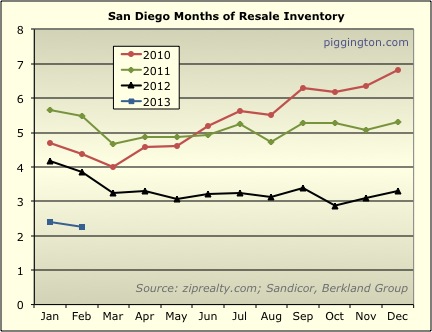

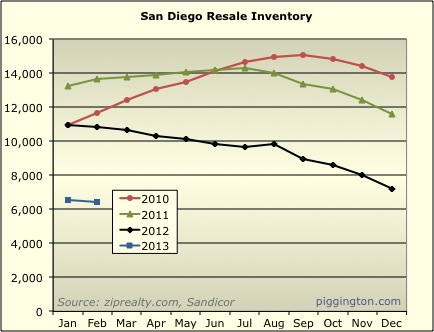

Would you happen to know how today’s inventory numbers compare to the inventory numbers during the spring of 2004? IIRC, that was the last low for inventory. It looks like we are at (or below) those levels now.

Just if you have the numbers at the ready, I don’t want to ask you to do any more work than you’re already doing on this.

Hi CAR — Unfortunately I

Hi CAR — Unfortunately I don’t have inventory data that far back… that would indeed be very interesting to compare. Maybe one of the realtors out there has that data?

Funny, just Googled it and Funny, just Googled it and found your article from 2006. 🙂

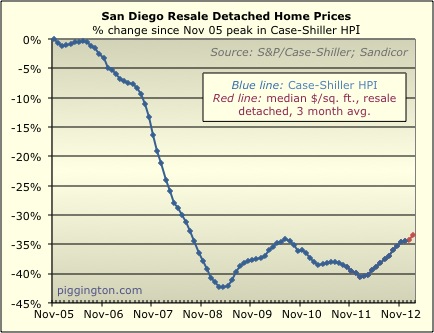

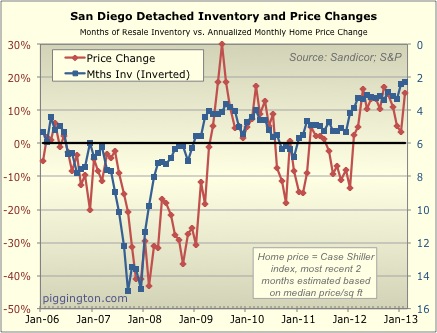

Many confused this temporary run on inventory with a longer-term structural housing shortage, but as the numbers above show, it was not. It was a short-term inventory drain caused by a temporary imbalance between buyers and sellers, which was in turn caused by a period of extreme homebuyer optimism, and it has already passed. The inventory of homes for sale, after reaching a low of around 2,000 in early 2004, is now back up to 15,000 and rising.

That prompted me to poke around more but I can’t seem to find any older inventory data. It looks like I had it at one point, though… here is a graph from a 2005-era post that goes back to mid-2004, after inventory had risen from the lows quite a bit already:

Interestingly we are right about where we were in summer 2004!

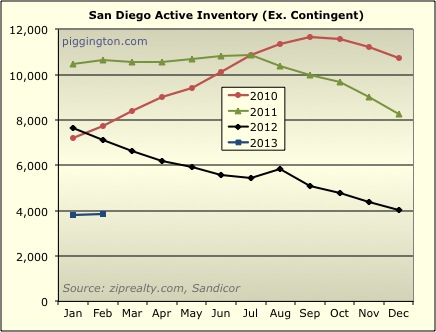

According to sdlookup San According to sdlookup San Diego city is just under 2,000 active listings currently and San Diego county is around 7,000. Just wondering are all graphs San Diego county or is there a mix.

moneymaker wrote:According to [quote=moneymaker]According to sdlookup San Diego city is just under 2,000 active listings currently and San Diego county is around 7,000. Just wondering are all graphs San Diego county or is there a mix.[/quote]

SD County. Numbers are probably different because mine were from mid-Feb.

CA renter wrote:Funny, just [quote=CA renter]Funny, just Googled it and found your article from 2006. 🙂

Many confused this temporary run on inventory with a longer-term structural housing shortage, but as the numbers above show, it was not. It was a short-term inventory drain caused by a temporary imbalance between buyers and sellers, which was in turn caused by a period of extreme homebuyer optimism, and it has already passed. The inventory of homes for sale, after reaching a low of around 2,000 in early 2004, is now back up to 15,000 and rising.

