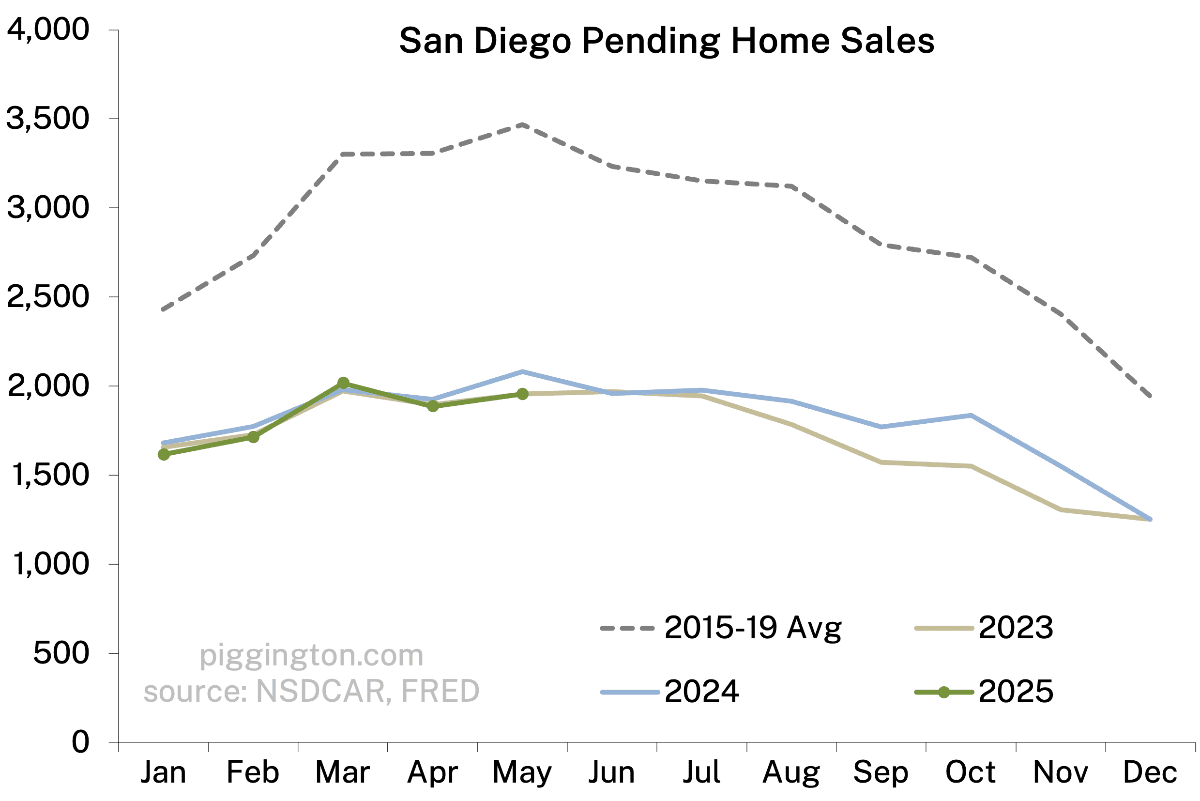

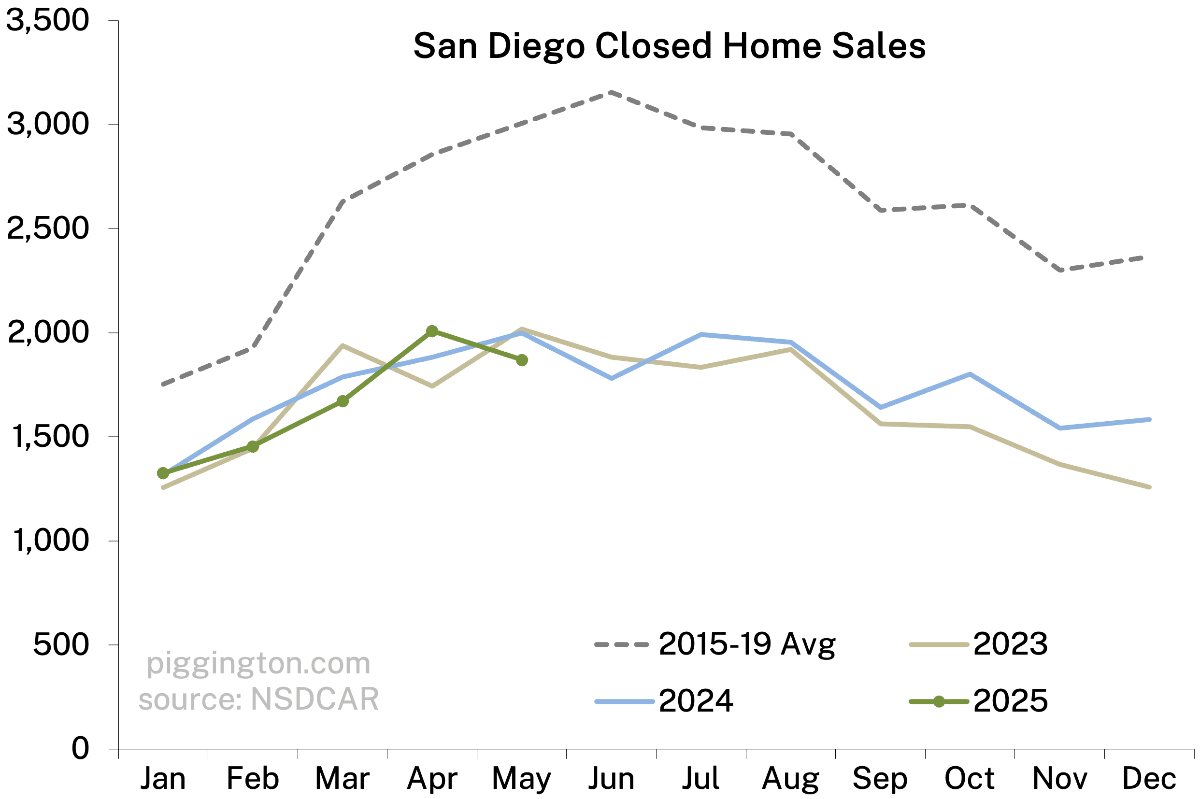

Sales activity