As discussed previously, prices on the whole rallied again last month:

I’m chalking the whackage in the condo size-adjusted median up to volatility (of which there is a lot, as the chart shows) rather than a trend change. This logic was also described in the last article on prices. All in all it seems that the rally endured for another month.

The plain vanilla median was directionally quite similar: detached homes up, condos down, but the volume-weighted aggregate up a hair.

My model of what the Case-Shiller HPI might look like when the July version finally comes out is below:

What’s interesting here is that even considering the spring rally effect, this price increase is fairly dramatic. As of July, the HPI model was up 4.9% from the April low in the HPI. This is significantly larger than the biggest spring rallies of the 1990s bust (2.3% each in 1991 and 1994). Of course, this assumes that my proxy will be an accurate representation of the actual Case-Shiller HPI when it comes out… that remains to be seen.

An unusually large bounce isn’t out of the realm of possibility considering how much demand there is in comparison to supply. Sales volume was once again healthy:

…and inventory, while up slightly from the prior month, was pretty tight:

…leading to a very low 4 months of inventory:

Contingent inventory amounted to about 29% of total inventory, so if we back out contingent homes there were fewer than 3 months of inventory for sale:

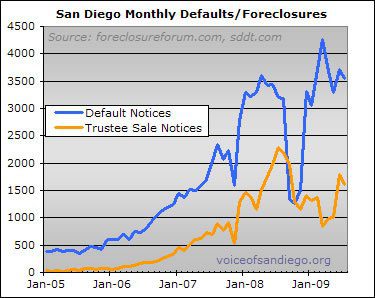

Yet as usual, against this scarce current inventory backdrop we have yet more homes piling atop the mountain of foreclosures each month:

The shadow inventory issue (most recently discussed here) looms large, its significance to be decided at a later date. In the meantime, there is little doubt that we are experiencing a significant rally in the San Diego housing market.

Stop it Rich… you are just

Stop it Rich… you are just talking nonsense.

No way would I buy now. Even

No way would I buy now. Even if this really was the bottom of the market (which I really doubt) there’s no way that I’m going to fight with ten other buyers over some crummy over-priced shack.

Instead of buying something now, we’ve decided to move into another rental house that we like better.

This feeding frenzy of buyers is just too weird.

fredo4 wrote:

This feeding

[quote=fredo4]

This feeding frenzy of buyers is just too weird.[/quote]

I have to agree with this. It doesn’t seem rational at all.

There is no shortage of

There is no shortage of irrationality in the world. We’re stocked up in that regard. However, we will soon have a shortage of willing and able buyers in the RE market.

Irrationality in markets manifests in euphoria or panic. We are in the euphoric state now getting ready to shift to panic.

The economy has been contracting for 2 years and incomes have been dropping for 1 year. This trend is not stopping tommorow.

UCGal wrote:fredo4

[quote=UCGal][quote=fredo4]

This feeding frenzy of buyers is just too weird.[/quote]

I have to agree with this. It doesn’t seem rational at all.[/quote]

Yeah, fredo – that’s a good way of putting it. Sometimes it’s the non-analyitical analysis that makes the most sense. I’m thrilled I’m not in need of a house right now. It is just too wierd.

I’m starting to think it will remain wierd for a while, too.

Ummm. OK.

Who cares if it

Ummm. OK.

Who cares if it really is the bottom. Its attractive. Very attractive in some cases. These comments were the same comments I heard about equities back in March.

As far as my house I’m getting my tax advantage and building equity. I wish I was a buyer for another property.

As long as equity-building

As long as equity-building outpaces depreciation (if any).

So do people who take advantage of the 8K tax credit forfeit any right to bitch about bailouts? I cease being a net taxpayer by several thousand dollars* for 2009 if I buy a house in next few months.

Edit: *well, at least as far as fed/state taxes are concerned.

Really, this stuff is not

Really, this stuff is not magic.

Since wages AND employment are trending down there is NO ‘mean’ to revert to. San Diego is not exempt from this trend.

Read the above 10x if you have to.

Coupled with the fact that the USG is suppling 80% of the financing AND banks are playing games with inventory, means that you have nothing to gage where a bottom would be. Nothing, zero, zip… It is IMPOSSIBLE to discern.

At this point all positive analysis is incomplete or requiring devine intervention. If that is your bag, then go for it.

vonbeeler wrote:

As far as my

[quote=vonbeeler]

As far as my house I’m getting my tax advantage and building equity. I wish I was a buyer for another property.[/quote]

Why aren’t you? Ah. Maybe you can’t b/c of credit or income or down?

That’ll be the problem for many who have already purchased. And that pool will shrink, IMO.

Considering the money the government has thrown at this problem and the incentives/tax credits and that it is spring/summer and that banks are being subsidized, therefore not foreclosing, but rather letting defaults continue for sometimes a year, this increase does not surprise me. I expect that people will buy. That is the whole goal of the forces at work.

The question is, can it continue? I expect this winter to be somewhat different. Maybe it’ll be the winter of discontent.

jpinpb][quote=vonbeeler

[quote=jpinpb][quote=vonbeeler]

As far as my house I’m getting my tax advantage and building equity. I wish I was a buyer for another property.[/quote]

Why aren’t you? Ah. Maybe you can’t b/c of credit or income or down?

quote]

Ah no and no. Never been an RE investor just an owner.

My point was that now is a good time to buy. For the doomsayers its usually never a good time until they miss the boat. Happens in every cycle.

No one can pick the bottom so if there is value and you need a home now is a good time. Will this winter be better? Who cares.

vonbeeler wrote:For the

[quote=vonbeeler]For the doomsayers its usually never a good time until they miss the boat.

[/quote]

Wow. 2006 called and they want their cliched straw man arguments back.

[quote=vonbeeler]Will this winter be better? Who cares.[/quote]

I don’t know about you but if I bought a home and two years later it was worth 20% less than I paid, I would care a great deal.

I think we will continue to

I think we will continue to be in a situation where there are no good fundamentals to grab hold of. Basic analysis of various indicators would suggest that what should happen is about the opposite of what IS happening.

So far it is hard to argue that the measures that the govt has took and will continue to take are not doing pretty much exactly what the govt hoped. No matter HOW DAMAGING they will be in the future.

