Let’s do a quick check-in on San Diego housing valuations:

Valuations have risen a bit in 2014, but haven’t changed

substantially since I reviewed them earlier this year. Thus, the

conclusions I made in that update

— about what this all means and so forth — remain. I’m far too

slothful to rehash them all here, so please so that prior

installment if you missed it the first time around.

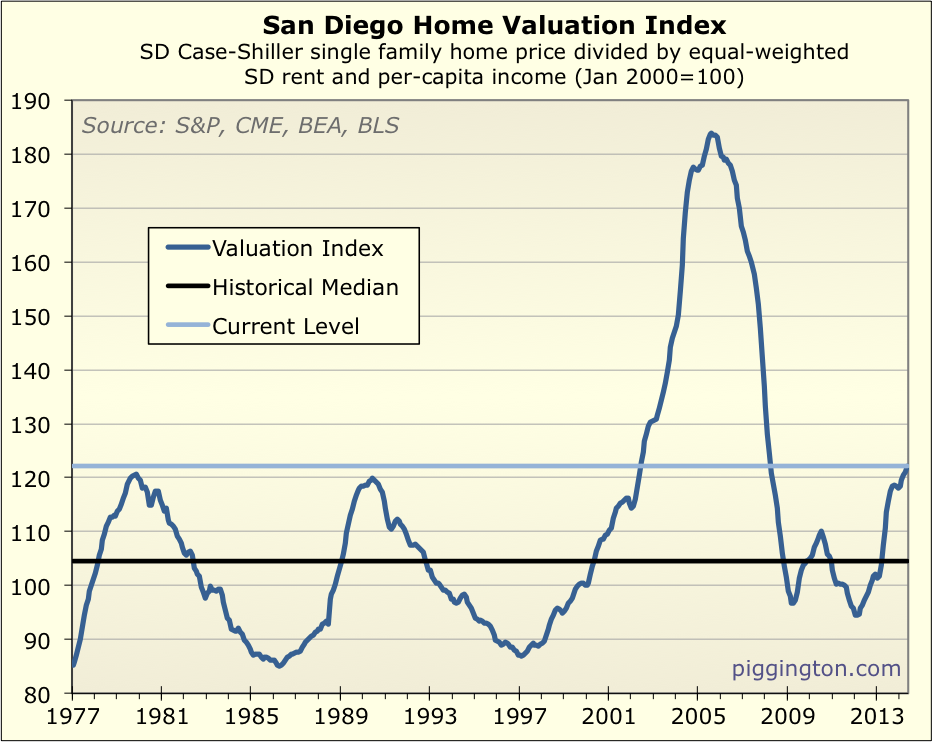

What’s new this time is that current valuations — how expensive San

Diego homes are compared to local rents and incomes — are 17% above

the historical median, a level that surpasses the 1979 and 1990

peaks. That is to say, in the history of the data I have, San

Diego housing is now more expensive than it has been at any time

outside the late, great housing bubble. Fun!

