With recent robust price increases has come a resurgence of talk about a

bubble. Whether a given investment is in a bubble or not may

depend on many factors, but in my mind, the most important of these

is valuations. If valuations (properly measured) do not show

the asset to be extremely overvalued, then you probably aren’t

dealing with a bubble. This is not to say the asset can’t go

down in price — not at all. It’s just to say that it’s not a

proper “bubble.”

So what are valuations telling us about the state of the San Diego

housing market right now? Let’s have a look at the two most

important ratios that have guided us through this boom and bust: the

home price to income ratio, and the home price to rent ratio.

These ratios compare home prices with two real-world fundamental

underpinnings: how much potential home buyers earn, and how much it

costs to rent (put another way, how much it costs to not buy).

Over time they have tended to “mean revert” around a middle of the

road value which we can roughly say represents the fair

value for San Diego housing.

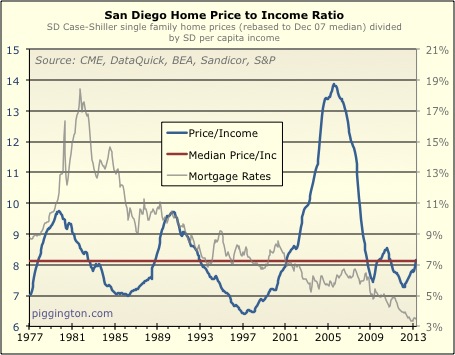

Let’s start with the price-to-income ratio:

As it happens, the current p/i ratio stands almost exactly on top of

the long-term median value (less than 1% above). This surprised me

a bit, given the recent jump in prices. But the last time I

updated this graph at the end of 2011, prices had gotten a decent

amount below fair value. So, prices had a bit to rise to get

to fair value, and nominal incomes have done some of the work by

rising that entire time as the economic recovery has plodded

along.

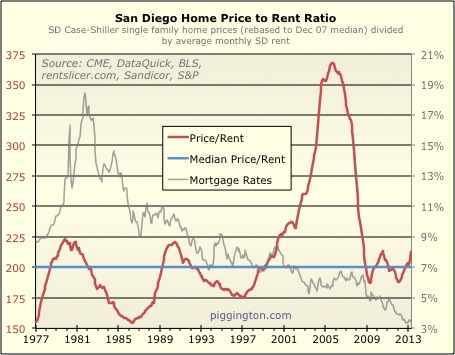

Homes look just a little pricier based on the price-to-rent ratio:

Here, they are 6% above their historical median. This is

actually not terribly far from the p/r ratio peaks in the early

1980s and 1990s, but it is nothing like what we saw during the

bubble in the mid-2000s, when the p/r ratio reached 83% over the

median.

Summing up: the price-to-rent ratio says that San Diego homes are

very mildly overvalued, and the price-to-income ratio says that they

are right at fair value. San Diego homes aren’t cheap, but

they aren’t notably expensive either — and it seems they are still

a good distance from bubble territory.

Next up, a look at the monthly payment ratios…

Finally! Thank you Rich!

If

Finally! Thank you Rich!

If we also consider the interest rates, I would expect housing prices to be quite reasonable when compared to historical averages. Forthcoming monthly payments graphs will likely confirm that.

I always thought that, for

I always thought that, for most people, the best indicators are the monthly payment ratios. However, I’ve recently started to wonder about that.

This is because I think that for most people in the house-buying cohort, their other monthly expenses have gone up quite quickly, leaving LESS available per month for house payments. Some of these other items include the following:

1. School costs (mainly college for their kids, plus student loan payments for themselves or their kids)

2. Health care costs (monthly premiums, copayments, etc, especially as employers try to push more of this onto employees)

3. Food/groceries costs

4. Gas costs

5. Planning for retirement costs (employers have been moving people from pensions to 401(k)’s as fast as possible, at greater costs to these people, especially how much they have to put into retirement savings to recover from the 2001-2002 and 2008-2009 market crashes)

6. Various taxes in the prime I-15 Corridor areas, such as Mello Roos, etc.

I think a case can be made that all the above costs have increased faster than wages since the inflation-adjusted wage peak in 1999/2000, leaving less available than before for house payments (including taxes, home insurance, etc). So yes, a house payment might seem historically reasonable due to lower interest rates. But I think families now would struggle more to make this “reasonable” house payment.

I think the 2004-2007 bubble obscured this deterioration in households’ payment abilities because houses became less a place to live and more and more an ATM machine to help people pay for increasingly expensive living conditions.

Adame99 wrote:

I think the

[quote=Adame99]

I think the 2004-2007 bubble obscured this deterioration in households’ payment abilities because houses became less a place to live and more and more an ATM machine to help people pay for increasingly expensive living conditions.[/quote]

Example always comes down from our beloved leaders:

http://www.latintimes.com/articles/4354/20130523/antonio-villaraigosa-outgoing-los-angeles-mayor-broke-work-job.htm

Adame99 wrote:I always

[quote=Adame99]I always thought that, for most people, the best indicators are the monthly payment ratios. However, I’ve recently started to wonder about that.

This is because I think that for most people in the house-buying cohort, their other monthly expenses have gone up quite quickly, leaving LESS available per month for house payments. Some of these other items include the following:

1. School costs (mainly college for their kids, plus student loan payments for themselves or their kids)

2. Health care costs (monthly premiums, copayments, etc, especially as employers try to push more of this onto employees)

3. Food/groceries costs

4. Gas costs

5. Planning for retirement costs (employers have been moving people from pensions to 401(k)’s as fast as possible, at greater costs to these people, especially how much they have to put into retirement savings to recover from the 2001-2002 and 2008-2009 market crashes)

6. Various taxes in the prime I-15 Corridor areas, such as Mello Roos, etc.

[/quote]

I think a few were left out such as cable/internet, cell phones, water, and utility costs. Seems to me these are pretty pricey when added together and then added on top of a mortgage.

Rich, and/or anyone else who

Rich, and/or anyone else who might care to comment:

We have friends who are planning to move to San Diego, but have no real “deadline” in mind. An acquaintance of theirs (mortgage broker) has told them that, in the next few years–specifically within the next two–San Diego housing prices may crash to the same lows we saw a few years ago–so they should wait to buy. (This, based upon the bubble territory and consequent volatility of the stock market, etc.)

We have a primary and rental property here, and, although I’m not a real estate professional, I haven’t read or heard any other predictions like this–in fact, I’ve read just the opposite–so I would really appreciate any thoughts you folks might have on this topic so I can pass the info along.

My thoughts are pretty much

My thoughts are pretty much summed up in the more recent “shambling towards affordability” installment:

http://piggington.com/shambling_towards_affordability_san_diego_housing_overpriced_but