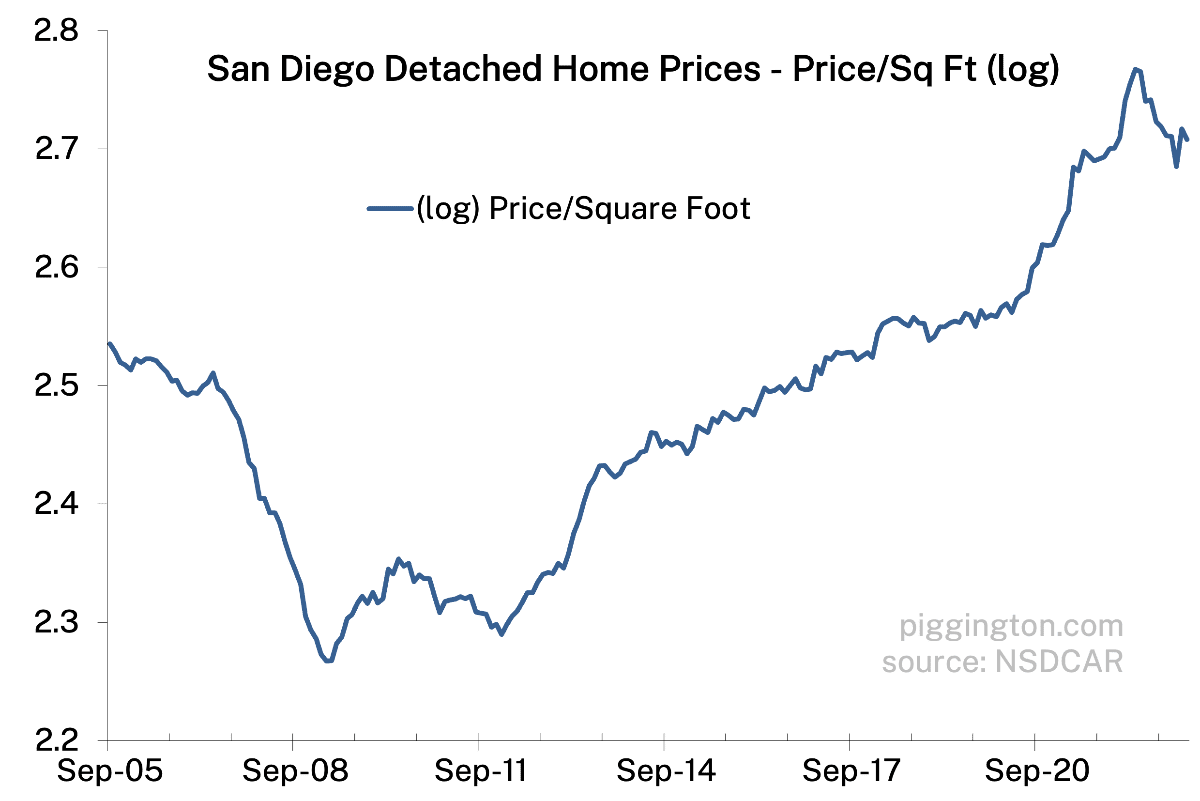

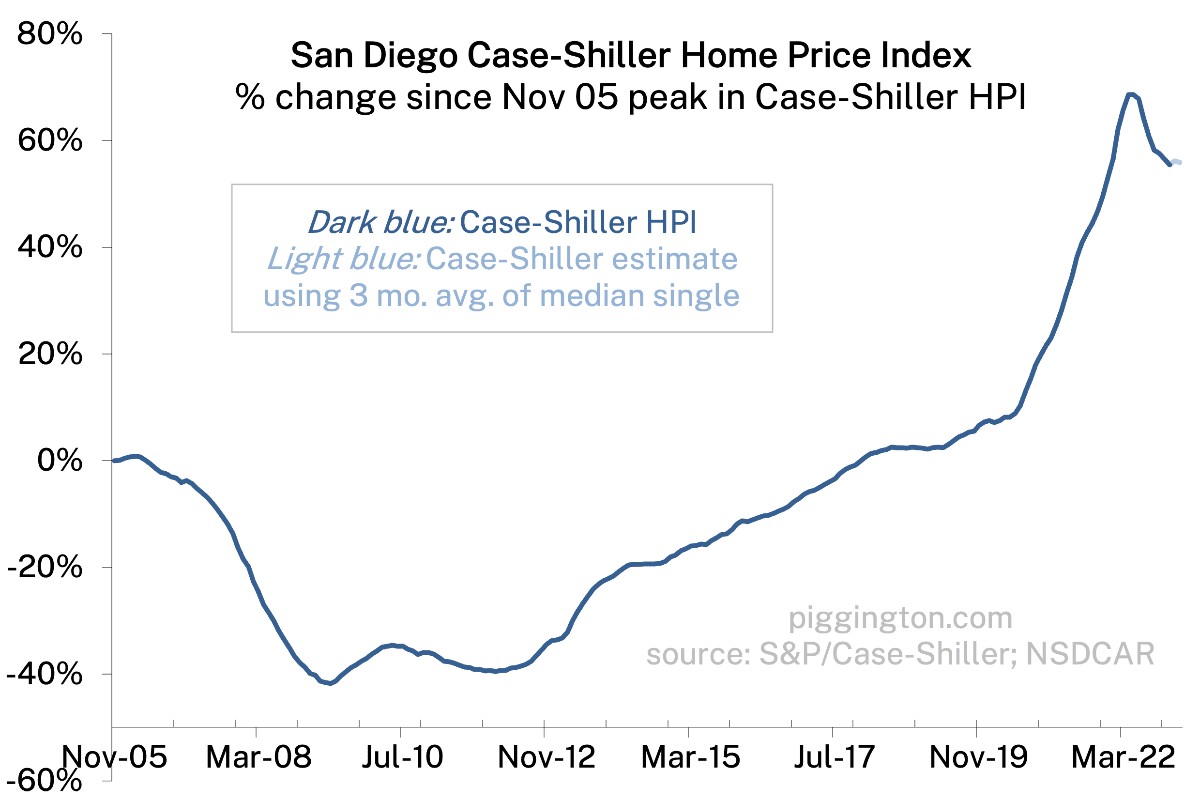

