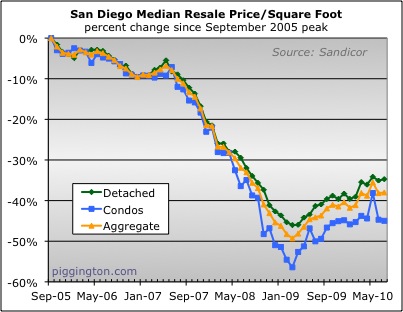

In the first month after the [insert preferred double homebuyer tax

credit catchphrase here], prices as measured by the median price per

square foot were pretty much flat:

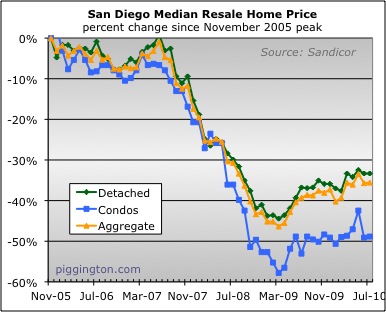

Same went for the vanilla median. Thrilling!

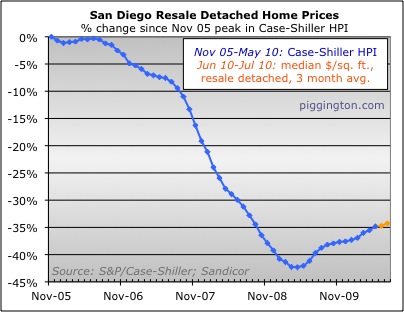

My Case-Shiller proxy, being a three-month average, crept up a bit

largely due to the big price jump in May, but this will roll out next

month and potentially lead to a decline:

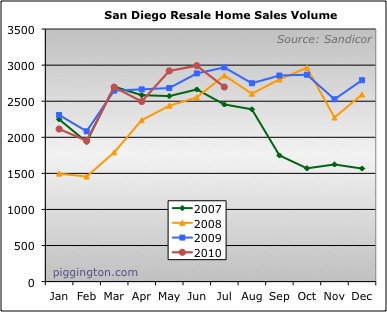

So prices were a bit of an analytical yawnfest. Much more

interesting was the action in sales and inventory.

As one would have expected post-double-tax-credit, sales

declined. This was during what has been a seasonally strong month

over the prior two years (sales were down in July 2007, but that

probably has more to do with subprime implosion than seasonality).

Schahrzad Berkland, former prolific Econo-Almanac poster, local

realtor, and proprietor of the San Diego Housing

Forecast website, was kind enough to share with me her historical

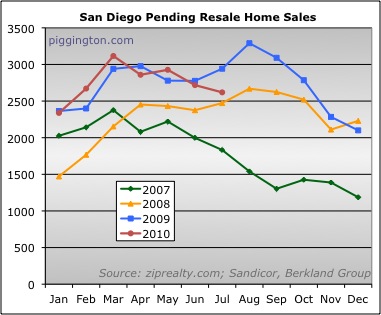

pending sales data so that I could do this next chart. Pending

sales are a more timely way to measure demand than closed sales,

because homes go pending when they go into escrow but don’t typically

become closed sales (and show up in a chart like the one above) until a

month or two later. Pending sales also dropped in July,

indicating declining closed sales ahead:

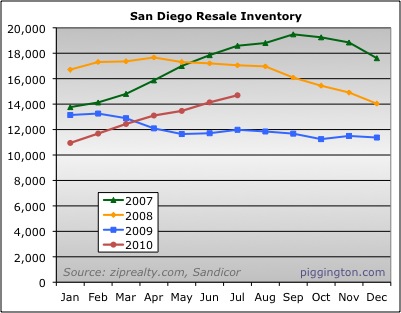

While demand was waning, supply continued to grow as it has all year:

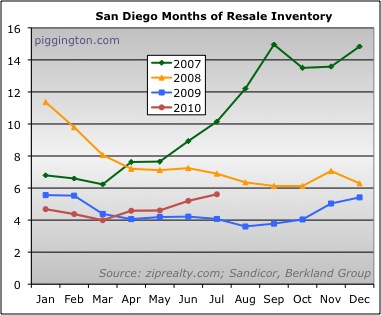

Month of inventory accordingly rose (the months of inventory chart is

updated to use pending sales instead of closings):

So here we are in the post-stimulus lull. The stimulus worked by

pulling forward future demand, but we’ve now arrived at the point in

time from which demand was poached. The concurrent rise in

inventory puts the months-of-inventory figure awfully close to the

6-month line that has often marked

the

difference between rising and falling prices. If current trends

continue, we will soon be at a level of inventory that has historically

been associated with price weakness.

Looks an awful lot like 2007.

Looks an awful lot like 2007. This should be getting interesting.

FWIW, I was surprised that the Fed didn’t apply the accelerator as much as they did in the past. Either they have run out of gas, or they are trying to save up what they can for something “unexpected” in the future.

Rich – pending sales don’t

Rich – pending sales don’t always close. I was pending for 6 months on a short sale that came back w/a lower appraisal, so I pulled out.

I’m not the only one. I see many that were contingent that I set an alert/favorite and come back active again many months later. Some of the ones that came back active also reduced their price. (of course, the one I wanted didn’t – drat!)

Nevertheless, if others see price declines and reduction in price, it’s possible future appraisals will come in lower, causing other pendings to go active and/or price reductions. Maybe some people who are in contingent status might see something they like better for a lower price.

To me, contingent/pending is starting to not mean much. I keep an eye on it if I like it, JIC it comes back. Sort of like, “It’s not over until the fat lady sings.” And frankly, I’m starting to see some that closed in 2008 come BOM for less. (crap – I’ve been looking that long) Of course, I’ve also seen some flips recently during the tax credit incentives. But at this rate, maybe we’ll see those back for less in a year or two.

