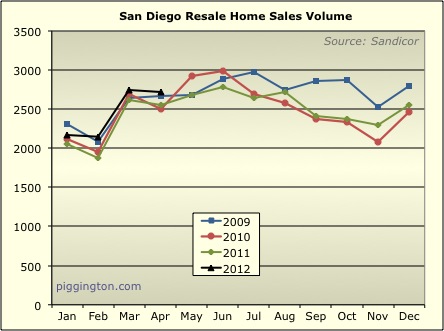

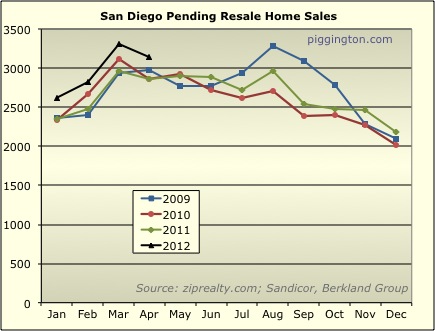

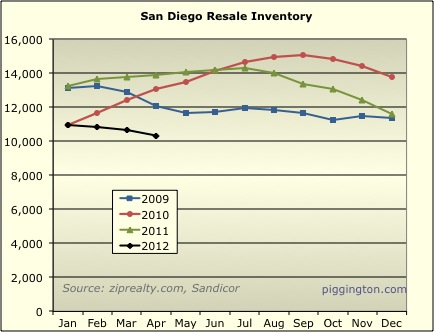

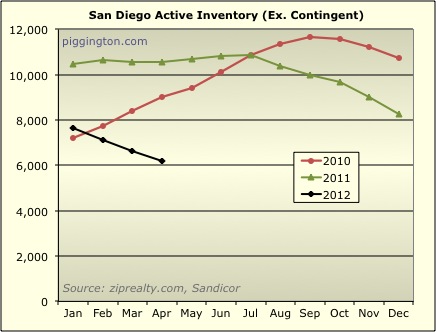

Inventory has remained super tight, and as the historical

relationship depicted in the following chart would have predicted,

prices have been on the rise:

Of course, we are in a seasonally strong time of year which, as the

following graph shows, tends to experience some price strength:

However, months of inventory is unusually low this spring:

This suggests that the spring bounce could be more pronounced this

year. As long as supply (as measured by months of inventory)

stays this low, all other things staying equal, the pressure on home

prices will be to the upside. Whether inventory stays this

low, and whether all other things remain equal, remain to be seen…

More graphs below:

All other things have

All other things have remained equal since the data you are using and inventory has dropped off a cliff. Who knows whats ahead but it could surprise some folks around here

Spring bounce no surprise.

Spring bounce no surprise. Big Q is – what happens in the Fall ? The Piggs are definitely split on that one:

http://piggington.com/poll_2012_prices_same_path_as_2009_2010_or_2011

IMO What we are looking at is

IMO What we are looking at is far more significant than a Spring bounce. Spring bounce is more a measure of demand. What we are seeing is a lack of supply which will lead the demand to start piling up on itself. Prices arent really increasing much if at all but the conditions building up put forth a good case for that coming sooner than most expected.

sdrealtor wrote:IMO What we

[quote=sdrealtor]IMO What we are looking at is far more significant than a Spring bounce. Spring bounce is more a measure of demand. What we are seeing is a lack of supply which will lead the demand to start piling up on itself. Prices arent really increasing much if at all but the conditions building up put forth a good case for that coming sooner than most expected.[/quote]

One might suggest that “flat” prices when inventory is this low (how does this compare to spring 2004 numbers?) and interest rates are skidding along the bottom…would be a very, very bearish sign.

But that’s just me. 🙂

Submitted by desmond on

Submitted by desmond on December 8, 2011 – 5:59pm.

There is a lot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months

desmond wrote:Submitted by

[quote=desmond]Submitted by desmond on December 8, 2011 – 5:59pm.

There is a lot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months[/quote]

desmond – not sure that’s really fair. I don’t think anyone is trying to “justify” anything.

sdr is calling like he see’s it and he doesn’t see weakness.

I see local buyers out there buying and weak inventory, but global economic clouds forming. Not sure what’s gonna happen. It looks side-ways as hell to me.

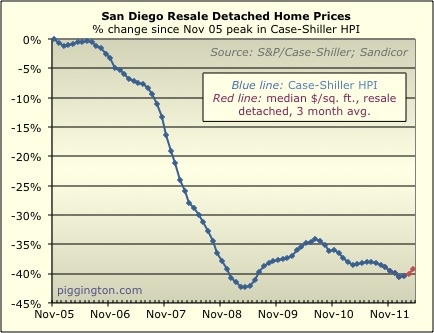

Looking at that graph we have crossed or come very close to that 40% line 6 or 7 times in the last 4 years.

sdduuuude wrote:desmond

[quote=sdduuuude][quote=desmond]Submitted by desmond on December 8, 2011 – 5:59pm.

There is a lot of effort trying to justify a “Flat or Sideways” market. I can’t wait to read the justifications in 3-6 months[/quote]

desmond – not sure that’s really fair. I don’t think anyone is trying to “justify” anything.

sdr is calling like he see’s it and he doesn’t see weakness.

I see local buyers out there buying and weak inventory, but global economic clouds forming. Not sure what’s gonna happen. It looks side-ways as hell to me.

Looking at that graph we have crossed or come very close to that 40% line 6 or 7 times in the last 4 years.[/quote]

dude,

That quote of mine was from last December. So I agree not much has happened. I will concede some small price gains in the near future but nothing to get excited about.