Astute observers I think are just now starting to realize how manipulated the markets are and just how powerful the government is. We are now in an era where pretty much any legislation can and will be passed no matter what the population thinks. As damaging as the continued spending will be, I do feel it is more unrealistic to think that the walls are going to come crashing down. I stopped believing that long ago.

As always this is not an endorsement to buy. It is simply a statement that I have never lived in such a bizarre time. I have never seen our country in such a situation, nor have I ever trusted my government less. Meanwhile with all the unemployment and debt the stock markets chug towards 10,000, home sales are up, and our own leaders are claiming that they have effectively fixed things.

All that Rich is doing is pointing out the numbers. One thing that numbers do not do is that they do not lie as long as the data that they are extracted from is real data.

I would say that those waiting for big declines should strap in. Again, we are segmented and high end is where the biggest and best drops will be. Other homes in the 600k and less range have turned the other way if they are in decent areas.

I’m waiting for a similar

I’m waiting for a similar thread this December. It’ll be very telling what’s going on right now. What would the bear say if the run up continue through this Winter? What would the bull say if RE come crashing down this winter?

AN wrote:I’m waiting for a

[quote=AN]I’m waiting for a similar thread this December. It’ll be very telling what’s going on right now. What would the bear say if the run up continue through this Winter? What would the bull say if RE come crashing down this winter?[/quote]

Just read the previous article (Ramsey Su), the employment reports and adjust for the % of mortgages in default.

BGinRB wrote:

Just read the

[quote=BGinRB]

Just read the previous article (Ramsey Su), the employment reports and adjust for the % of mortgages in default.[/quote]

I did, and still don’t get what you’re talking about.

AN wrote:BGinRB wrote:

Just

[quote=AN][quote=BGinRB]

Just read the previous article (Ramsey Su), the employment reports and adjust for the % of mortgages in default.[/quote]

I did, and still don’t get what you’re talking about.[/quote]

I am looking at the aggregate sales – the chart says we are back at September or October 2008 levels. So, what is different today?

– The unemployment is up.

– High paying professional jobs are being lost or replaced by low paying/no benefits service jobs.

– NOD’s (mortgages in default) are up.

– $7.5K no interest loan from the government turned into $8K gift.

Today’s balance is not brought to you by organic supply/demand. The supply is severely constrained. There are houses where the initial NOD’s are more than a year old.

There are now houses with the initial NOT’s more than a year old.

And there are many reasons why servicers allow people not to pay their mortgages. One of them, they get to charge late payment and processing fees and they are first to collect if the property goes into foreclosure. It is you, the taxpayer, who will get to hold the bag.

What would to say if the government says that no house can be sold at PPSF price lower than the last month’s median for the given zipcode? If the lowest offer on a property after 30 days on MLS is less than prescribed value the government will cover the difference.

BGinRB wrote:

I am looking at

[quote=BGinRB]

I am looking at the aggregate sales – the chart says we are back at September or October 2008 levels. So, what is different today?

– The unemployment is up.

– High paying professional jobs are being lost or replaced by low paying/no benefits service jobs.

– NOD’s (mortgages in default) are up.

– $7.5K no interest loan from the government turned into $8K gift.

Today’s balance is not brought to you by organic supply/demand. The supply is severely constrained. There are houses where the initial NOD’s are more than a year old.

There are now houses with the initial NOT’s more than a year old.

And there are many reasons why servicers allow people not to pay their mortgages. One of them, they get to charge late payment and processing fees and they are first to collect if the property goes into foreclosure. It is you, the taxpayer, who will get to hold the bag.

What would to say if the government says that no house can be sold at PPSF price lower than the last month’s median for the given zipcode? If the lowest offer on a property after 30 days on MLS is less than prescribed value the government will cover the difference.[/quote]

Once again, all that is great and good (I agree with most of it), but I’m saying it’ll be interesting to see December’s data. So, we have to wait another 4 months to find out what that data looks like. Who would have guess this July data 8 months ago?

sdcellar, I know you lack the ability to read the data and make your own analysis, but I’m only interested in the data. I like to make my own analysis. People can lie, data cannot.

http://www.cnbc.com/id/158376

http://www.cnbc.com/id/15837671

realtytrac’s head is seeing contradictory data that says foreclosures can increase and housing can recover simultaneously. It comes down to affordability, the 90% with jobs can buy half priced homes. If unemployment only went to 7%, if there were no bailouts or stock market crashes, if there was a soft landing last year and houses went down only 20%, would that make you bullish on R/E, it wouldn’t do it for me. I’m bullish because of the bad news. I’m bullish because 50% off was the goal and it arrived. If unemployment hits 15%, I’ll leverage everything and buy rentals because nobody else will and I’ll get them for even less, at least in theory. Right now the best I can find on newer rentals under 100x rent multipliers is 30 cents on the dollar from peak. Right now, that has 10 people in line and is bid up about 10%, still a bargain at 40 cents on the dollar, but not my goal. No matter what happens macroeconomically, until those 10 bids stop coming in, it’s not going down any more.

The realtytrac guy and Olick have traditionally been bearish and a notch below the main stream meadia. This winter is the last chance at the bottom, by this time next year, the main stream media will declare housing has bottomed and even more fence sitters will jump along with with their friends, they wont do it because they will make a killing, they will do it because they can afford it at current prices.

TG, you better tone down your

TG, you better tone down your questionable bullishness, unless you already got your flame suit on. Don’t you know, we’re only in the 5th inning? We’ll have another 50% decline before we hit bottom. Affordability means nothing, didn’t you get the memo?

AN wrote:TG, you better tone

[quote=AN]TG, you better tone down your questionable bullishness, unless you already got your flame suit on. Don’t you know, we’re only in the 5th inning? We’ll have another 50% decline before we hit bottom. Affordability means nothing, didn’t you get the memo?[/quote]Again, attacking me indirectly. Weak.

Most of everything I read that TG posts makes solid sense. He’s also quite correct when he points out that the San Diego market isn’t his market. You, on the other hand, must miss that.

Did I say it was the 5th inning? Did I come anywhere close to saying there’s another 50% (in all markets according to you) to come. Nope.

You know how I said there were a few who made smart buys and then there were the others. TG was one of the smart ones I was talking about.

I guess you needed the flame

I guess you needed the flame suit AN, not me.

may I propose a truce between you two, sdceller, props for not making the argument nasty and taking the high ground, but I think AN was just playing a little, he gets like sometimes, as we all do, he means no harm. In time you’ll love him like a brother, little spats are just part of that process.