The part that’s sad is all the money thrown at this and the best they can do is ultimately flatline.

I ask anyone: Wouldn’t it be better to have a quick bottom to achieve a quicker real recovery, or drag it out slowly?

As someone who owns and wants to buy, to me, life’s to short and I want to get this over with and see a real recovery, but I know to have a real recovery, we have to feel the pain first. I say rip the band aid off quick. Peeling it off slowly is just agonizing.

We are leaving “return to

[img_assist|nid=12219|title=We are leaving “return to normal”|desc=|link=node|align=left|width=540|height=350]

A couple quick points:

JP-you

A couple quick points:

JP-you were not in “pending” status for 6 months you were “contingent”. What you see with continegnts coming back at lower prices is likely this. Agents list short sales and take an offer to the bank for approval. According to Sandicor rules it must be marked pending during that phase. The offer can often be lower than asking price. When that offer gets approved the listing agent goes back to the buyer who more often than not has moved on. The property comes back on the market as “active” at a new “previously approved short sale price”. All this has aboslutely no bearing on what the market is doing and is simply related to the mechanics of going through a short sale. Thats all it is and nothing more.

CAR-2010 is looking nothing like 2007 and exactly like 2009. Lending has loosened up relative to where we were in 2007. I wonder why you post things like this because you know the inventory build up is more related to undesireable properties and/or overpriced properties piling up. These properties are generally overpriced for the current market and if they were priced for the current market most if not all would sell. Price reductions on these do not mean price levels are falling but rather sellers in denial are capitulating to the reality of the marketplace. There are plenty of qualified buyer in all but the highest price ranges for every home on the market as long as its pricing falls within the range of recent closed sales.

We are and have been in a very stable market for at least a year and I expect we will be in a very similar market for the next 2 to 5 years. There is no crash coming anytime soon. People appear to have finally given up on the notion of a foreclosure tsunami which I have been debunking as far fetched for years. We are in for a slow bleed and have been doing so for the last couple years. There will be no “real recovery” in the next decade but rather a slow return to normalcy as the valuations come back in line through modest declines and eventually wage inflation.

Now more than ever the challenge is to find a home you like enough to call home for the next decade that is reasonably priced for the current market rather than someone’s fantasy of where they think prices should or will go. It isnt going to happen. The cost of interest, insurance and taxes is not far off rental parity even in desireable NCC neighborhoods at interest rates hovering just above 4%. Throw in the tax benefits for someone with an income above $100K and its right there. Here are the numbers:

$750K home in NCC

Monthly rent easily $3000

Monthly interest on 80% of 750K at 4.125% is $2125 and it goes down over time as you make principal payments.

Insurance is about $100/month

Taxes are about $700/month

Total carrying costs excluding principal payments = $2925.

Throw in a tax benefit on the $2800 portion representing interest and taxes at a marginal tax rate of 28% federal and 9% state gets you down close to $2000 net per month.

We might as well make reservations at Donovan’s for tonite. Its over.

sdr – Rich’s graph was using

sdr – Rich’s graph was using historical “pending” sales data.

If you say that Sandicor rules it must be marked “pending” during that phase that I was “contingent,” would it not influence the graph, regardless of the term “pending” or “contingent”?

w/regard to your math accounting, those numbers do make sense when one puts 20% down. I don’t have stats at my fingertips. Are there a lot of people doing 20% down? Last time I talked to my loan guy, he said he had to brush up on FHA loans, b/c that’s pretty much all that people were doing.

jpinpb wrote:

If you say that

[quote=jpinpb]

If you say that Sandicor rules it must be marked “pending” during that phase that I was “contingent,” would it not influence the graph, regardless of the term “pending” or “contingent”?

[/quote]

I think he meant to say that it’s supposed to be marked “contingent” during that phase. This is my understanding, and in this case, it would not impact the graph.

jp

There is a “contingent”

jp

There is a “contingent” status on the mls and yours was likely in that category not pending. A short sale becomes pending when the lender accepts your offer and you open escrow. Did you ever deliver a check to an escrow office? If not, the property you referenced was never included in the pending.

As for the 20% down, I was specifically refering to NCC where 20% or more down is far more the rule than the exception. FHA loans on SFR’s are virtually non-existent around here. Your loan guy may not be working this area or may be working condo markets. In his world FHA may be all people are doing but his world is not THE world. This market is made up of many very different markets.

sdrealtor wrote:

We are and

[quote=sdrealtor]

We are and have been in a very stable market for at least a year and I expect we will be in a very similar market for the next 2 to 5 years. There is no crash coming anytime soon. People appear to have finally given up on the notion of a foreclosure tsunami which I have been debunking as far fetched for years. We are in for a slow bleed and have been doing so for the last couple years. There will be no “real recovery” in the next decade but rather a slow return to normalcy as the valuations come back in line through modest declines and eventually wage inflation.

.[/quote]

-SDR August 14, 2010

LOL – Maybe you should add

LOL – Maybe you should add this just for scaredy’s sake:

“Nothing to fear, but fear itself,”

FDR – March 4, 1933

or Oingo Boingo, 1988.

Arraya

The mechanisms for

Arraya

The mechanisms for watching, understanding and manipulating the markets today couldnt have been imagined in 1930. Your a screwball if you think the world of today is anything like the world back then. Things have changed.

Mark the date and etch it in concrete. I’m happy to put my money where my mouth is. I’ll be enjoying a very nice dinner at Donovan’s courtesy of CAR soon enough. I’d be happy to extend the same offer to you. Let’s put our money where our mouths are. Name your wager BearBoy?

sdr (NOT SDR)

lol… A realtor saying RE

lol… A realtor saying RE prices never go down, how cliché of you. This time with new and improved rationale. Is that what realtors are saying today – “Don’t worry, the government won’t let prices fall” – as a sell point. In place of, “They’re not making any more land”

Sorry, that’s inline with circa 2005 FB thinking. It’s different this time. Why did prices come down at all, they could have “manipulated” the market, right? Or are you saying they wanted prices to collapse in 2007? Or now, they just figured it out? Or they can only manipulate within a given range and you happen to know what that range is?