remained at typical post-2022 depressed levels…

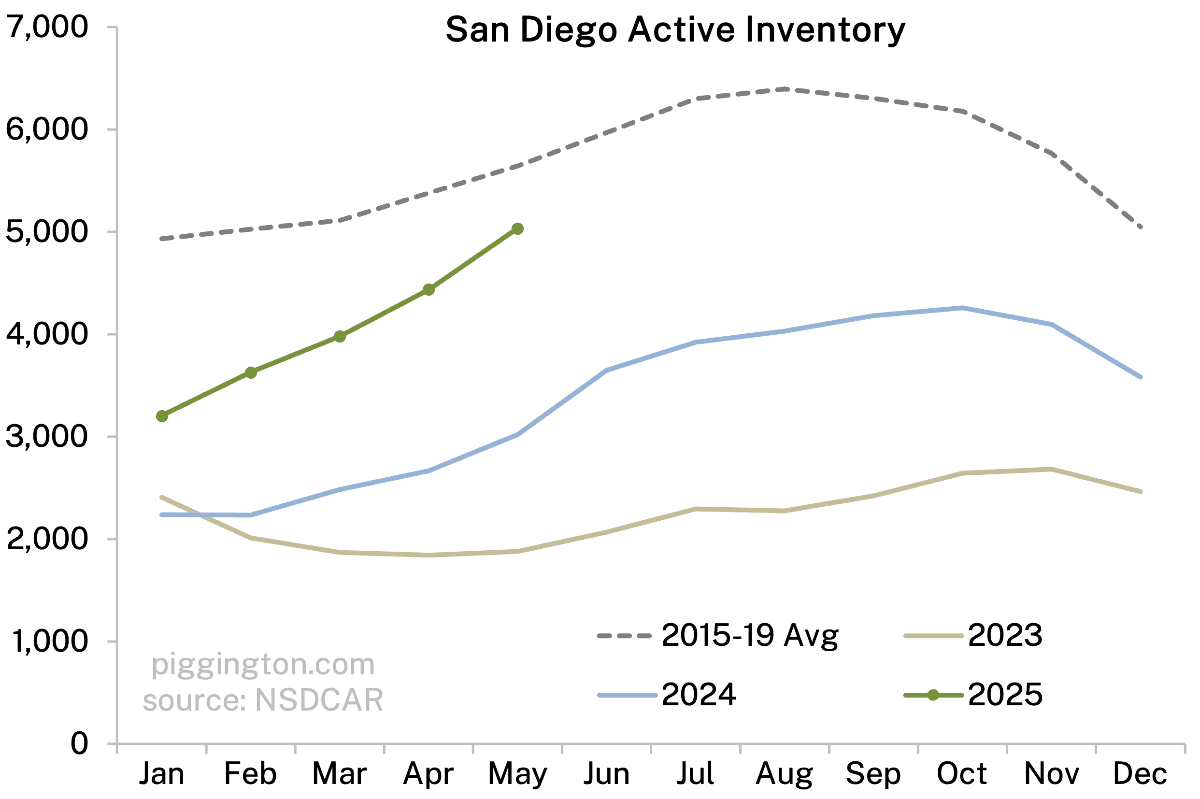