In my hood you could have

In my hood you could have gotten a house for 20 to 50k less than you could get the same house today. Would that excite you as a buyer? Would missing out on a small window like that not bother you? It was a 2 to 3 month window that came and went

Not bearish at all. Just

Not bearish at all. Just still working through and digesting the distress that is left out there. The number of REO and short sales hitting the market is dropping like a rock also. Delinquancies are dropping as reported by all the servicers also. Another year perhaps two more and we should be completely out of the woods with the distress. By then Desmond will be out of the woods too and back in civilization 🙂

BTW Richs graphs show 4 consecutive months of price gains. The graphs are a month in arrears so we will be up to 5 soon enough with no end in sight. Doom away doomsayers…..

Remember I am older and it is

Remember I am older and it is hard to see any gains on those graphs! If prices rise after all the REO’s and SS are basically done with that will be a better indicator then just the low end that is on “going out of business” sale.

News from the field-its not

News from the field-its not just the low end that has rising prices. And without my reading glasses I am blind as a bat also.

CA renter wrote:sdrealtor

[quote=CA renter][quote=sdrealtor]IMO What we are looking at is far more significant than a Spring bounce. Spring bounce is more a measure of demand. What we are seeing is a lack of supply which will lead the demand to start piling up on itself. Prices arent really increasing much if at all but the conditions building up put forth a good case for that coming sooner than most expected.[/quote]

One might suggest that “flat” prices when inventory is this low (how does this compare to spring 2004 numbers?) and interest rates are skidding along the bottom…would be a very, very bearish sign.

But that’s just me. :)[/quote]

Correct that is just you….wrong as usual!

The stats lag and take time to catch up with the reality those of us aactive in the business see. From today’s U-T:

The overall median price in May rose 3.2 percent from a year ago to $335,000, matching the median 18 months ago. When compared to April, prices rose 1.7 percent.

http://www.utsandiego.com/news/2012/jun/13/single-family-home-sales-hit-6-12-year-high/

Its starting in the lower priced areas and spreading to the higher priced areas. You dont see it in the stats for the higher priced areas…yet but its coming too.

Of course prices should rise

Of course prices should rise a bit given the inventory and interest rate environment. But how sustainable are these prices if inventory and/or interest rates normalize?

Given what I’m seeing, prices are not rising to anywhere near the levels one would expect in this environment — lowest interest rates in history, one of the lowest inventory levels in history, artificially supppressed foreclosure activity, ~90% govt-backed mortgages with low down payment requirements (3%?!?!?), and it’s the “Spring Selling Season”!!! Very bearish.

I’m not seeing the market as being “on fire” around here. Well-priced, highly-desirable properties sell very quickly, and for a good price; that’s nothing new…these types of properties sold quickly even during the “recession.” Houses that are average, even those priced at 2009 levels, are still sitting for the most part.

Again, what is happening on the lower end is more due to the interest rate environment and investors who are scouring all markets in order to earn some kind of yield. Everyone I know with cash is looking at real estate more than any other asset class at this moment. No exceptions.

Only time will tell who is right. We have to see what happens when/if we ever see a “free market” WRT interest rates and foreclosures.

Very sustainable. Prices are

Very sustainable. Prices are being held down by tight lending and appraisals. Without that they would be rising faster. Example-I had a client lose a property to a cash buyer last month even though they bid $15K more, were putting 20% down on a house in the 700’s and we sent a bank statement showing they had another $300K in cash sitting in their money market.

I had 4 sales close in the last 2 weeks and not one of them was on time. Sellers are taking lower offers because they dont trust the lenders to fund the loans.

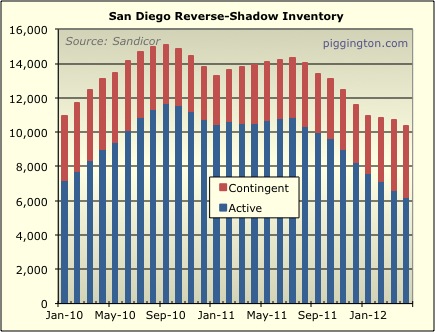

On CR, I just saw that shadow inventory using probably the strictest definition is down 20% year over year. Around here down payments are averaging well over 20%. Without 20% its tough to even get a house these days as you are bidding against stronger buyers. The dark clouds are clearing. I see more evidence of that every day.

You see very little and live in a fantasy world that you have concocted based upon a few years ago that no longer exists. Very few houses are sitting.

Dont be surprised to see 10% year over year appreciation come Janury 2013.

FWIW I just checked your neighborhood defined as North of mine and South of LC. There are 7 houses on the market. Four of them were listed in the last 7 days (actually 3 today). The other 3 are strange properties that have been off and on the market several times each over the last 6 years. Nothing is sitting except for a few oddballs that have been sitting for many years.

One of the 3 oddball houses

One of the 3 oddball houses just sold. Its been off and on the market for years. That leaves 2 more that have been off and on since 2006. Any questions left about how much demand is out there now.

CA renter wrote:

…these

[quote=CA renter]

…these types of properties sold quickly even during the “recession.” [/quote]

Just what is intended by the quotation maerks around recession ?

Most people would interpret this the same way as someone saying “so-called recession” or “alleged recession”.

I thought there was a 100% consensus around here that we did go through a recession.

But maybe that’s just me.

FormerSanDiegan wrote:CA

[quote=FormerSanDiegan][quote=CA renter]

…these types of properties sold quickly even during the “recession.” [/quote]

Just what is intended by the quotation maerks around recession ?