As for the bet, sorry, but, no thanks. Read into that, how you will…

Arraya it is embaressing

Arraya it is embaressing watching you hopelessly flail away. You lost and cant admit it. Nowhere did I say RE prices never go down in fact here is my quote from above.

“There will be no “real recovery” in the next decade but rather a slow return to normalcy as the valuations come back in line through modest declines and eventually wage inflation.”

Can you read? It says modest D-E-C-L-I-N-E-S! That means prices coming down. I was right in 2005, right in 2006, right in 2007, right in 2008, right in 2009 and right again in 2010 thus far. My track record over the last 4 years can easily be found in the archives of this site. Its been spot on. Meanwhile you whistle down the road calling for tsunamis, 50% declines and other nonsense. You’ve been right about very little that i can see.

As for the bet, I’d bet a bottle of water just to enjoy drinking it down at your expense. I dont have read anything into the no thanks on the bet it obvious for all to see . You are full of hot air.

sdrealtor wrote:

CAR-2010 is

[quote=sdrealtor]

CAR-2010 is looking nothing like 2007 and exactly like 2009. Lending has loosened up relative to where we were in 2007. I wonder why you post things like this because you know the inventory build up is more related to undesireable properties and/or overpriced properties piling up. These properties are generally overpriced for the current market and if they were priced for the current market most if not all would sell. Price reductions on these do not mean price levels are falling but rather sellers in denial are capitulating to the reality of the marketplace. There are plenty of qualified buyer in all but the highest price ranges for every home on the market as long as its pricing falls within the range of recent closed sales.

We are and have been in a very stable market for at least a year and I expect we will be in a very similar market for the next 2 to 5 years. There is no crash coming anytime soon. People appear to have finally given up on the notion of a foreclosure tsunami which I have been debunking as far fetched for years. We are in for a slow bleed and have been doing so for the last couple years. There will be no “real recovery” in the next decade but rather a slow return to normalcy as the valuations come back in line through modest declines and eventually wage inflation.

Now more than ever the challenge is to find a home you like enough to call home for the next decade that is reasonably priced for the current market rather than someone’s fantasy of where they think prices should or will go. It isnt going to happen. The cost of interest, insurance and taxes is not far off rental parity even in desireable NCC neighborhoods at interest rates hovering just above 4%. Throw in the tax benefits for someone with an income above $100K and its right there. Here are the numbers:

$750K home in NCC

Monthly rent easily $3000

Monthly interest on 80% of 750K at 4.125% is $2125 and it goes down over time as you make principal payments.

Insurance is about $100/month

Taxes are about $700/month

Total carrying costs excluding principal payments = $2925.

Throw in a tax benefit on the $2800 portion representing interest and taxes at a marginal tax rate of 28% federal and 9% state gets you down close to $2000 net per month.

We might as well make reservations at Donovan’s for tonite. Its over.[/quote]

When I said it looked like 2007, you have to compare the trends on Rich’s graphs. Sales and inventory growth trends are looking like the trajectory seen in 2007.

I think the rise in inventory is more due to the delusional sellers who think they’re entitled to 2005/2006 prices. Lots of people took their homes off the market in late 2007 through all of 2008. They thought they would “wait until things got better” in a year or two, so keep listing, delisting, relisting, delisting…you know the drill. They’ve seen the market strengthen due to the govt/Fed intervention, and decided to make their way to the exit. Too bad they’re either a few months too late, and/or they overpriced their listings and will now likely be stuck for many more years, IMHO.

I know a lot of people who did a final draw-down on their HELOCs and/or did a cash-out refi in 2007/2008. They were doing this to capture their “equity” before it went away — there were quite a few folks who saw the writing on the wall and tried to hunker down. Problem is, they thought (and still think) that 2006 prices are “normal” and that the deflation was some sort of anomaly that came out of the blue. Too many people can’t seem to tie together the existence of rising prices and the subsequent falling prices.

Anyway, I think a lot of budgets are getting thin, and people are starting to understand that wages and prices don’t “always go up,” even in the mid-long run. Many of the listings today are actually better than what we saw a year ago, and are better priced, relatively speaking.

You can’t ignore all those high-end places that are clogging up the MLS. Some of those people actually want to sell, and when that top-heavy inventory starts crumbling, look out below.

There is no doubt in my mind that we’ll see lower prices from here on out. There are valid arguments to be made by the inflationistas, but I’m still leaning toward deflation — which seems to be the most powerful force out there, at least for now. I’ll change my mind just as soon as we hear about sigificant and sustainable wage increases.

Sorry CAR but I dont buy it.

Sorry CAR but I dont buy it. 2010 looks like 2009 not 2007. Compare the months inventory numbers which combine sales and inventory and tell me 2010 looks like 2007. It is not even close. In 2007 inventory built up because sales volume fell off the map when financing shut down. Do you beleive we will see financing shut down in the next 30 to 90 days like it did in 2007? Of course not.

We are heading into our typical seasonal duldrums and we should get some declines over the next couple months in some places. Nothing major but defintely some small declines to be found by opportunistic buyers.

I watch the market around here like a hawk and there is no credence to the list, de-list, relist, de-list drill. I dont see it happening to any degree. Find me 10 houses that have come on and off the market around here over the last 5 years. Find me 5 or even 3.

I do agree delusional sellers exist and sit overpriced. Yes some people drew down HELOCs but other people are coming in to this market and others are suceeding. The world is not ending. People are suceeding all around you.

As for the high end markets struggling – that market is not large enough to take down the much larger entry level and mid priced tiers. I just saw an REO today that was formally worth about $1.5 to $1.7M on the market for $1M. You had to take a ticket to get in the house. Traffic was more backed up then the deli counter at Stater Brothers.

