- This topic has 1,076 replies, 26 voices, and was last updated 12 years, 5 months ago by

markmax33.

-

AuthorPosts

-

November 2, 2011 at 12:02 PM #732015November 2, 2011 at 12:31 PM #732018

SK in CV

ParticipantIt is pure shit. Or at least the article about the report is. It claims that the GSE’s bought subprime loans. They didn’t, until after the bubble already started bursting in 2006, and that was mainly in the form of purchases of MBS’s. (A stupid move, cost the taxpayers billions, but had nothing to do with creating the bubble.)

It also cites Countrywide as one of the main offenders. Indeed. But Countrywide, as a piece of their total business, did very little with the GSE’s. They were the Wall Street darlings for providing inventory to package and resell in the private MBS market.

It also mentions the CRA again, which wasn’t (and still isn’t) an issue for mortgage banks, only commercial banks. Hence, lenders like Countrywide were under no obligation to meet CRA standards. They did voluntarily agree to meet HUD standards, which are often the target of criticism. The problem with that line of criticism is that they didn’t meet those standards. A report just issued about a month ago showed that Countrywide failed to meet HUD underwriting standards on half of the loans tested. Remember, Countrywide was the go-to subprime lender. Was the go-to lender for product for Wall Street. And they sold products which were ineligible for the GSE to purchase.

This horse has been dead for years. It should stay that way.

November 2, 2011 at 1:23 PM #732024markmax33

Guest[quote=SK in CV]It is pure shit. Or at least the article about the report is. It claims that the GSE’s bought subprime loans. They didn’t, until after the bubble already started bursting in 2006, and that was mainly in the form of purchases of MBS’s. (A stupid move, cost the taxpayers billions, but had nothing to do with creating the bubble.)

It also cites Countrywide as one of the main offenders. Indeed. But Countrywide, as a piece of their total business, did very little with the GSE’s. They were the Wall Street darlings for providing inventory to package and resell in the private MBS market.

It also mentions the CRA again, which wasn’t (and still isn’t) an issue for mortgage banks, only commercial banks. Hence, lenders like Countrywide were under no obligation to meet CRA standards. They did voluntarily agree to meet HUD standards, which are often the target of criticism. The problem with that line of criticism is that they didn’t meet those standards. A report just issued about a month ago showed that Countrywide failed to meet HUD underwriting standards on half of the loans tested. Remember, Countrywide was the go-to subprime lender. Was the go-to lender for product for Wall Street. And they sold products which were ineligible for the GSE to purchase.

This horse has been dead for years. It should stay that way.[/quote]

How about the Federal reserve artificially lowering interest rates after the .com bubble? Explain that one away. The money flowed straight out of the stock market and into the housing market to create the next bubble instead of letting the tech bubble completely fail.

November 2, 2011 at 1:26 PM #732023Guest[quote=urbanrealtor]I think you could make the argument that government (via HUD and the private GSE’s) were a contributing factor but that article is pure shite.

The hilarious part is that they refer to this as a “smoking gun”.

Its just a 20 page memo about not discriminating based on protected class (like race or gender).

That discrimination does occur too.

I have seen it up close.

Here is one of my favorite examples:

While working at a bank several years ago, our manager froze the account of a car dealer because she felt “that Arab guy uses too much cash for a business”.

He was Persian.

I asked what he was doing wrong and mentioned that he was Persian.

My manager’s comment:

“Well what’s the difference? Anyway, I just don’t trust him.”I managed his account.

I know there was nothing wrong on our end.

I have no knowledge as to whether he was an ethical business man or not.[/quote]A bank manages risk, if a person sees something they think is risky, they should act. The GOV should not be able to intervene in that business decision. It’s crazy. Couldn’t your boss have had several bad loans with local persians and seen a higher risk with that type of individual without being a “racist”?

