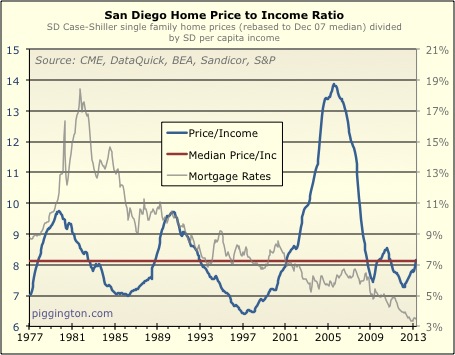

I recently updated the price-to-income

and price-to rent-ratios for San Diego single family homes.

I think these are the best metrics to determine whether homes are

overpriced or underpriced based on their fundamental economic

underpinnings.

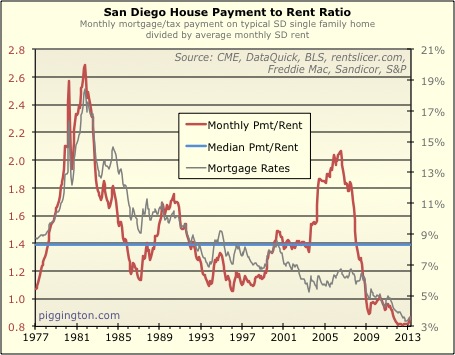

It’s also interesting to look at the ratio of monthly payments

to incomes rents, but for a different reason. I’ll get into

this in a moment, but first let’s check out the graphs:

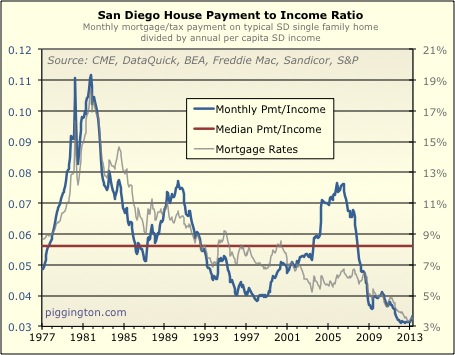

The recent price increases have just been a blip compared to the

incredibly low level of interest rates. The payment-to-income ratio

is 41% below the historical median, and the price-to-income ratio is

38% below it.

In my view, it is erroneous to use these graphs in support of the

argument that “housing is cheap.” The payment-based ratios

combine home prices and mortgage rates to tell you how good a deal

you are getting by financing a home at that particular time.

But if the question is whether homes are cheap or expensive on a

long-term, sustainable basis, interest rates don’t really figure

into it in my view. Rates can go up and down over time, but it

is incomes and rents that will determine how much houses are

intrinsically “worth.” I guess another way to put it is: low

rates help, but only for as long as they stay low. (And when

they have nowhere to go but up, one could even argue that that is a

source of potential downward pressure on prices in the future).

Just to emphasize the point — according to the payment-to-income

ratio (if one were to try to use it as a valuation metric), houses

were more “expensive” in 1985 than in 2006. In fact, the price-to-income

ratio shows that housing was dirt cheap in 1985, and absurdly

overvalued in 2006. (In case the below graph isn’t convincing

enough, consider the subsequent price changes in each case).

So the payment-based ratios don’t justify the view that houses are

cheap. However, they do tell us that if you are financing a long-term

home purchase with a fixed-rate mortgage, you are pretty much

getting the deal of a lifetime.

Agree that a homebuyer is

Agree that a homebuyer is getting the “deal of a lifetime” if they finance their home purchase today. But they STILL have to pay the outstanding balance back when they sell and if they take out an FHA/VA loan (96.5% to 100% LTV + any financed MIP or funding fee), they could very well find themselves upside down if mtg rates even go to ~7% at the time they end up in a situation of having to relocate/sell.