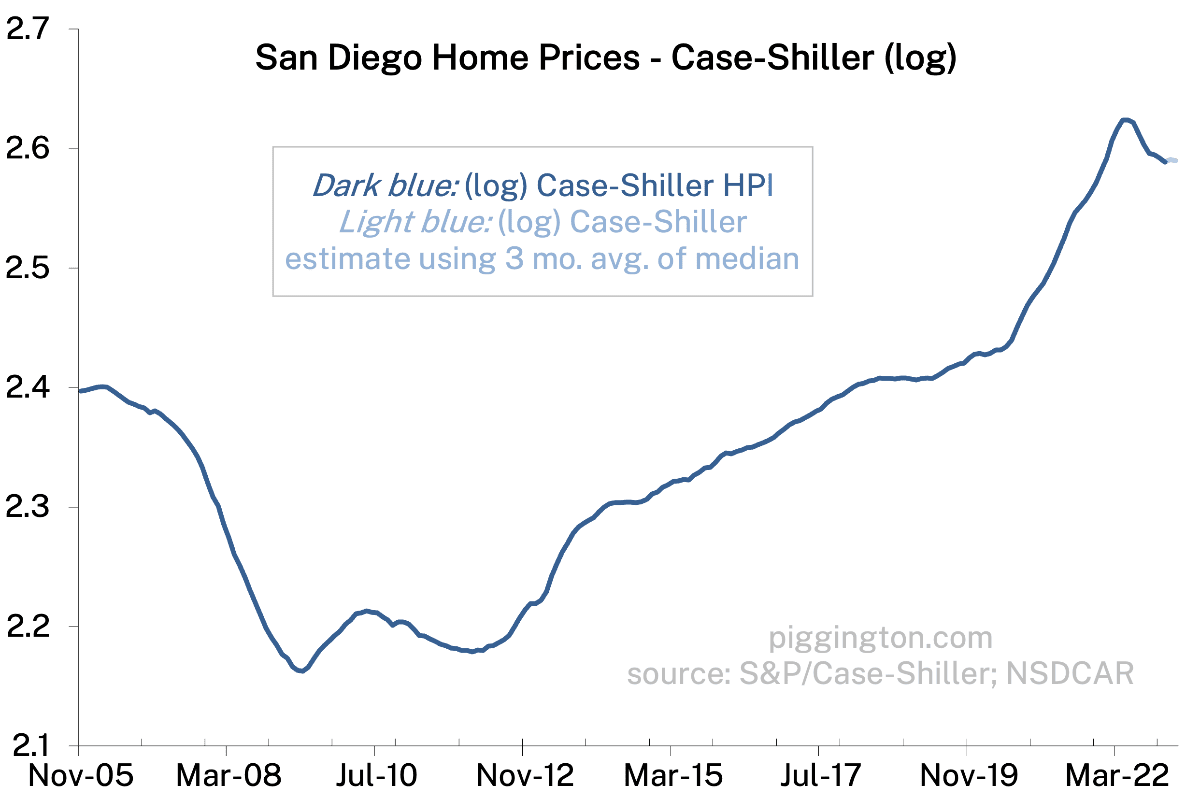

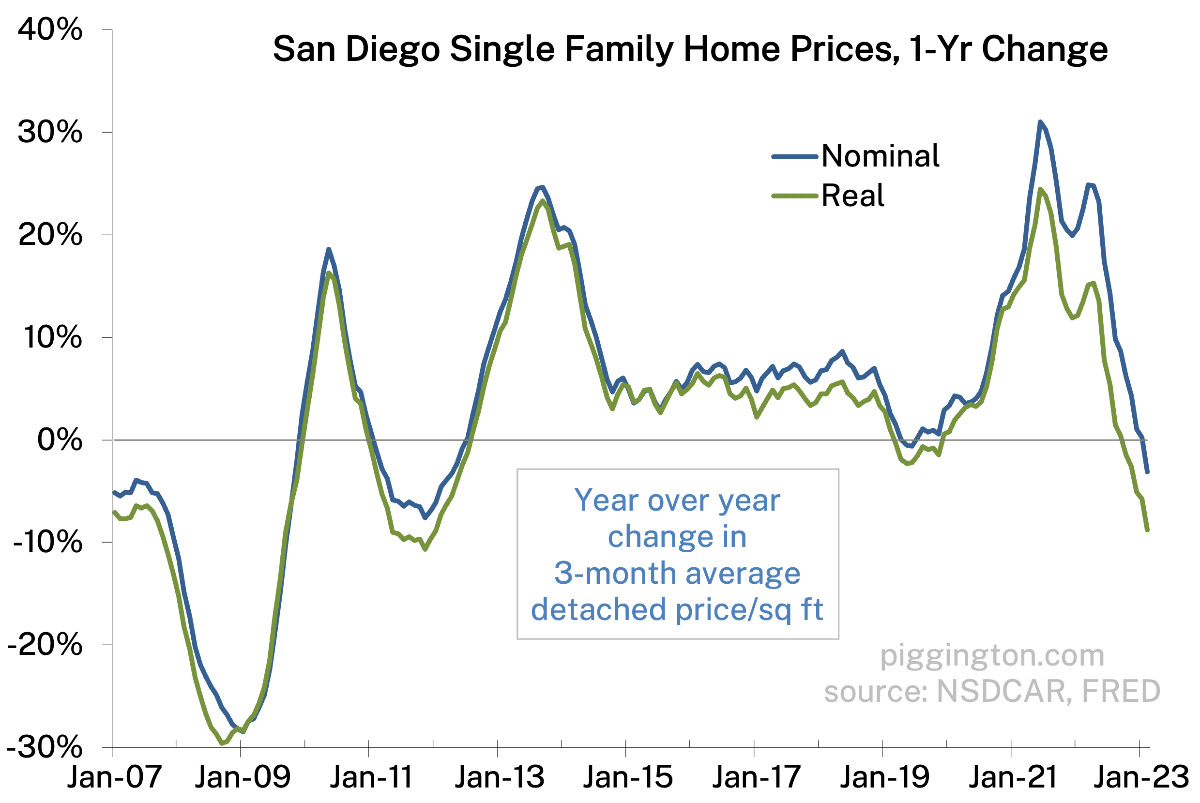

Well, prices backed off a bit after last month’s whipsaw, but the smaller move suggests some stabilization.

