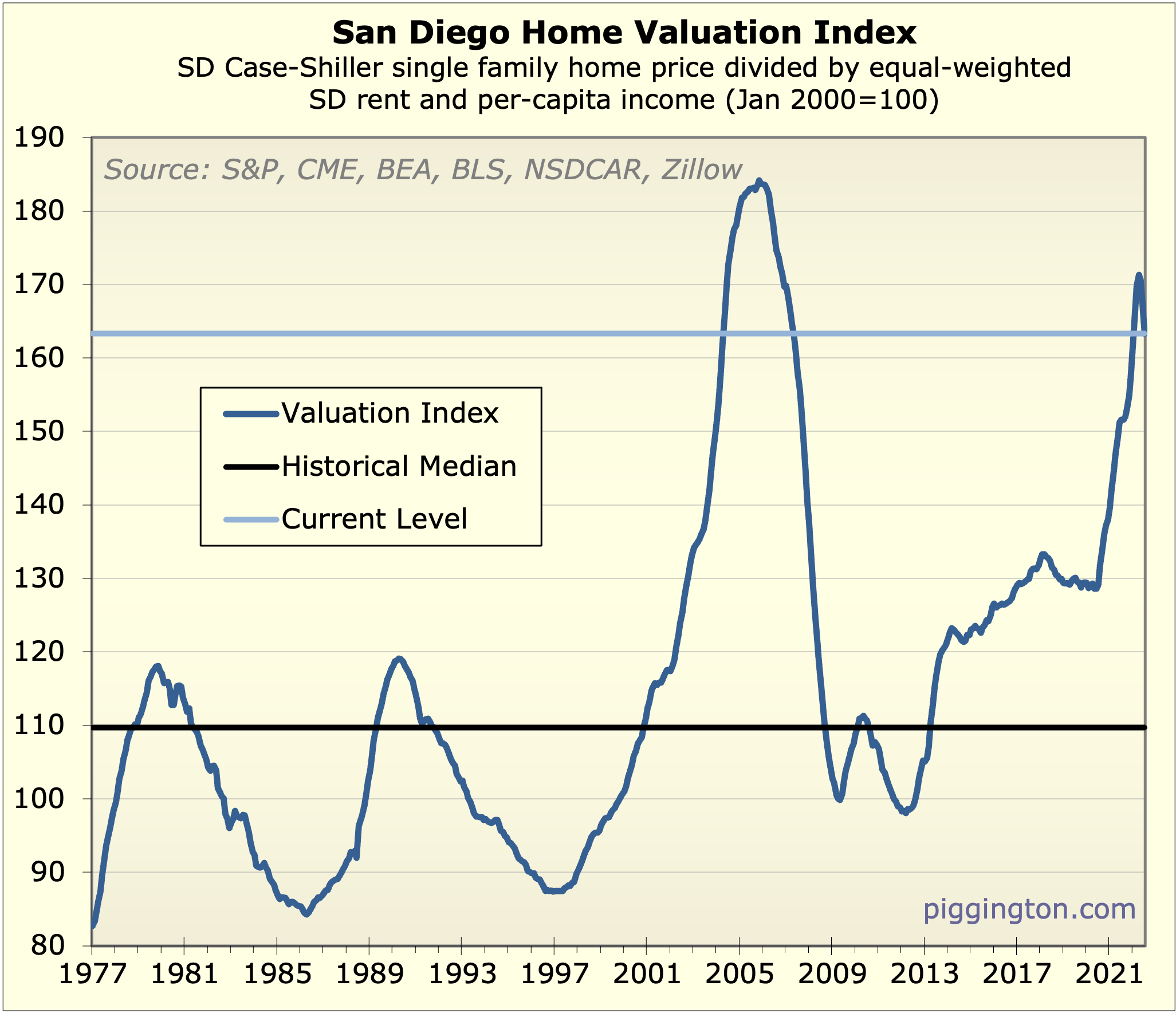

I had a chance to update the valuation info. There shouldn’t be any big surprises here based on what I’ve been posting in the regular monthly threads. The good news is that I can reinstate the “shambling towards affordability” title for this series.