I hope everyone understands how very quickly market conditions like this can change, as evidenced by your last sentence, above.

Thanks, Rich…then and now! :)[/quote]

That article may very well be describing what’s going on currently with the housing market. IOW, should we expect another downturn in the housing market in the next couple years?

Not sure about when, but I’m Not sure about when, but I’m very convinced that we’ll be seeing another downturn — the completion of the recent downturn that was artificially stopped in its tracks via various govt and Fed manipulations.

Even with today’s low interest rates, people are still struggling with their housing payments because the price of everything else has been pushed up along with housing, thanks to the Fed’s irresponsible policies. 🙁

These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.

CA renter wrote:…These [quote=CA renter]…These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.[/quote]

I would suspect that the large REITS and even smaller investor groups will continue to hold these properties 5+ years from now if they don’t think they can get the prices they want due to higher prevailing interest rates. They really don’t have to sell if they don’t wish to as they don’t have mortgages.

However, in the past, rising interest rates never affected sales volume, unless the 30-yr fixed MIR was over 10%. And residential properties still sold to owner occupants even then, mostly with seller participation.

The only effect a higher MIR has on a homebuyer is to drop them down to a lower tier of home to buy. It does NOT preclude them from buying.

bearishgurl wrote:CA renter [quote=bearishgurl][quote=CA renter]…These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.[/quote]

I would suspect that the large REITS and even smaller investor groups will continue to hold these properties 5+ years from now if they don’t think they can get the prices they want due to higher prevailing interest rates. They really don’t have to sell if they don’t wish to as they don’t have mortgages.

However, in the past, rising interest rates never affected sales volume, unless the 30-yr fixed MIR was over 10%. And residential properties still sold to owner occupants even then, mostly with seller participation.

The only effect a higher MIR has on a homebuyer is to drop them down to a lower tier of home to buy. It does NOT preclude them from buying.[/quote]

These investment groups have investors who might want/need to cash out at 5-7 years. Not only that, but many investment groups are mortgaging the properties after acquiring them for cash, so they do occasionally have mortgages. The mortgages aren’t the problem, but redemptions certainly could be, and if interest rates are higher at that time, then the value of their RE investments will be lower. If the fund managers levered up the funds, there could be some serious problems.

Higher interest rates absolutely affect the prices of assets bought with credit. Under no circumstances will higher rates force people to buy a lower tier home because interest rates affect buyers all across the spectrum. People with certain education levels, and in certain professions, etc. expect to live in an area with their peers. The housing expectations of buyers will not change; their ability/willingness to pay a certain price for a given house is what will change. And cash buyers are every bit as sensitive to interest rates as mortgaged buyers because their money can earn decent returns in a higher interest rate environment, which will induce them to either use a mortgage or keep more cash in order to make more money on investments. Cash is dear when interest rates are high. Rich people don’t get rich by overpaying for things.

CAR, I’m not so sure these CAR, I’m not so sure these large REITs have any intentions of leveraging their massive (mainly distressed SFR) inventory they acquired within the last year or so. There was plenty of investor money to buy it with and plenty more coming in as being a “flipper” or “landlord” is not for everyone. As long as the REIT’s are paying their investors good to great dividends, why would they want to redeem and invest elsewhere … even if the CD/MM/bond interest rates go up?

The vast majority of properties these REITs bought in bulk were purchased at prices well under market (even in CA) and some were bought at less than land value. Certainly, they will make very profitable rental investments if they are not too encumbered with HOA/MR.

But mainly I disagree with this portion of your statement:

“Under no circumstances will higher rates force people to buy a lower tier home because interest rates affect buyers all across the spectrum. People with certain education levels, and in certain professions, etc. expect to live in an area with their peers. The housing expectations of buyers will not change; their ability/willingness to pay a certain price for a given house is what will change.”

Historically, when MIR’s were 7-12%, prospective owner-occupants and investors still bought residential RE. They bought what they could qualify for if taking out a purchase-money mortgage. “Education level” and “profession” had nothing to do with it. Assets and/or W-2/self-employment income had everything to do with it.