Most people would interpret this the same way as someone saying “so-called recession” or “alleged recession”.

I thought there was a 100% consensus around here that we did go through a recession.

But maybe that’s just me.[/quote]

Good question.

While I understand the official definition of a recession, I’m a bit cynical about how this recession has been framed — like it was a blip between late 2007 and mid 2009. IMHO, we’ve been in a recession since at least 2000/2001, with a credit bubble in the middle that masked the recession/depression. I put it in quotation marks because I think “long-term depression” better describes our economic situation.

Rates are low, but alot of

Rates are low, but alot of folks probably lost 9% of their down-payment in the market over the last couple of weeks.

As Rich points out the reason

As Rich points out the reason for this apparent price resilience is because of low rates and squeezed inventory, which is ipso facto not a recovery. So all things being pretty unequal, how can buyers build equity, refinance, and move up in the next few years when prices are likely to remain flat, or down if inflation bites?

Jazzman wrote:As Rich points

[quote=Jazzman]As Rich points out the reason for this apparent price resilience is because of low rates and squeezed inventory, which is ipso facto not a recovery. So all things being pretty unequal, how can buyers build equity, refinance, and move up in the next few years when prices are likely to remain flat, or down if inflation bites?[/quote]

When’s the last time inflation bites and price of RE didn’t go up? IIRC, the last time inflation bite really hard (70s/80s) price went up BIG. http://www.jparsons.net/housingbubble/. In 1970s, the median was $25k, by 1986, it was at $75k. We’re talking about tripling in price after just 16 years. Take that another 4 years and we’re talking about 4x 1970’s price after just 20 years.

BTW, that was national median price. Here’s the census numbers: http://www.census.gov/hhes/www/housing/census/historic/values.html. Take a look at CA nominal price between 1970 and 1990. We’re talking about over 8x increase. Between 1970-1980, price went up 3.6 times. That’s what happened in the past when inflation bites.

Now, if you say deflation, then I’d agree with you. But if inflation hit, nominal price will most likely increase if history repeats itself. If nominal price increase, people will build equity and be able to refi/move up. They won’t be stuck in their house since they can sell it for more than what they bought it for (in another word, equity).

AN wrote:Jazzman wrote:As

[quote=AN][quote=Jazzman]As Rich points out the reason for this apparent price resilience is because of low rates and squeezed inventory, which is ipso facto not a recovery. So all things being pretty unequal, how can buyers build equity, refinance, and move up in the next few years when prices are likely to remain flat, or down if inflation bites?[/quote]

When’s the last time inflation bites and price of RE didn’t go up? IIRC, the last time inflation bite really hard (70s/80s) price went up BIG. http://www.jparsons.net/housingbubble/. In 1970s, the median was $25k, by 1986, it was at $75k. We’re talking about tripling in price after just 16 years. Take that another 4 years and we’re talking about 4x 1970’s price after just 20 years.

BTW, that was national median price. Here’s the census numbers: http://www.census.gov/hhes/www/housing/census/historic/values.html. Take a look at CA nominal price between 1970 and 1990. We’re talking about over 8x increase. Between 1970-1980, price went up 3.6 times. That’s what happened in the past when inflation bites.

Now, if you say deflation, then I’d agree with you. But if inflation hit, nominal price will most likely increase if history repeats itself. If nominal price increase, people will build equity and be able to refi/move up. They won’t be stuck in their house since they can sell it for more than what they bought it for (in another word, equity).[/quote]

Not necessarily. In the 1970s, women were entering the workforce en masse. The purchasing power of households in the initial phases of women entering the workforce grew tremendously…until prices rose to match that purchasing power, which forced more women into the workforce just to keep up with the cost inflation caused by the initial wave of women entering the workforce. It spiraled up at a time when unions were still strong, so unions were able to demand raises to “keep up with inflation.” And on and on it went for years.

We also saw the credit markets take off in the 1980s which affected prices. Interest rates were high in the initial phase, and have been on a downward trajectory to this very day. This supports prices of assets that are bought with leverage (housing!!!).

Interest rates are now at the lowest point in many, many decades. Credit expansion grew to such an extreme that it, in the past 10-15 years, it caused some of the greatest asset price/credit bubbles in history. That is in the process of popping and reversing. We are in the deleveraging stage now.

Additionally, wages are going nowhere for most working people as more and more money is siphoned from the workers to a relative handful of capitalists at the top (aided and abetted by vast swaths of ignorant “private sector” workers who don’t even comprehend what’s going on and who keep fighting against their own interests, I might add).

Because of all this, workers have very little power, and they are losing what little they have very quickly. There will be no large-scale wage increases going forward, IMO. Any “inflation” will be cost inflation, which is apparently the only kind of “good” inflation according to the Fed (they think rising wages are worse!).

If people have to spend more on food, energy, healthcare, retirement savings, etc., there will be less and less left for housing expenses.

I anticipate more “crowding” as more and more people move into the homes of friends and relatives, more blight, higher crime rates, and a lower quality of life for most working people in the US and other developed nations.

This just doesn’t look like a set-up for rising housing prices going forward.

