Sorry if the title sounds hyperbolic, but… wow, it’s true.

As of March, the market was blazing (to continue with the

heat-related metaphors).

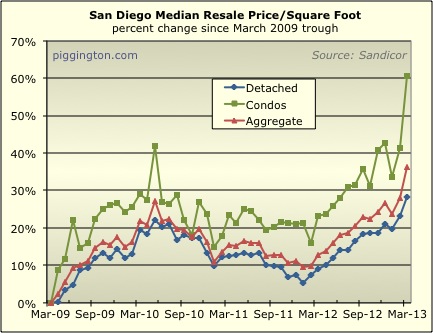

Let’s start with this graph of the median price per square foot

since the 2009 trough:

OK, you can probably ignore the huge spike in the condo psf, as the

condo series tends to be all over the map. But how about that

(much more reliable) detached home psf — up 4% for the month, and

18% year-over-year.

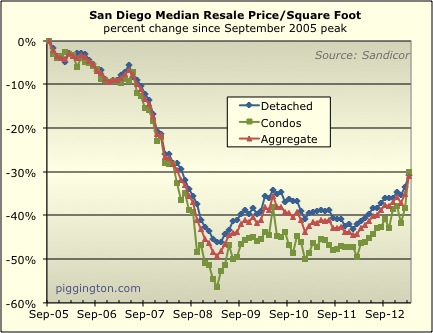

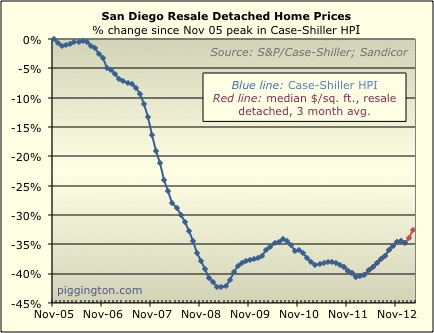

Here’s how it looks from the peak:

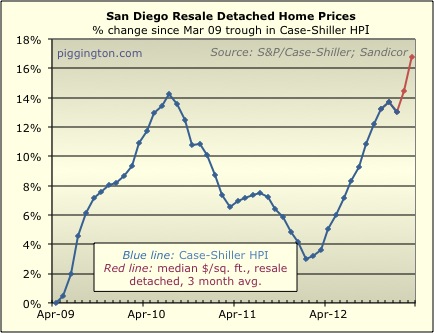

Here’s the “predicted” Case-Shiller price index, based on three

months of single family psf’s:

