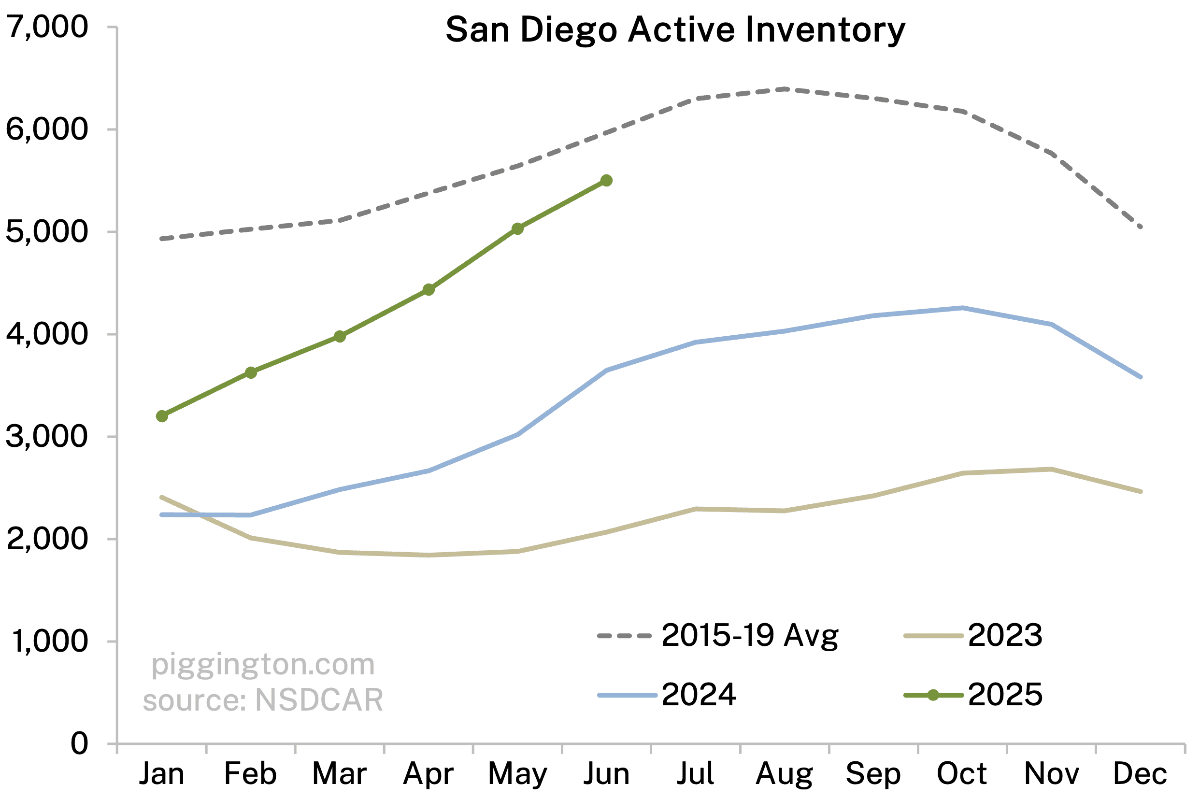

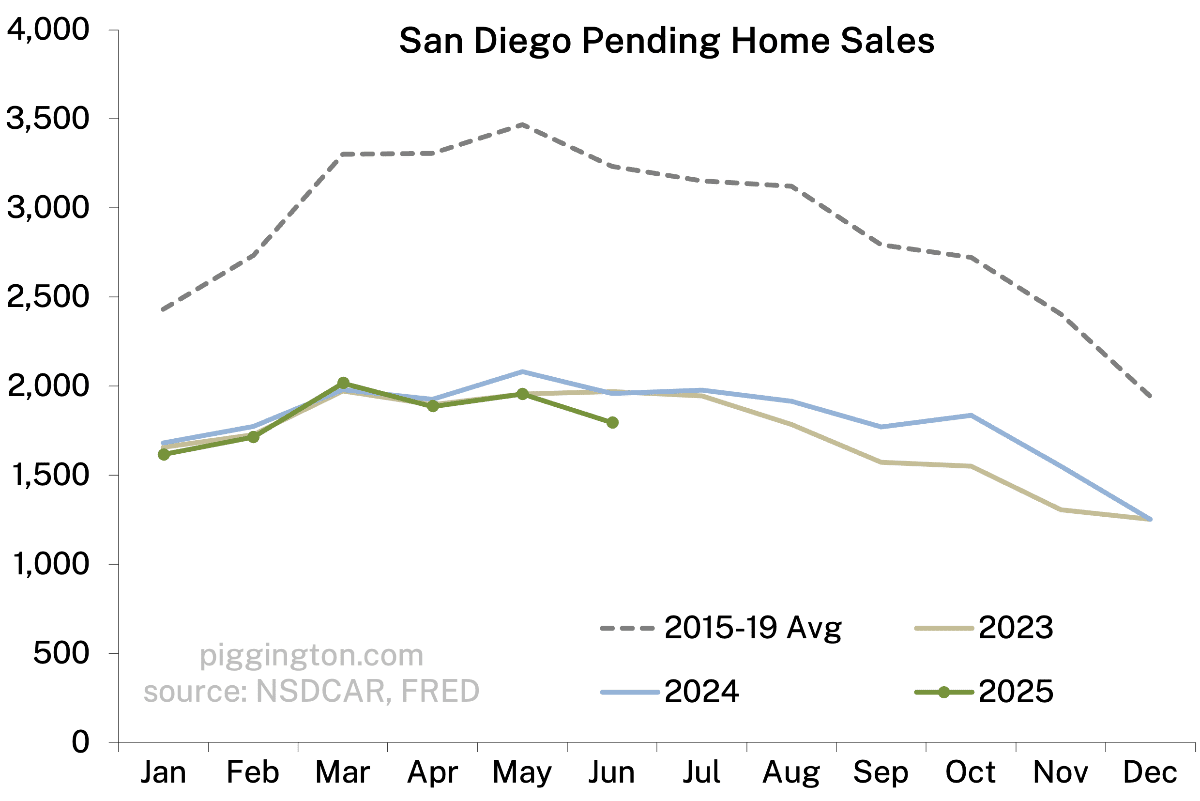