Those many cities in CA’s Silicon Valley (San Mateo and Santa Clara Counties, for example) are a case in point. Excepting one small area, “newer” (last 15 yrs) SFR construction there does not exist for 65+ miles, north to south, inclusive of SF and the majority of the housing stock is over 50 yrs of age. In the most expensive areas, most of the stock is 50-90 yrs old. A buyer using a $250K+ downpayment and taking out a $750K jumbo mortgage could very well be buying a <1500 sf charmer circa 1953 on a 6500K lot. No matter the "profession" or "educational level" of this SV worker/homebuyer, they have three options there: (1) buy a locally listed resale; (2) continue to rent locally or elsewhere (and commute to/from work every day); or (3) buy elsewhere and commute to/from work every day.

It doesn't matter what the prevailing MIRs are. If these "professional" workers don't like what is on offer there or feel they won't be living with their "peers" in those areas (due to age of stock and its longtime existing homeowners) or they don't like the "tier" they perceive these homes to be in (independent of actual cost), they will leave the area to shop elsewhere. These properties will sell regardless.

You can't choose your neighbors ... anywhere, most especially not in CA's finest coastal enclaves. A buyer/owner occupant gets what they get when they close escrow ... and those new neighbors may or may not be what they consider to be "representative of their peers."

In all RE climates, CA homebuyers must pay the prevailing interest rate, negotiate a successful owner carryback, if necessary, or prepare to shop inland ... often FAR inland, depending on locale, and attempt to do same at a lower price point. Cash buyers will pay the prevailing prices within reason ... in consideration of the convenience of a cash transaction (if that is "customary" in a particular market area) or lose out to another cash buyer.

"Worker buyers" in coastal CA counties who need purchase-money mortgages absolutely WILL buy what they can qualify to buy and if their "expectations" don't match what is on offer to them, they will continue to rent or leave the area to shop elsewhere. It's as simple as that and this is as it should be and always has been, IMHO.

Some good stuff on how the Some good stuff on how the large investment funds are planning to take their profits while leaving the idiots to suffer the impending losses:

[You can be sure that the pension funds will inevitably be caught up in this one, too…and the public sector employees will be blamed for Wall Street’s mess, once again.]

The scale of the problem [think redemption and disposition time!]:

Understand that these investments will generally act like bonds relative to interest rates. As rates rise, the value of these securities will likely go down since rents (the ROI) are fairly fixed. I also seriously doubt that these funds have properly figured in the real costs of maintaining and managing these rentals over the years, so their assumed rates of return are probably unrealistically optimistic as this would increase the value of the securities that these fund managers and initial investors are trying to cash out of (totally IMHO).

—————

Private equity firm Blackstone Group borrowed $2 billion from banks to invest in single-family homes it intends to rent out. Someone thinks the housing rally will continue! The Wall Street Journal reports that “Blackstone’s agreement with Deutsche Bank, Bank of America, Credit Suisse, and other lenders more than tripled the size of its previous loan, to $2.08 billion from $600 million, a person familiar with the deal said. Deutsche, which had arranged Blackstone’s initial accord, will remain the lead bank on the bigger loan. Private-equity firms such as Colony Capital LLC and real-estate investment firm Waypoint Real Estate Group LLC have snapped up thousands of previously foreclosed homes in recent months to rent out as part of a strategy to take advantage of the recovery of the housing market.” It appears that leverage is alive and well. “Blackstone has said it is buying single-family homes at the rate of $100 million a week, a faster pace than any other buyer. The firm now owns around 20,000 homes, say people familiar with the matter. The firm expects to spend more than $4 billion on homes, and could seek additional loans related to fund these purchases, these people said.”

But back to your assertion But back to your assertion that people will lower their housing expectations in the face of higher interest rates, I would argue that this is absolutely incorrect. Any buyer with two brain cells would know that if their purchasing power is reduced by higher rates, then the purchasing power of those above and below them will be reduced just the same. Everybody will have the same housing expectations, but will reduce the amount they are willing/able to pay for a given house.

Housing prices are not static. They change based on conditions in the credit market (interest rates and credit availability, growth/shrinkage of the overall credit market, etc.) and job market. They are also greatly affected by things like family formation trends; investor appetite (absence or existence of better investments in other asset classes or other parts of the world); demographic and cultural shifts like women entering or leaving the workforce, or people being foreclosed on en masse which can lead to unusually high rental demand and low demand for owner-occupied housing (good for funds who plan to buy-to-rent, but for how long?), etc. Right now, all of these other variables are favorable for the housing market, but there are good reasons to believe that this is a temporary situation.