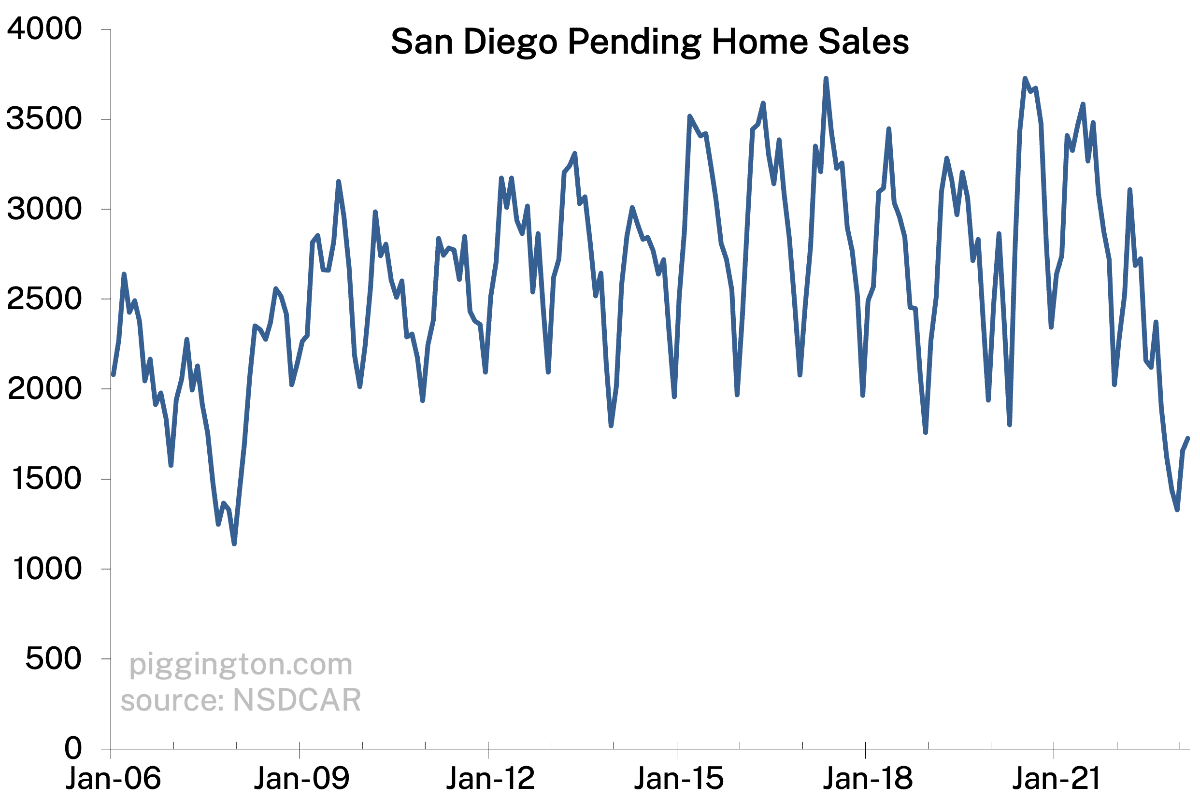

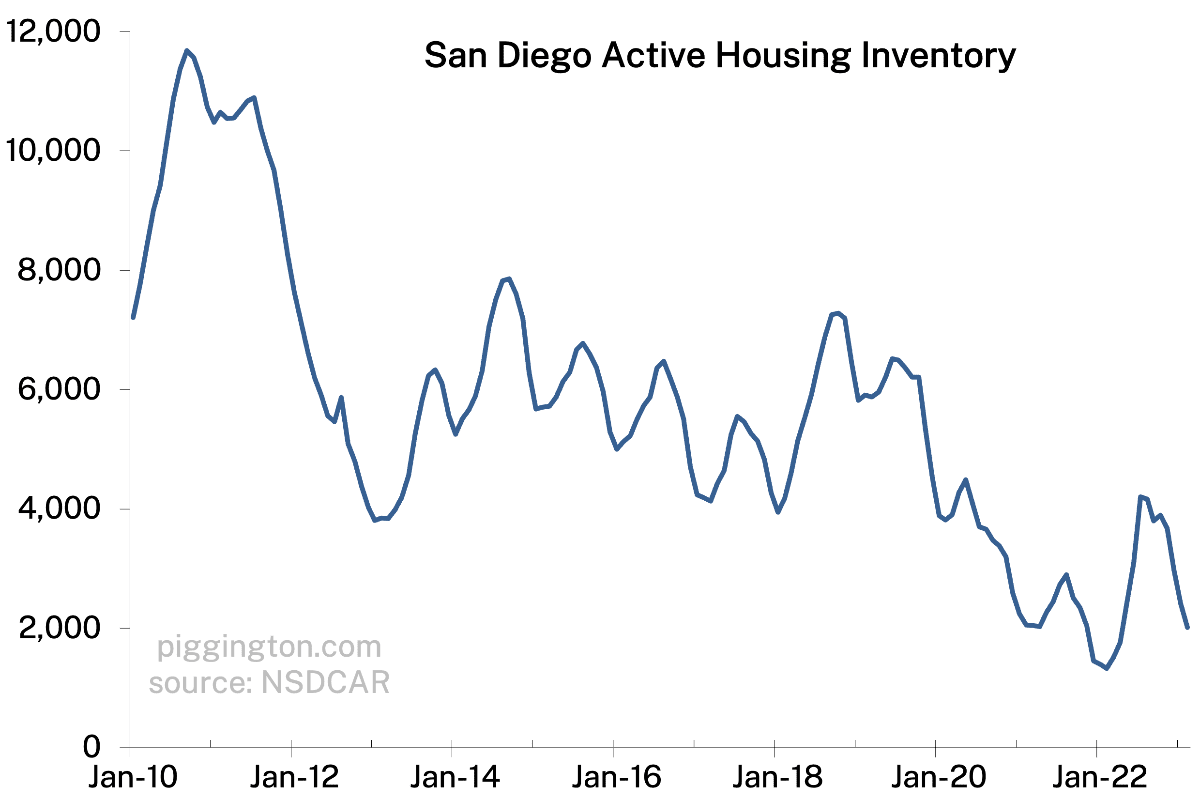

It continues to be a bit of a standoff, with extremely low demand (first graph) meeting extremely low supply (second).

