Something has been on my mind to write about for a while and I’ve got some time. I touched upon it on the Redfin thread but in a nutshell the residential real estate and lending industry is in deep trouble. Having been in the industry as long as I have I was always amused by people thinking the business was great when prices were going up and awful when the weren’t. I had my best years in the “worst years” and my worst years in the “best years”. To the industry home values are mostly irrelevant. The industry thrives on transaction volume.

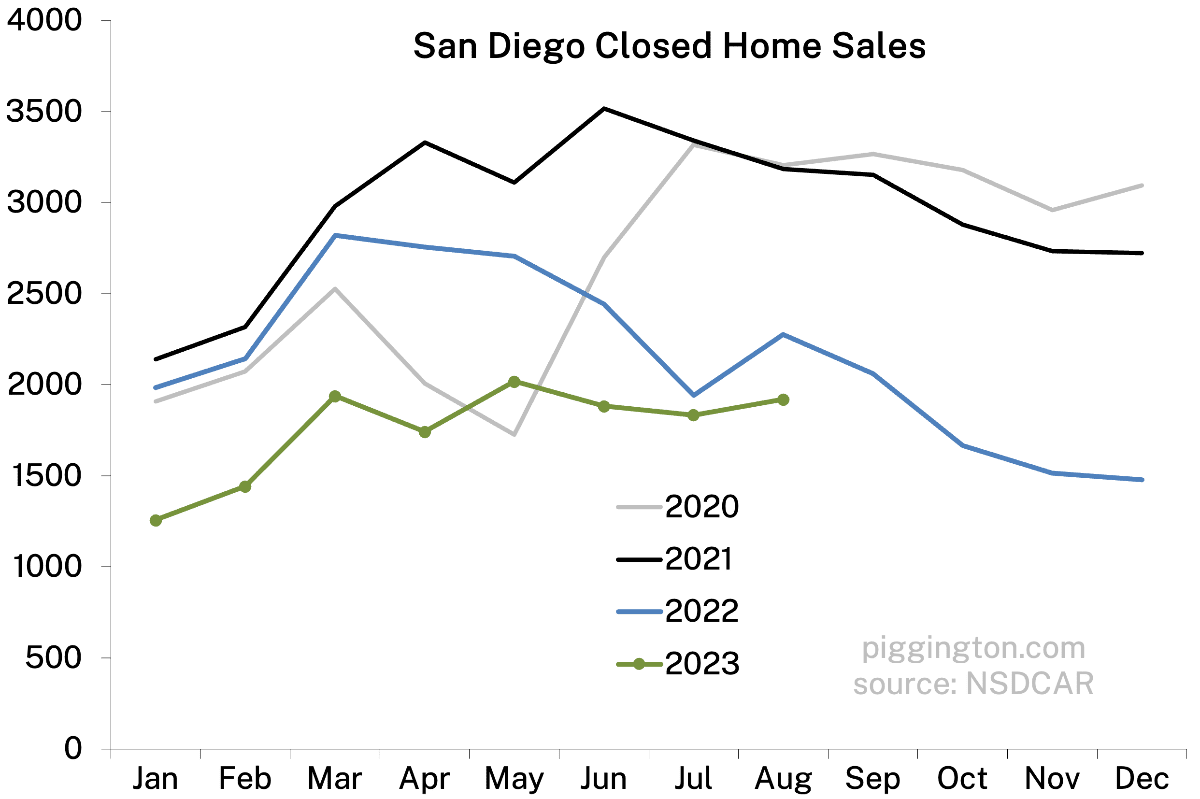

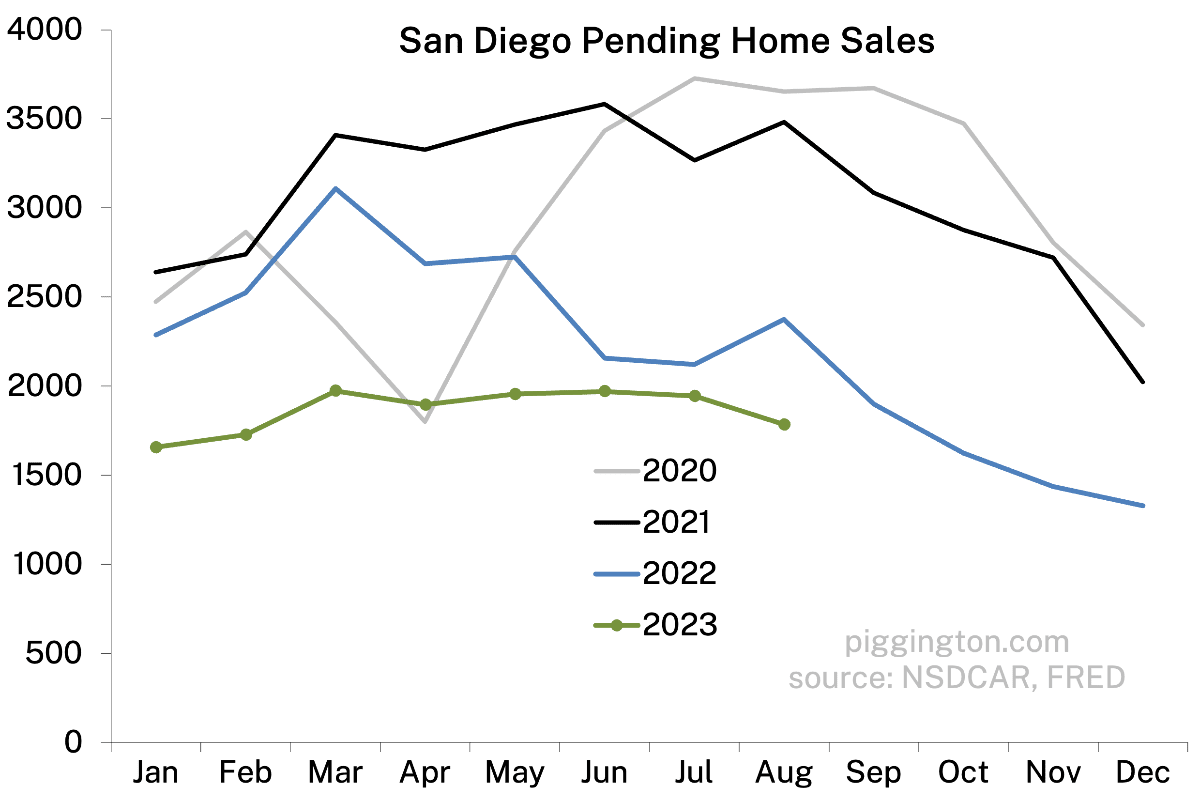

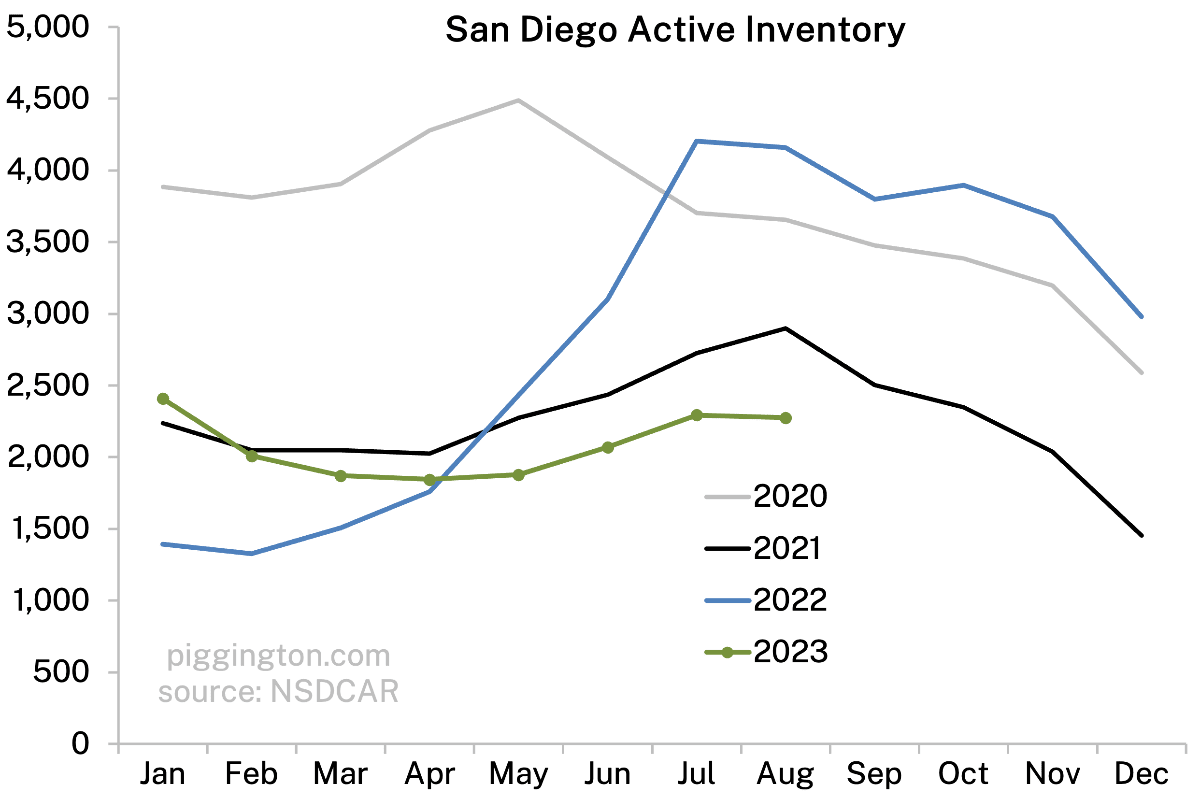

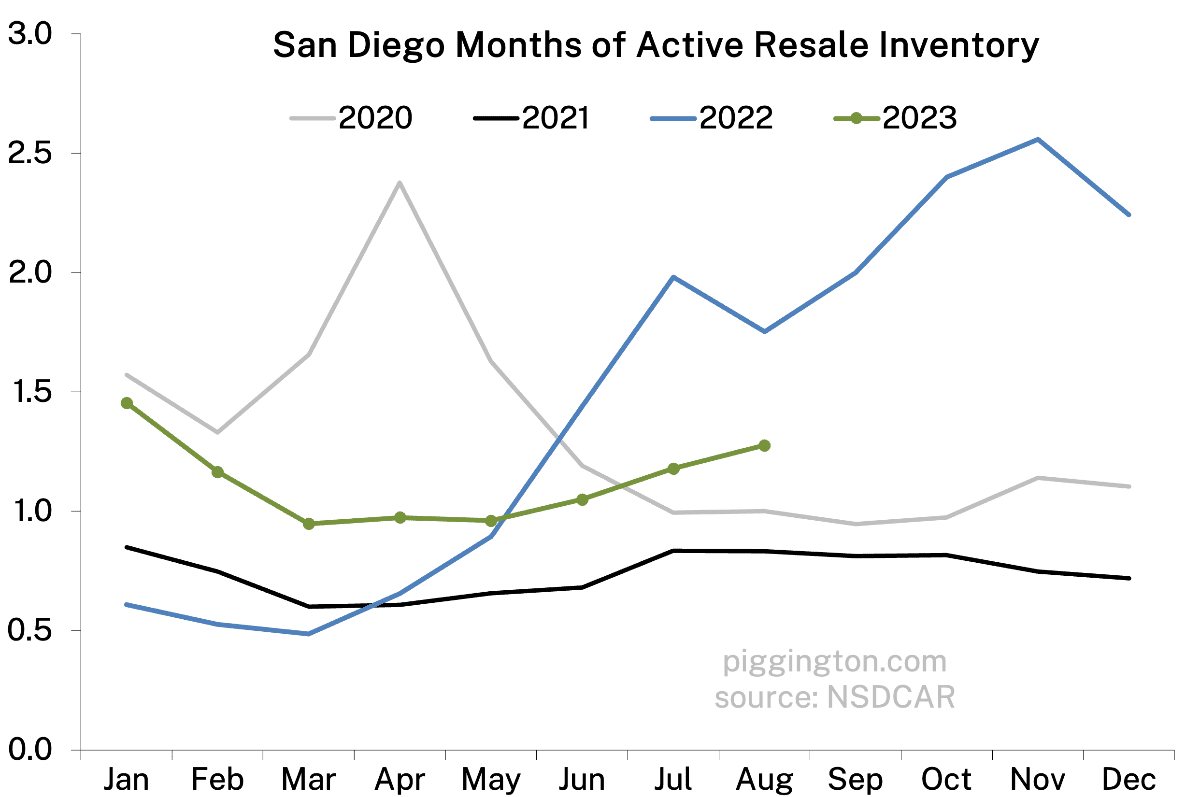

I live and largely follow my local North County Coastal market closest. I ran these quickly without all the clean up of data I do in my weekly reports but order of magnitude is what is critical here. I could look at other or larger areas but the story would be largely the same. Closed sales in my 3 ZIPS for first 8 months

Transaction volume has been steadily decreasing for a long time in an area with a growing population. In 2021 we had an outlier year, a boom with record low rates. But we pretty much should be selling between 750 and 800 single family homes in the first 8 months. Lets call that 100 homes.