The importance of interest rates in this whole equation cannot be understated, BTW. For the past decade, except for a brief period of sanity in 2007, savers have been absolutely decimated by the Fed’s policies. I would argue that wage earners have also been negatively affected since their purchasing power has been reduced as asset prices are pushed up artificially by the low rates and increased use of leverage.

peterb

13 years ago

I seem to remember the I seem to remember the inventory for the City of SD was in the 3000 to 4000 range for most of 2003 to 2006. It’s getting a bit foggy, though.

bearishgurl

12 years ago

CAR, I would agree with you CAR, I would agree with you about buyer housing expectations not being lowered in inland CA counties and flyover states in the face of higher MIRs. But I would NOT agree with it within ~ten miles from the CA coast. This “immunity” is even more pronounced in particular exclusive enclaves and covenants, particularly in CA coastal counties as well as within ~5 miles of the CA coast.

IOW, if a buyer (ESP a buyer using a mortgage for the bulk of their PM) thinks they’re going to “steal” a residential property in CA’s best areas just because the prevailing MIR is now a few notches higher, they better think again. It’s not going to happen. It won’t happen because the vast majority of these properties are in the “best hands.” Plain and simple. Without wholesale repeal of entire sections of CA law, this will always be so.

I will check in a few hours and read your interesting articles about REIT leveraging.

Nobody is trying to “steal” Nobody is trying to “steal” anything. Prices are set by buyers, not sellers. Otherwise, we could all list our homes or cars for whatever pie-in-the-sky price we want and claim that our list price is the market price. It doesn’t happen that way, and it never has.

Coastal areas are a bit more resilient, in general, because there is more demand for housing along the coast with a more limited supply of housing, and higher-end buyers tend to be more resilient than lower-end buyers, but that doesn’t mean that housing prices along the coast are unaffected by interest rates or other market conditions. Back in the mid 90s, we were looking at houses in Malibu that had fallen in price by around 40% from their ~1989 peaks. Nothing is immune from economic shocks and changes in market conditions, not even housing in highly desirable coastal enclaves.

Again, rich people don’t get rich by overpaying for things. They aren’t stupid and they understand the correlation between interest rates and asset prices better than most. Additionally, these are the very people who will want to preserve cash when interest rates are high; they will not want to squander their hard-earned money on overpriced housing just because an ignorant seller believes his/her house is worth a million dollars when it’s really only worth $600,000.

Rich,

Would you happen to

Rich,

Would you happen to know how today’s inventory numbers compare to the inventory numbers during the spring of 2004? IIRC, that was the last low for inventory. It looks like we are at (or below) those levels now.

Just if you have the numbers at the ready, I don’t want to ask you to do any more work than you’re already doing on this.

Thank you so much for everything you do!

Hi CAR — Unfortunately I

Hi CAR — Unfortunately I don’t have inventory data that far back… that would indeed be very interesting to compare. Maybe one of the realtors out there has that data?

Rich

Funny, just Googled it and

Funny, just Googled it and found your article from 2006. 🙂

Many confused this temporary run on inventory with a longer-term structural housing shortage, but as the numbers above show, it was not. It was a short-term inventory drain caused by a temporary imbalance between buyers and sellers, which was in turn caused by a period of extreme homebuyer optimism, and it has already passed. The inventory of homes for sale, after reaching a low of around 2,000 in early 2004, is now back up to 15,000 and rising.

http://www.voiceofsandiego.org/housing/article_dd954903-0ff4-5172-b646-3d2d87d27812.html#user-comment-area

———-

I hope everyone understands how very quickly market conditions like this can change, as evidenced by your last sentence, above.

Thanks, Rich…then and now! 🙂

Haha, good find!

That

Haha, good find!

That prompted me to poke around more but I can’t seem to find any older inventory data. It looks like I had it at one point, though… here is a graph from a 2005-era post that goes back to mid-2004, after inventory had risen from the lows quite a bit already:

Interestingly we are right about where we were in summer 2004!