Yes we will see some lower prices but we will also see some higher prices. That is the nature of the RE markets. Have you considered that we could see neither inflation or deflation? Thats what I see, relatively stable prices for the next 2 to 5 years. Eventually all the stimulus and money that has been put into circulation will make its way into paychecks a little at a time. May not in the already bloated public sector but defintely in the private sector.

sdrealtor wrote:Sorry CAR but

[quote=sdrealtor]Sorry CAR but I dont buy it. 2010 looks like 2009 not 2007. Compare the months inventory numbers which combine sales and inventory and tell me 2010 looks like 2007. It is not even close. In 2007 inventory built up because sales volume fell off the map when financing shut down. Do you beleive we will see financing shut down in the next 30 to 90 days like it did in 2007? Of course not.

We are heading into our typical seasonal duldrums and we should get some declines over the next couple months in some places. Nothing major but defintely some small declines to be found by opportunistic buyers.

I watch the market around here like a hawk and there is no credence to the list, de-list, relist, de-list drill. I dont see it happening to any degree. Find me 10 houses that have come on and off the market around here over the last 5 years. Find me 5 or even 3.

I do agree delusional sellers exist and sit overpriced. Yes some people drew down HELOCs but other people are coming in to this market and others are suceeding. The world is not ending. People are suceeding all around you.

As for the high end markets struggling – that market is not large enough to take down the much larger entry level and mid priced tiers. I just saw an REO today that was formally worth about $1.5 to $1.7M on the market for $1M. You had to take a ticket to get in the house. Traffic was more backed up then the deli counter at Stater Brothers.

Yes we will see some lower prices but we will also see some higher prices. That is the nature of the RE markets. Have you considered that we could see neither inflation or deflation? Thats what I see, relatively stable prices for the next 2 to 5 years. Eventually all the stimulus and money that has been put into circulation will make its way into paychecks a little at a time. May not in the already bloated public sector but defintely in the private sector.[/quote]

The only place I see that money going into is the horrifically bloated FIRE sector. We’ll see if it ever makes its way into either the public or *productive* private sector (as opposed to the parasitic financial sector).

Back in 2007, it was the credit market seizing up that caused the big chunk down. This year, I believe it will be the end of many stimulative programs that will lead the next chunk down (so far — we’ll see what else they pull out of their hats). I really think they’re pushing on a string, and it’s getting worse with every new program they announce. It has to be progressively bigger and badder than the last program just to keep things level, and I don’t see that as sustainable.

I’ll get you your ten houses next. Will have to do some legwork.

As a frustrated buyer, part

As a frustrated buyer, part of me hopes this is true and that you can tell me what month “fear” will hit so I can plan accordingly. 🙂

If not obvious, I am really making fun of myself as the long term frustrated buyer.

I get a kick out of those

I get a kick out of those trying to say it is time to buy because the payment is equal to rent, then they do their best to show the numbers.

They say, “all you need to do is put 20%” down and your payment will be this or that.

That 20% has value and should be considered . It is much like saying, “if you put down 90%” your payment will be ……..” It doesn’t make sense!

When coming up with the calculation you must calculate as if 100% is financed.

In addition, in the last 12 months my landlord has had a termite treatment (about 1k), replaced the heating/cooling system (3to 5K) and replaced the fridge (400.00). Not to mention the long term things like paint jobs and re roofing.

Where are these numbers in your examples of rent versus buying?

And, I don’t know how old you are but up til 1990 buying was ALWAYS cheaper than renting, even when considering the above.

sobmaz, would it be a time to

sobmaz, would it be a time to buy if the interest + tax + insurance – tax deduction on 100% financing is $600/month cheaper than comparable rent?

AN wrote:sobmaz, would it be

[quote=AN]sobmaz, would it be a time to buy if the interest + tax + insurance – tax deduction on 100% financing is $600/month cheaper than comparable rent?[/quote]

I dont know, but three questions:

1) Why no principal payment? Sure, you are able to say that is savings, but paying off debt on an underwater house isnt going to return dollar for dollar. Just curious to your train of thought.

2) What is the rent? $600 off $1200/m is alot differnet than $600 off $5000/m.

3) Whos income? Cause child tax credits, interest deductions, standard deductions, home buiz writeoffs; no two income are the same. How do you handle a tax return where the interest deduction doesnt pay off due to AMT? again, just curious.

Also, if your gonna do the math the way I think you are, you really need to add in a 1month per 2 year vacancy period. And some repair/maintaince costs.

DWCAP wrote:AN wrote:sobmaz,

[quote=DWCAP][quote=AN]sobmaz, would it be a time to buy if the interest + tax + insurance – tax deduction on 100% financing is $600/month cheaper than comparable rent?[/quote]

I dont know, but three questions:

1) Why no principal payment? Sure, you are able to say that is savings, but paying off debt on an underwater house isnt going to return dollar for dollar. Just curious to your train of thought.

2) What is the rent? $600 off $1200/m is alot differnet than $600 off $5000/m.

3) Whos income? Cause child tax credits, interest deductions, standard deductions, home buiz writeoffs; no two income are the same. How do you handle a tax return where the interest deduction doesnt pay off due to AMT? again, just curious.

Also, if your gonna do the math the way I think you are, you really need to add in a 1month per 2 year vacancy period. And some repair/maintaince costs.[/quote]

1) Assuming you bought a house you can afford, your mortgage is less than comparable rent, and it’s your primary resident and not an investment property, why would you want to sell at a loss? That’s why I don’t count principal. At some point in the future, you’ll break even. Why wouldn’t it return dollar for dollar? Just curious to your train of thought?

2) Does rent matter? Is $600 discount somehow not $600 discount when it’s 10% off vs 50% off?

3) Does income really matter? Same questions as #2.