I must say, throwing props to sdrealtor and me in the same thread might get your card pulled from the other bears, it’s risky to side with the contrarians, especially those who were formerly bears and defected. I’m delusional enough to think that i haven’t changed, but the group has changed, kinda like everyone took a step back and I look like I took a step forward to volunteer.

In case anyone is keeping score, it’s the 7th inning, month 19 of 24, ends in december with unemployment peaking in June 2010, so there still some ball to be played. The problem is that the various markets are in different time zones so it may be a different inning in some markets, check your own scoreboard. 2001 pricing or half of peak should be what everyone gets, I’m still pulling for you guys, we will just have to wait and see.

temeculaguy wrote:I guess you

[quote=temeculaguy]I guess you needed the flame suit AN, not me.

may I propose a truce between you two, sdceller, props for not making the argument nasty and taking the high ground, but I think AN was just playing a little, he gets like sometimes, as we all do, he means no harm. In time you’ll love him like a brother, little spats are just part of that process.

I must say, throwing props to sdrealtor and me in the same thread might get your card pulled from the other bears, it’s risky to side with the contrarians, especially those who were formerly bears and defected. I’m delusional enough to think that i haven’t changed, but the group has changed, kinda like everyone took a step back and I look like I took a step forward to volunteer.

In case anyone is keeping score, it’s the 7th inning, month 19 of 24, ends in december with unemployment peaking in June 2010, so there still some ball to be played. The problem is that the various markets are in different time zones so it may be a different inning in some markets, check your own scoreboard. 2001 pricing or half of peak should be what everyone gets, I’m still pulling for you guys, we will just have to wait and see.[/quote]

TG,

You know I agree 100% with the 50% off and/or 2001 prices…but, in our area, prices are still at or near peak. I’ve even seen some ***MAKE MONEY*** as they’ve sold for over “peak” prices during this latest frenzy.

Personally, I’m not willing to step into this mess until rates rise. Of course, we might end up by-passing our “family” home and going straight for our retirement pad with the way things are going. 🙁

CA, you are smart to wait if

CA, you are smart to wait if your target neighborhood hasn’t taken it’s hit yet or you might be the one to take the hit. I honestly don’t follow coastal SD other than what I read here, but Rich posts charts that show Sd county is down close to 50% from peak, this thread alone starts with charts depicting the aggregate at exactly 50% off per sq ft., so it the neighborhood you like hasn’t gone down, then some other neighborhood has gone down even more than 50%.

One of two things will happen, your chosen hood will catch up to the rest of the county or you may end needing to break out a map book.

I do see the pressure you are under, it seems every reason for the wind to come out of the higher end coastal areas is met with something that prevents it, over and over and at some point you have to wonder if the bargains will run out in the other places. You’ve got time, it will be a few years before appreciation sets in again, what is happening in the other areas is price stabilization, not price appreciation.

temeculaguy wrote:

…. what

[quote=temeculaguy]

…. what is happening in the other areas is price stabilization, not price appreciation.[/quote]

Thanks, TG. I’ve said this before on other threads. People calling bottom seem to think that tomorrow prices are going up and we’ll be missing the boat. All the efforts by government, all the money, all the moratoria is attempting to “soft land” this mess.

I think the goal is to stablize, to prevent further damage. I don’t see prices shooting up any time soon. But maybe there’s something else up their sleeves. If they do NINA loans again, then I believe prices will go up. Right now, I don’t know what it will be.

Having to qualify and prove you can make the payments puts a limit on prices for many. Using FHA is helping w/the low and median priced homes, which is moving quickly.

Whenever we do have inflation, we may see home prices increase. But you still need to have a buyer w/money down and proof of ability to make payments. Unemployment could effect that. I know it’s been said that’s the last to recover. Nevertheless, it’s a factor when buying a house.

FWIW, NCC prices are solidly

FWIW, NCC prices are solidly down 20% or more in most of even the best hoods. Homes down well into 6 figures are not selling at or close to peak by my definition. Over 3 years ago, I called for 30 to 35% off in my hood at the bottom in a worst case scenario with 5 to 10% drops in the first 3 years followed by a slow bleed after that. This is exactly what has happened.

A couple years ago I tried to explain that prices rise in dollars not percentages and was dismissed (even by the professor himself). It is what happened and what is happening to a large degree. In January 2004, just about every property went up by $100 to 150K almost overnight. Over the peak of the bubble appreciation year (Spring 2003 to Spring 2004), homes in Oceanside went from 350 to 550 while homes in La Costa went 500 to 700 and from 750 to 950 for the most part. The percentage gains were no where near what they were in Oceanside than what they were in La Costa. Don’t expect 50% drops here because you got em in Oceanside. The percentage gains werent the same on the way up and wont be on the way down. Dont lose sight of that simple reality, lest you will be disappointed.

sdrealtor wrote:A couple

[quote=sdrealtor]A couple years ago I tried to explain that prices rise in dollars not percentages and was dismissed (even by the professor himself). [/quote]

I “dismissed” it because if you look back at the 1990s bust, the high tier fell by a HIGHER percentage than the low tier. So what i don’t agree with is the idea that it’s a law of real estate nature that prices move up and down in dollar terms instead of percent terms, as that’s not what happened in the prior bust.

This time around the low end moved up a much higher percentage, but that imho had more to do with the subprime boom. The net result was that cheaper properties moved up a higher percent, and thus moved up similar dollar amounts — and now they are doing so on the downside. But the data from the 90s boom/bust suggest that this was due to financing conditions that were unique to this cycle, not because it’s “how it works”.

While i’m chiming in, i will second CAR’s note that the Fed left themselves huge amounts of wiggle room to expand their monetization. If rates get too high, “prevailing conditions” will induce them to start monetizing again. (If they ever even stop.)

rich

One question that’s on my

One question that’s on my mind is, does the conforming rate have anything to do with what the price settle down at. We all know that price premium contracts in a down market. However, I think we all assumed that it contracts to what is considered affordable. As we’ve seen so far this Spring, even against one of the worse macroeconomic back drop, J6P are still out there buying. So, does that mean that as long as someone is willing to lend them money, they’ll keep on buying?

So, last year conforming rate were $417k, so it seems like everything was ratcheting down to that level quickly. However, how that the government have increased the conforming rate, are we going to see that level as what we’ll settle to? Do you have info on the conforming rate in the mid 90s?