Gasp! I just realized that’s

Gasp! I just realized that’s almost 9 years ago!!! We just keep on getting older, don’t we? 🙁

According to sdlookup San

According to sdlookup San Diego city is just under 2,000 active listings currently and San Diego county is around 7,000. Just wondering are all graphs San Diego county or is there a mix.

moneymaker wrote:According to

[quote=moneymaker]According to sdlookup San Diego city is just under 2,000 active listings currently and San Diego county is around 7,000. Just wondering are all graphs San Diego county or is there a mix.[/quote]

SD County. Numbers are probably different because mine were from mid-Feb.

CA renter wrote:Funny, just

[quote=CA renter]Funny, just Googled it and found your article from 2006. 🙂

Many confused this temporary run on inventory with a longer-term structural housing shortage, but as the numbers above show, it was not. It was a short-term inventory drain caused by a temporary imbalance between buyers and sellers, which was in turn caused by a period of extreme homebuyer optimism, and it has already passed. The inventory of homes for sale, after reaching a low of around 2,000 in early 2004, is now back up to 15,000 and rising.

http://www.voiceofsandiego.org/housing/article_dd954903-0ff4-5172-b646-3d2d87d27812.html#user-comment-area

———-

I hope everyone understands how very quickly market conditions like this can change, as evidenced by your last sentence, above.

Thanks, Rich…then and now! :)[/quote]

That article may very well be describing what’s going on currently with the housing market. IOW, should we expect another downturn in the housing market in the next couple years?

Not sure about when, but I’m

Not sure about when, but I’m very convinced that we’ll be seeing another downturn — the completion of the recent downturn that was artificially stopped in its tracks via various govt and Fed manipulations.

Even with today’s low interest rates, people are still struggling with their housing payments because the price of everything else has been pushed up along with housing, thanks to the Fed’s irresponsible policies. 🙁

These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.

CA renter wrote:…These

[quote=CA renter]…These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.[/quote]

I would suspect that the large REITS and even smaller investor groups will continue to hold these properties 5+ years from now if they don’t think they can get the prices they want due to higher prevailing interest rates. They really don’t have to sell if they don’t wish to as they don’t have mortgages.

However, in the past, rising interest rates never affected sales volume, unless the 30-yr fixed MIR was over 10%. And residential properties still sold to owner occupants even then, mostly with seller participation.

The only effect a higher MIR has on a homebuyer is to drop them down to a lower tier of home to buy. It does NOT preclude them from buying.

bearishgurl wrote:CA renter

[quote=bearishgurl][quote=CA renter]…These large investment groups that have been such a force in today’s housing market have a 5-7 year disposition plan. What then? What if interest rates are higher at that point? IMHO, people are making foolish decisions, once again, because of the Fed.[/quote]

I would suspect that the large REITS and even smaller investor groups will continue to hold these properties 5+ years from now if they don’t think they can get the prices they want due to higher prevailing interest rates. They really don’t have to sell if they don’t wish to as they don’t have mortgages.

However, in the past, rising interest rates never affected sales volume, unless the 30-yr fixed MIR was over 10%. And residential properties still sold to owner occupants even then, mostly with seller participation.

The only effect a higher MIR has on a homebuyer is to drop them down to a lower tier of home to buy. It does NOT preclude them from buying.[/quote]

These investment groups have investors who might want/need to cash out at 5-7 years. Not only that, but many investment groups are mortgaging the properties after acquiring them for cash, so they do occasionally have mortgages. The mortgages aren’t the problem, but redemptions certainly could be, and if interest rates are higher at that time, then the value of their RE investments will be lower. If the fund managers levered up the funds, there could be some serious problems.

Higher interest rates absolutely affect the prices of assets bought with credit. Under no circumstances will higher rates force people to buy a lower tier home because interest rates affect buyers all across the spectrum. People with certain education levels, and in certain professions, etc. expect to live in an area with their peers. The housing expectations of buyers will not change; their ability/willingness to pay a certain price for a given house is what will change. And cash buyers are every bit as sensitive to interest rates as mortgaged buyers because their money can earn decent returns in a higher interest rate environment, which will induce them to either use a mortgage or keep more cash in order to make more money on investments. Cash is dear when interest rates are high. Rich people don’t get rich by overpaying for things.