4) Why would you count in vacancy? Are you not going to need a roof over your head 24/7/365? Is $600/month saving not enough to at least cover repair and maintenance?

Cmon AN the vacancy factor is

Cmon AN the vacancy factor is important to count for the time you live in your parents basement when you get laid off your job at Hollywood Video.

AN wrote:DWCAP wrote:AN

[quote=AN][quote=DWCAP][quote=AN]sobmaz, would it be a time to buy if the interest + tax + insurance – tax deduction on 100% financing is $600/month cheaper than comparable rent?[/quote]

I dont know, but three questions:

1) Why no principal payment? Sure, you are able to say that is savings, but paying off debt on an underwater house isnt going to return dollar for dollar. Just curious to your train of thought.

2) What is the rent? $600 off $1200/m is alot differnet than $600 off $5000/m.

3) Whos income? Cause child tax credits, interest deductions, standard deductions, home buiz writeoffs; no two income are the same. How do you handle a tax return where the interest deduction doesnt pay off due to AMT? again, just curious.

Also, if your gonna do the math the way I think you are, you really need to add in a 1month per 2 year vacancy period. And some repair/maintaince costs.[/quote]

1) Assuming you bought a house you can afford, your mortgage is less than comparable rent, and it’s your primary resident and not an investment property, why would you want to sell at a loss? That’s why I don’t count principal. At some point in the future, you’ll break even. Why wouldn’t it return dollar for dollar? Just curious to your train of thought?

2) Does rent matter? Is $600 discount somehow not $600 discount when it’s 10% off vs 50% off?

3) Does income really matter? Same questions as #2.

4) Why would you count in vacancy? Are you not going to need a roof over your head 24/7/365? Is $600/month saving not enough to at least cover repair and maintenance?[/quote]

It’s not a matter of *wanting* to sell or not, it’s a matter of *having* to. This can be for financial reasons, health reasons, family dynamics, or just wanting to move!

The vast majority of people don’t sell their houses because they increased in value. They sell because they want to (or have to) move for a variety of reasons, and they can’t — or don’t want — to become landlords. It’s that simple.

I would ALWAYS calculate principal payments in my rent/own calculations. After all, it is borrowed money that has to be paid back. You might get that back “in the long run,” but you might not. I think too many people are counting on inflation to bail them out of their bad decisions. That’s not necessarily how things are going to play out from here on out. There are many economic and demographic changes which point to housing deflation for a long, long time to come.

CA renter wrote:

It’s not a

[quote=CA renter]

It’s not a matter of *wanting* to sell or not, it’s a matter of *having* to. This can be for financial reasons, health reasons, family dynamics, or just wanting to move![/quote]

Understandable. Those are the cases you can’t plan for.

[quote=CA renter]The vast majority of people don’t sell their houses because they increased in value. They sell because they want to (or have to) move for a variety of reasons, and they can’t — or don’t want — to become landlords. It’s that simple.[/quote]

Again, why would you want to if the current value is below what you bought it for and selling it and renting a similar place would mean you have to pay more every month?

[quote=CA renter]I would ALWAYS calculate principal payments in my rent/own calculations. After all, it is borrowed money that has to be paid back. You might get that back “in the long run,” but you might not. I think too many people are counting on inflation to bail them out of their bad decisions. That’s not necessarily how things are going to play out from here on out. .[/quote]

What do you mean you might not? After 30 years, you’re done. You have no more mortgage payment and the house is yours.

[quote=CA renter]There are many economic and demographic changes which point to housing deflation for a long, long time to come.[/quote]

Oh really? So you think 10-20 years from now, people will be able to buy a house for less than what you can today?

Not counting principal

Not counting principal payments assumes neither inflation nor deflation. Either could happen but we dont know which and when. In the LONG run inflation is most more likely.

Interest costs go down as principal is reduced and rent goes up over time. There are also moving costs. I would estimate that each time you move it costs about 1 months rent. None of these costs were factored in which all benefit buying over renting.

Quibling over this is not the point though because the current carrying costs for a typical home in NCC are pretty darn close if not neutral on rent vs buy right now as the numbers above show. Whether the numbers I used are a couple hundred too low or too high doesnt much matter. A significant change in prices (i.e. 20% or more) is very unlikely to occur anytime soon from current levels. I dont know where or when a bottom will occur but all signs tell me we are close enough that buying makes sense for alot of people if they are fortunate to find a home they love and could live in long term around here.

AN wrote:

1) Assuming you

[quote=AN]

1) Assuming you bought a house you can afford, your mortgage is less than comparable rent, and it’s your primary resident and not an investment property, why would you want to sell at a loss? That’s why I don’t count principal. At some point in the future, you’ll break even. Why wouldn’t it return dollar for dollar? Just curious to your train of thought?

2) Does rent matter? Is $600 discount somehow not $600 discount when it’s 10% off vs 50% off?

3) Does income really matter? Same questions as #2.

4) Why would you count in vacancy? Are you not going to need a roof over your head 24/7/365? Is $600/month saving not enough to at least cover repair and maintenance?[/quote]

1) There is no way to count what will happen in the future. But very few people hold onto their houses for 30,40+ years. What was it, 5 years or something is the avearage time americans spend in their homes? It isnt a huge strech to imagine that in 5 years time housing prices are 5-10% below where they are now, with the exception of some current REO property. (just imagine interest rates at 7+%) If that was the case, then all your prinicpal payments are kaput and it isnt dollar for dollar.

I am not saying people cant do this in their calculations, but that they need to explain WHY they are doing it. You are using a long term buy and hold startagy for ‘average’ americans who dont do that. One of the biggest problems I have with alot of these types of calculations is that people pick and choose what timelines they are using, to better build their case. As and example, if you are using long term, you need to account for the fact that your tax deducation will fall over time.