Need to double check my

[img_assist|nid=11710||link=node|align=left|width=100|height=60]

Need to double check my median prices, but looks like whacky loans have had a far greater impact (or at least there’s no strict correlation to the conforming loan limit). They make a difference no doubt, but it’s just one piece of the cheaper money puzzle.

I suspect it played a greater role back in the day of less nuttiness. Perhaps it will again.

Thanks for the chart

Thanks for the chart sdcellar. Based on that chart, median price traced conforming rate between 1980-2001 (with some minor swings above and below the conforming line). 2001 is when the extreme funny money went into effect, which is why we have a massive upswing. Now, we had a massive swing below the conforming limit. My feeling is that FHA is funny money, but they’re limited by the conforming rate. That might be why we saw median price tracing conforming rate so closely. People have always been and will always want to buy a home. The main deterrent is whether they can get a loan or not. With FHA, you don’t need very much to qualify. So, the funny money will always be there (FHA).

FYI, the conforming limits

FYI, the conforming limits are supposed to track the median and are adjusted to changes in the median so the conforming limit should be impact by prices not vice versa.

sdrealtor wrote:FYI, the

[quote=sdrealtor]FYI, the conforming limits are supposed to track the median and are adjusted to changes in the median so the conforming limit should be impact by prices not vice versa.[/quote]

If this is the case, then are we expecting conforming rate to drop down to the mid 300s soon? Conforming limit stayed the same between 1993-1995 @ $203,150. It then went up in 1996. But median bottomed out in 1996. One other thing I noticed is that since 1980, conforming limit never went down, it only stayed flat.

AN wrote:One other thing I

[quote=AN]One other thing I noticed is that since 1980, conforming limit never went down, it only stayed flat.[/quote]Have you generally noticed the government lower much of anything? Governments grow, that’s just what they do. I was a little amazed that they held it at $417 recently (but they really didn’t, did they?).

Before all of this, I thought raising the limits was a good thing. Now that I understand the world better, I realize the cost.

sdcellar wrote:AN wrote:One

[quote=sdcellar][quote=AN]One other thing I noticed is that since 1980, conforming limit never went down, it only stayed flat.[/quote]Have you generally noticed the government lower much of anything? Governments grow, that’s just what they do. I was a little amazed that they held it at $417 recently (but they really didn’t, did they?).

Before all of this, I thought raising the limits was a good thing. Now that I understand the world better, I realize the cost.[/quote]

Up until last election, I was idealistic, thinking the government is the solution to everything. The more I poke around, the more I find that they’re more of the problem than the solution in a lot of cases. But, they are the house and they create the rules. Either you accept the rules and play by their rules or move to a different country. You give them an inch and they’ll take a mile.

In 2005, when the crash went underway, I thought free market would take this back to well below affordability level (i.e. well below the historical mean). However, I start to notice that they (the government, the house, the rule maker) start to interfere. They don’t want this thing to crash hard and revert well below the mean. They just want it to fall enough to get their agenda through. Unlike you, I never thought raising the limit was a good thing. I always viewed it as one way for them to manipulate the market. FHA is the funny money and conforming limit is their sandbox border. Increase the limit will just give them a bigger sand box to play in and you’ll never able to make it smaller again. Call me bullish if you like, but I think of myself as more of a realist. I personally think that the house will always win. The house always prefer inflation over deflation, and their action over the history of the fiat currency shows it. I think our government and the fiat currency will last much longer than we can stay alive. I’m not one of those who think the US and the world economy will collapse and us going back to the dark ages anytime soon.

BTW, before you jump down my throat again and call me an insensible bull, I just want to put a disclaimer out there. This is my opinion, agree to it or disagree to it at your own will. I say it like how I see it. No agenda.

AN wrote:sdcellar wrote:AN

[quote=AN][quote=sdcellar][quote=AN]One other thing I noticed is that since 1980, conforming limit never went down, it only stayed flat.[/quote]Have you generally noticed the government lower much of anything? Governments grow, that’s just what they do. I was a little amazed that they held it at $417 recently (but they really didn’t, did they?).

Before all of this, I thought raising the limits was a good thing. Now that I understand the world better, I realize the cost.[/quote]

Up until last election, I was idealistic, thinking the government is the solution to everything. The more I poke around, the more I find that they’re more of the problem than the solution in a lot of cases. But, they are the house and they create the rules. Either you accept the rules and play by their rules or move to a different country. You give them an inch and they’ll take a mile.

In 2005, when the crash went underway, I thought free market would take this back to well below affordability level (i.e. well below the historical mean). However, I start to notice that they (the government, the house, the rule maker) start to interfere. They don’t want this thing to crash hard and revert well below the mean. They just want it to fall enough to get their agenda through. Unlike you, I never thought raising the limit was a good thing. I always viewed it as one way for them to manipulate the market. FHA is the funny money and conforming limit is their sandbox border. Increase the limit will just give them a bigger sand box to play in and you’ll never able to make it smaller again. Call me bullish if you like, but I think of myself as more of a realist. I personally think that the house will always win. The house always prefer inflation over deflation, and their action over the history of the fiat currency shows it. I think our government and the fiat currency will last much longer than we can stay alive. I’m not one of those who think the US and the world economy will collapse and us going back to the dark ages anytime soon.

[/quote]

Put your money behind your thesis then. The government tried to interfere back when this happened last in early last century and failed. You can’t stop a massive deflationary credit collapse but with policy and so-called “printing” and “stimulus” you can slow it down but the underlying problem remains. There is too much debt that cannot be serviced and all that the Gov’t is doing is transferring that to the taxpayer. The effect is a bullish retrace in all asset classes but the fundamentals are still far from sound so there will be more violent waves to the downside. That will happen quickly if the Gov’t credit line gets turned off or slowly when unemployment continues to rise and the consumer hits the brick wall. Fiat currency or not beyond the room for the Gov’t to play in the markets there are limits and we saw the limit nearly hit when the Fed decided to reverse policy on QE because the dollar was taking too much of a hit. On top of this the FDIC yesterday became unofficially insolvent with the takeover of Colonial bank and that org will now be a further drain on the Treasury complex. To top that the FHA program is rumored to be close to imploding and Ginnie’s CEO left the ship as rats tend to do. Be bullish all you want the underlying info/data/support is not there for anything more than a short term bounce.