As a reminder, these valuation ratios attempt to measure the fundamental expensiveness of San Diego housing by comparing home prices or monthly payments to a combination of SD rents and per capita incomes.

The small apparent purchase price decline, combined with the upward march of rents and incomes, has resulted in a slight retreat in purchase valuations. Emphasis on slight; this ratio is still not terribly far off bubble-peak levels.

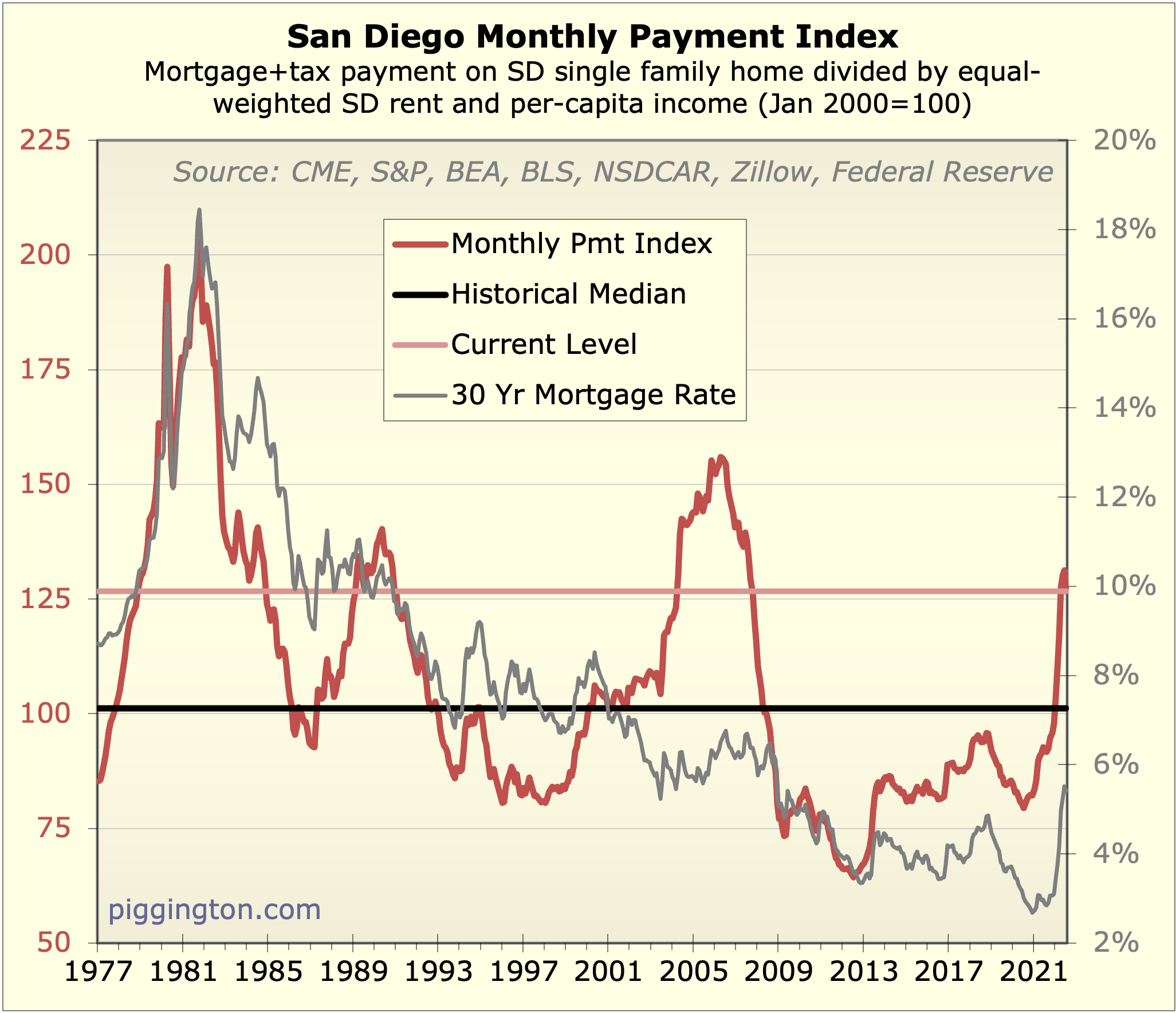

This next chart shows the same thing except that instead of measuring purchase prices, it measures monthly payments. Until recently, this figure was nice and low as a result of very low mortgage rates. Not so much any more. Here there is some more distance from the bubble peak, but we’re still well above anything seen outside the housing bubble and the high-rate 1980s.

My feeling is that the red line in this chart is likely to come down. I don’t see monthly payments at this level as sustainable. The monthly payment ratio could come down by some combination of mortgage rates declining, prices declining, and rents/incomes catching up to prices. I don’t have a strong view on what that combination might be. But I do suspect that one way or the other, that red line is coming down.

Clearly I have less of a view on prices themselves. I think it’s a reasonable base case that they will decline, as they seemingly already have to a degree: they went up a ton in a very short time, and one of the tailwinds of that scorching rise (super low rates) has turned into a headwind. So of course, prices could decline and nobody should be surprised if they do.

But I’m open to the possibility that if things play out just so, there could be little or no price decline from here. For instance, if inflation/rates were to drop quickly without a serious economic downturn, home prices could meander along while rents and incomes catch up. But there’s a lot that could derail that scenario — stubborn inflation, a recession, or the knock-on effects of the (in my opinion) still only half-burst bubble in US growth stocks, to name a few.