2) Rents most certainly matter, because your whole argument is return on investment. If I have to borrow 100k to make 600 savings, or if I have to borrow 1million to do it, the risk/return is very very different. Buying a house is risky, what happens if I have to move? or get sick? or get laid off?

3) Income matters because you deduct tax benifits from your equation. That is assuming you get those tax benifits, or that they are not just replacing others. AMT nails alot of people, making their tax benifits moot. People get standard deductions, child deductions, buiz deductions etc etc etc. If you are just substituting one for another, then the savings is moot becuase both the renter and the home owner never pay the taxes anyways.

4) Vacancy matters in how you are calculating the costs. I thought you were calculating as a LL, but rereading, you are doing it as a buy/not buy. My bad. In this, it doesnt matter.

But the costs equation is still valid. A homeowner is responsible for costs a renter isnt. New water heater, new paint, new flooring/carpet, new roof. All on the owner, not the renter. You need to account for that in your $600/month savings.

I personally think the formula should be very simple. When you get fancy things blow up in peoples faces. My brother had a very complex excel document showing that with tax breaks he couldnt loose money on his 2005 condo (to be a rental) purchase. He is a very smart fellow, but still out manuvered himself and is very likley to loose money unless he holds until death, and maybe not even then.

PITI= Rent+5% (10% for the more agressive buyer if you want).

If your PITI payment is within 5% of average rent (for that type of house), then your buy option is a good one. Call the tax deduction a wash for your extra costs, and the P your compensation for extra risk.

I agree there is no way to

I agree there is no way to know what will happen in the future which is exactly the case for assuming stable values.

Not that you would remember but I went through this about 3 years ago with AN. The average occupancy for a SFR around here is much longer than 5 years. Pick a street any street in SD where the homes are at least 10 years and I will calculate it for you. The street has to be old enough to produce an accurate result because people cant live for 10 years in 5 year old houses.

My calculation is not a return on investment but rather a break even analysis looking at owning vs. renting. My point is that it was close enough that the notion of steep declines are not supported by the current situation. I am not saying no declines nor am I saying appreciation. Just showing why the permabear case that the market has to go down hard from here has no basis with current market realities.

I’m not claiming a $600/month savings nor is it part of my case. My point is that things are close enough to equality on the rent vs buy that a crash (i.e. 20% decline or more) seems highly unlikely). Yes there is ongoing repairs and maintenance but there are also moving costs, increasing rent and often subpar living conditions associated with renting (i.e. my LL wont fix the fence, the heater, the roof etc.).

Lastly if you are going to make the tax deduction a wash for extra costs and the P compensation for extra risk it is only fair to include some kind of premium for ownership. If people didnt place some sort of premium on owning vs. renting we wouldnt be here talking about buying RE to begin with.

sdrealtor wrote:I agree there

[quote=sdrealtor]I agree there is no way to know what will happen in the future which is exactly the case for assuming stable values.

Not that you would remember but I went through this about 3 years ago with AN. The average occupancy for a SFR around here is much longer than 5 years. Pick a street any street in SD where the homes are at least 10 years and I will calculate it for you. The street has to be old enough to produce an accurate result because people cant live for 10 years in 5 year old houses.

My calculation is not a return on investment but rather a break even analysis looking at owning vs. renting. My point is that it was close enough that the notion of steep declines are not supported by the current situation. I am not saying no declines nor am I saying appreciation. Just showing why the permabear case that the market has to go down hard from here has no basis with current market realities.

I’m not claiming a $600/month savings nor is it part of my case. My point is that things are close enough to equality on the rent vs buy that a crash (i.e. 20% decline or more) seems highly unlikely). Yes there is ongoing repairs and maintenance but there are also moving costs, increasing rent and often subpar living conditions associated with renting (i.e. my LL wont fix the fence, the heater, the roof etc.).

Lastly if you are going to make the tax deduction a wash for extra costs and the P compensation for extra risk it is only fair to include some kind of premium for ownership. If people didnt place some sort of premium on owning vs. renting we wouldnt be here talking about buying RE to begin with.[/quote]

And I agree with you. Without some serious problems in the economy, 20%+ isnt gonna happen. But my point is that all the variation being used is just adding uncertainty and can only be used for individual situtations. If we are looking for a way to see if real estate is fairly valued, then IMO it should be simple and basic.

If PITI = RENT plus some small premium (I would argue that the premuim is higher in NCC than El Cajon, hence the range, do you disagree?) than it isnt a bad idea to be in the market.

DWCAP wrote:

And I agree with

[quote=DWCAP]

And I agree with you. Without some serious problems in the economy, 20%+ isnt gonna happen. But my point is that all the variation being used is just adding uncertainty and can only be used for individual situtations. If we are looking for a way to see if real estate is fairly valued, then IMO it should be simple and basic.

If PITI = RENT plus some small premium (I would argue that the premuim is higher in NCC than El Cajon, hence the range, do you disagree?) than it isnt a bad idea to be in the market.[/quote]

Why complicate things w/ the TI part? Why not just compare PI with rent? My experience, TI is equivalent to the tax deduction. Also, depend on how skillful you are at shopping around, the I part can vary a lot.

DWCAP, if your time frame is

DWCAP, if your time frame is <5 years and you would sell regardless of whether you up or down, then yeah, you shouldn't buy. BTW, you should reread my original post. Here it is:

[quote=AN]sobmaz, would it be a time to buy if the interest + tax + insurance - tax deduction on 100% financing is $600/month cheaper than comparable rent?[/quote]

I didn't pick any time frame, I was plainly asking, would it be a good time to buy if you're saving $600/month compare to rent (excluding principal).

If you consider tax deduction fall over time, you should also consider the interest you're paying fall over time and rent rise over time. There a many variables that I didn't count for.

Where did you see my whole argument is return on investment?

I guess I should put in, YMMV with regards to tax deduction. But please reread my original post.

BTW, I'm trying to keep it simple, you're the one who's trying to make it complicated.