Psychic momentary thought

Psychic momentary thought tells me that the coastal areas will drop more then the cheap areas did in the coming years. The 90’s drop was primarily related to job loss and as Rich pointed out the higher tier suffered more then, I believe history will repeat itself. I closed in February fully believing that I would see a 20% drop before bottom and now Zillow says it is zestimated 93% higher than the sales price 6 months ago. Does not make any sense when the average ppf in our area has dropped 10-15%. One other thing that is weird is that according to Rich’s post 29% of listings are contingent, well from SDLookup it appears that the number is closer to 75% in my zip code, for SFR,what’s up with that? By the way the ones that don’t have contingencies are in the higher end of this zip.

capeman wrote:

Put your money

[quote=capeman]

Put your money behind your thesis then.[/quote]

I did.

Buy another one! 😉

Buy another one! 😉

capeman wrote:Buy another

[quote=capeman]Buy another one! ;-)[/quote]

As I said earlier, there’s the catch. Some people who bought, can’t buy again. Remember, now you have to prove you can make the payments and if you already bought, you have to prove you can make payments on more than one place, come up w/down, etc. As much as some people want to buy more, they are limited by these constraints and can’t. Hence, the pool of buyers continues to shrink. Those 70% of people who bought during the bubble, the people who have bought as the bubble was deflating, and last, the hold-outs.

[edit]hadn’t read sdrealtor’s

[edit]hadn’t read sdrealtor’s post when I wrote this, so might be a bit repetitive (and sadly, wordier…)[/edit]

Yes, but I also believe there’s also a cause/effect that actually swings back and forth with regard to the conforming limits. As I understand it, one of the factors that affects what the limit is set to *is* the median price. So in some years, median pulls the limit and in others the limit helps tug the median along.

Coastal California is an interesting case since they really have seemed closely related historically. Wouldn’t seem to be that way in many other parts of the country though.

Nonetheless, it is just one of the other knobs for some Fed thing to screw with to pull the market along. We might not have subprime any longer, just low rates in what we’re told is a tight credit market and enormous amounts of dollar bills being printed to support it. We also know that they can make exceptions whenever/whereever they want–witness the temporary limit increases.

Sigh… so now it’s just the fed __fill-in-the-blank__. I liked it better when I *thought* it was indepedent financial instituions and investors putting there own funny money at risk. Of course, that turns out to not really have been the case either.

Agree with your rational 100%

Agree with your rational 100% Professor that “it was truly different this time” because of the subprime nonsense. Then again, it’s always different. As nice as it would be to beleive that history repeats itself, it never does exactly. There are always nuances and differences in how things play out each time..

sdrealtor wrote:FWIW, NCC

[quote=sdrealtor]FWIW, NCC prices are solidly down 20% or more in most of even the best hoods. Homes down well into 6 figures are not selling at or close to peak by my definition. Over 3 years ago, I called for 30 to 35% off in my hood at the bottom in a worst case scenario with 5 to 10% drops in the first 3 years followed by a slow bleed after that. This is exactly what has happened.

A couple years ago I tried to explain that prices rise in dollars not percentages and was dismissed (even by the professor himself). It is what happened and what is happening to a large degree. In January 2004, just about every property went up by $100 to 150K almost overnight. Over the peak of the bubble appreciation year (Spring 2003 to Spring 2004), homes in Oceanside went from 350 to 550 while homes in La Costa went 500 to 700 and from 750 to 950 for the most part. The percentage gains were no where near what they were in Oceanside than what they were in La Costa. Don’t expect 50% drops here because you got em in Oceanside. The percentage gains werent the same on the way up and wont be on the way down. Dont lose sight of that simple reality, lest you will be disappointed.[/quote]

Not disagreeing with anything you’ve said here except for the “solidly down 20%” part. I would have agreed with you on that in late 2008/early 2009, but have been witnessing some crazy-insane stuff these past few months. From what I’m seeing, sellers are now regularly listing at over 2005/2006 prices, and many of them are actually getting it!

BTW, like Rich said, the big push during this cycle was from the bottom up. I’ve always believed prices would drop 35-50%, depending on the area. In our target areas, there is very little decent inventory, and prices seem to have rebounded from the 15-25% drops (from peak) witnessed a while back.

If I believed the recent buying/selling activity was due to organic supply/demand factors, we’d be buying already. The problem is that the market is so heavily manipulated right now on both supply (deadbeats not being foreclosed on, moratoriums, loan mods, etc.) and demand (seller-assisted down payments, $8,000 tax credits, $10,000 state tax credits for new homes, and artificially suppressed interest rates, etc.), it’s impossible to accurately predict what’s going to happen going forward **over the long run.**

In the short term, it would appear obvious that the above programs would boost sales and prices. I’m more concerned about the eventual, long-term consequences of these actions.

temeculaguy wrote:I guess you

[quote=temeculaguy]I guess you needed the flame suit AN, not me. [/quote]

I never took my flame suit off since last December. With regards to sdcellar, he’s officially on my ignore list, so there’s no need for a truce. It’s all fun and game to me now, especially quoting sdcellar. There never was a constructive debate with him. It has always been, either you agree with him, or you lack common sense.

AN wrote:With regards to

[quote=AN]With regards to sdcellar, he’s officially on my ignore list[/quote]Sure I am. Just another thing you’re kidding yourself about again, I suppose.

[quote=AN]It’s all fun and game to me now, especially quoting sdcellar. There never was a constructive debate with him. It has always been, either you agree with him, or you lack common sense.[/quote]Again, to continue with my example, I’ve disagreed with sdrealtor plenty in the past. Never suggested he lacked common sense and I’ve learned a lot from him.

The debate isn’t constructive because you struggle to stay on point, especially when it’s not what you want to hear.

What did I tell you TG, it’s

What did I tell you TG, it’s like being in HS all over again. You’re trying your best to ignore someone, but that someone keep on trying to talk to you. Ahhh, the memories. So glad I’m not in HS anymore.