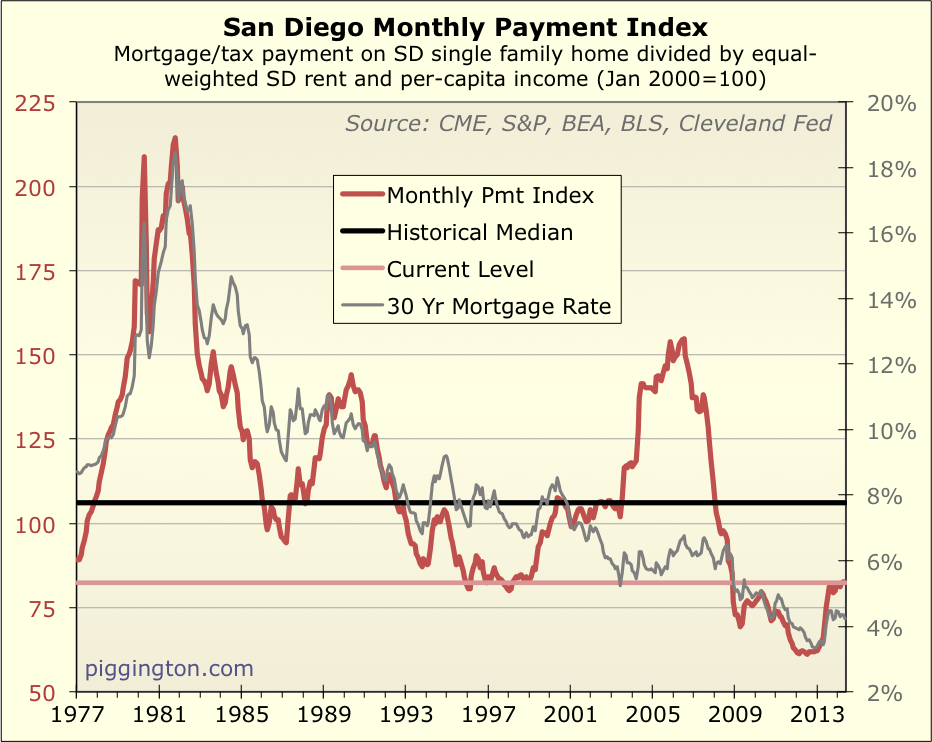

In my view, unusually low mortgage rates are playing a major role in

keeping valuations aloft despite a not-terribly-robust economic

backdrop. Nothing’s changed there: thus far in 2014, the small

valuation increase has been entirely offset by a decline in rates.

Monthly payments (as compared to rents and incomes) may have clawed

their way out of the abyss to some degree, but they are still quite

low compared to decades past:

So there’s that going for housing, for as long as it lasts (which is

a subject of considerable debate).

It’s worth bearing in mind, though, that the valuation series shown

in the first graph has been highly mean-reverting across a wide

variety of interest rate climates. Rates come and go; in my view,

the fundamentals such as rents and incomes are the more important

factor in determining whether homes are over- or under-valued on a

long-term basis. And right now, those fundamentals say that San

Diego housing is the most overpriced it’s been outside of the

mid-2000s bubble.

Fascinating. Most overpriced

Fascinating. Most overpriced outside that huge bubble.

Not to sound like a guy with a lot of his assets in real estate but…

The highly-mean-reverting valuation series shown in the first graph could revert to the mean through rising incomes and rents, rather than through falling prices. (Holds breath, crosses fingers, peers out through one squinted eye, and waits).

Hopefully it will be a bit of

Hopefully it will be a bit of both.

zk wrote:

The

[quote=zk]

The highly-mean-reverting valuation series shown in the first graph could revert to the mean through rising incomes and rents, rather than through falling prices. (Holds breath, crosses fingers, peers out through one squinted eye, and waits).[/quote]

Well, it’s happened before! (In the 80s). In any case, the squinting should help… 😉

If the squinting doesn’t

If the squinting doesn’t help, there’s always sell! sell! sell!

Not that there’s any obviously both decent-yielding and safe alternative investments these days. If there are, someone should tell me about them.

Sell! Sell! Sell! would be

Sell! Sell! Sell! would be interesting to watch. Here’s hoping…

Were the 1979, and 1990 peaks

Were the 1979, and 1990 peaks bubbles? If they were does that mean we’re now in a bubble? 🙂

Probably not bubbles, just

Probably not bubbles, just part of a normal economic cycle.

spdrun wrote:Probably not

[quote=spdrun]Probably not bubbles, just part of a normal economic cycle.[/quote]

So “San Diego housing is now more expensive than it has been at any time outside the late, great housing bubble.” is part of a normal economic cycle”?

Jazzman wrote:Were the 1979,

[quote=Jazzman]Were the 1979, and 1990 peaks bubbles? If they were does that mean we’re now in a bubble? :)[/quote]

I discussed that very question at length in the prior installment: http://piggington.com/shambling_towards_affordability_san_diego_housing_overpriced_but

(halfway down: “Bonus Nerd-Out: Is Housing In a Bubble?”)

So “San Diego housing is now

We’ve so far matched the 1979/90 peaks, not really surpassed them when you take margins of error into account.