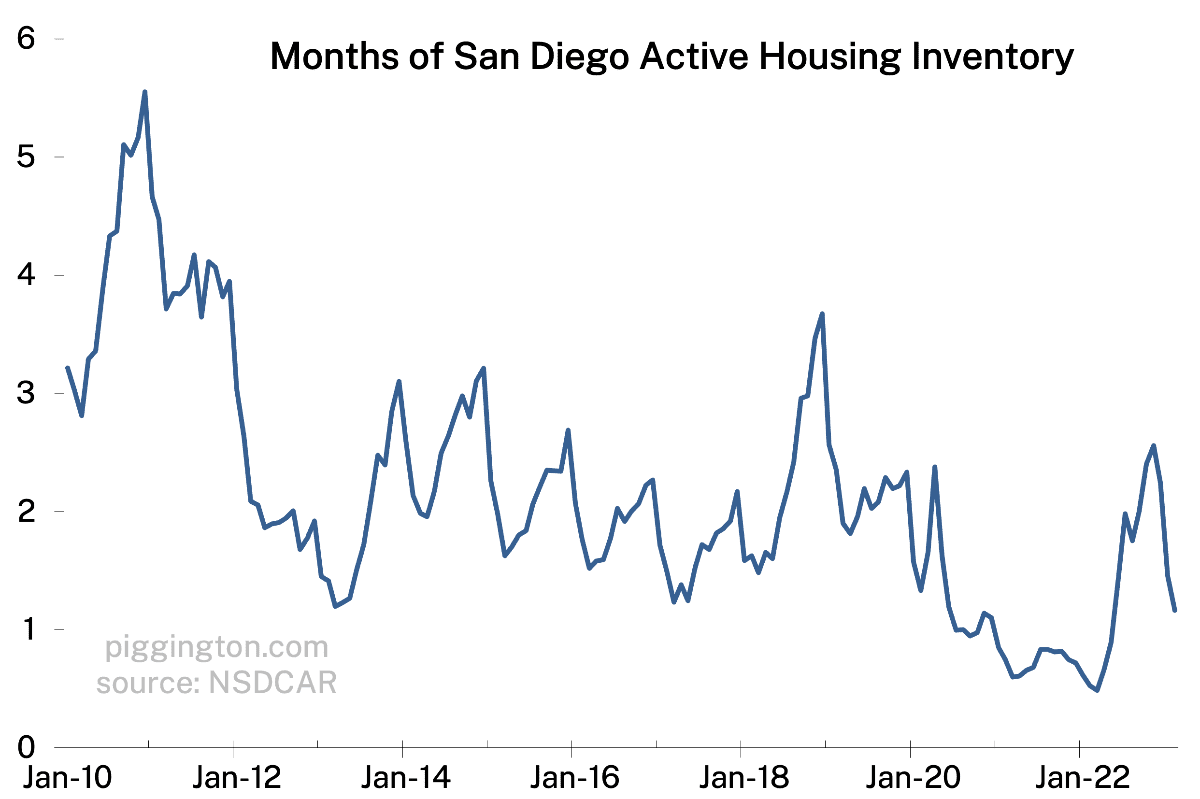

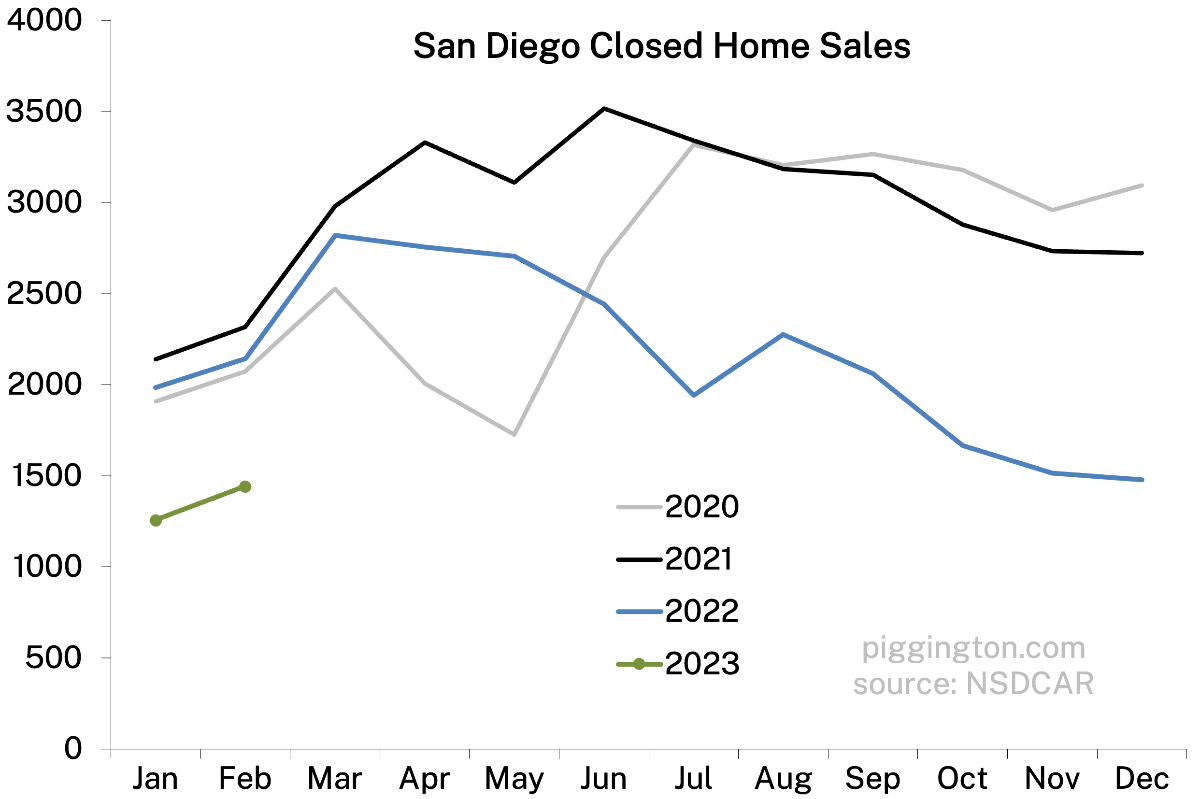

However, the sellers seem to be gaining ground as months of inventory has declined back to the bottom of its post-GFC/pre-Covid range:

This level of inventory suggests that prices could strengthen immediately ahead…

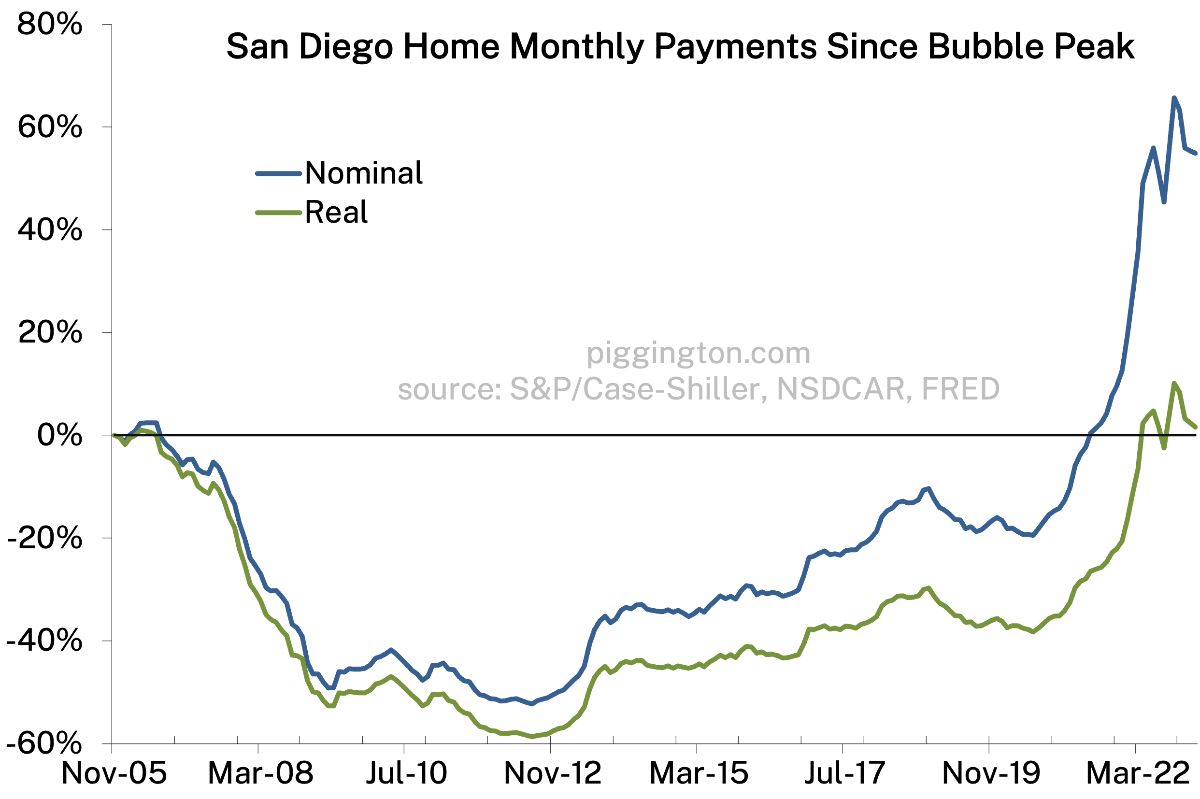

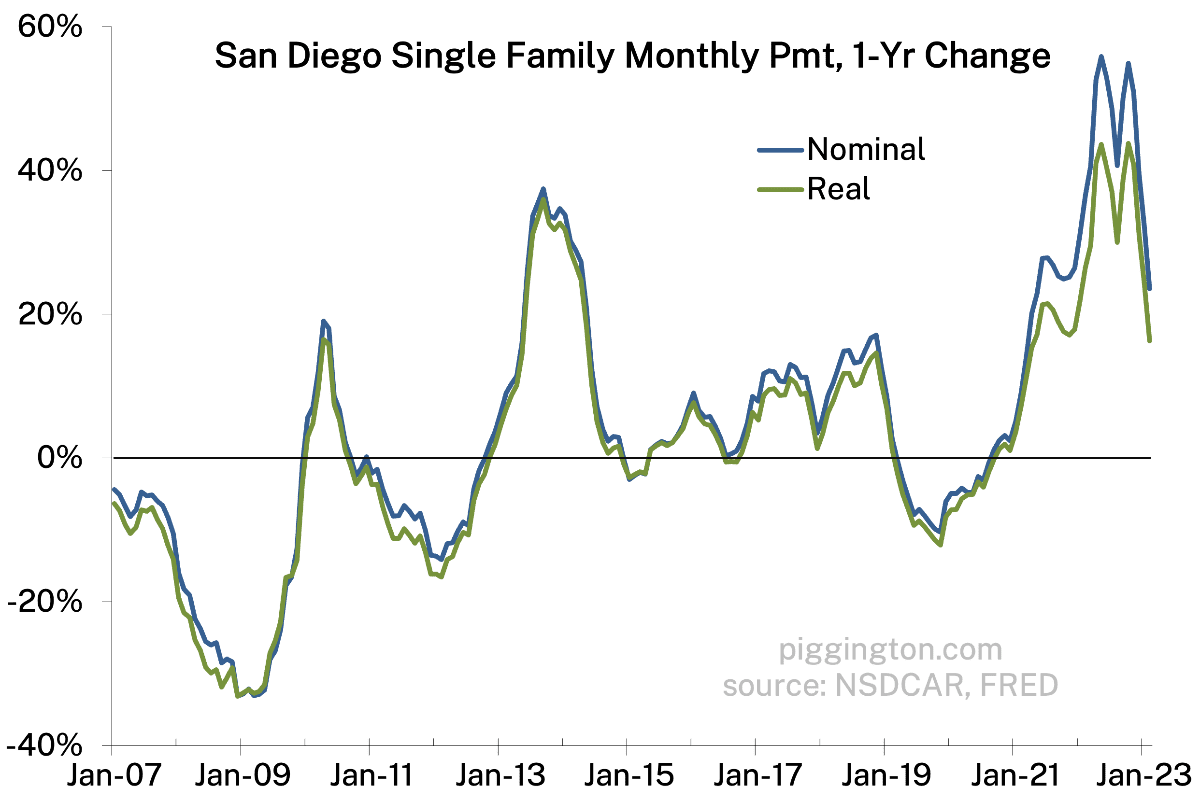

…despite the fact that affordability is absolutely abysmal:

More charts below, and for some thoughts on the longer-term outlook, please see the recent valuation update.

Happy to see the prices stable despite 7% mortgage rates.

We may avoid further nominal price decreases because so few people want to sell. I just saw a chart showing existing first lien mortgages by rate. Half of the US is locked in at 3.5% or lower, and another 20% 3.5-4.0%.

The economic loss of giving up a $500k mortgage locked at 3.5% when rates are 7% is at least $300,000! Think about it, the additional interest is $17,500. The precise way to get a PV of that depends on a lot of assumptions like future rates and remaining loan term. But 300k is going to be in the right ballpark.

When you factor in the loss of a low property tax valuation, and then also add in capital gains taxes, it is just crazy to sell appreciated California homes with locked rates unless you are truly desperate.