AN wrote:So glad I’m not in

[quote=AN]So glad I’m not in HS anymore.[/quote]Are you sure? You are *killing* me. I am now laughing out loud.

temeculaguy wrote:may I

[quote=temeculaguy]may I propose a truce between you two, sdceller[/quote]man, I was on board (at least for the day, this thread, something!), but then the rationalizer had to get right back to it.

temeculaguy wrote:In case

[quote=temeculaguy]In case anyone is keeping score, it’s the 7th inning, month 19 of 24, ends in december with unemployment peaking in June 2010, so there still some ball to be played. The problem is that the various markets are in different time zones so it may be a different inning in some markets, check your own scoreboard. 2001 pricing or half of peak should be what everyone gets, I’m still pulling for you guys, we will just have to wait and see.[/quote]Anyhoo, I’ll try to get back closer to topic myself. Yes, this is pretty much where my head is at as well. The notable exception is 2001 pricing (or half peak) for everyone (but also understand you’re rooting, no guarantee). I’d sure like that to be true, but afraid it may not turn out that way, at least for the areas I’m interested in (NCC and then heading eastward along the 56).

That said, I’m not panicing quite yet, but I’m doing my best to be pragmatic about it all. I would like to settle into a place before I’m into my next decade–pretty sure at least that part will happen.

temeculaguy

[quote=temeculaguy]http://www.cnbc.com/id/15837671

realtytrac’s head is seeing contradictory data that says foreclosures can increase and housing can recover simultaneously. It comes down to affordability, the 90% with jobs can buy half priced homes.[/quote]

That scenario could survive a double-dipper?

smshorttimer

[quote=smshorttimer][quote=temeculaguy]http://www.cnbc.com/id/15837671

realtytrac’s head is seeing contradictory data that says foreclosures can increase and housing can recover simultaneously. It comes down to affordability, the 90% with jobs can buy half priced homes.[/quote]

That scenario could survive a double-dipper?[/quote]

Who knows? can it survive a nuclear war or a mega earthquake? Does it matter? Buy a house that is 3 times your gross income or less, take a loan that is even less and it wont matter, double dip, U, W, L or even a tripple lundy (ala Rodney dangerfield), put your financial house in order, bite off less than you can chew and ignore the macro picture.

AN wrote:sdcellar, I know you

[quote=AN]sdcellar, I know you lack the ability to read the data and make your own analysis, but I’m only interested in the data. I like to make my own analysis. People can lie, data cannot.[/quote]I don’t even know what your deal is (other than your knack for changing the subject). You’re the one who (misguidely, in my opinion) suggests Rich is bullish in reporting the data in this article. It seems pretty clear that I’m still bearish even in light of this springtime (and now summertime) frothiness. You’re mostly bullish, but lately you’ve been more waffle-ish. I do know you’ve posted the “hey, rich don’t be bullish, sdcellar doesn’t like it” thing two or three times now. That seems like a non-data based interjection (which is fine by me, but ? by you?)

Man up and answer my questions (or don’t, but don’t keep changing the subject). You suggested Rich was bullish with this article. Do _you_ think he was?

…and don’t get me wrong, Rich can be as bullish as he wants. Based on his track record, I’d certainly heed that more than some of the other opinions I’ve seen.

Do I only respect the bearish opinions? Nope. sdrealtor’s put forth many things that aren’t necessarily what I want to hear, but man, that dude’s right a lot. I’m also not saying he’s a bull, but he certainly isn’t always feeding me honey.

bigmoneysalsa wrote:vonbeeler

[quote=bigmoneysalsa][quote=vonbeeler]For the doomsayers its usually never a good time until they miss the boat.

[/quote]

Wow. 2006 called and they want their cliched straw man arguments back.

[quote=vonbeeler]Will this winter be better? Who cares.[/quote]

I don’t know about you but if I bought a home and two years later it was worth 20% less than I paid, I would care a great deal.[/quote]

Your not getting it.

vonbeeler wrote:Ummm. OK.

Who

[quote=vonbeeler]Ummm. OK.

Who cares if it really is the bottom. Its attractive. Very attractive in some cases. These comments were the same comments I heard about equities back in March.

As far as my house I’m getting my tax advantage and building equity. I wish I was a buyer for another property.[/quote]

What is stopping you? Extract some of the existing equity and use it as seed money. It worked so well in 2005, why not do it again?

BGinRB wrote:

What is

[quote=BGinRB]

What is stopping you? Extract some of the existing equity and use it as seed money. It worked so well in 2005, why not do it again?[/quote]

Never been an extractor but hey thanks for the great idea. Sounds familiar, Is Countrywide hiring?

vonbeeler wrote:BGinRB

[quote=vonbeeler][quote=BGinRB]

What is stopping you? Extract some of the existing equity and use it as seed money. It worked so well in 2005, why not do it again?[/quote]

Never been an extractor but hey thanks for the great idea. Sounds familiar, Is Countrywide hiring?[/quote]

You are welcome. It is always good time for one to put some money where one’s mouth is.

Re countryfried, research pennymac.

BGinRB wrote:vonbeeler

[quote=BGinRB][quote=vonbeeler][quote=BGinRB]

What is stopping you? Extract some of the existing equity and use it as seed money. It worked so well in 2005, why not do it again?[/quote]

Never been an extractor but hey thanks for the great idea. Sounds familiar, Is Countrywide hiring?[/quote]

You are welcome. It is always good time for one to put some money where one’s mouth is.

Re countryfried, research pennymac.[/quote]

Nevermind, guess that one went right over.

vonbeeler wrote:…and

[quote=vonbeeler]…and building equity.[/quote]Really? This year? Next year? Over the next three? Ten? Clearly a speculative postion, but I’m curious to hear what you’re speculating–especially since it’s been put forth like a matter of fact. Perhaps in your case it’s historical gain?

sdcellar wrote:vonbeeler

[quote=sdcellar][quote=vonbeeler]…and building equity.[/quote]Really? This year? Next year? Over the next three? Ten? Clearly a speculative postion, but I’m curious to hear what you’re speculating–especially since it’s been put forth like a matter of fact. Perhaps in your case it’s historical gain?[/quote]

So I guess when my mortgage is paid off I won’t have any equity. OK.

As sdcellar once

As sdcellar once said:

[quote=sdcellar]…but if you’re going to spout questionable (as in none of us know) bullishness (especially here), be prepared to defend…[/quote]

So Rich, you might want to stop spouting questionable bullishness.

AN wrote:As sdcellar once

[quote=AN]As sdcellar once said:

[quote=sdcellar]…but if you’re going to spout questionable (as in none of us know) bullishness (especially here), be prepared to defend…[/quote]

So Rich, you might want to stop spouting questionable bullishness.[/quote]

Oh yes, ha ha ha, that’s a good one, you got me.