Last year we had a very slow year and this year its much slower. We have about 60 homes selling per month.

That’s roughly 40% below what the industry built itself for. Now prices are high and when people get paid they get paid well but there’s a lot less paychecks being distributed among the real estate brokerages around here.

Whatever industry you are in, what would it look like if your employer lost 40% of its business? That’s what I think is coming to real estate.

And lending? That is far worse. The mortgages that are golden handcuffing people into their homes are not being refinanced and many if not most never will be! A couple months ago I had some mortgage volume stats and did some back of the envelope calculations. By my rudimentary calculation their business is down 75 to 80% from what it was. I could be off a bit but not off by an order of magnitude. Its bleak out there now in lending. Now some of that will come back eventually as transaction volumes eventually rise and those who bought with todays higher rates refinance but its gonna be a tough several years out there. Really tough!

Myself? I just look back and feel both lucky and fortunate to have lived the way I did. I spent the last 20 years preparing for something like this. Im fortunate it has no impact at all on me but I feel for my friends many of whom are unaware or unwilling to accept what is coming. I hope there are a lot of Plan B’s out there

Good stats and insights, thanks for sharing. Pretty incredible hollowing out of the business, especially the mortgage side of things.

Per your point about down years sometimes being good years: a recession could potentially help these industries in a couple ways. For one, rates would likely come down, leading to at least some refis and (if they went down enough) also people being released from their rate lock prison. Also, if people lost jobs or relocated that could force more sales and increase volume.

Whatever happens, my non-professional guess is that volume has to get back up there somehow. Like you suggested, these volumes are just too low for a city this size. SD as a whole doesn’t have much of a growing population, I think it was shrinking last I looked but it’s by like 1% or whatever so let’s call it basically flat vs. the massive decrease in volumes. Seems like something has to change… it could be a long process but I don’t think this is a stable equilibrium.

I would agree that it has to change but I think its gonna take 5 to 10 years to get back there. I’ve completed 60 laps around the sun now. I don’t have the inclination or need to wait for it to happen. I’ll keep doing my best for my past clients and those they refer to me. I’m sure I will continue getting my share and doing a great job at that. But the days of looking to aggressively build and expand this business are past for me.

I don’t think that’s a bad call. My time period is not based upon any strong feeling other than this is not going to completely resolve itself in 2 or 3 years. We may see some improvement but I do believe we are looking at a greatly diminished market size for more than a short while. Maybe I’m just a grumpy old man yelling at clouds

John S.

2 years ago

Maybe it WILL be different this time: ?itok=8b5yQQUW

Even more reason to sit tight and not sell. Especially if you have a < 3.5% interest rate. It sucks to be a buyer right now. Not only is it much more costly, there not much to choose from.

Something has been on my mind to write about for a while and I’ve got some time. I touched upon it on the Redfin thread but in a nutshell the residential real estate and lending industry is in deep trouble. Having been in the industry as long as I have I was always amused by people thinking the business was great when prices were going up and awful when the weren’t. I had my best years in the “worst years” and my worst years in the “best years”. To the industry home values are mostly irrelevant. The industry thrives on transaction volume.