Your right CA, and don’t

Your right CA, and don’t forget that rents are increasing so anybody renting now it is going to be harder saving any money for a down payment. The “crowding” thing can really be a drag if you live across the street or hallway and you have 2,3 4 families or extra roommates living there. I know I can’t take that anymore and need more space or I will probably “lose it”.

desmond wrote:Your right CA,

[quote=desmond]Your right CA, and don’t forget that rents are increasing so anybody renting now it is going to be harder saving any money for a down payment. The “crowding” thing can really be a drag if you live across the street or hallway and you have 2,3 4 families or extra roommates living there. I know I can’t take that anymore and need more space or I will probably “lose it”.[/quote]

I’m right there with you, desmond. I haven’t lived in multifamily housing for several decades but I can’t even stand SFR neighbors on the same street who have too many vehicles and are spilling out of their houses and garages.

This is why I don’t like some of the “SD beach areas,” even where the lots are somewhat generous. Even 1+ mile from the beach, you have a 17 yo “runaway” from Kansas rinsing sand off themselves with your hose, changing clothes and even going to the bathroom behind your weeping bottlebrush to get ready to catch the city bus on the next corner. Not to mention constantly picking up beer and soda bottles and cans and fast food trash in your front yard and having people sift thru your recycle bins when they’re out for pickup. It’s a zoo around there for 6+ months per year and the houses aren’t cheap!

I would just as soon live on 1/4+ AC or even 100+ feet from the next neighbor, regardless if I needed or used the land … or not. It acts as a buffer and there is no substitute for peace, tranquility and privacy.

CAR, in essence, what you’re

CAR, in essence, what you’re saying is, it’s different this time. I guess we’ll just have to wait and see if it really is different this time.

I have a few questions for you. Do you think women entering the work force add 8x to their buying power between 70-90?

Here’s inflation adjusted income for both men and women: http://en.wikipedia.org/wiki/File:InflationAdjustedMedianIncomeHistory.jpg. Doesn’t look like it went up 8x inflation adjusted.

Nominal price went up over 3x between 70 and 80. Between 80 and 90, it only went up a little over 2x. so credit market taking off statement doesn’t really explain why 70s saw a larger price spike.

Interest rate went up from ~7.5% to over 17.5% between 1970 and 1980: http://www.mortgagenewsdaily.com/mortgage_rates/charts.asp, yet price went up over 3x.

Didn’t people have to spend more on food, energy, etc between 70-80?

Blah Blah Blah go back to the

Blah Blah Blah go back to the ivory towers. CAR you have far too many ifs and buts to live in the real world. I just ran a search in Mira Mesa for homes in Mira Mesa with at least 3Br and 1400 sq ft up to $400K. These were the houses you told me would be in the 200’s by now. There are 33 and 29 of those are pending or contingent. Of the 4 actives 1 came on the market today and another has tenants that wont let anyone in to see it. Good luck finding one if you are buyer.

sdrealtor wrote:Blah Blah

[quote=sdrealtor]Blah Blah Blah go back to the ivory towers. CAR you have far too many ifs and buts to live in the real world. I just ran a search in Mira Mesa for homes in Mira Mesa with at least 3Br and 1400 sq ft up to $400K. These were the houses you told me would be in the 200’s by now. There are 33 and 29 of those are pending or contingent. Of the 4 actives 1 came on the market today and another has tenants that wont let anyone in to see it. Good luck finding one if you are buyer.[/quote]

I’m not at all familiar with Mira Mesa, so find it difficult to believe I’ve made any predictions or comments about that area. I make every attempt to debate only about things I know fairly well; Mira Mesa isn’t really on my radar.

Nonetheless, there is no doubt that inventory is being manipulated down on the supply side, and demand is being artificially increased with these low interest rates, etc. I don’t see the housing market as being anywhere near a “free market,” yet even with these manipulations, prices are still relatively flat during a period with extremely low inventory and extremely low interest rates…and it’s “Spring Selling Season!!!” on top of it. That’s bearish, IMO.

More BLah Blah Blah. Who said

More BLah Blah Blah. Who said it was ever a truly free market? Its not only being manipulated to the down side but to the upside as well. Good luck getting something to appraise 5% above comps even though there are stacks of buyers at that price.

You had Summerhill dropping into the 200’s along with entry level houses in Mira Mesa and Clairemont. If I cared enough to find the time I could prove it. Prices arent flat anymore or for much longer. Just ran a search for 2BR condos in MM. 26 sales in the last 90 days, about 40 pending or contingent and ONE active (that is priced too far above the market right now).

sdrealtor wrote:More BLah

[quote=sdrealtor]More BLah Blah Blah. Who said it was ever a truly free market? Its not only being manipulated to the down side but to the upside as well. Good luck getting something to appraise 5% above comps even though there are stacks of buyers at that price.

You had Summerhill dropping into the 200’s along with entry level houses in Mira Mesa and Clairemont. If I cared enough to find the time I could prove it. Prices arent flat anymore or for much longer. Just ran a search for 2BR condos in MM. 26 sales in the last 90 days, about 40 pending or contingent and ONE active (that is priced too far above the market right now).[/quote]

Right here:

http://piggington.com/shambling_towards_affordability

Summerhill dropping into the $300K range (per your numbers), and no mention of Mira Mesa on my part. Like I’ve said, I won’t debate/argue about things I’m not familiar with.

And how in the world do you figure inventory is being manipulated to the up-side?

Prices not inventory. They

Prices not inventory. They are manipulating the market to control price drops (withholding inventory, low rates) and price increases (overly tough appraisals)

sdrealtor wrote:Prices not

[quote=sdrealtor]Prices not inventory. They are manipulating the market to control price drops (withholding inventory, low rates) and price increases (overly tough appraisals)[/quote]

The lenders have (hopefully) learned their lesson. If you were loaning out your own money, and you knew prices/inventory/interest rates were manipulated they way they are — and knowing how it would affect prices if things should ever return to normal — wouldn’t you institute “overly tough appraisals”?