CAR, I’m not so sure these

CAR, I’m not so sure these large REITs have any intentions of leveraging their massive (mainly distressed SFR) inventory they acquired within the last year or so. There was plenty of investor money to buy it with and plenty more coming in as being a “flipper” or “landlord” is not for everyone. As long as the REIT’s are paying their investors good to great dividends, why would they want to redeem and invest elsewhere … even if the CD/MM/bond interest rates go up?

The vast majority of properties these REITs bought in bulk were purchased at prices well under market (even in CA) and some were bought at less than land value. Certainly, they will make very profitable rental investments if they are not too encumbered with HOA/MR.

But mainly I disagree with this portion of your statement:

“Under no circumstances will higher rates force people to buy a lower tier home because interest rates affect buyers all across the spectrum. People with certain education levels, and in certain professions, etc. expect to live in an area with their peers. The housing expectations of buyers will not change; their ability/willingness to pay a certain price for a given house is what will change.”

Historically, when MIR’s were 7-12%, prospective owner-occupants and investors still bought residential RE. They bought what they could qualify for if taking out a purchase-money mortgage. “Education level” and “profession” had nothing to do with it. Assets and/or W-2/self-employment income had everything to do with it.

Those many cities in CA’s Silicon Valley (San Mateo and Santa Clara Counties, for example) are a case in point. Excepting one small area, “newer” (last 15 yrs) SFR construction there does not exist for 65+ miles, north to south, inclusive of SF and the majority of the housing stock is over 50 yrs of age. In the most expensive areas, most of the stock is 50-90 yrs old. A buyer using a $250K+ downpayment and taking out a $750K jumbo mortgage could very well be buying a <1500 sf charmer circa 1953 on a 6500K lot. No matter the "profession" or "educational level" of this SV worker/homebuyer, they have three options there: (1) buy a locally listed resale; (2) continue to rent locally or elsewhere (and commute to/from work every day); or (3) buy elsewhere and commute to/from work every day.

It doesn't matter what the prevailing MIRs are. If these "professional" workers don't like what is on offer there or feel they won't be living with their "peers" in those areas (due to age of stock and its longtime existing homeowners) or they don't like the "tier" they perceive these homes to be in (independent of actual cost), they will leave the area to shop elsewhere. These properties will sell regardless.

You can't choose your neighbors ... anywhere, most especially not in CA's finest coastal enclaves. A buyer/owner occupant gets what they get when they close escrow ... and those new neighbors may or may not be what they consider to be "representative of their peers."

In all RE climates, CA homebuyers must pay the prevailing interest rate, negotiate a successful owner carryback, if necessary, or prepare to shop inland ... often FAR inland, depending on locale, and attempt to do same at a lower price point. Cash buyers will pay the prevailing prices within reason ... in consideration of the convenience of a cash transaction (if that is "customary" in a particular market area) or lose out to another cash buyer.

"Worker buyers" in coastal CA counties who need purchase-money mortgages absolutely WILL buy what they can qualify to buy and if their "expectations" don't match what is on offer to them, they will continue to rent or leave the area to shop elsewhere. It's as simple as that and this is as it should be and always has been, IMHO.

Some good stuff on how the

Some good stuff on how the large investment funds are planning to take their profits while leaving the idiots to suffer the impending losses:

http://news.firedoglake.com/2012/08/26/the-worst-idea-in-the-world-securitizing-rental-revenue/

[You can be sure that the pension funds will inevitably be caught up in this one, too…and the public sector employees will be blamed for Wall Street’s mess, once again.]

The scale of the problem [think redemption and disposition time!]:

http://news.firedoglake.com/2012/11/15/hedge-fund-blackstone-buying-100-million-in-foreclosed-homes-every-week/

Understand that these investments will generally act like bonds relative to interest rates. As rates rise, the value of these securities will likely go down since rents (the ROI) are fairly fixed. I also seriously doubt that these funds have properly figured in the real costs of maintaining and managing these rentals over the years, so their assumed rates of return are probably unrealistically optimistic as this would increase the value of the securities that these fund managers and initial investors are trying to cash out of (totally IMHO).