Yes, I know. Just having a

Yes, I know. Just having a bit of fun here. Talking of over-priced, or over-valued homes, Oahu (Hawaii) is in a bit of a pickle. You might want to hire out your services to them Rich. Your Himalayan graphs would spook everyone. There’s a big move to build upwards (high rise) and urbanize around a rail link. This means shops, facilities within walking distance of dwellings in an attempt to reduce sprawl and cope with growing numbers more effectively. Some argue the island has reached saturation point in every habitation sense, and that people should start leaving. Others predict home price appreciation will reach an average of $1m in a few years for a SFH if current unaffordable levels keeping rising at the same rate. Home prices are a joke there. The catalysts for change are home prices, transportation infrastructure built around the car, and exponential growth. All very symptomatic of modern day living, and will eventually effect other major urban areas and conurbations to one degree or another. Bubbly (frothy if you don’t like bubbly) home prices in my home town of London have not only caught the attention of the Bank of England, but even the PM has come out and said it is a concern. I think people need to wake up a little, and realize that sharp increases in prices so soon after a crash and while in a delicate economy is not something to be jumping up and down over.

I think people need to wake

Ding! Ding! Ding! We have a winner.

But it does pay attention to

But it does pay attention to larger cities like LA.

There is a financial squeeze on most large cities right now (In TX as well).

Taper will only last as long as housing continues to show price gains IMO.

Well then: here’s hoping that

Well then: here’s hoping that housing creeps up till October, then we see a beautiful correction. Should take 6-12 months for the Fed to get its act together on a new QE. Meanwhile, par-TAAAAY time, BABY! Similar to what happened in 2011 to mid-2012.

But as I said, as long as the national average is flat or slightly rising, a single region will be seem as an anomaly.

BTW – TX is a different case. Housing prices are at all-time highs, but it’s been a gradual rise since the 1990s with no real bubble in the mid-2000s. Perhaps their low-tax policies combined with costs due to growth are coming to haunt them. Fortunately, property taxes in TX aren’t capped at a % of value, and millage rates can be adjusted as needed.

The bigger cities in TX are

The bigger cities in TX are becoming Los Angeles they just don’t know it yet LOL.

I know someone who bought a 300K home just outside Dallas and is paying over 16K a year in property tax.

They got to get it somewhere.

Exactly. And if the value of

Exactly. And if the value of his home drops to $250k, he’ll still be paying $16k/yr since the city will raise the tax per unit of assessment. Not a problem like in CA.

That’s TX’s dirty secret, BTW. Low income taxes. Low corporate taxes. High property taxes. Great if you’re high-income with an unspectacular property, less good if you’re middle-income with a $300k house.

Does TX law still require 20% down on residential mortgages or has that changed in the last ~10 years?

Property tax in Texas are

Property tax in Texas are about 3%, at least that’s what I pay for a SFH in Dallas. And there really wasn’t a bubble to speak of; property taxes may be having something to do with that. If I sold now, I’d just about cover my sales costs.

Rising home prices are being touted as the key indicator of a recovery, and one reason given is that it lubricates sales by reducing negative equity. However, that hasn’t happened, at least on a grand scale you need for a recovery. In fact, sales are now in reverse. It also ignores so many other factors, such as the mini-bubbles being created (the uneven effect regionally), affordability issues, and not least the net effect of creating a grand illusion that everything is happening as it should. For those reasons, I don’t believe tapering is dependent of home prices, and that interest rates will rise next year, but probably not enough to cause huge waves.

We’re in this for the long haul, so the silent minority of fixed incomers will continue to suffer, sales will remain depressed, and long term appreciation stagnant. When, and if mini bubbles pop (fizz), FTBs will again become frustrated by competition from yield chasers, investors, cash buyers, and will remain on the sidelines longer, further burdened by other personal debt.

Not sure the exact specifics

Not sure the exact specifics but it you buy a home in TX make sure it either a working farm/ranch or has a very small lot, that is the advise I was given.

Is your graphs/data only for

Is your graphs/data only for San Diego City or San Diego County?

I’ve been watching the market for a while now, looking to purchase.

How can it not be compared to the bubble of 2005?

I’m looking in West Lakeside, Santee, El Cajon, Lemon Grove, and East La Mesa (geographic limitation due to children). I’m seeing 2/1, 3/1 and 3/2 homes (at ~1000 sq ft…or less) listing and selling for $350-$400k!!!