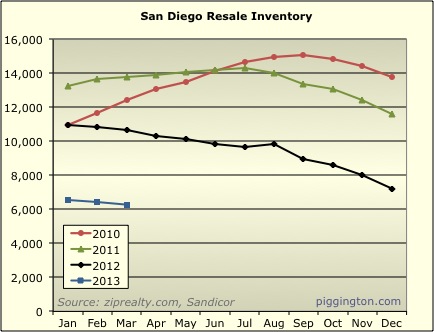

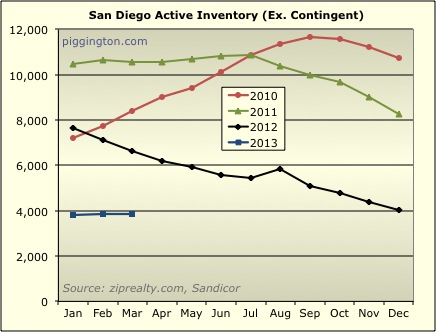

The culprit for this recent and accelerating price surge is the

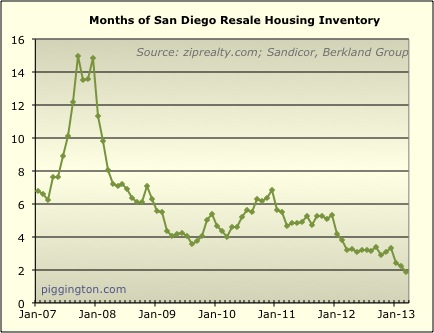

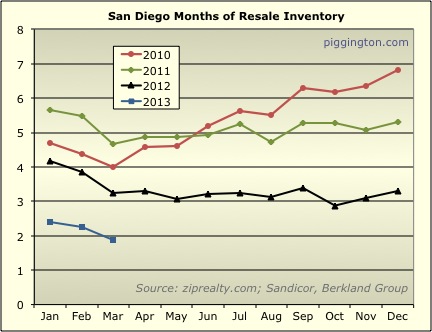

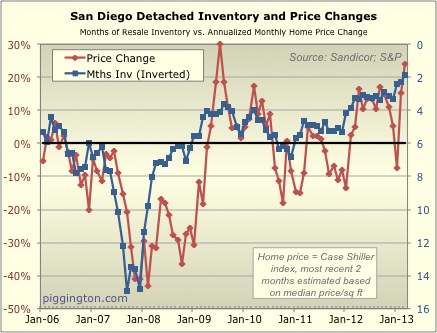

unbelievably low level of inventory…

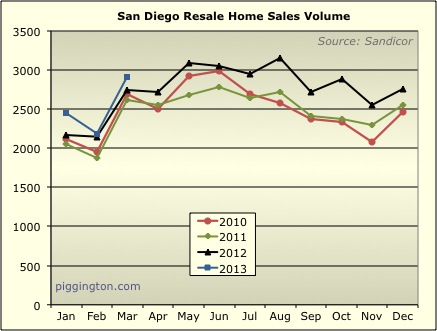

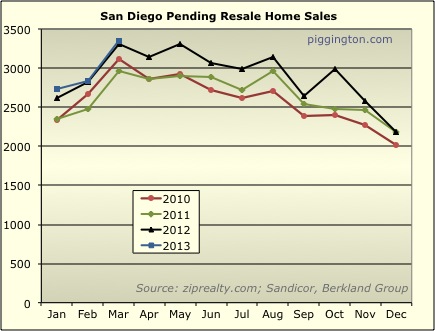

…against the strongest March demand in years:

…which combines to plunge the all important “months of inventory”

figure into the abyss:

I refer to the month of inventory ratio as “all important” because

it measures how much supply there is compared to demand, and has

historically been correlated very well with short-term price

pressure as seen in the following graph:

Months of inventory just reached a low (for the period of time for

which I have data), and the monthly change in single family home

prices was the second highest ever. Not a coincidence.

The ratio isn’t a perfect indicator (there isn’t such a thing), but

it makes sense that it should work this way, and historically, it

has. The new low in months of inventory implies more upward

price pressure ahead.

I’d be interested in people’s thoughts: why do you think is

inventory so low, and what might cause that to change?

One reason inventory is low

One reason inventory is low is momentum. People don’t want to sell because they don’t know if they can find a place to buy after selling their residence. i.e. people don’t list their house because of the low inventory.

In CV, I think people are selling their over-sized properties and hanging on to smaller properties.

People see some momentum in the market and are waiting until they can get their prices before selling. Seeing all the people listing houses waaaay over market (even waaaay over market after the market has risen) suggests this. The people who list are just bolder and less realistic that the people who are still waiting for higher prices.

I used to think that higher prices would bring the inventory and higher rates would stifle the buyers, but I think the opposite is true in the short term.

If we see prices start to come down, the sellers will come out in droves, trying to catch the top. As long as prices are coming up, why sell when you could get more later ?

Buyers saw rates come up and went into a panic trying to buy before the rates priced them out of the market. Rates started coming down, which I think will cool buyers just a bit.

Well Rich, speaking strictly

Well Rich, speaking strictly for prospective “equity sellers” who have owned the same property in excess of ten years and have never been “in distress,” I can honestly say that they want to be certain that they will be able to recover from “lender malaise” should they decide to list . . . that is, be able to recover from those sold-comps from their respective micro-areas which often were not high enough to even represent even the land value of said lot (mostly due to the closing of non-arms-length short-sales) … or occasionally from an REO sale where the (sometimes) foreclosing second-TD lender didn’t spend anything to ready the property for sale.