So, I don’t so much have a price prediction here, but rather a view that San Diego housing is “priced for perfection,” or at least for a very good economic outcome. We might get lucky and get that good economic outcome. But we might not, and I don’t really think anyone can reliably predict where we’ll end up on that spectrum. Hence, my view that the future path of prices is fairly uncertain.

The first unadjusted chart I

The first unadjusted chart I don’t see as helpful. Imagine looking at it in 2003: “Oh well we’re the top of the cycle, bad time to buy.”

Or at 2014: “Other than the big bubble, prices are higher than any other time. Bad time to buy.”

The second chart tells the story correctly if not perfectly. It shows correctly the late 90s and early 10s as the two best times to buy.

It breaks down when you look at the prior era of high inflation.

This is easy to explain. San Diego real property provides a bundle of legal and economic rights whose values are not well correlated. One of them is inflation protection. The value of that protection was high around 1977-84, and gradually dropped until 2019. After a full 25 years of “Great Moderation” inflation averaging around 2%, the inflation-protection stick in the RE bundle was a thin twig. The fact that, like medical care and tuition, our rents rose faster than inflation did give the twig a little life even back then.

Another little complication is how to model the fact that homeowners can refi rates down and view today’s rates as transitory.

That’s an incredibly complicated topic to model. One way to partly capture it simply is the cost of rate buydowns in points. Right now, as seen in the article I linked to a little while ago, rate buydowns are historically very cheap in points. This reflects a market view where most lenders expect rates to go down. To put it another way, rates are “lower” now than prior 5% 0-point periods because you can now cheaply buy-down to 4.75 when you couldn’t before. Breakeven is under 2 years compared to the normal of about 5.

The fact jumbos are drastically cheaper than conforming is another reason the headline rate is higher than on the ground financing costs. If you are curious, my locked jumbo rate from 2 weeks ago is:

Purchase, 25% down, 7/30 ARM, 4.5%, 0 fees and points. The broker said I am “locking the whole rate sheet” so I may switch to 30 fixed, buy the rate down a little, or reduce the DP to 20%.