For this reason, I still don’t think it’s a good idea for an active duty servicemember and their family to purchase a home in San Diego if they have at least five years left until retirement as they don’t have much (if any) control over the fact that they will likely have to transfer to their next duty station in 1-3 years. It is wiser for them to take the (now gargantuan in CA coastal counties) housing allowance offered to them and rent.

This is, of course, presuming that mtg rates go to 7% in the next five years or so (poss unlikely).

If there is still any discount at all in this market for cash buyers, then it is still worth it to pay cash, IMO. If there is no longer a customary cash discount due to high demand, then it is only worth it to pay cash if the cash buyer wishes to buy now and an all-cash offer is the ONLY way to “win” in a multiple-bid situation, the cash buyer is retiring or retired and cannot get financing and/or the property is not eligible for financing (ex: heavy fixer).

I’m surmising that cash discounts may only only customarily apply to some submarkets in the county but not all.

*************

Rich, thank you for pointing out with your graph that buyers in past generations did not have anywhere near as good of a house-payment-to-income ratio as today’s buyers do, using your “1985” example. I’ve been saying this here for years as well as stating here repeatedly that “professional” buyers raising families in the ’80’s bought what they could afford in the area they could afford to live in.

I can assure everyone that this was a far more modest house and area than today’s buyers of lesser (relative) incomes would even bother to drive by or shop in.

I’m still shocked at how picky young FTB’s and STB’s are today when it comes to housing and area. If MIR’s were in the normal 7%-10% (as we boomers had to contend with from abt 1983 forward), today’s buyers wouldn’t be able to afford to be so picky. They would be forced to accept what is available is their price range or rent. It is the artificially low interest rates for about ten years now (plummeting even further in the last 4 years) which have driven up RE prices as well as continued to enable buyers’ extremely-high housing expectations to be met.

The only downfall I see to this phenomenon is IF prices should stop rising and even fall a bit in areas where inventory is more plentiful in the future and those buyers HAVE to sell, they may not be able to get the price they paid plus closing costs and the money they put into the property because their purchase price in 2013 was predicated on the prevailing low MIR’s at the time.

The 2009-2010 buyers will probably be okay in this regard.

It’s going to be interesting to see how this all plays out in SD County in the coming years. It is entirely possible that the popular established areas will continue to be dominated by all-cash buyers from here on out. If this ends up being reality, I feel we will see an exacerbation of the abyss between the two factions of homeowners here …. the encumbered and the unencumbered. This doesn’t bode too well for the future values in those newer subdivisions which 90%+ of young-buyer families seem to be attracted to like bees to honey and also in which 90%+ of sales are financed, IMHO.

Thanks for updating

Thanks for updating Rich.

Regardless of whether price to income is a better metric than monthly payment to rent, the latter metric clearly shows that the most recent housing bust has been the most favorable time to buy rental property in San Diego since 1977 (in terms of cash flow).

… assuming fixed rate mortgage is used of course.

Those graphs certainly do

Those graphs certainly do make housing look fairly cheap. What’s odd is that our neighborhood is seeing peak prices…and higher! It just feels awfully bubbly from where we sit.

Of course, as you’ve already noted, the PITI/rent ratios have been favorable for buyers with fixed-rate mortgages and plans to stay for the long haul. There is no doubt about that, which is one of the main reasons we bought when we did.

Thank you so much for your work, Rich!

CAR, that’s where these

CAR, that’s where these graphs break down a bit; they lump the whole county together when there can be large disparities between different areas in both incomes and prices (both of which have likely gotten worse as general wealth inequality has gotten more pronounced).

But you are right that the payment/rent ratios are probably good no matter where you go…

It seems we’ve replaced

It seems we’ve replaced interest only loans with principal only loans. People are using these “principal only loans” as affordability products to buy more house than they could if they had to pay interest.

My math has the payment on a $400k loan jumping from $2,315 a month to $3,739 if rates moved from 3.5% to 9%. Front end DTI jumps from 28% to 45% which basically means you no longer get that loan assuming $100k income.