As you know, landscape, hardscape, fencing and termite work is costly, as well as interior repairs and replacements of both cosmetic enhancements and internal systems.

Today’s sellers of resales need to be confident that they will be reimbursed upon COE for 50 – 75% of the above cost upon sale (over and above the price they paid for the property), depending on when they purchased it.

Otherwise, there is no reason to list.

We are above peak pricing in

We are above peak pricing in west Encinitas.

http://encinitasundercover.blogspot.com/2012/11/the-bubble-is-back-encinitas.html

Thank you for confirming

Thank you for confirming statistically what I have been saying for awhile now. So far this year is poised for the sheer jump in annual pricing.

As we have discussed, the real mystery is the lack of inventory. I think there are several factors involved. As dude noted the greed factor is one of the issues keeping sellers on the sidelines. However I disagree that any sort of avalanche of inventory will occur when prices level out or even drop some.

Another factor is the hangover effect from the way that the downturn is handled. Those with principal reductions are pretty much locked into where they live. Remember when you modify the principal then it is done. Anything above that modified amount goes back to the bank. In fact there may also be back interest collected as well on a sale where profit “was” to be made. So forget about seeing those people move. The same is true in one form or another for those who had modifications made with regards to simply lowering monthly payments.

I think we are also seeing a more universal acceptance that finding a haven, any sort of haven from future interest rate shock is becoming important for people. While the equities markets have been flying high the element of risk is always there with equities. Rents may dip but never crater. Even at the worst of the housing market crash I don’t believe rents declined more then 15% at most. For my personal residences I know this to be true.

Let’s not forget about lending as well. There is no private secondary market and basically the ENTIRE secondary market is and has been the GSE’s for the past 6 years. While underwriting guidelines have been followed in a more strict manner, IF you have strong proof of income you WILL get the loan. Low downpayments have never gone away and are more possible then ever. Again, it is simply about proof of income and a good income history.

So when does it slow down? There are two things that can slow the market down. The first is interest rates. Unfortunately this will not happen in the short run. In the long run it will happen but long maybe be a year or two or five or ten. You just don’t know.

The second and more probable in the short term is that the price to income ratios will whittle away the buyers pool over time. That will normalize the pricing in various areas and you will see inventory accumulate and depreciation slow. You may even see a dip in pricing but that is expected and is not indicative of a market turn, but is simply expected as things normalize. Once more you will have more subdued appreciation rate as inventories find levels closer to previous annual averages.

This is from Zip Realty:

This is from Zip Realty:

“Why is the inventory so low? There are multiple reasons.

Foreclosures are back to historic norms (at least in Southern California)

The back-up of properties tied up in short sales have, or are in the process of, come to final sales.

There is a lot of cash in the marketplace right now. Money from China and Europe are looking for someplace to park their money, so they buy a property and turn it into a rental. Before this, most of the cash buyers would improve the property and then put it back on the market for sale.

Owners who would have to short sell right now are looking at the rising prices and waiting to sell until they won’t have to do a short sell and can sell their home normally.

What would have been move-up buyers when they sell their existing home don’t have enough equity in their current home to purchase a new home, so they are staying put.

Because the rental market is so strong, people who would have to short sell their house are instead moving out, renting that house and then renting a smaller house – reducing their monthly cash outflow and essentially keeping two potential sale properties out of the market.

Also because the rental market is so strong (and also their low equity position), people who are moving away are renting their properties instead of selling them.

There is very little new construction. Historically, new homes accounted for about 20% of inventory. That’s now around 4% or less. There is very little developable land in San Diego, and development/construction financing is very difficult to get.”

That is a great question, why

That is a great question, why is the inventory so low? I’m a long time reader here and do respect the opinions of those with much more experience than I in the housing market, but I’m starting to get flashbacks of 2004 when “everyone” (piggs not included) had a big list of reasons why prices kept going up, many of which Rich covered in the past. However, not many of them included 100’s of thousands people including buyers, sellers, inspectors, loan officers, wall street bankers, rating’s agencies, etc out right lying and manipulating the entire system.