Or, at least you would have if you’d only posted this once or if you weren’t confused about the difference between reporting data and the reporter’s position on it. Did you read what Rich wrote? It didn’t sound too bullish to me.

You do grok that you can be a bear in a bull market and vice versa, right?

vonbeeler wrote:sdcellar

[quote=vonbeeler][quote=sdcellar][quote=vonbeeler]…and building equity.[/quote]Really? This year? Next year? Over the next three? Ten? Clearly a speculative postion, but I’m curious to hear what you’re speculating–especially since it’s been put forth like a matter of fact. Perhaps in your case it’s historical gain?[/quote]

So I guess when my mortgage is paid off I won’t have any equity. OK.[/quote]

Sorry, but your money wasn’t what immediately comes to mind when I think of equity. So, are you conceding that side of the “benefit”?

fredo4 wrote:

Instead of

[quote=fredo4]

Instead of buying something now, we’ve decided to move into another rental house that we like better.

[/quote]

me too

Ill tell you what I am

Ill tell you what I am looking for, I am looking to see what happens when the FED starts to unwind its lifesupport to the treasury and morgage markets. I feel that this support has done more to stop the falling housing prices than anything Bush/Obama/congress did. Just imagine if the FED stops the punishment of savers and actually allows interst rates to be set by the market. Maybe people wont care and will go out and buy no matter what and will disregard little things like interest rates, but I doubt it.

We wont have to wait till December numbers come out to find out what will happen, I am just gonna wait till the end of October, If rates spike up to pre-manipulation numbers of 6.5%+ this upturn will get pressured, especially since itll be the fall/winter.

DW I was thinking the same

DW I was thinking the same thing. The only problem with that is, (putting my tinfoil hat on) that will it matter?

What difference does it make if the FED makes publicized purchases or if the FED simply shuttles cash to the various windows so that the dealers can just make UBER purchases at the auctions?

I would agree 100% with you that the key to buying something you cannot afford is cheap credit. For all the whining that credit is hard to come by I call BS. Residential loans are NOT hard to come by right now. Now is the secondary market for them a dead zone? Yes it is. However for J6P to get a loan? Yes you need documentation and things take longer but J6P is getting his loan if he is qualified. The bottom line is rates. I tend to agree with you that 6.5% and above makes it a hell of alot harder.

I am interested like you indicated to see what will happen after the “official” program ends in October. However it will not surprise me if mysteriously things just seem to be maintained…

You brought up a good point.

SD Realtor wrote:I am

[quote=SD Realtor]I am interested like you indicated to see what will happen after the “official” program ends in October. However it will not surprise me if mysteriously things just seem to be maintained…

[/quote]

I am expecting it, though not right away. Itll be all over the internet and a major embaresment if they are caught lying to the public. Instead I think they will allow rates to spike up in fall when few are hurt, and will sneak into the market (in a hidden way) Feb 1 or so and buy down rates for the next spring rally.

SD Realtor wrote:DW I was

[quote=SD Realtor]DW I was thinking the same thing. The only problem with that is, (putting my tinfoil hat on) that will it matter?

What difference does it make if the FED makes publicized purchases or if the FED simply shuttles cash to the various windows so that the dealers can just make UBER purchases at the auctions?

I would agree 100% with you that the key to buying something you cannot afford is cheap credit. For all the whining that credit is hard to come by I call BS. Residential loans are NOT hard to come by right now. Now is the secondary market for them a dead zone? Yes it is. However for J6P to get a loan? Yes you need documentation and things take longer but J6P is getting his loan if he is qualified. The bottom line is rates. I tend to agree with you that 6.5% and above makes it a hell of alot harder.

I am interested like you indicated to see what will happen after the “official” program ends in October. However it will not surprise me if mysteriously things just seem to be maintained…

You brought up a good point.[/quote]

It’s a done deal, guys. IMHO, the stimulus will be with us until the Fed’s hand is forced (foreign govts flat-out reject the dollar…maybe???). I’m betting on ultra-low rates for an extended period of time, and for the $8,000 tax credit to morph into the $15,000 tax credit beginning next year. The Fed is buying over a **TRILLION** dollars worth of MBSs just this year!!!! That’s on top of its Treasury purchases which are artificially supressing all interest rates.

From yesterday’s FOMC meeting (bold is mine):

“Although economic activity is likely to remain weak for a time, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.” [assuming that “price stability” means they intend to keep prices artificially inflated…because “stability” in Fed-speak means that prices only go up]

AND

“In these circumstances, the Federal Reserve will employ all available tools to promote economic recovery and to preserve price stability. [there it is, again] The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period. As previously announced, to provide support to mortgage lending and housing markets and to improve overall conditions in private credit markets, the Federal Reserve will purchase a total of up to $1.25 trillion of agency mortgage-backed securities and up to $200 billion of agency debt by the end of the year. In addition, the Federal Reserve is in the process of buying $300 billion of Treasury securities. To promote a smooth transition in markets as these purchases of Treasury securities are completed, the Committee has decided to gradually slow the pace of these transactions and anticipates that the full amount will be purchased by the end of October. The Committee will continue to evaluate the timing and overall amounts of its purchases of securities in light of the evolving economic outlook and conditions in financial markets. The Federal Reserve is monitoring the size and composition of its balance sheet and will make adjustments to its credit and liquidity programs as warranted.”

http://www.federalreserve.gov/newsevents/press/monetary/20090812a.htm

meow, splat, boing

My crystal

meow, splat, boing

My crystal ball suggested that there will be another leg down in coastal SD. It didn’t say how much more though. I think I’ll wait until it is more apparent what is happening with the (lack of) inventory in light of record NODs and foreclosures.

The simple fact of the matter

The simple fact of the matter is that if you looked solely at prices and monthly payments, compared to income and rents (per Rich’s original analysis) todays’ prices and payments are at the low end of historical ranges.

FormerSanDiegan wrote:The

[quote=FormerSanDiegan]The simple fact of the matter is that if you looked solely at prices and monthly payments, compared to income and rents (per Rich’s original analysis) todays’ prices and payments are at the low end of historical ranges.[/quote]My thing is certainly rent vs. buy. Not there yet in my situation, but sure that others are.

sdr, I was one of those

sdr, I was one of those people who didn’t believe you at the time when you made the argument of $ increase instead of % increase. As this thing unwind, so far, it seems like you’re right on the money.