What I would and right or

What I would and right or wrong are irrelevant. The reality is they are artificially keeping prices down in some areas the way the appraisals are being done.

sdrealtor wrote:What I would

[quote=sdrealtor]What I would and right or wrong are irrelevant. The reality is they are artificially keeping prices down in some areas the way the appraisals are being done.[/quote]

Nothing artificial about it…they are **finally** making rational decisions WRT collateralization and lending.

So how many appraisals have

So how many appraisals have you seen in the last 6 months?

sdrealtor wrote:So how many

[quote=sdrealtor]So how many appraisals have you seen in the last 6 months?[/quote]

Not as many as you have, but I’ve seen a couple that people were complaining about, and thought that the appraisers were very reasonable about it.

I think too many people think that 2003-2006 prices were “normal” and that we’d still be there if not for the recession that “came out of nowhere.” Too many people don’t grasp the connection between the unsustainable credit bubble and unsustainable housing prices.

Too many people don’t seem to understand that the lenders are doing exactly what they should be doing given the current manipulations in the credit/housing markets and the political rhetoric about lowering mortgage amounts to “market” prices when prices fall (but not when they go up!).

I’m callin BS on this as I

I’m callin BS on this as I sincerely doubt you have seen actual appraisals and its unlikely if you did that you would understand all the details anyway.

Explain this to me. A friend just bought a house and appraisal came in almost $100K below purchase price. He put about 50% down so it wasnt an issue. There were multiple offers on it and after we got it under contract a few ALL CASH back up offers came in at or around asking price. Is the definition of value not what a ready, willing and able buyer will pay for something? These are cash buyers. As an aside the appraiser told the buyers lender (off the record of course) that even though he couldnt come close to appraising it at the sales price he rarely saw houses like this in 20 years of appraising. He said on a personal level he saw the value but couldnt appraise it at such and further would have no problem paying that price also.

Here you go for your viewing pleasure:

http://www.sdlookup.com/MLS-120024836-7920_Winans_Cove_San_Diego_CA_92126

11 offers first weekend on market. No more showings

Or 5292 Stallion Run in Carmel Valley which got about 20 offers the first weekend. No more showings

There arent anywhere close to 10 or 20 comparable shadow inventory properties like these in the immediate area but if there were there would be buyers for them

sdrealtor wrote:I’m callin BS

[quote=sdrealtor]I’m callin BS on this as I sincerely doubt you have seen actual appraisals and its unlikely if you did that you would understand all the details anyway.

Explain this to me. A friend just bought a house and appraisal came in almost $100K below purchase price. He put about 50% down so it wasnt an issue. There were multiple offers on it and after we got it under contract a few ALL CASH back up offers came in at or around asking price. Is the definition of value not what a ready, willing and able buyer will pay for something? These are cash buyers. As an aside the appraiser told the buyers lender (off the record of course) that even though he couldnt come close to appraising it at the sales price he rarely saw houses like this in 20 years of appraising. He said on a personal level he saw the value but couldnt appraise it at such and further would have no problem paying that price also.

Here you go for your viewing pleasure:

http://www.sdlookup.com/MLS-120024836-7920_Winans_Cove_San_Diego_CA_92126

11 offers first weekend on market. No more showings

Or 5292 Stallion Run in Carmel Valley which got about 20 offers the first weekend. No more showings

There arent anywhere close to 10 or 20 comparable shadow inventory properties like these in the immediate area but if there were there would be buyers for them[/quote]

Winans just went pending well above asking price all cash and no contingencies. Yes that could be the most bearish indicator of them all CAR!

sdrealtor wrote:sdrealtor

[quote=sdrealtor][quote=sdrealtor]I’m callin BS on this as I sincerely doubt you have seen actual appraisals and its unlikely if you did that you would understand all the details anyway.

Explain this to me. A friend just bought a house and appraisal came in almost $100K below purchase price. He put about 50% down so it wasnt an issue. There were multiple offers on it and after we got it under contract a few ALL CASH back up offers came in at or around asking price. Is the definition of value not what a ready, willing and able buyer will pay for something? These are cash buyers. As an aside the appraiser told the buyers lender (off the record of course) that even though he couldnt come close to appraising it at the sales price he rarely saw houses like this in 20 years of appraising. He said on a personal level he saw the value but couldnt appraise it at such and further would have no problem paying that price also.

Here you go for your viewing pleasure:

http://www.sdlookup.com/MLS-120024836-7920_Winans_Cove_San_Diego_CA_92126

11 offers first weekend on market. No more showings

Or 5292 Stallion Run in Carmel Valley which got about 20 offers the first weekend. No more showings

There arent anywhere close to 10 or 20 comparable shadow inventory properties like these in the immediate area but if there were there would be buyers for them[/quote]

Winans just went pending well above asking price all cash and no contingencies. Yes that could be the most bearish indicator of them all CAR![/quote]

Quick comments on the house on Stallion Run Pl. This house is plan 1x for the Carriage Run which in my opinion is a better floor plan than previously released plan 1 and plan 2. There is strong demand for houses in Torrey Hills area especially newer houses with access to Sage Canyon/Ocean Air elementary school. I was at the open house and I will say there are at least 5 potential buyers with agents present in there at the same time. In this area, I wish I can buy a house at 2003 price. Seriously.

sdrealtor wrote:sdrealtor

[quote=sdrealtor][quote=sdrealtor]I’m callin BS on this as I sincerely doubt you have seen actual appraisals and its unlikely if you did that you would understand all the details anyway.