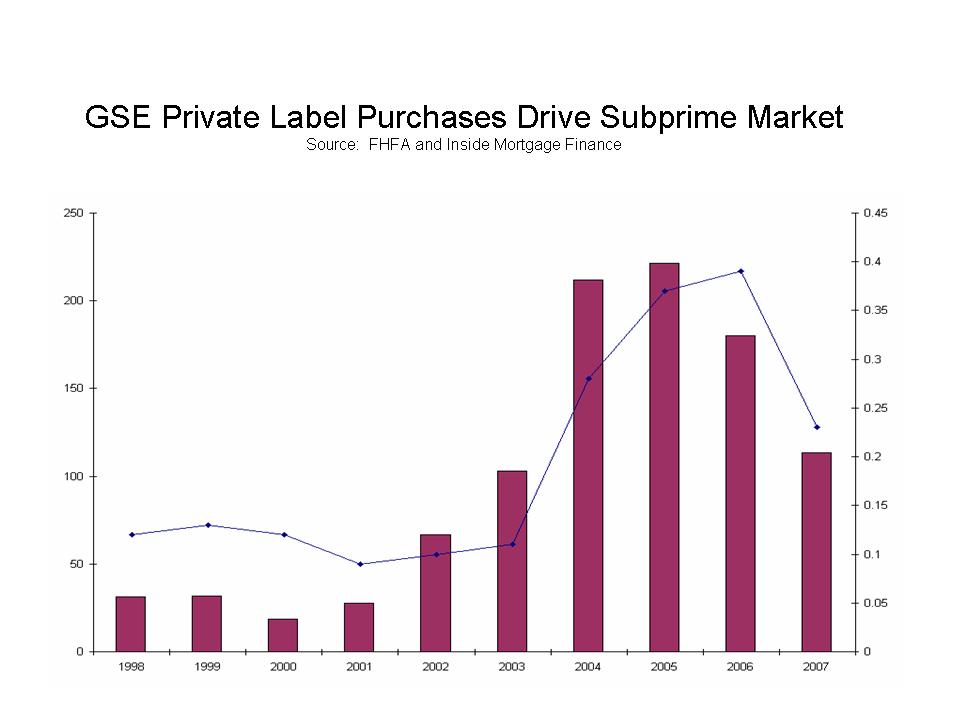

The GOV 100% caused the housing bubble through ENABLING the bad loans to be resold from the banks balance sheets! Without the ENABLING element of the GSEs and the low interest rates of the FED the housing bubble COULD NOT HAVE HAPPENED! PLEASE explain how a bubble could have started without a 2ndary market to resell risk.

Actually your statement above that the GSE loan volume went up AFTER the bubble is flat out a lie. Here is a graph. The highest years are right before the bubble:

November 2, 2011 at 1:43 PM #732025Participant[quote=markmax33]

How about the Federal reserve artificially lowering interest rates after the .com bubble? Explain that one away. The money flowed straight out of the stock market and into the housing market to create the next bubble instead of letting the tech bubble completely fail.[/quote]How about it?

How about the repeal of glass-steagall that allowed Wall Street unfettered access to product to fill an insatiable demand in order to collect billions of dollars in fees for creating mortgage backed securities? How about the virtual disappearance of underwriting standards? How about loan brokers and agents who knowingly and willfully prepared loan applications for their clients to sign which they knew contained lies? How about mortgage lenders who paid more to those that brokered bad loans than those who brokered good loans? How about real estate agents who encouraged buyers to buy property that they knew their clients couldn’t afford and told them not to worry because they could always refinance when the teaser rates expired? How about buyers who knowing lied on their loan applications? How about the debt rating agencies who collected huge fees to grant their seal of approval on debt instruments they either knew, or should have known were of low quality. How about investment advisors who collected commissions and fees for telling their investor clients to buy crappy mortgage backed securities? How about clients who did no due diligence on the investments they were making?

In the current economic model there is no such thing as “real” interest rates. The Fed has control of some interest rates. The open market controls some. The financial markets control others. If you think the Fed was the driving force behind the bubble, you’re sadly mistaken. They were a piece of a puzzle. Nobody was blameless.

November 2, 2011 at 2:45 PM #732031Guest[quote=SK in CV][quote=markmax33]

How about the Federal reserve artificially lowering interest rates after the .com bubble? Explain that one away. The money flowed straight out of the stock market and into the housing market to create the next bubble instead of letting the tech bubble completely fail.[/quote]How about it?