Your valuation chart is very

Your valuation chart is very ‘valuable’ (ha, ha), Rich. To me, it clearly illustrates how out-of-bounds current home prices are relative to income, and, thus, how unsustainable current home prices are.

Me, I think we are going back to pre-FIRE economy norms, and I now place great weight on pre-1985 home price/income data as a guide to where we will return.

I think interest (and

I think interest (and mortgage) rates are going higher.

The Petrodollar system, which kept U.S. dollars from coming back home and circulating – and causing massive rises in consumer prices — looks like it is coming to an end, and maybe soon (one year? two years?). Saudi Arabia’s warm welcome of Putin in a recent visit is a sign of such to me, along with the Saudis moving to join the broadening BRICS alliance. India, European countries, and others are now buying Russian oil with home currencies or the ruble, bypassing the USD.

Russia has demonstrated a military that is second to none, with technologies and tactics that are years ahead of anything in the West, to wit, its use of unstoppable hypersonic missiles (9K MPH!) in its ‘special military operation’ in Ukraine. (Horrifically, one estimate is that Ukraine has suffered 200K KIA to-date). The West has received hints of Russia’s technological supremacy over the past 10 years, with the Iranians intercepting and landing an advanced U.S. stealth UAV 10 years ago (I presume the result of joint Russian/Iranian electronic warfare development), and the multiple, poorly explained loss of propulsion or control incidents with U.S. Navy warships in the Black Sea (Cook) and Western Pacific (McCain, Fitzpatrick), which some have plausibly attributed to Russian/Chinese electronic warfare efforts.

To me, it appears that U.S. military dominance – which implicitly underlies the Petrodollar ‘system’ – is on its last legs. And, the world clearly saw – with Western confiscation of Russia’s foreign reserves held in the U.S. and Europe – that the West is a fickle custodian of its ‘enemies’ assets. That, of course, tempers enthusiasm for buying more U.S. Treasuries, or even maintaining a current stash.

During these past five years, interest rates were at all-time – in thousands of years of recorded history! — lows. I do not know of a large-scale, purposeful use of negative interest rates happening before, as was done in select European countries.

To me, it appears that our Federal Reserve bank note system, with its wildly accelerated emission these past 15 years, is finally bumping up against the hard reality of rising consumer prices stateside, falling dollar use overseas, and implicit threat of dumping of Treasuries by adversaries such as China and other BRICS+ nations.

That is why, going forward, I only see interest (and mortgage) rates moving higher.

Well, that’s one hell of a

Well, that’s one hell of a rabbit hole. You and I read some dramatically different news feeds, but at least they still point to the fed raising rates a couple more times this year. I don’t see home prices getting much of a chance to flatten out until the Spring selling season kicks in.

Glad I wasnt the only one

Glad I wasnt the only one thinking that. And agree, we had a pretty hefty drop and should creep down until that spring brings back eternal hope

https://www.redfin.com/news/h

https://www.redfin.com/news/home-sellers-drop-prices-july-2022/

50% of homes for sale in San Diego had a price drop in July.

“ Russia has demonstrated a

“ Russia has demonstrated a military that is second to none, with technologies and tactics that are years ahead of anything in the West”

OK Boris, time to put away the Stoli.

What did you drink or smoke

What did you drink or smoke before writing this?

John S. wrote:

To me, it

[quote=John S.]

To me, it appears that our Federal Reserve bank note system, with its wildly accelerated emission these past 15 years, is finally bumping up against the hard reality of rising consumer prices stateside, falling dollar use overseas, and implicit threat of dumping of Treasuries by adversaries such as China and other BRICS+ nations.

That is why, going forward, I only see interest (and mortgage) rates moving higher.[/quote]

ever consider the reason interest rates were low is because of baby boomer demographics???

as an undergrad @ UCSD became aware of looking at demographics as a way to make sense of the world,… and as I see things Peter Zeihan has the best big picture analysis out there!

https://www.youtube.com/watch?v=IGvsHqvtJfA