Explain this to me. A friend just bought a house and appraisal came in almost $100K below purchase price. He put about 50% down so it wasnt an issue. There were multiple offers on it and after we got it under contract a few ALL CASH back up offers came in at or around asking price. Is the definition of value not what a ready, willing and able buyer will pay for something? These are cash buyers. As an aside the appraiser told the buyers lender (off the record of course) that even though he couldnt come close to appraising it at the sales price he rarely saw houses like this in 20 years of appraising. He said on a personal level he saw the value but couldnt appraise it at such and further would have no problem paying that price also.

Here you go for your viewing pleasure:

http://www.sdlookup.com/MLS-120024836-7920_Winans_Cove_San_Diego_CA_92126

11 offers first weekend on market. No more showings

Or 5292 Stallion Run in Carmel Valley which got about 20 offers the first weekend. No more showings

There arent anywhere close to 10 or 20 comparable shadow inventory properties like these in the immediate area but if there were there would be buyers for them[/quote]

Winans just went pending well above asking price all cash and no contingencies. Yes that could be the most bearish indicator of them all CAR![/quote]

Yes, I’ve seen the appraisals, and have no problem understanding the details in the appraisal reports; it’s not rocket science. Again, lenders understand that we are in an abnormal market environment and are taking perfectly rational precautions.

I personally know cash buyers (current and previous) who are/were in the market because they couldn’t get any decent returns in safe fixed income/savings investments, and they don’t trust the stock market. After waiting and renting for years, the numbers make sense for them to buy vs. rent, especially if interest rates are going to be artificially suppressed for the duration.

In the past, some cash buyers were able to make enough money on their investments to pay the rent, so they were gaining purchasing power as prices fell and their rents were being paid for out of investment income. That’s not the case today, so they are looking for a better way to deploy their cash.

We’re also seeing a lot of investment pools making cash offers for the very same reasons. Once interest rates go up, things can change.

And there we have it! The

And there we have it! The “perfectly rational precautions” the lenders are taking are aslo manipulations. An appraisal should be an objective opinion based upon current market conditions and not subject to someone’s “perfectly rational precautions”.

If prices were below 2001 prices along the coast there would be even fewer sales as the profits from renting one’s home vs. selling it would be irresistable. That would take supply lower and demand higher exerting prices right back up.

sdrealtor wrote:Here you go

[quote=sdrealtor]Here you go for your viewing pleasure:

http://www.sdlookup.com/MLS-120024836-7920_Winans_Cove_San_Diego_CA_92126

11 offers first weekend on market. No more showings[/quote]

This one just went pending after ~3 weeks on the market: http://www.sdlookup.com/MLS-120022349-10891_Canyon_Hill_Ln_San_Diego_CA_92126

Would be interesting to see what the sold price is. The range definitely put in the late 2003 price, not even early 2003 price. We all know 2003 saw a pretty significant price increase. This one have no view and average size lot. Nothing really special about the house.

Correct as last sale on that

Correct as last sale on that one was Nov 2003 at $435K. 2003 was a year of big increases but the biggest and final increase came between Nov 2003 and April 2004. That house probably went up close to $100K right after it was purchased. This sale should put it at roughly 20% below the peak price. The “not in our lifetime will we see those prices” arguments are getting weaker.

BTW, Winans Cove had more than 10 offers and went all cash, above asking with no contingencies.

CA renter wrote: . . . I

[quote=CA renter] . . . I think too many people think that 2003-2006 prices were “normal” and that we’d still be there if not for the recession that “came out of nowhere.” Too many people don’t grasp the connection between the unsustainable credit bubble and unsustainable housing prices. . . .[/quote]

I wasn’t suggesting we revert to 2003 to 2006 prices, CAR (the era where buyers bought with “funny money”).

But I don’t understand why some of these SS’s which are NOT in bad condition have been sold for ’98-’02 prices today. Some of these properties are on 8-12K lots (which are larger than the majority of surrounding properties)! The only explanation is that the SS “sellers'” listing agents are NOT in any way interested in getting seller’s lender(s) the highest and best price (since they don’t “represent” the lender[s]). Instead, they have obviously placed a pre-prepared friend/relative buyer’s offer (or even “straw person’s offer [for themselves]) with the defaulted-upon lender the same day as the property was debuted on the MLS (just so they could say they “marketed it”).

There are absolutely NO market fundamentals in place which would suggest we are reverting to ’98-’02 prices as sales occurring during that era were financed with traditional lender ratios and qualifications in place. The “sold comps” emanating from these ridiculous recent “crooked short sales” should NOT be used for valuation purposes when appraising well-maintained “equity sales” where no lenders were ever stiffed during that seller’s period of ownership, IMO.

A SS and an “equity sale” are two completely different animals.

“A friend just bought a house

“A friend just bought a house and appraisal came in almost $100K below purchase price.”

So the appraisal came in 20k under the 2001 price? That does seem a little low given that interest rates are basically half of what they were in 2001.

pemeliza wrote:”A friend just

[quote=pemeliza]”A friend just bought a house and appraisal came in almost $100K below purchase price.”

So the appraisal came in 20k under the 2001 price? That does seem a little low given that interest rates are basically half of what they were in 2001.[/quote]

sdr rarely gives actual pricing on the homes that he posts about. It is usually a $20K-100K spread on something that really means nothing unless you know the actual details.

pemeliza wrote:”A friend just

[quote=pemeliza]”A friend just bought a house and appraisal came in almost $100K below purchase price.”