When you say PITI = Rent + 5%, are you talking about PITI of 100% financing or w/ 20% down? Why not count in tax deduction?

AN wrote:DWCAP, if your time

[quote=AN]DWCAP, if your time frame is <5 years and you would sell regardless of whether you up or down, then yeah, you shouldn't buy. BTW, you should reread my original post. Here it is:

[quote=AN]sobmaz, would it be a time to buy if the interest + tax + insurance - tax deduction on 100% financing is $600/month cheaper than comparable rent?[/quote]

I didn't pick any time frame, I was plainly asking, would it be a good time to buy if you're saving $600/month compare to rent (excluding principal).

If you consider tax deduction fall over time, you should also consider the interest you're paying fall over time and rent rise over time. There a many variables that I didn't count for.

Where did you see my whole argument is return on investment?

I guess I should put in, YMMV with regards to tax deduction. But please reread my original post.

BTW, I'm trying to keep it simple, you're the one who's trying to make it complicated.

When you say PITI = Rent + 5%, are you talking about PITI of 100% financing or w/ 20% down? Why not count in tax deduction?[/quote]

Different strokes for different folks. I found your formula of changing tax breaks and excluded portions of payment complicated.

As for the 'return on investment' portion, you are correct, you never used those words. I am not going to say you did. But your original post was read to coded, with few details, and some big numbers in no context. I asked for context, and then gave what I found to be a simplier formula to use. If you dont find it easier, then please do not listen to me.

DWCAP wrote:

Different

[quote=DWCAP]

Different strokes for different folks. I found your formula of changing tax breaks and excluded portions of payment complicated.

As for the ‘return on investment’ portion, you are correct, you never used those words. I am not going to say you did. But your original post was read to coded, with few details, and some big numbers in no context. I asked for context, and then gave what I found to be a simplier formula to use. If you dont find it easier, then please do not listen to me.[/quote]

I have a whole excel set up for this, so I can run any number quickly. Be it, PITI vs rent, PI vs rent, PITI – tax deduction vs rent, PI – tax deduction, ITI – tax deduction, etc. So, they all are the same to me, one is not simpler than another. I just need to plug in the paid price, % down, interest rate, and Insurance rate and excel does the rest.

DWCAP wrote:

PITI= Rent+5%

[quote=DWCAP]

PITI= Rent+5% (10% for the more agressive buyer if you want).

If your PITI payment is within 5% of average rent (for that type of house), then your buy option is a good one. Call the tax deduction a wash for your extra costs, and the P your compensation for extra risk.[/quote]

This is one of the more logical things I’ve read today. I have to agree. I used the “car payment” rule of thumb when bying our first house. Our entire house payment (PITI + PMI) was equal to our previous rent + car payment.

DWCAP wrote:

1) There is no

[quote=DWCAP]

1) There is no way to count what will happen in the future. But very few people hold onto their houses for 30,40+ years. What was it, 5 years or something is the avearage time americans spend in their homes? [/quote]

Not to nitpick too much – but my gut called bs on the 5 years in a home thing… so I googled and I looked at my microcosm – my block.

The google turned up the figure of 11.9 years average time of home ownership. I would imagine younger people change homes more frequently as they get ‘starter’ homes then either relocate for a job, or move up to the ‘forever’ homes. But look at the 40+ crowd – most have been in their home a while and have no plans to move. And that percent of long-termers gets greater as you go up in age. Factor in the fact that the older you are, the more likely you are to be a home owner, vs renter… and the 5 year figure gets destroyed.

Now for the anectdotal evidence. I live on a block that was developed in 1964. There are 47 houses on the street. There are 4 houses that are owned by the children of the previous (original or close to original) owners (including mine.) We purchased over 7 years ago and are relatively new on the block. Only 6 houses have changed hands since we purchased. 2 of those were more than 5 years ago. A quick scan of the prop tax records for the street (combined with my childhood memory of who lived there then) turns up 13 houses that are owned by the original owners who bought new in 1964. That’s a quarter of the houses that have people in their homes more than 45 years. Add in the 2nd generation folks (kids who grew up in the house, and bought from their parents) and you’ve got 36%.

But… to support your argument… I only owned my first house 3 years – sold when I moved to another state. I owned my 2nd home 8 years – sold when I moved out of state. And I’m in my current home 7 years… so on average I only own homes for 6 years.

Exactly UCG and those shorter

Exactly UCG and those shorter stay are the reason the average gets pulled down. I’m in my house 11 years already and it will be at least another 10 before I would consider moving. Even then I have plans on selling it.

NO prinicpal payment because

NO prinicpal payment because it is paying down the debt and over the long run it comes back to you in most cases-impoprtant I said LONG run.

Over time rent increases with inflation but mortgage payments stay the same. Also interest actually goes down as you pay down the principal.

NO vacancy because it is for your shelter not for an investment property. You do need a roof over your head.

DWCAP wrote:

3) Whos income?

[quote=DWCAP]

3) Whos income? Cause child tax credits, interest deductions, standard deductions, home buiz writeoffs; no two income are the same. How do you handle a tax return where the interest deduction doesnt pay off due to AMT? again, just curious.

[/quote]

Fact check: Mortgage interest IS deductible under AMT.

FormerSanDiegan wrote:DWCAP

[quote=FormerSanDiegan][quote=DWCAP]

3) Whos income? Cause child tax credits, interest deductions, standard deductions, home buiz writeoffs; no two income are the same. How do you handle a tax return where the interest deduction doesnt pay off due to AMT? again, just curious.

[/quote]

Fact check: Mortgage interest IS deductible under AMT.[/quote]

Thank you for the nit pick fact check. The point was no two tax returns are the same, and using it as a write off is gonna bring variation.

sobmaz wrote:I get a kick out

[quote=sobmaz]I get a kick out of those trying to say it is time to buy because the payment is equal to rent, then they do their best to show the numbers.