I live and largely follow my local North County Coastal market closest. I ran these quickly without all the clean up of data I do in my weekly reports but order of magnitude is what is critical here. I could look at other or larger areas but the story would be largely the same. Closed sales in my 3 ZIPS for first 8 months

2015 – 951

2016 – 847

2017 – 899

2018 – 754

2019 – 764

2020 – 751

2021 – 878

2022 – 570

2023 – 493

Transaction volume has been steadily decreasing for a long time in an area with a growing population. In 2021 we had an outlier year, a boom with record low rates. But we pretty much should be selling between 750 and 800 single family homes in the first 8 months. Lets call that 100 homes.

Last year we had a very slow year and this year its much slower. We have about 60 homes selling per month.

That’s roughly 40% below what the industry built itself for. Now prices are high and when people get paid they get paid well but there’s a lot less paychecks being distributed among the real estate brokerages around here.

Whatever industry you are in, what would it look like if your employer lost 40% of its business? That’s what I think is coming to real estate.

And lending? That is far worse. The mortgages that are golden handcuffing people into their homes are not being refinanced and many if not most never will be! A couple months ago I had some mortgage volume stats and did some back of the envelope calculations. By my rudimentary calculation their business is down 75 to 80% from what it was. I could be off a bit but not off by an order of magnitude. Its bleak out there now in lending. Now some of that will come back eventually as transaction volumes eventually rise and those who bought with todays higher rates refinance but its gonna be a tough several years out there. Really tough!

Myself? I just look back and feel both lucky and fortunate to have lived the way I did. I spent the last 20 years preparing for something like this. Im fortunate it has no impact at all on me but I feel for my friends many of whom are unaware or unwilling to accept what is coming. I hope there are a lot of Plan B’s out there

Good stats and insights, thanks for sharing. Pretty incredible hollowing out of the business, especially the mortgage side of things.

Per your point about down years sometimes being good years: a recession could potentially help these industries in a couple ways. For one, rates would likely come down, leading to at least some refis and (if they went down enough) also people being released from their rate lock prison. Also, if people lost jobs or relocated that could force more sales and increase volume.

Whatever happens, my non-professional guess is that volume has to get back up there somehow. Like you suggested, these volumes are just too low for a city this size. SD as a whole doesn’t have much of a growing population, I think it was shrinking last I looked but it’s by like 1% or whatever so let’s call it basically flat vs. the massive decrease in volumes. Seems like something has to change… it could be a long process but I don’t think this is a stable equilibrium.

I would agree that it has to change but I think its gonna take 5 to 10 years to get back there. I’ve completed 60 laps around the sun now. I don’t have the inclination or need to wait for it to happen. I’ll keep doing my best for my past clients and those they refer to me. I’m sure I will continue getting my share and doing a great job at that. But the days of looking to aggressively build and expand this business are past for me.

I’ll take the under on that timeline…

I don’t think that’s a bad call. My time period is not based upon any strong feeling other than this is not going to completely resolve itself in 2 or 3 years. We may see some improvement but I do believe we are looking at a greatly diminished market size for more than a short while. Maybe I’m just a grumpy old man yelling at clouds

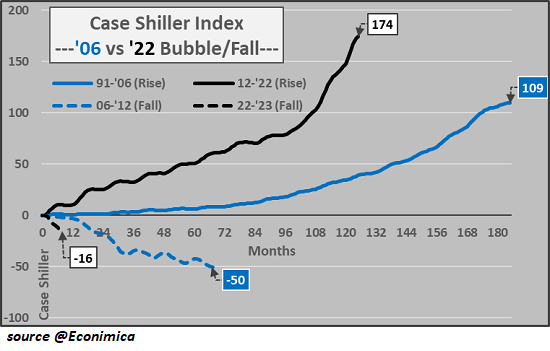

Maybe it WILL be different this time:

?itok=8b5yQQUW

?itok=8b5yQQUW

Source: https://www.zerohedge.com/personal-finance/housing-bubble-different-its-much-more-precarious

What a run up, this time.

And, believe it or not, overall, things are unwinding faster, this time.

Faster, deeper fall?

Should be ‘interesting.’

Uh oh:

https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed

https://imgflip.com/i/81c2cd

Even more reason to sit tight and not sell. Especially if you have a < 3.5% interest rate. It sucks to be a buyer right now. Not only is it much more costly, there not much to choose from.