So the appraisal came in 20k under the 2001 price? That does seem a little low given that interest rates are basically half of what they were in 2001.[/quote]

Price was around 06/07-not quite peak but pretty close. Appraisal came in around late 03 numbers and was $95K below. Only a guy wondering lost on a mountain would have issue with calling that almost $100K below purchase price.

CA renter wrote:I think too

[quote=CA renter]I think too many people think that 2003-2006 prices were “normal”…[/quote]

Uh, have you checked price lately? A lot of desirable bread and butter places between $300-800k are selling for around 2003 price. I even saw a house in Carmel Valley selling at around 2004-2005 price. Even lowly Mira Mesa are selling at 2003 price, if you don’t count beat up REO/SS that goes to all cash buyers/flippers.

AN wrote:CA renter wrote:I

[quote=AN][quote=CA renter]I think too many people think that 2003-2006 prices were “normal”…[/quote]

Uh, have you checked price lately? A lot of desirable bread and butter places between $300-800k are selling for around 2003 price. I even saw a house in Carmel Valley selling at around 2004-2005 price. Even lowly Mira Mesa are selling at 2003 price, if you don’t count beat up REO/SS that goes to all cash buyers/flippers.[/quote]

Yes, but would we be seeing those price levels if we were in a “normal” credit and housing market environment? Where would prices be if the govt got out of the mortgage market and if banks were forced to foreclose on all the deadbeats and put the houses on the market?

IMHO, the credit bubble began in 2001 and I think prices would be below 2001 levels if not for all the interventions.

CA renter wrote:Yes, but

[quote=CA renter]Yes, but would we be seeing those price levels if we were in a “normal” credit and housing market environment? Where would prices be if the govt got out of the mortgage market and if banks were forced to foreclose on all the deadbeats and put the houses on the market?

IMHO, the credit bubble began in 2001 and I think prices would be below 2001 levels if not for all the interventions.[/quote]

When’s the last time we were in a “normal” market? Based on historical data, mortgage rate has been going down since early 80s.

In Southern California, the

In Southern California, the “normal” markets include those brief instants in time in which we cross the long-term averages on our way up and down between booms and busts.

AN wrote:CA renter wrote:Yes,

[quote=AN][quote=CA renter]Yes, but would we be seeing those price levels if we were in a “normal” credit and housing market environment? Where would prices be if the govt got out of the mortgage market and if banks were forced to foreclose on all the deadbeats and put the houses on the market?

IMHO, the credit bubble began in 2001 and I think prices would be below 2001 levels if not for all the interventions.[/quote]

When’s the last time we were in a “normal” market? Based on historical data, mortgage rate has been going down since early 80s.[/quote]

After the stock market crash and 9/11, interest rates were forced much lower than they ever should have been, and they’ve been kept too low for too long. This has created asset bubbles and unsustainable debt loads all around the world.

I’d say that pre-2001 levels were fairly “normal.” Though there have always been maniupulations in the housing market, the past 10 years have been off the charts.

CA renter wrote:After the

[quote=CA renter]After the stock market crash and 9/11, interest rates were forced much lower than they ever should have been, and they’ve been kept too low for too long. This has created asset bubbles and unsustainable debt loads all around the world.

I’d say that pre-2001 levels were fairly “normal.” Though there have always been maniupulations in the housing market, the past 10 years have been off the charts.[/quote]

Based on the data I’m seeing, rates in 2002 is about the same as rates in 1993. So, if you think post-2001 is “abnormal”, then 1993 was abnormal too. They lower the rates because of the recession and raise rates when the economy is booming. Are you suggesting they should have raise rate in the middle of a recession?

AN wrote:CA renter

[quote=AN][quote=CA renter]After the stock market crash and 9/11, interest rates were forced much lower than they ever should have been, and they’ve been kept too low for too long. This has created asset bubbles and unsustainable debt loads all around the world.

I’d say that pre-2001 levels were fairly “normal.” Though there have always been maniupulations in the housing market, the past 10 years have been off the charts.[/quote]

Based on the data I’m seeing, rates in 2002 is about the same as rates in 1993. So, if you think post-2001 is “abnormal”, then 1993 was abnormal too. They lower the rates because of the recession and raise rates when the economy is booming. Are you suggesting they should have raise rate in the middle of a recession?[/quote]

Not raise rates, but they didn’t need to lower them, either.

Recessions can happen for a variety of reasons, and the 2000/2001 recession was largely the result of a bubble bursting. Asset bubbles should not be propped up. The losses should be taken as quickly as possible so that healthy growth can form from a sustainable bottom/foundation.

Personally, I have a big problem with interest rate manipulation and inflation targeting. I’d rather see things handled via changes in taxes, trade policies, and infrastructure spending.

Asset prices should not be propped up, IMHO. Wage stability/growth and the maintenance of household purchasing power should be a higher priority, IMHO.

Here is a graph for the Effective Fed Funds Rate since 1955:

http://research.stlouisfed.org/fred2/series/FEDFUNDS

………..

A chart for mortgage rates (Freddie Mac) since 1971:

http://www.freddiemac.com/pmms/pmms30.htm

……………

More rate graphs for comparison:

http://mortgage-x.com/trends.htm

It seems to be the Effective

It seems to be the Effective Federal Funds rate for most of the manipulated last decade is very much in line with your golden era of workers/household purchasing power between 1955 and 1975. They must have been propping up prices back then…no?