In 1995 rates were 9% and yet and payments were low relative to income. How was that possible given that it would decimate the current market? Because prices were low relative to income in ’95.

I would much rather buy when prices are low and rates are high and then refinance during the next recession rather than buy when rates are at record lows and prices are high, monthly payments be damned.

It’s counter-intuitive but it might make more sense to buy a smaller home when rates are low so you’re able to relocate if necessary when rates increase. Of course that’ll never happen which explains why used car dealers ask you how much monthly payment you can afford when buying an old Camaro.

Rich, you need interest rates, price to income, and payment to income on one graph to really see this. And I’ll admit that rates may never top 4% again, but that didn’t seem to help home prices in Japan.

mckirkus wrote:

I would much

[quote=mckirkus]

I would much rather buy when prices are low and rates are high and then refinance during the next recession rather than buy when rates are at record lows and prices are high, monthly payments be damned.

[/quote]

That is a great plan. The only problem with it is that those conditions (low prices, high rates) existing for about 2-3 years once, maybe twice in the last 42 or so years.

So, one could wait 10-20 years or more for such conditions. It’s not really practical other than an academic exercise. For any particular individual, they are likely better off in the long run if they buy when they are capable and just avoid the few periods of extreme peaks of the market (2003-2006 for example).

In a similar vein, studies show that workers lifelong salary is higher if they enter the workforce when unemployment is low. That does not mean that an individual ho graduated in 2008 would be better off waiting out the 5-10 years it takes for unemployment to drop below 6%.

mckirkus wrote:It seems we’ve

[quote=mckirkus]It seems we’ve replaced interest only loans with principal only loans. [/quote]

That’s clever; I never thought of it that way.

[quote=mckirkus]I would much rather buy when prices are low and rates are high and then refinance during the next recession rather than buy when rates are at record lows and prices are high, monthly payments be damned.[/quote]

It depends on your goal. If you are more worried about price appreciation, that makes sense. But if you are buying a “permanent” place with financing and are more worried about getting the lowest possible monthly payments, it may be better to just buy when rates are low. (I described this thought process in my “piggington jumps the shark” article last year).

[quote=mckirkus]Rich, you need interest rates, price to income, and payment to income on one graph to really see this.[/quote]

Good idea… I will add it to my to-do list.

Rich Toscano wrote:mckirkus

[quote=Rich Toscano][quote=mckirkus]It seems we’ve replaced interest only loans with principal only loans. [/quote]

That’s clever; I never thought of it that way.

[/quote]

Agreed. That was a great way to describe the current mortgage/housing market, mckirkus.

IMO U.S.A. Rates will not

IMO U.S.A. Rates will not rise much until there is significant wage inflation to compensate.

If the fed raises rates I think they will have to reverse course very quickly when everything goes south in a hurry.

I could be wrong but I Think it will be a very long time before we see 8 percent or greater Mortgage rates.

Also

Japan’s real-estate bubble was much larger than America’s. And its demographics are far worse;

So really there is no comparison between Japan and the USA real estate bubble fallouts IMO.

I think The housing bubble

I think The housing bubble created a bigger monster than few realized it could (it’s not just prices, it’s the whole package).

from municipalities revenue collection to local businesses to negative wealth effect its all a factor that cannot be overcome easily once the genie is out of the bottle and it was let out in 2004-6.

Just to be a little

Just to be a little contrarian, I think this bubble could potentially be bigger than the previous bubble. This bubble is being fueled by cash offers, REIT’s, and people with deep pockets. Greed can be a powerful oxidant that could cause this rocket to go higher. With the recent dip in the dow, seems to me that reit’s might just be a no brainer at least for now. Now would I bet on it, no, but it could happen. P.S.- Now on a personal note I do feel I got a good deal buying in Feb 2009 (with 3.5% down) and currently paying a 15 year mortgage that is less than Zillow’s rent zestimate.