—————

Private equity firm Blackstone Group borrowed $2 billion from banks to invest in single-family homes it intends to rent out. Someone thinks the housing rally will continue! The Wall Street Journal reports that “Blackstone’s agreement with Deutsche Bank, Bank of America, Credit Suisse, and other lenders more than tripled the size of its previous loan, to $2.08 billion from $600 million, a person familiar with the deal said. Deutsche, which had arranged Blackstone’s initial accord, will remain the lead bank on the bigger loan. Private-equity firms such as Colony Capital LLC and real-estate investment firm Waypoint Real Estate Group LLC have snapped up thousands of previously foreclosed homes in recent months to rent out as part of a strategy to take advantage of the recovery of the housing market.” It appears that leverage is alive and well. “Blackstone has said it is buying single-family homes at the rate of $100 million a week, a faster pace than any other buyer. The firm now owns around 20,000 homes, say people familiar with the matter. The firm expects to spend more than $4 billion on homes, and could seek additional loans related to fund these purchases, these people said.”

http://www.mortgagenewsdaily.com/channels/pipelinepress/03142013-blackstone-compliance-mba.aspx

Sometimes, “all-cash” is not really all cash.

—————-

A possible canary in the coal mine…are PE investors getting wise? [Note: this includes commercial, too.]

Private-Equity Property Fundraising at Lowest Since 2003

http://www.preqin.com/item/private-equity-property-fundraising-at-lowest-since-2003/102/6449

But back to your assertion

But back to your assertion that people will lower their housing expectations in the face of higher interest rates, I would argue that this is absolutely incorrect. Any buyer with two brain cells would know that if their purchasing power is reduced by higher rates, then the purchasing power of those above and below them will be reduced just the same. Everybody will have the same housing expectations, but will reduce the amount they are willing/able to pay for a given house.

Housing prices are not static. They change based on conditions in the credit market (interest rates and credit availability, growth/shrinkage of the overall credit market, etc.) and job market. They are also greatly affected by things like family formation trends; investor appetite (absence or existence of better investments in other asset classes or other parts of the world); demographic and cultural shifts like women entering or leaving the workforce, or people being foreclosed on en masse which can lead to unusually high rental demand and low demand for owner-occupied housing (good for funds who plan to buy-to-rent, but for how long?), etc. Right now, all of these other variables are favorable for the housing market, but there are good reasons to believe that this is a temporary situation.

The importance of interest rates in this whole equation cannot be understated, BTW. For the past decade, except for a brief period of sanity in 2007, savers have been absolutely decimated by the Fed’s policies. I would argue that wage earners have also been negatively affected since their purchasing power has been reduced as asset prices are pushed up artificially by the low rates and increased use of leverage.

I seem to remember the

I seem to remember the inventory for the City of SD was in the 3000 to 4000 range for most of 2003 to 2006. It’s getting a bit foggy, though.

CAR, I would agree with you

CAR, I would agree with you about buyer housing expectations not being lowered in inland CA counties and flyover states in the face of higher MIRs. But I would NOT agree with it within ~ten miles from the CA coast. This “immunity” is even more pronounced in particular exclusive enclaves and covenants, particularly in CA coastal counties as well as within ~5 miles of the CA coast.

IOW, if a buyer (ESP a buyer using a mortgage for the bulk of their PM) thinks they’re going to “steal” a residential property in CA’s best areas just because the prevailing MIR is now a few notches higher, they better think again. It’s not going to happen. It won’t happen because the vast majority of these properties are in the “best hands.” Plain and simple. Without wholesale repeal of entire sections of CA law, this will always be so.

I will check in a few hours and read your interesting articles about REIT leveraging.

Nobody is trying to “steal”

Nobody is trying to “steal” anything. Prices are set by buyers, not sellers. Otherwise, we could all list our homes or cars for whatever pie-in-the-sky price we want and claim that our list price is the market price. It doesn’t happen that way, and it never has.

Coastal areas are a bit more resilient, in general, because there is more demand for housing along the coast with a more limited supply of housing, and higher-end buyers tend to be more resilient than lower-end buyers, but that doesn’t mean that housing prices along the coast are unaffected by interest rates or other market conditions. Back in the mid 90s, we were looking at houses in Malibu that had fallen in price by around 40% from their ~1989 peaks. Nothing is immune from economic shocks and changes in market conditions, not even housing in highly desirable coastal enclaves.

Again, rich people don’t get rich by overpaying for things. They aren’t stupid and they understand the correlation between interest rates and asset prices better than most. Additionally, these are the very people who will want to preserve cash when interest rates are high; they will not want to squander their hard-earned money on overpriced housing just because an ignorant seller believes his/her house is worth a million dollars when it’s really only worth $600,000.