How about the repeal of glass-steagall that allowed Wall Street unfettered access to product to fill an insatiable demand in order to collect billions of dollars in fees for creating mortgage backed securities? How about the virtual disappearance of underwriting standards? How about loan brokers and agents who knowingly and willfully prepared loan applications for their clients to sign which they knew contained lies? How about mortgage lenders who paid more to those that brokered bad loans than those who brokered good loans? How about real estate agents who encouraged buyers to buy property that they knew their clients couldn’t afford and told them not to worry because they could always refinance when the teaser rates expired? How about buyers who knowing lied on their loan applications? How about the debt rating agencies who collected huge fees to grant their seal of approval on debt instruments they either knew, or should have known were of low quality. How about investment advisors who collected commissions and fees for telling their investor clients to buy crappy mortgage backed securities? How about clients who did no due diligence on the investments they were making?

In the current economic model there is no such thing as “real” interest rates. The Fed has control of some interest rates. The open market controls some. The financial markets control others. If you think the Fed was the driving force behind the bubble, you’re sadly mistaken. They were a piece of a puzzle. Nobody was blameless.[/quote]

This is simple to explain! Without the federal reserve system or the 2ndary GOV resale market to unload risk we would have never needed glass-steagall. That law is a barrier to limit the abuse of the federal reserve by the bankers. Ultimately there were MANY PEOPLE who were scamming the system but WITHOUT THE ENABLING ELEMENTS IT COULD NOT HAVE HAPPENED. THE MARKET WOULD HAVE TAKEN CARE OF ITSELF!

You don’t prosecute drug users, you cut off the drug dealers. The GOV intervention was the crack cocaine to the housing bubble. The home buyers/loan officers/RE Agents/home buyers, etc were all the crackheads.

November 2, 2011 at 3:10 PM #732046aldante

ParticipantSK,

I notice that you did not address that GSE graph that Markmax asked you about. That seems to take your arguement down like hard.November 2, 2011 at 3:25 PM #732048urbanrealtor

Participant[quote=markmax33]

A bank manages risk, if a person sees something they think is risky, they should act. The GOV should not be able to intervene in that business decision. It’s crazy. Couldn’t your boss have had several bad loans with local persians and seen a higher risk with that type of individual without being a “racist”?

[/quote]

Uhhhh….No.

Doing that would be, by definition, racist and illegal.

Logic isn’t your strong suit is it?

[quote=markmax33]The GOV 100% caused the housing bubble through ENABLING the bad loans to be resold from the banks balance sheets! Without the ENABLING element of the GSEs and the low interest rates of the FED the housing bubble COULD NOT HAVE HAPPENED! PLEASE explain how a bubble could have started without a 2ndary market to resell risk.

Actually your statement above that the GSE loan volume went up AFTER the bubble is flat out a lie. Here is a graph. The highest years are right before the bubble:

Well your unlabeled JPEG does not support your assertions. The higher graph marks (again its basically unlabeled) are pretty solidly within what is widely accepted as the bubble period. Also, that wasn’t my statement. Aim before firing (as Allan says).

Another thing is this: the GSE’s were not public or government entities prior to 2008. They were sponsored and set up by the government but operated independently (and sold stock on the NYSE and such).

The FED’s prime rate had some connection but was not as direct as you imply.

Prime rate affects credit cards and money market rates and HELOCS.

It does not generally affect mortgages.

Even ARMs are based on LIBOR, not prime (the L in LIBOR stands for LONDON, not Liberal).

If anything, the tech bust had more to do with it.

It chased money from stocks to bonds and debt-based securities in massive amounts.

Bear in mind the GSE’s don’t handle stated anything and were rather late to the subprime game.

This is not something you can clearly lay at the government’s door.

This was a largely a failure of private risk management.

This is typical of unregulated credit markets.November 2, 2011 at 3:29 PM #732049ParticipantEdit:

Most HELOCS are based on LIBOR also.November 2, 2011 at 3:43 PM #732050Participant[quote=aldante]SK,

I notice that you did not address that GSE graph that Markmax asked you about. That seems to take your arguement down like hard.[/quote]No I didn’t. Which graph?

November 2, 2011 at 3:48 PM #732052Guest[quote=urbanrealtor]

Well your unlabeled JPEG does not support your assertions. The higher graph marks (again its basically unlabeled) are pretty solidly within what is widely accepted as the bubble period. Also, that wasn’t my statement. Aim before firing (as Allan says).

[/quote]Widely accepted as the BUBBLE INFLATING PERIOD! EXACTLY, THANK YOU SIR! You are proving my point.