Looking at this from the 30k foot level, if inventory is really that low compared to historic norms going back decades when is the point where the levels become so low percentage wise it is more likely to be shady dealings then many small innocent factors? I’m not a conspiracy theorist but watching the inventory go down since 2009 is starting me make me think someone needs to follow the money and figure out what’s really going on?

Yeah, I’m getting flashbacks

Yeah, I’m getting flashbacks to 2004 also. But in a different way.

I have an answer to at least part of your question. Why is the inventory so low? Because if you don’t need to sell, you feel like a fool for selling while prices are obviously gapping up. You think of what you could be getting had you waited for a couple of more months, or till year, or whatever. You think that maybe it wouldn’t be so bad to be a landlord for a couple of years, wait for the peak prices to come in and then sell. (Yeah, nobody can perfectly time the peak, but we’re talking emotions here, not pure logic).

I say that because I’m currently living that experience. Just put my home on the market and I’m already getting seller’s remorse.

A young couple just bought

A young couple just bought house next door which is mirror image to mine, except a little smaller. They paid 30% more what I paid two years ago (25% if you subtract the costs of the upgrades). Their story is familiar: they kept getting out bid, usually by people with all-cash offers, so they started bidding 5% – 10% above asking price.

I remember inventory in the neighborhood back when I was looking was around 100 SFR. Now it’s below 50.

People want to buy houses. Rates are low, the loans are affordable and rents have gone up. There’s something about making offers over and over and being outbid over and over that makes you see red and more willing to raise your “limits”.

I’m actually somewhat concerned. Prices going up is good for me as a home owner, but this all seems too fast too soon. Where’s the new construction? Where did all the flippers go? Is there simply not enough flippable inventory? Higher prices without increasing inventory seems like a huge lost opportunity for jobs and a healthy check of the market.

It’s not uncommon for an

It’s not uncommon for an oversold stock to “Gap up” significantly on a good news catalyst. I think we are seeing that situation play out with housing right now. The housing market over corrected and now that the weakhanded holders have sold (or were foreclosed on) there is no one left to sell at these prices and the market is rapidly adjusting to a level where current holders will sell.

In my opinion, the next wave of inventory will come from the investors that purchased in 2009-2010 and are looking to cash out. If they don’t sell and rates remain low, then we could see bubble prices very soon.

Also, anti-foreclosure laws

Also, anti-foreclosure laws (aka California Homerenters’ Bill of Wrongs) have something to do with the weak-handed holders not HAVING to sell, at least not immediately.

I think an important question

I think an important question to ask is … are sellers holding off because there is something about current socio-economic circumstances that has reduced the “need” for people to sell who may have needed to sell under different socio-economic circumstances ? Or is it just the upward price movement ?

Why do people sell in the first place ? They move/change jobs, move-up purchase, empty-nester move-down, divorce, death, mortgage trouble, decide to rent (rare, I’d guess), selling a speculative/income/second property for profit.

The last one is a price-related decision anyway and I don’t know of anything that would mean fewer people in the other situations now. As I mentioned before, the low inventory itself puts off move-up/move downs.

So I have to assume it is the upward price movement that is delaying seller listings, which leads me to the conclusion that pent-up supply is building. Not necessarily enough for a crash, but enough for some kind of let-off, perhaps?

This could happen in a couple of months or a couple of years and could be triggered by those pesky macro-economics.