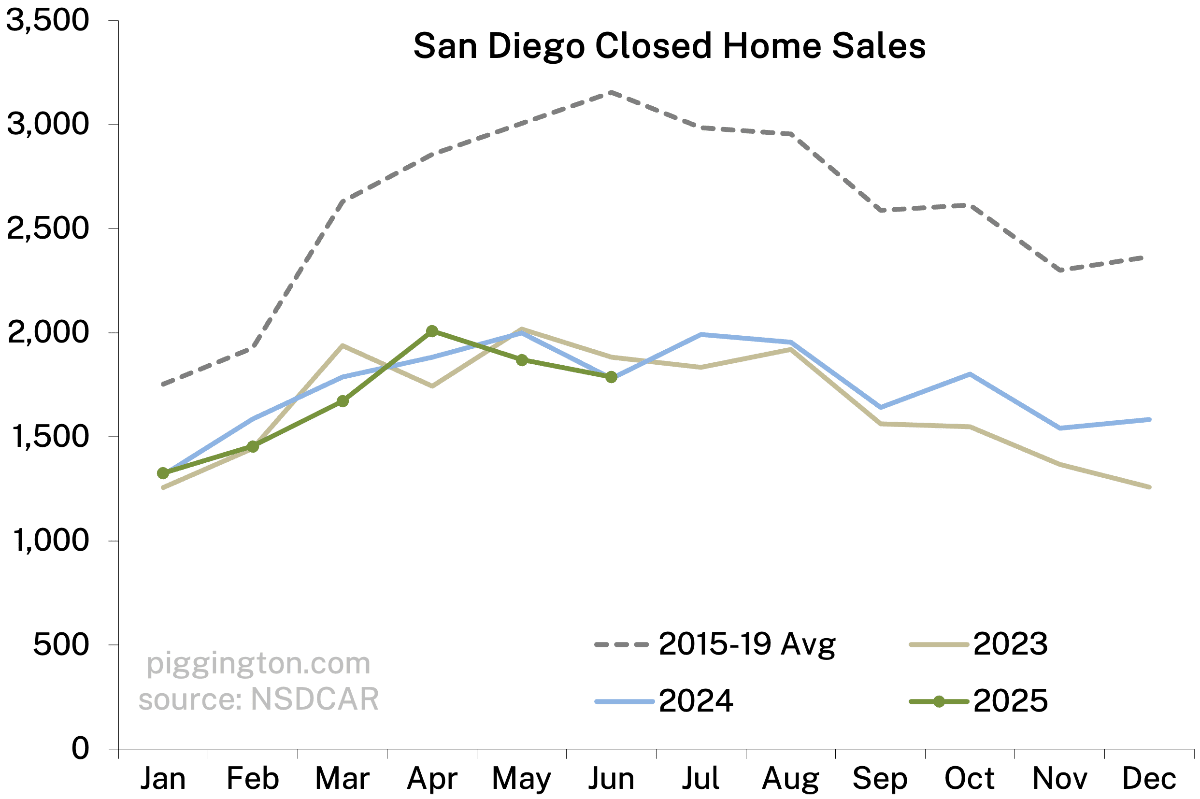

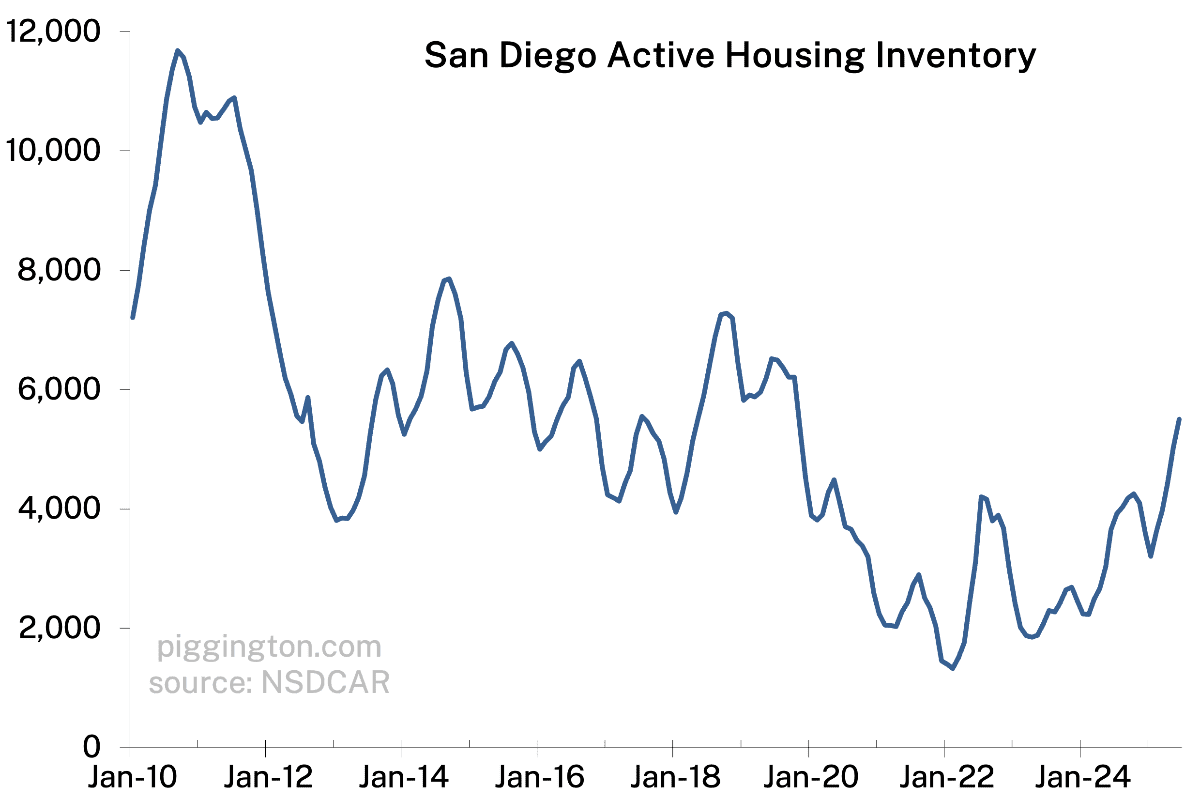

Inventory rose further last month, as sales stayed in the doldrums:

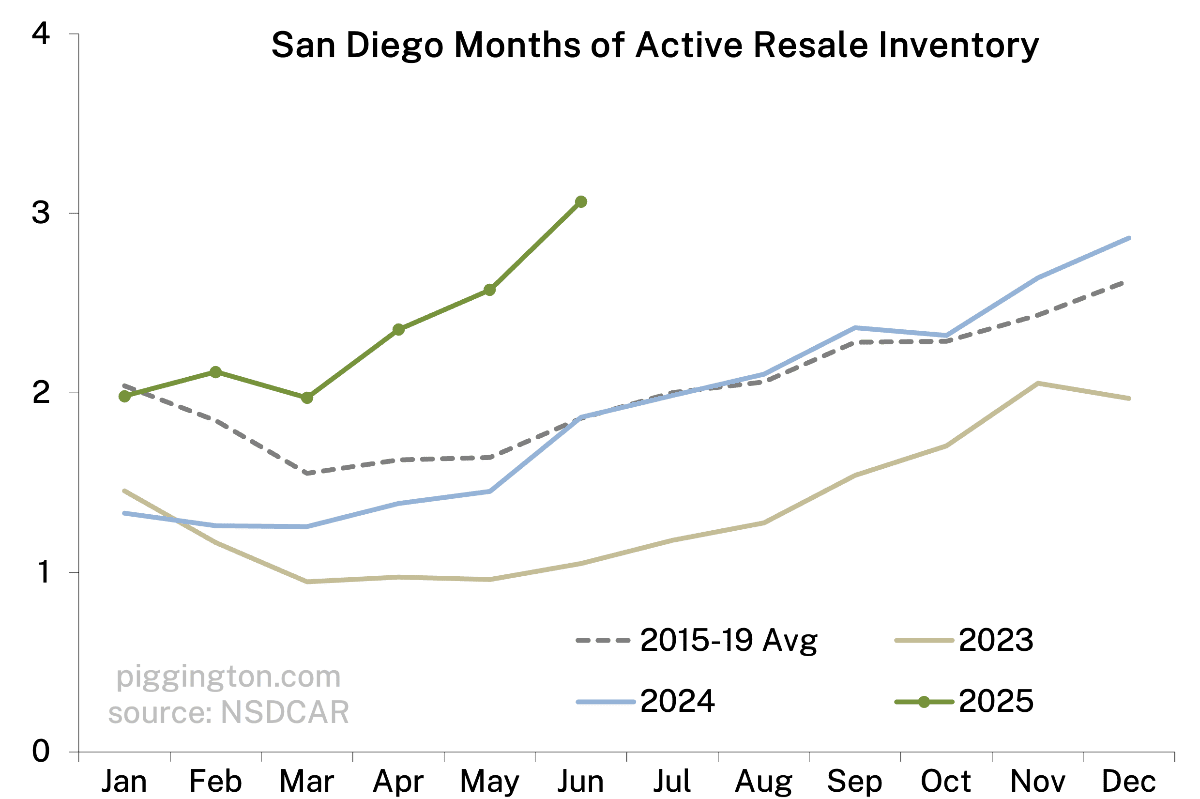

The result was a months of inventory level that far exceeded the pre-pandemic average for this time of year:

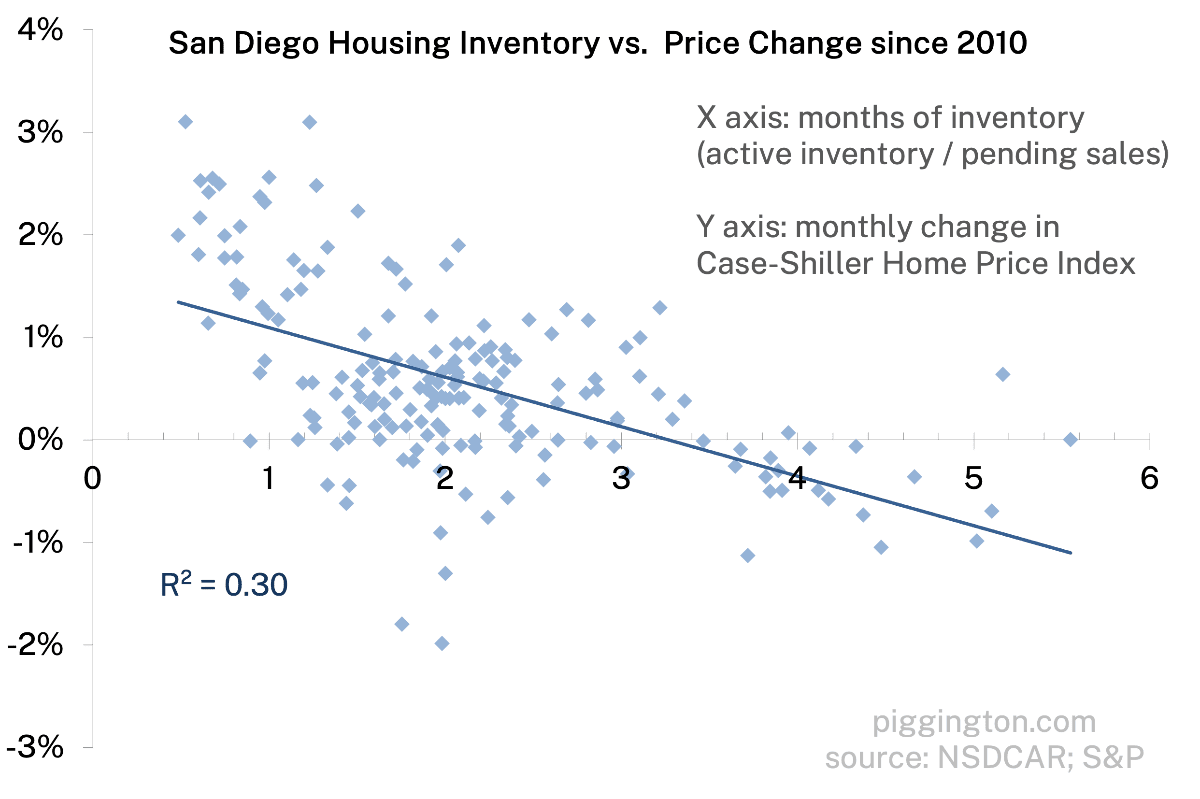

With that, we’ve crept up alongside inventory level at which price declines become a lot more likely:

There is a tendency for months of inventory to rise in the latter half of the year. A typical seasonal rise from this point would take us well into the likely price decline zone.

But it’s possible that we won’t get the typical seasonal increase. For instance, the tariff panic might have prematurely increased inventory (putting people off buying and/or inducing some to list their homes). Also, I read that some would-be sellers are getting frustrated and just yanking their homes off the market. That obviously wasn’t happening on net as of last month, but it seems plausible that it could.