They say, “all you need to do is put 20%” down and your payment will be this or that.

That 20% has value and should be considered . It is much like saying, “if you put down 90%” your payment will be ……..” It doesn’t make sense!

When coming up with the calculation you must calculate as if 100% is financed.

In addition, in the last 12 months my landlord has had a termite treatment (about 1k), replaced the heating/cooling system (3to 5K) and replaced the fridge (400.00). Not to mention the long term things like paint jobs and re roofing.

Where are these numbers in your examples of rent versus buying?

And, I don’t know how old you are but up til 1990 buying was ALWAYS cheaper than renting, even when considering the above.[/quote]

Speaking of 1990, how much was it to rent a 3/2 1500 sq foot home vs now? Anyone here own a home bot in the 1990 that can tell us whether they regret owning that home and would rather rent it from a landlord? You know, just as all ownership experirces are not smooth, not all rental experiences are pleasant either, especially if you happen to rent from someone here whose name I won’t mention : )

outtamojo wrote:sobmaz

[quote=outtamojo][quote=sobmaz]I get a kick out of those trying to say it is time to buy because the payment is equal to rent, then they do their best to show the numbers.

They say, “all you need to do is put 20%” down and your payment will be this or that.

That 20% has value and should be considered . It is much like saying, “if you put down 90%” your payment will be ……..” It doesn’t make sense!

When coming up with the calculation you must calculate as if 100% is financed.

In addition, in the last 12 months my landlord has had a termite treatment (about 1k), replaced the heating/cooling system (3to 5K) and replaced the fridge (400.00). Not to mention the long term things like paint jobs and re roofing.

Where are these numbers in your examples of rent versus buying?

And, I don’t know how old you are but up til 1990 buying was ALWAYS cheaper than renting, even when considering the above.[/quote]

Speaking of 1990, how much was it to rent a 3/2 1500 sq foot home vs now? Anyone here own a home bot in the 1990 that can tell us whether they regret owning that home and would rather rent it from a landlord? You know, just as all ownership experiences are not smooth, not all rental experiences are pleasant either, especially if you happen to rent from someone here whose name I won’t mention : )[/quote]

That is a no brainer.

If you recall we had the largest housing bubble in history from 1999 to 2007. You would have to be out of touch with reality to not want to have owned for the last 20 years.

That said, unless the FED continues to socialize the mortgage market, continues to control the long term yield curb and thereby getting 30 year rates down to the 2 to 3% range, there is unlikely to be a repeat of the latest bubble.

Therefor it would be prudent to believe that om the immediate future, housing is apt to be more like it was from 1800 to 1980 than from 1999 to 2007.

Just my opinion.

sobmaz wrote:

That is a no

[quote=sobmaz]

That is a no brainer.

If you recall we had the largest housing bubble in history from 1999 to 2007. You would have to be out of touch with reality to not want to have owned for the last 20 years.

That said, unless the FED continues to socialize the mortgage market, continues to control the long term yield curb and thereby getting 30 year rates down to the 2 to 3% range, there is unlikely to be a repeat of the latest bubble.

Therefor it would be prudent to believe that om the immediate future, housing is apt to be more like it was from 1800 to 1980 than from 1999 to 2007.

Just my opinion.[/quote]

Here’s the historical average home price according to the Census: http://www.census.gov/hhes/www/housing/census/historic/values.html

If it’s going to be more like 1940-1980, I’m cool with that.

Rich- If you’re still in

Rich- If you’re still in touch with Ramsey Su, it would be very interesting to hear his take on the RE market at this time.

His analytical work has been very impressive.

Thanks

peterb wrote:Rich- If you’re

[quote=peterb]Rich- If you’re still in touch with Ramsey Su, it would be very interesting to hear his take on the RE market at this time.

His analytical work has been very impressive.

Thanks[/quote]

He’s very bearish based on all the delinquencies and the fact that there is no private mortgage market.

Guess he didnt see my

Guess he didnt see my observation today on a $1M REO that attracted 16 offers and counting. Plenty of demand when they are priced right or slightly below market as that one is.

sdrealtor wrote:Guess he

[quote=sdrealtor]Guess he didnt see my observation today on a $1M REO that attracted 16 offers and counting. Plenty of demand when they are priced right or slightly below market as that one is.[/quote]

If it’s the one I’m thinking of, that house was priced at around 2000/2001 levels, no? Price any house around here at 2000/2001 levels, and you’ll get it sold, no problem. This is the price level that we’re waiting for. 🙂

House was low 800’s when new

House was low 800’s when new in 2001. Add pool and landscaping and it might have gotten up to $1M in 2001/2002. This house sold for $1.4M in 2005 and then got a nice remodel inside so I’d put its peak value around $1.5M. It looks like it will take about 50K to put it back in order now as appliances, door knobs, lights and many plumbing fixtures are gone. In 2004 a bigger one in a much nicer location went for $1.25M.

I figure this one closes around $1.1M which would be a 2003 price.

‘San Diego Housing Bubble

‘San Diego Housing Bubble News and Analysis’.

Hi Rich,

Looking at all these interesting comments ( returning after many months away) it occurs to me that maybe it is time to re-name this 2004 established blog to remove the name ‘Bubble’ if selling at 2002/3 prices is pre-dominant ( but keep the old name for the archive).

If you are reluctant to do so, might you then still think we are in bubble territory; as some think.

Perhaps it boils down to whether it was a mid to late 200s bubble or

we are still in a much longer , decades long phenomenon based on the mechanism of easy government backed credit that the nation will be weaned off over time (made worse by the ‘underwater’ iceberg if debt forgiveness does not become complete).

Graham

Graham — Welcome back and

Graham — Welcome back and good point… that’s a throwback from the olden days. Housing certainly has its problems but it really couldn’t accurately be called a “bubble” at this point. I changed the description to read “market” instead of “bubble.”