Let’s assume upward price

Let’s assume upward price movement is delaying seller listings and causing pent-up supply. If that’s the case, I’d argue that a greater amount of pent-up demand is also building. The pent-up supply from your typical move-up/move-down buyer is equally offset by pent-up demand caused by a lack of inventory — sell one house to purchase another (this is a conservative assumption as many move-up buyers will keep their current homes as investments especially if they refinanced into a sub 4% interest rate). If you then consider the demand from those who want to buy but can’t due to lack of available inventory, you have a scenario where pent-up demand > pent-up supply.

skerzz wrote:Let’s assume

[quote=skerzz]Let’s assume upward price movement is delaying seller listings and causing pent-up supply. If that’s the case, I’d argue that a greater amount of pent-up demand is also building. The pent-up supply from your typical move-up/move-down buyer is equally offset by pent-up demand caused by a lack of inventory — sell one house to purchase another (this is a conservative assumption as many move-up buyers will keep their current homes as investments especially if they refinanced into a sub 4% interest rate). If you then consider the demand from those who want to buy but can’t due to lack of available inventory, you have a scenario where pent-up demand > pent-up supply.[/quote]

That’s valid. It’s complicated a bit by seasonal factors, but a valid point, yes.

Lots of investors buying to rent, though. Eventually some buyers decide to go that route and rent instead of buy.

I wouldn’t agree with SD

I wouldn’t agree with SD Realtor that: “low down payments are more possible then ever”. They were MUCH more possible from ’03-’07 when like 50% of purchases were ZERO down stated income. Now at least you have to put 3% down. And FHA has increased mortgage insurance recently and also the mortgage insurance now stays for the life of the loan if you put <5% down, so I wouldn't say it's getting easier to put less down. It's actually getting much more expensive to put less down.

The last bubble we all know came from easy lending standards and stated income, so house prices were not tied to local incomes. Now house prices are pegged to local incomes because buyers have to qualify based on their income. So if prices went up 20%+ year over year in SD this year, they can't do that many more times or people flat out will not be able to qualify for loans. Prices will be pegged to incomes. I know there are cash buyers, but there is a limit to cash buyers. The higher prices go, the less cash buyers there will be.

I know that doesn't answer the question where inventory will come from, b/c frankly I don't know nor do the best minds in the real estate business. I'm guessing once prices level out based on maxed out local incomes, more supply will come on and in a few years builders will be able to fully build out large new subdivisions (at least in places like Riverside Co.).

I think maybe the mystery to

I think maybe the mystery to why the inventory is so low is ignoring the obvious. Houses ARE selling. There is no shortage of conventional sellers today as compared with other times. Nationally anyway, conventional sales are up sharply from a year ago, and up even more from 2 years ago. We’re close to the sales rate during the silly housing credits from a few years ago. Distressed sales are way down in most markets, though they still remain pretty high in others. Inventory is down because homes are selling faster.

Anyone have any numbers for historical average DOM? I looked at a couple zips in SD, and the current averages were under 50 days, which seems incredibly short. I suspect this is far below historical numbers.

I I think that DOM is

I I think that DOM is misleading right now due to the variations. You have the hungover short sales that are taking months still. You have the non distress sales that are taking days. 50 days is a quick DOM but in reality homes are going from active to pending in a week or two at most if they are priced anywhere near comps.

From the comments here, this

From the comments here, this is what I gathered for the possibly reasons for lack of supply:

1) Home owners that bought during the bubble and couldn’t afford their homes but were fortunate enough to get loan modifications don’t have incentive to sell

2) Home owners that bought during the bubble and could afford their homes don’t want to sell until they are no longer under water (need down payment for new home)

3) Lack of new construction.

4) Greed / momentum, although this would seem to at least initially be a secondary reason since something would first need to cause the price trend.

5) Slightly higher sales volumes over the last year driven by low rates

If there isn’t an obvious reason, maybe its a combination of several.

The answer to lack of supply

The answer to lack of supply is complex but there is also a local twist to it:

Qualcomm

whose Nasdaq market cap is bigger then CSCO and INTC, is headquartered here in SD, they are hiring like crazy and it is pulling up the RE market locally.

For SD I think it’s all about

For SD I think it’s all about QCOM right now.

The closer the home is to QCOM the hotter the market.

The-Shoveler wrote:For SD I

[quote=The-Shoveler]For SD I think it’s all about QCOM right now.