If you look at the public records, many of these houses sold for the same price in 2004/2005, then forclosed and sold, now selling for similar cost in 2014.

sd_rider wrote:Is your

[quote=sd_rider]Is your graphs/data only for San Diego City or San Diego County?

[/quote]

County

[quote=sd_rider]

How can it not be compared to the bubble of 2005?

I’m looking in West Lakeside, Santee, El Cajon, Lemon Grove, and East La Mesa (geographic limitation due to children). I’m seeing 2/1, 3/1 and 3/2 homes (at ~1000 sq ft…or less) listing and selling for $350-$400k!!!

If you look at the public records, many of these houses sold for the same price in 2004/2005, then forclosed and sold, now selling for similar cost in 2014.[/quote]

You answered your own question. You are comparing prices to 9 or 10 years ago — an entire decade during which inflation, incomes, and rents have been rising pretty much all along. So something selling for $400k now is a completely different situation, valuation-wise, from something that was selling at $400k in 2004 or 2005.

I don’t have the numbers for

I don’t have the numbers for SD Co, but median income in the US hasn’t risen much since 2004-5. If rents have risen, perhaps that means that they’ve gotten out of whack with incomes, meaning that a rent bubble exists.

spdrun wrote:I don’t have the

[quote=spdrun]I don’t have the numbers for SD Co, but median income in the US hasn’t risen much since 2004-5. If rents have risen, perhaps that means that they’ve gotten out of whack with incomes, meaning that a rent bubble exists.[/quote]

I don’t know what you mean by “much” but national income has absolutely risen since 2004-5. Here’s a graph from the beginning of 2004 showing that the median hh income has risen about 15% since then.

http://research.stlouisfed.org/fred2/graph/?g=C05

You are right that SD income has fared better than nationwide though… SD per capita income is up about 25% since 2004.

I know this has been brought

I know this has been brought up by Rich and others as well, but rents compared to a mortgage with 20% down in a lot of areas is more expensive according to a lot of articles and news reports I’ve seen.

I don’t think we will see any large correction until either rent goes back down or something crazy happens. People aren’t going to be selling their homes at a discount when they can rent them out for a lot more than their existing mortgage.

This is also why homes aren’t being listed because many people (anyone who bought in 2009-2011) can easily cash flow their home since they bought at a low point and probably were forced to put enough down to buy to begin with.

I know I wouldn’t be able to afford buying anything now, but doing a quick craiglist check in my area, rents are still insanely high.

Another point to add is I think for a lot of areas, the “median income” earner is simply not supposed to live there. This is true for many areas in CA and San Diego as well…

If you make median income, you are not supposed to be able to buy here.

Assuming that a sizable

Assuming that a sizable portion of sales are to people who want to rent homes out, at 5% rate (7% incl. principal repayment), renting the homes out at current prices would simply not make sense. This would knock the wind out of that part of the market.

spdrun wrote:Assuming that a

[quote=spdrun]Assuming that a sizable portion of sales are to people who want to rent homes out, at 5% rate (7% incl. principal repayment), renting the homes out at current prices would simply not make sense. This would knock the wind out of that part of the market.[/quote]

You’re assuming facts not in evidence. San Diego has almost never been a great market for single family landlords from a cash-flow standpoint. There have been some good periods to buy as a landlord, and some good neighborhoods to do so. But for the most part, it hasn’t been. That’s why the big PE real estate investors mostly stayed away. Prices too high, rents too low. (Anectdotal evidence that someone made a great buy with good cash flow is NOT data.)

^^^

I’m assuming (correctly)

^^^

I’m assuming (correctly) that the current mini-bubble has been driven by buy-to-let investors, at least for condos. Not by organic demand.

spdrun wrote:^^^

I’m assuming

[quote=spdrun]^^^

I’m assuming (correctly) that the current mini-bubble has been driven by buy-to-let investors, at least for condos. Not by organic demand.[/quote]

Though I disagree with calling it any kind of bubble, you could be right, but that’s why I said single family homes. The big investors stayed away from the SD single family home market despite buying significant numbers of properties in the inland empire. It just doesn’t pencil out very often.

I believe timber property is

I believe timber property is taxed the lowest in Texas, so buy some property with trees on it if you can find any!