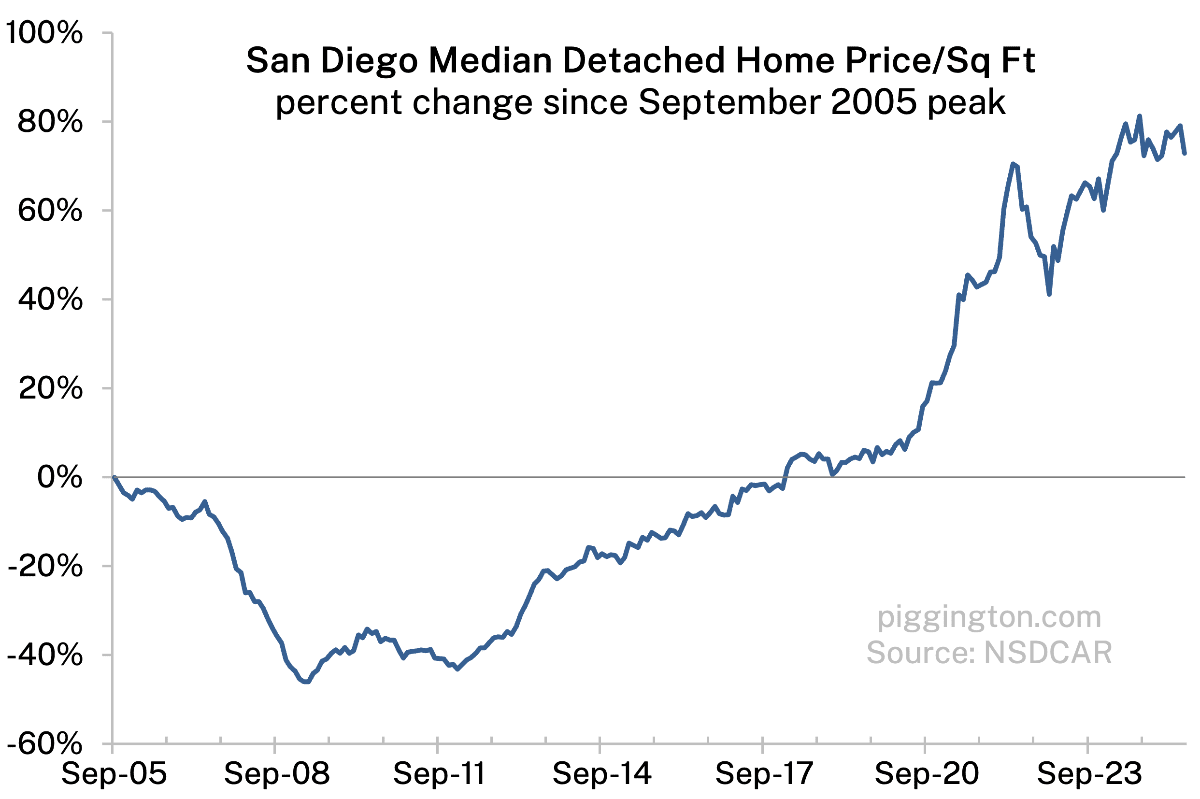

Prices did decline last month, with the median price per square foot down 3.4%. This is a noisy figure so don’t read too much into it — here’s a graph of the price/square foot, showing that it can move around quite a bit from month to month:

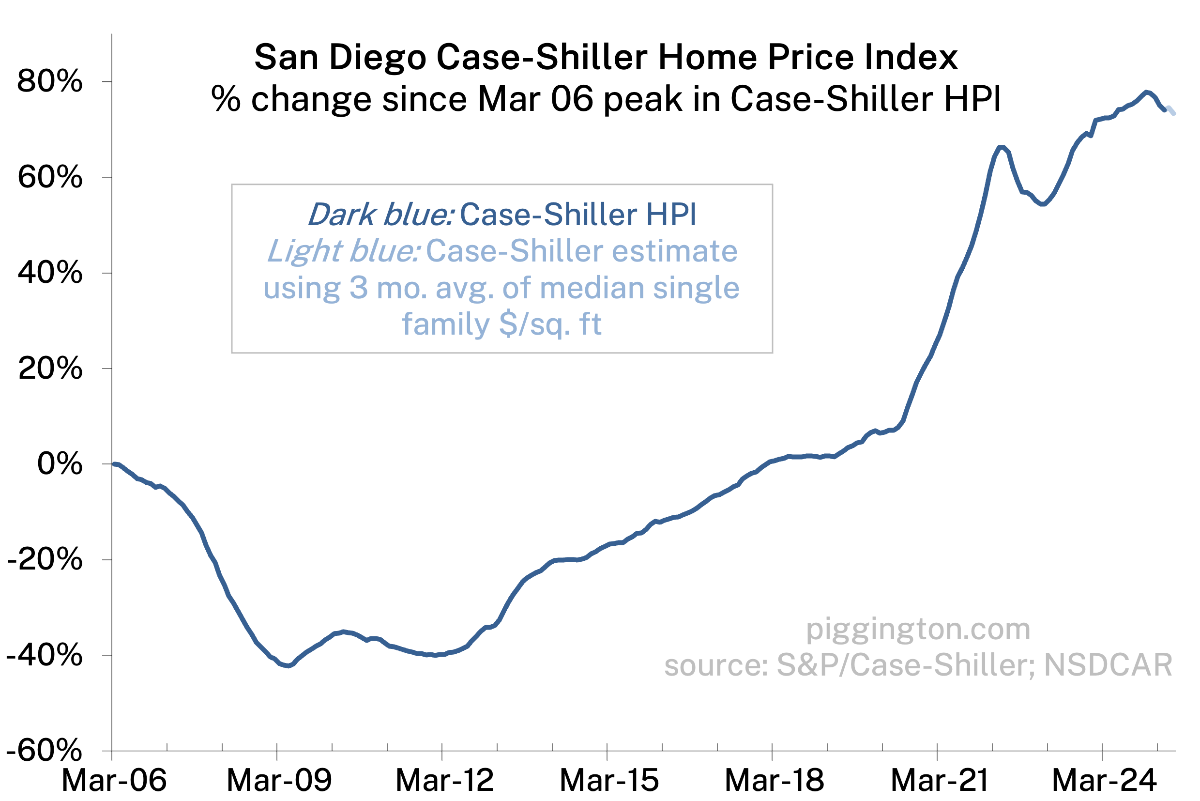

Nevertheless this does suggest a continuation of the price weakness that had already appeared in the much more accurate Case-Shiller price index:

More charts below, and I’ll follow up with a valuation update soon.

purgatory continues… https://www.housingwire.com/podcast/decoding-the-2025-housing-market-with-bill-mcbride/