CAR, based on the Effective

CAR, based on the Effective Federal Funds rate chart, they’ve been manipulating and propping up price as far back as 1955. Just look at every sing recession since 1955, every single time there’s a recession, they’ve dropped rate. Further more, after most recessions since 1955, they’ve kept rate flat for a period of time past the end of the recession. So, 2001 is no different. So, if you think post 2001 was not “normal” market, then you must also think anything since 1955 are not “normal”.

sdrealtor wrote:It seems to

[quote=sdrealtor]It seems to be the Effective Federal Funds rate for most of the manipulated last decade is very much in line with your golden era of workers/household purchasing power between 1955 and 1975. They must have been propping up prices back then…no?[/quote]

The longer term Fed Funds trend between 1960 and 1980 was up, and the longer term trend between 1980 and 2012 is down.

Of course, you have to take into consideration the expansion of credit at the same time.

Mish shares some insights regarding this topic:

http://globaleconomicanalysis.blogspot.com/2010/02/law-of-diminishing-returns-of-credit.html

From that same page, economic stats by decade:

http://globaleconomicanalysis.blogspot.com/2010/02/law-of-diminishing-returns-of-credit.html

AN wrote:Jazzman wrote:As

[quote=AN][quote=Jazzman]As Rich points out the reason for this apparent price resilience is because of low rates and squeezed inventory, which is ipso facto not a recovery. So all things being pretty unequal, how can buyers build equity, refinance, and move up in the next few years when prices are likely to remain flat, or down if inflation bites?[/quote]

When’s the last time inflation bites and price of RE didn’t go up? IIRC, the last time inflation bite really hard (70s/80s) price went up BIG. http://www.jparsons.net/housingbubble/. In 1970s, the median was $25k, by 1986, it was at $75k. We’re talking about tripling in price after just 16 years. Take that another 4 years and we’re talking about 4x 1970’s price after just 20 years.

BTW, that was national median price. Here’s the census numbers: http://www.census.gov/hhes/www/housing/census/historic/values.html. Take a look at CA nominal price between 1970 and 1990. We’re talking about over 8x increase. Between 1970-1980, price went up 3.6 times. That’s what happened in the past when inflation bites.

Now, if you say deflation, then I’d agree with you. But if inflation hit, nominal price will most likely increase if history repeats itself. If nominal price increase, people will build equity and be able to refi/move up. They won’t be stuck in their house since they can sell it for more than what they bought it for (in another word, equity).[/quote]

You may be right, and I’m not going to make predictions, but as CAR says this time may be different, since mortgage rates and home prices from 2002 to 2006 behaved contrary to expectations, as a result of subprime lending.

Normally, homes are a good hedge against inflation, since the cost of materials and labor goes up pushing up prices. However, inflation is followed by rising interest rates, which impacts home prices. The effect of interest rates on prices are estimated as having a lag of six months to three years. Although bond prices are a good bellwether for mortgage rates, oversupply of MBSs can drive up rates. I don’t know if the end of the Feds MBS purchase program effects supply.

Oversupply of homes also will adversely effect home prices, even if inflation is high. That is possibly why we are seeing a stranglehold on supply of REOs right now.

Deflation in respect of home prices is the enemy, and I see all arguments against further falls in prices spurred by the fear of it, as much as by the fundamentals.

I like your way that

I like your way that graphical representation is the best way to understand someone.

I believe many appraisals for

I believe many appraisals for “regular sale” properties currently in escrow have in the past year been forced into the toilet by “crooked” SS closings.

As stated on another thread . . .

http://piggington.com/yet_another_funny_short_sale

. . . by SDR and carlsbadworker, SS sellers (and their lender[s]) “don’t give a crap.” Why should they? The “sellers” won’t recover anything from the sale and their credit will take the same or similar “hit” whether they short sale the property (to stave off a trustee’s sale) or squat until they are evicted after the inevitable trustee’s sale. It’s six of one and a half-dozen of the other for them.

see: http://firsttuesdayjournal.com/short-sale-or-foreclosure-the-naked-truth-for-underwater-homeowners/

Their partially-stiffed lender(s) are obviously NOT minding the store (as the REO benes are, when they’re commissioning a local “BPO” prior to marketing the property). Likely out-of-county or out-of-state, these obviously ignorant do-nothing defaulted-upon lenders just automatically assume since their “local broker/agent” is stating the property is only worth a particular amount (because that’s all their “friend” or “relative” that they’re slipping in the back door is willing to pay), then it MUST BE SO! In many, many of these SS transactions, it appears that the lenders who are supposed to be calling the shots are allowing themselves to get ripped off by trusting the “sellers'” local listing brokers/agents to obtain the highest and best price for them!

The truth is, neither the SS “seller” or their lender give a rat’s a$$ what their “selling price” will do to the values of the short-sold property’s surrounding properties. It is a travesty that these artificially-low closings are being used to pollute the appraisals for the “equity” or “traditional” market in the same neighborhood, IMHO.

The independent “BPOs” obtained by foreclosing benes are more “legitimate” because the brokers performing the BPOs don’t yet have the property listed and a willing buyer on the hook (“familiar” to them … or not) and thus a commission on the line when they severely “lowball” the unsuspecting out-of-sight, out-of-mind lender (as a SS agent does) with phony “sold comps” that aren’t really “comps” to the subject “SS property” at all. Thus, the REO lender has a better idea of what their soon-to-be-marketed REO is REALLY worth, ESP if they are willing to spend $$ on cleanup and cosmetic enhancements.

Hi Rich

Any word from Ramsey

Hi Rich

Any word from Ramsey Su lately?

thanks