Looking at the market for mortgage points, my 300k estimate is too high. The cost to buy down a 7% zero point 500k purchase loan down to 5.5% is $21,000. That’s about as low as you can go, as the cost increases exponentially. There’s also a wonky reason that the point market underestimates value: the market for 5.5% prime loans is more liquid and preferred to the brand new 7% prime loan market. There’s also a still a decent chance you do an early payoff of a 5.5% loan, but much less than for a 3.5% loan.

175 or 200k is probably a more reasonable estimate than 300k.

May prevent nominal declines? Have you not been paying attention to the data Rich and I have been posting the last several months? That’s exactly what has happened

If you look at what I said, it was “may avoid further nominal price decreases” not a denial that such declines have already occurred.

gotcha and I dont think it is a may avoid going forward either. Sellers have already demonstrated on masse there will be no large scale liquidation. There will always be sellers (pretty much every new listing in MM lately is because someone died) but going forward we have to live with a lot less of them. There could and should be some more nominal declines but as I opined many months ago most of the nominal damage was swift and sudden last year with not much more to follow. I beleive that more than ever today. This Fall the window of opportunity should be close to the best we will see for the next few years.

SDRealtor,

I would love to hear your thoughts on why the 3-Roots Development in Mira Mesa is totally defying price decreases. In fact prices have continued to rise in this subdivision for past year.

For example Phase 1 Atwood sold for $700,000 and closed in June 2022. Phase 8 Atwood just sold for $875,000 last month.

I just saw a listing go pending on 10553 Coupland way go pending at $975,000 (prob will end up selling for less) but that guy closed on that unit in like July at the height of the price bubble for like mid 700’s so the guy made a profit of prob. 200K after living there less than a year during the “crash”.

Thoughts?

Seems like they were underpriced before. Very good location near many high wage jobs, high end new construction, low HOA.

The June/July 2022 closings there could have been priced and under contract in early 2021.

People will always pay a premium for new homes. There havent been new homes built in that area for decades. Over that time the tech/life science sector has boomed. There is massive demand for new turnkey homes from high wage earners in the area.

And gzz is correct those closings last Summer were likely put under contract at prices in late 2021

If you work for Google in Sorrento Valley, Amazon in UTC, Dexcom in Sorrento Valley, or the many other biotech companies in Sorrento Valley and want a brand-new house within 10-15 minutes door to door commute, you only have one choice. Also, 3Roots was priced originally, IMHO, based on MM’s pricing. So, in hindsight, it looks like 3Roots was underpriced, as gzz stated.

You can see comparable price appreciation with Alta in 3Roots. It started out at $1.6m, first ones in in 92126 at that price range. So, no one really knows if people are willing to pay $1.6m for homes in 92126. The development closed at over $1.9m. With upgrades and landscaping, those homes end up over $2m for sure. That’s unheard of in 92126.

I think with financial institutions starting to fail, interest rate hikes having to end in sight, and the beginnings of increasing unemployment, its only a matter of time before a load of current homeowners that bought on the edge of their budget are forced to capitulate. I read that the median income of buyers dropped sharply during the pandemic, so there are for sure a large amount of people that bought houses that they can barely afford IMO. Unemployment spiking could be the match that lights the fuse of a major downturn in prices…

Yep, next week should be interesting. We will see if ZeroHedge’s prediction that layoffs begin as soon as Monday at startups that banked at Silicon Valley Bank (SVB) comes to pass. What a shock, to suddenly have no access to your company’s cash. I was CFO at three medical device startups, and banked solely at SVB; I cannot fathom the worry and pain those startups are facing, overnight.

Well, Yesterday Yellen said there will be no bailout and this is a one-off. Today, a second bank failed (3rd largest in history, SVB is #2, WaMu #1) and the feds are now guaranteeing all deposits for SVB customers.

“Oh no not again.” -a bowl of petunias, probably

30 year rates peaked at 7.1% on March 2. Now 6.57%.

Good deal for lenders, that’s 3 percentage points higher than 10 year treasuries.

I haven’t looked at OB/92107 sales lately, but just did today. Wow, the market is still very strong. One pretty average meh house after another above $1000/sf.

While we technically are below peak prices, the peak was so brief it didn’t really sink in or establish a lot of comparables. So it still feels like peak pricing and much higher than 2020-21.

It really is astounding. I keep checking the days expecting inventory to start flowing in. I expected sellers to dig in but what is happening far exceeds what I thought possible. Looking at data around the country it’s happening all over but SD seems to be leading the charge more than anywhere else.

I wonder if conversion of dying commercial real estate to residential will shift the market?

In DC the commercial real estate sector is looking at a 50% loss of value. I’m hoping that many of these flailing properties will become “Loft” style apartments. Old warehouses and industrial facilities were converted into residences and restaurants, no reason why old office buildings won’t. The top floor of an office building would make a banging disco or restaurant.