FormerSanDiegan wrote:The

[quote=FormerSanDiegan]The simple fact of the matter is that if you looked solely at prices and monthly payments, compared to income and rents (per Rich’s original analysis) todays’ prices and payments are at the low end of historical ranges.[/quote]

Rent vs buy has always been my #1 test too. As you stated, it’s a simple fact. Everyone can run their own number for the area they’re interested in. Some people have a harder time than others, understanding that every area is different. They take their interested area and extrapolate to the rest.

My Analysis Of This Market Is

My Analysis Of This Market Is As Follows:

[cue theme music from the Twilight Zone]

AN, I find myself reluctangly agreeing with you. I also thought that market forces would bring the prices down to a low bottom, and did not expect the degree of intervention from “the house” that we’ve seen. I keep waiting for “the house” to run out of gas and actual market forces to have their way. But like a roach you keep stomping on but it keeps on scurrying, “the house” just seems to be unkillable.

However some phenomena are robust right up until the instant they fall completely apart, and who knows, the Fed/banks holding onto these NOTs/etc may not be exempt from this rule either.

Like a number of other commentors, I am going to wait and see what happens round late September/October timeframe. If the macro economy seems to be hanging in there, I will move into a rental that I like better and wait for bottom in my neck of the woods.* On the other hand if the macro economy turns landing gear up and drills in toward the Marianas trench, I will stay in my current cheap rental, buy a sound-dampening Window Factory window for my bedroom vs the noisy neighbors, and wait out the storm.

*Up here in RB rents are close to buy for condos, but SFR are still more expensive to buy than rent.

CricketOnTheHearth, I totally

CricketOnTheHearth, I totally agree with you that SFR is still not close to rent parity yet in RB. RB, PQ, Scripps, Carlsbad and Sorrento Valley were all the areas I would rather buy in, if it was rent neutral. But it wasn’t and still isn’t. We both seem to agree on the problem, but our solutions are different. I chose to buy in an area near by where it is cheaper to buy than rent, while you choose to continue renting. In my eyes, both are correct answer. You do what feels right for you. If the government continue to interfere at the rate they are today, I have a feeling we might not see the bottom in the higher end until 2015-2020. Unless inflation take flight. I can’t stand renting for another 5-10 years, so I jumped in. If you can rent another 5-10 years, more power to you. Different strokes for different folks. That’s why freedom and individuality is so great. We all are not forced to follow anyone but ourselves.

Pretty good posts AN. PQ is

Pretty good posts AN. PQ is ridiculous. I had some clients close in PQ in February and the same floorplan is now 8% higher then when they closed.

It makes no sense.

sdrealtor, mad props to you,

sdrealtor, mad props to you, cogent statements. Some of my opinions were uninformed regarding the percentage increase of NCC dring the boom. Without getting into any numbers or years (since some here have pointed out that ncc boomed at different times than most places) let’s just say that once it gives back the increase that wasn’t supported by fundamentals, then that’s all it will give back. It’s your hood, you’ve made accurate predictions for a couple of years now, so I’m just going to trust your judgment, just remind me of this if the next time I contradict you.

I know everyone hates the permabull phrase about land being a finite commodity, but I was reading the mark twain quotes from a link aecitia left for me on another thread and he was actually the author of the phrase “buy land, they aren’t making it anymore.” It got me to think about my misguided forray into giving r/e advice regarding NCC. With each boom/bust cycle in the last fifty years, the population of the county has increased, while the narrow strip of land along the ocean from la jolla to carlsbad hasn’t grown in size, nor lost it’s appeal. It may just be that it will never be a middle class area ever again, it may see times of increased affordability, but not for everyone. Come to think of it, when I lived there 20 years ago, it wasn’t affordable then, it may only get worse over time.

sdceller, AN, nice to see you playing well, even without a brokered agreement and even if it feels forced, you guys are both valued players so at least keeping your hands to yourself is an improvement.

Just trying to keep it real

Just trying to keep it real whilst I try to figure out this whole Vick thing that’s got my head spinning.

temeculaguy wrote:

sdceller,

[quote=temeculaguy]

sdceller, AN, nice to see you playing well, even without a brokered agreement and even if it feels forced, you guys are both valued players so at least keeping your hands to yourself is an improvement.[/quote]

TG, nothing I said was forced. I give props when props is due. I do not like to instigate, but when people push me, I tend to push back. If anyone read my posts for the last 3+ years I’ve been here, I’m always about mortgage vs rent for a primary resident. I tried to give advice (when asked), based on the mortgage vs rent principle. But ever since I bought, although I’ve been saying the same thing for the last 3 years, I get flamed. sdcellar seemed to seek out my posts and flame me (I have no idea why, it’s not like I’m saying anything different than what I said 3-4 years ago). But now that he seems to put away the torch, I’ll gladly put away the flame suit.

AN wrote:If you can rent

[quote=AN]If you can rent another 5-10 years, more power to you.[/quote]Perhaps we can agree that there’s something between buying today and waiting five to ten more years?

sdcellar wrote:Perhaps we can

[quote=sdcellar]Perhaps we can agree that there’s something between buying today and waiting five to ten more years?[/quote]

Yes we can. It really depends on what type of house you’re looking for, what area you’re looking at, and how much more interference the government decides to do. I personally don’t like most of the houses built after 2000, so, I’m looking for houses built in 80s and 90s in RB, PQ, Scripps, Carlsbad, and Encinitas. I’m also looking for houses between 2000-3000 sq-ft. If the government continue interfere the way they are, I personally think these houses will bottom later than houses built around 2003-2006, since there’s a lot less distress. The owner can hold out for much longer. If you’re looking for houses built in 2003-2006 in these areas, they might bottom out earlier. If you’re looking for much older and smaller homes in less desirable location in these areas, they might have bottomed out already (or at least is already rent neutral).

capeman, remember, the calculation for primary resident vs rental property is very very different. Nothing w/in 20 minutes drive from me is any where near good enough to be purchased as a rental. I was looking for rental in south bay and Fresno, but I haven’t convinced myself to buy rental that far away. Taking mortgage vs rental ratio of Fresno, if I can find a decent looking SFR in MM for ~$200k, then I’ll probably buy a couple already. SFR in Fresno that rents for ~$1000 are going for around $75-95k right now.