The closer the home is to QCOM the hotter the market.[/quote]

I doubt it. The size of the county compared to QCOM’s size make that virtually impossible.

Low interest rates are

Low interest rates are causing both speculators and owner-occupants to compete for what few listings there are. IMHO, the world’s central banks are distorting the market, and the longer it goes on, the worse the eventual outcome will be.

Like others have mentioned, those who want to move up/down can now refinance into a very low mortgage and rent the house out for close to break-even, if not a positive cash flow. In the past, many/most of these homes would have been sold first, but it makes more sense to just rent them out now. For as long as rents remain stable, there is little reason for these houses to hit the market.

And then we have all of the manipulations that have been going on for years, where deadbeats are (still!) living in houses without paying for them, and/or getting loan mods which make it affordable for them to stay put. That, and the fact that people see housing as a no-lose bet; the Fed/govt have proven that they will do anything to keep the housing market from correcting naturally.

IMHO, this is still a credit-driven asset price bubble. If interest rates rise for an extended period of time, things will get ugly. Of course, that may not happen in our lifetimes. Who knows?

Speculators? What

Speculators? What speculators?

From this thread:

http://piggington.com/dow_15000

[quote=The-Shoveler]Not to be out done,

China Accounts For Nearly Half Of World’s New Money Supply

http://www.zerohedge.com/news/2013-02-08/china-accounts-nearly-half-worlds-new-money-supply

http://www.youtube.com/watch?v=xRnUhcwio7k

http://www.businessinsider.com/china-worlds-fastest-printing-press-2011-1

Add the ECB’s efforts and DANG!!! that a lot of moolah!![/quote]

“Home sellers in greater

“Home sellers in greater numbers are finding they have sufficient equity to consider selling, but continue to be constrained by creditworthiness,” Fleming says in a CoreLogic publication called “The MarketPulse.” …

“It is currently estimated that 45% of all mortgage homeowners have insufficient equity,” Fleming says, to make it worthwhile to sell.

http://www.nationalmortgagenews.com/dailybriefing/corelogic-many-sellers-cannot-qualify-new-mortgage-1035895-1.html

Ed wrote:“Home sellers in

[quote=Ed]“Home sellers in greater numbers are finding they have sufficient equity to consider selling, but continue to be constrained by creditworthiness,” Fleming says in a CoreLogic publication called “The MarketPulse.” …

“It is currently estimated that 45% of all mortgage homeowners have insufficient equity,” Fleming says, to make it worthwhile to sell.

http://www.nationalmortgagenews.com/dailybriefing/corelogic-many-sellers-cannot-qualify-new-mortgage-1035895-1.html%5B/quote%5D

Ed. I can’t see your article because I’m not a subscriber. But the title fits. LOTS of people, especially the semi-retired and retired, can’t qualify for a new mortgage.

The irony of this dilemma is that under *new* FF “guidelines,” a mortgage applicant who can ostensibly pay all cash for their next house often can’t even qualify to borrow $100K in purchase money! Credit scores be damned. What good is an 800 FICO score if one can’t properly “document” their income to the degree required by the GSE’s?

I haven’t investigated lately but the solution probably lies in applying with a portfolio lender if a person in this category wants/needs a purchase-money mtg.

Meanwhile, it is likely this group of potential “equity sellers” is taking their time to list while exploring their options.

The result is the same. Strict mtg lending requirements (indirectly) keep properties off the market which otherwise might be listed. How many is anyone’s guess but I think this problem primarily affects inventory levels in established areas which are more than 30 years old.

If you can actually afford to

If you can actually afford to pay all-cash, 25-50% down mortgages at not much above the GSE rates aren’t all that hard to find.

If you asked woud-be sellers

If you asked woud-be sellers why they’re not listing, you’d get a hundred different answers. If inventory is lowest in the former subprime market, my guess would be an historically high proportion of investors has depleted supply. I seem to remember seeing a conspicuous drop in listings around May 2012.