Thanks to the fantastic folks at Calculated Risk for alerting me to Moody’s latest home price forecast.

According to Moody’s, the San Diego-Carlsbad-San Marcos triumvirate is in store for an aggregate home price decline of 10.9% between the peak (which they peg at Q1 2006) to the trough (Q4 2008).

While I’m all for mainstream outfits acknowledging that San Diego prices are going to drop, the particular forecast seems hopelessly optimistic in comparison to what’s happened already.

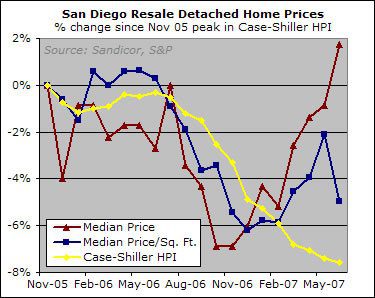

The S&P Case Shiller Home Price Index — which is as good a measure of aggregate price movements as you will find — indicates that San Diego home prices had already fallen 7.6% from their peak as of June. That reflects pricing on deals closed in May or even late April, which means that the prices reflect neither the effect of the credit crunch (round 2) nor the increasing prevalence of distressed inventory over the ensuing months.

Which is to say as of right now, aggregate prices have almost certainly declined more than the June HPI’s 7.6% (and that’s without even considering the fact that the HPI is probably overstating home prices because it has difficulty accounting for seller concessions or home improvements). We may be nudging up towards that 10.9% decline as we speak.

So it just seems a bit optimistic to assume that after all is said and done — "all" here referring to the unwinding of a record-shattering housing bubble that has led to widespread foreclosures, an abrupt tightening of mortgage credit, and real estate valuations that have nothing to do with their underlying fundamentals — that home prices are barely going to fall any more than they already have.

At least they’re back

At least they’re back peddling. Given the data you’ve been posting, that probably won’t change. Last October, they were calling a bottom sometime in Q2 2008 of 8.5%(edit: 8.5% off-peak, which they said was Q5 2005). How they come up with such “precise” numbers is beyond me.

http://money.cnn.com/2006/10/05/real_estate/moodys/index.htm

Anyone want to take a stab at what they’ll be saying next year around this time?

Agreed that the declines

Agreed that the declines they are estimating seem like too little in many markets.

Does anyone think, though, that we might reach the bottom more quickly in this bust than in prior ones? I wonder if better/more information about market conditions will speed the decline. Just musing on whether things like this blog and really good data like the case-shiller index might make the market more efficient.

One more thought….Heaven help Stockton…they’re screwed….

The Moody forecast is based

The Moody forecast is based on the median. Since the median is not down nearly as much as the more accurate measures such as the Case-Shiller index or even price/square foot measures they may end up being close to their target. For example, the C-S could end up with a net drop of 20-25%, while the median ends up dropping 10-15%. Granted, most of us know that the median is not an accurate indicator of price decline for a given property, and is a flawed metric.

Note: The gap between C-S and median is nearly 10% currently.

Great catch FSD… I didn’t

Great catch FSD… I didn’t even pick up on that throwaway line about how they are all median prices. They do seem to be equating the “median” and “home prices” — pretty unbelievable given the glaring disparity you cite in your comment.

Even still, I think it’s optimistic. I think the distortions in the median are temporary, and may even already have ended now that the credit crunch hit the higher end. So if “actual” prices (or as close as we can measure them, ie the Case Shiller index) are down in the high single digits, it seems optimistic to say that the median — which does a semi-decent job of tracking actual prices over long time periods — will only end up dropping 10.9%.

We will see. Actually, we may get an indication in a couple weeks… I think the Sept. data will be very telling on this front.

rich

Even still, I think it’s

Even still, I think it’s optimistic. I think the distortions in the median are temporary

I tend to agree. When things are closer to the bottom and even during the initial stages of a recovery, I think that the sales will be biased towards the lower-priced houses, which may drive the median down.

September data I believe

September data I believe will be quite revealing.

My Escrow is ending on September-28th.

The house was originaly built and sold as new in November 2005. So the price was a peak price by itself. Now I am getting it for 19% less to what it was sold back than.

This house was sitting on the market unsold in excess of 130 days. I am tracking the Carlsbad and San Marcos listings daily. Thinks are really really ugly – prices of 175$/SqFt for homes less than 5 years old and they are still sitting on the market unsold.

Prices are going down for sure. And more than 10% compared to the peak in 2005.

I don’t understand how the

I don’t understand how the median price would never show the real decline. My understanding is that the median is lagging the decline due to a different distribution of sales. More expensive homes are selling at a greater percentage of total sales than previous. It seems to me that the only way the median continues to lag “real” price depreciation is if the bottom end of the market never comes back. That doesn’t seem likely. If in an “up” market the opposite effect is supposed to take place then it seems the median will continue to decline after more accurate measures are on the rise.

Am I missing something here? If the median is artificially high now, shouldn’t it appear artificially low later?

people_are_smart… you are

people_are_smart… you are not missing anything. I don’t think it will necessarily appear artificially low, but once the distribution of sold homes returns to normal, the median should more accurately reflect prices. (You might see a sharp drop in the median that reflects not an actual drop in prices, but rather the median getting back into line — but that’s not the same as the median being artificially low).

Rich

“Anyone want to take a stab

“Anyone want to take a stab at what they’ll be saying next year around this time?”

They’ll be saying, “Prices in the San Marcos area have now fallen over 25% from their peak and we can not predict how far they will drop before they hit the absolute bottom.

Nah……they won’t ever print that………..they’ll just keep making absurdly low predictions and never mention how far off the mark they were with the prior predictions.

Confessions from a former

Confessions from a former mortgage broker:

This bottom calling (by Moody’s most recently) is truley rediculous. I am a former Mtg. broker who listened to a WAMU account exec during a meeting proudly announce (2-3 years ago) that 80% of WAMU’s portfolio holdings were Option ARMs, AKA: Pick a Pays, Cash Flow ARMS or Toxic Time Bomb Loans. The implosion of these loans, of which CA has the highest percentage, are going to make the subprime problem look like a walk in the park by comparison, folks.

Just to give you an idea, 2 years ago there was a tremendous number of Option ARMs with 620 FICO’s, stated income, a paltry 2 months of reserves required, combined loan to value of 90% of a unquestioned, overinflated appraised value. Many chose a 40 year minimum payment term which, in effect, facilitated the Neg Am feature of the loan by reducing the minimum payment more and increasing the fully indexed rate.

This may sound like Chinese Algebra to many of you, but bottom line is that since banks like WAMU had an initial recast mark of 125% of the loan amount, many of these loans (even though I’d bet my bottom dollar that most of these borrowers are upside down today) won’t start recasting to a higher payment for 3 more years…

These bottom callers that are saying Q408 are clueless…

justinmac,

I’d have to check

justinmac,

I’d have to check my rule book, but I don’t think you get credit here on Piggington’s for a post if you’ve previously posted it over on the Union-Tribune’s site. LOL.

Usually it goes the other way – shows up first on Piggington then migrates over to the U-T. BTW, I post over there under the handle “Cbad.”

BTW, good post – both of them.

justinmac

My sources confirm

justinmac

My sources confirm the same thing. I think between now and 3 years from now, WAMU will be in very dire straits