[quote=urbanrealtor]

Another thing is this: the GSE’s were not public or government entities prior to 2008. They were sponsored and set up by the government but operated independently (and sold stock on the NYSE and such).

[/quote]LOLOLOLOLOLOLOLOLOLOLOLOLOLOL! Do you actually believe that any corporation with a GOV gaurentee would not be abused?! WOW! “Government Sponsored Enterprise”.

[quote=urbanrealtor]

The FED’s prime rate had some connection but was not as direct as you imply.

[/quote]Since when does Bernanke not set the interest rates in the market? If he moved the overnight rate to 10% do you think the market would be lower that than? Really? LOL!

[quote=urbanrealtor]

Prime rate affects credit cards and money market rates and HELOCS.

It does not generally affect mortgages.

Even ARMs are based on LIBOR, not prime (the L in LIBOR stands for LONDON, not Liberal).

[/quote]The FED directly/indirectly controls the money flow in this country on EVERY level.

[quote=urbanrealtor]

If anything, the tech bust had more to do with it.

It chased money from stocks to bonds and debt-based securities in massive amounts.

Bear in mind the GSE’s don’t handle stated anything and were rather late to the subprime game.

[/quote]If the market had to absorb the cost of the loans the GSE took on the overall interest rates would have been higher and THUS the GSEs did contribute very directly to the overall market. They also helped set the tone for the rest of the market. They were the enablers.

[quote=urbanrealtor]

This is not something you can clearly lay at the government’s door.

This was a largely a failure of private risk management.

This is typical of unregulated credit markets.[/quote]Do you think if the banks had to carry any of the risks for the homeloans like they used to, they would have made those loans. No way in hell. It is true that China, Japan and the retirement plans bought many of these securities as well, but when they see the GOV doing it and gaurenteeing everyone with FDIC, FED bailouts, etc, why wouldn’t they join in? It is an overflawed thought process the GOV enabled very directly.

The loser is the tax payer through massive debt and inflation.

November 2, 2011 at 4:36 PM #732059Participant[quote=SK in CV][quote=aldante]SK,

I notice that you did not address that GSE graph that Markmax asked you about. That seems to take your arguement down like hard.[/quote]No I didn’t. Which graph?[/quote]

This one:

November 2, 2011 at 4:47 PM #732063Participant[quote=aldante][quote=SK in CV][quote=aldante]SK,

I notice that you did not address that GSE graph that Markmax asked you about. That seems to take your arguement down like hard.[/quote]No I didn’t. Which graph?[/quote]

This one:

http://1.bp.blogspot.com/_gsLSecmB4no/TA%5B/quote%5D

No, not in the least. It’s unlabeled. I don’t even know what it is supposed to represent. If I did, and I knew which argument it’s supposed to take down, I would be glad to address it.

November 2, 2011 at 8:58 PM #732078GuestHere is the full report:

http://www.cato-at-liberty.org/krugmans-fannie-mae-fantasyland/

I’m pretty sure that puts the nail in the coffin.

November 2, 2011 at 9:18 PM #732083Participant[quote=SK in CV][quote=aldante][quote=SK in CV][quote=aldante]SK,

I notice that you did not address that GSE graph that Markmax asked you about. That seems to take your arguement down like hard.[/quote]No I didn’t. Which graph?[/quote]

This one:

http://1.bp.blogspot.com/_gsLSecmB4no/TA%5B/quote%5D

No, not in the least. It’s unlabeled. I don’t even know what it is supposed to represent. If I did, and I knew which argument it’s supposed to take down, I would be glad to address it.[/quote]

http://www.cbo.gov/doc.cfm?index=2839&type=0

Sk this is a report by CBO in 2001.

Here is an exerpt

Fannie Mae asserts that intense competition forces the housing GSEs to pass through all subsidies. As evidence, it cites its estimate that, as of December 31, 2000, Fannie Mae and Freddie Mac together held only 22.7 percent of the fixed-rate single-family mortgages outstanding in the United States. However, adjusting for other government mortgage guarantees, GSE-guaranteed mortgage-backed securities, and jumbo mortgages, CBO estimates that Fannie Mae and Freddie Mac have at least a 71 percent share of the market. That share is growing, which suggests that they have significant market power.

-

AuthorPosts

{kind=link}

{kind=link}

- You must be logged in to reply to this topic.