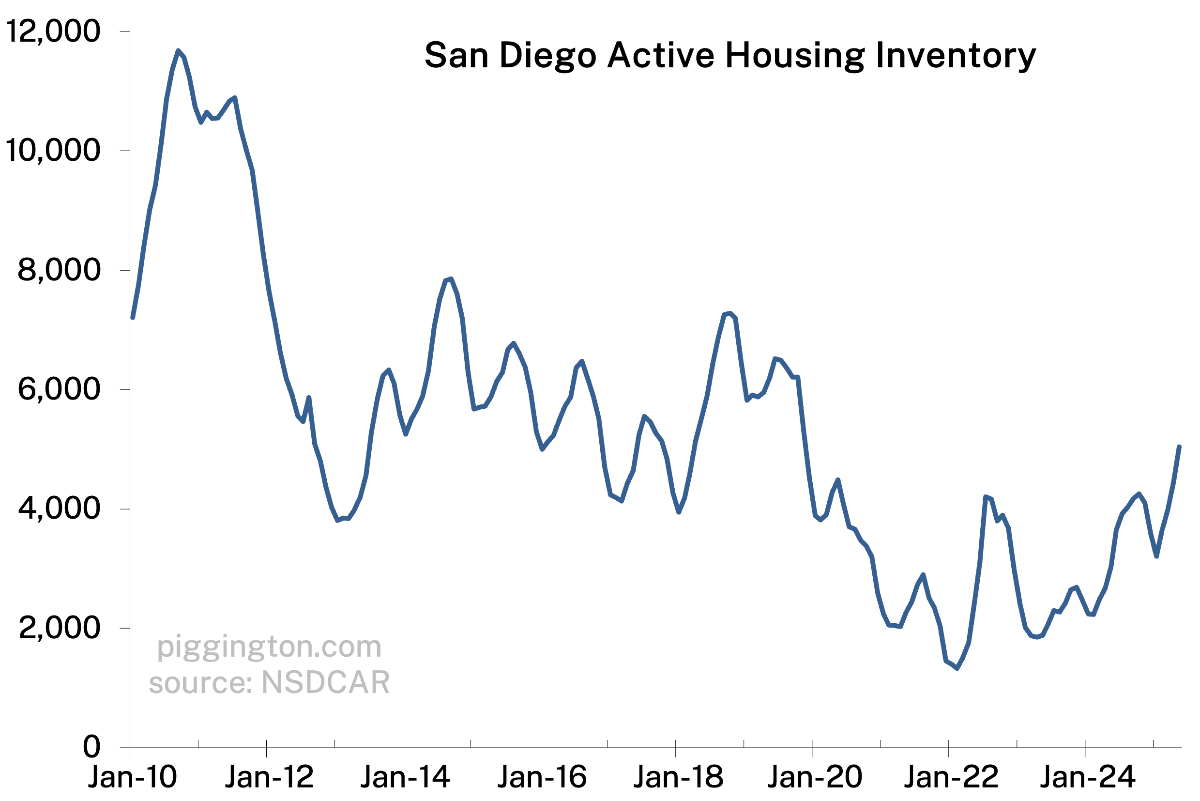

But inventory keeps rising and is not too far now from pre-pandemic norms:

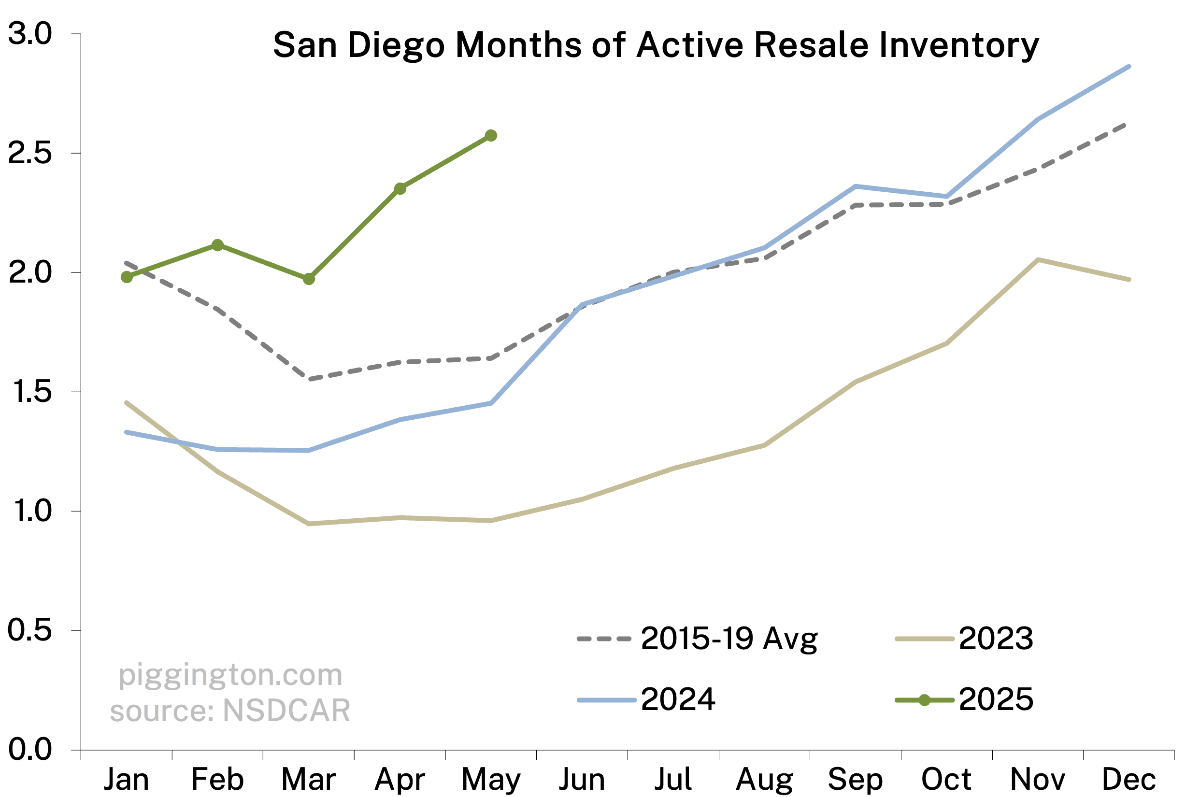

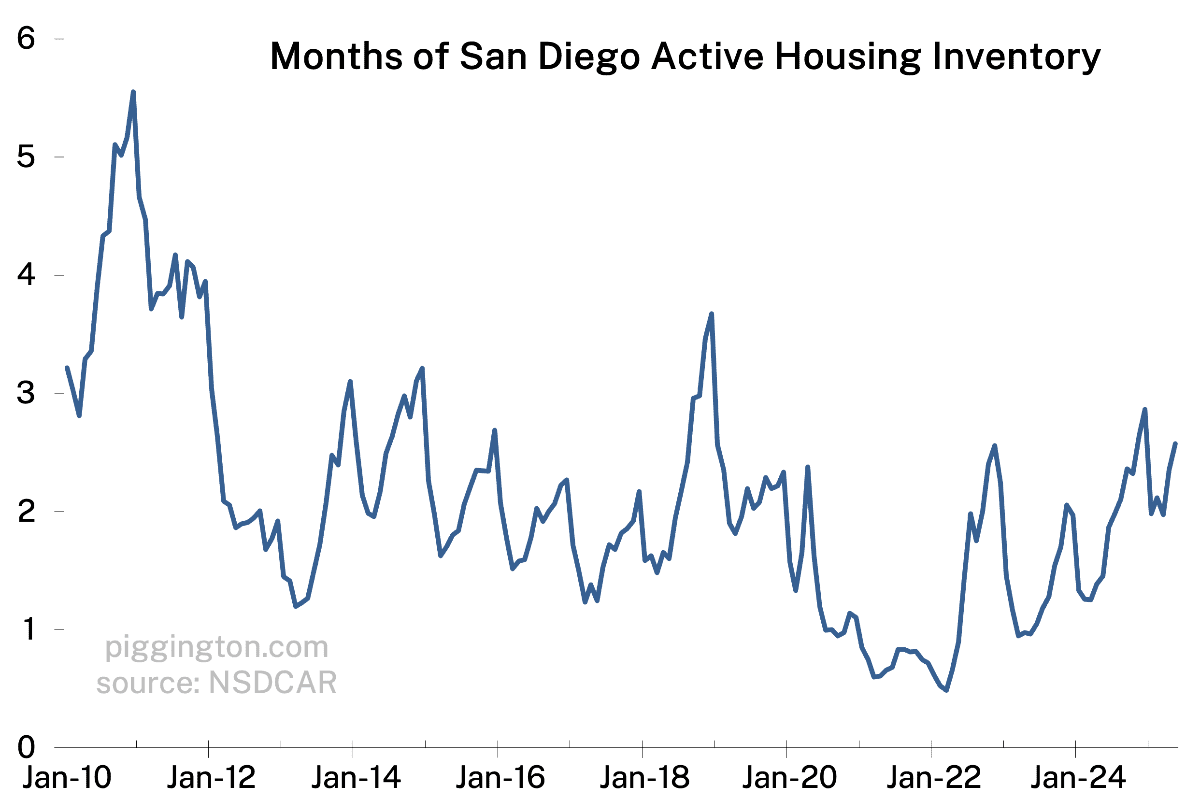

As a result, the months of inventory measure has surpassed typical May levels by a pretty wide margin:

Will months of inventory level off here, or follow the typical seasonal pattern and increase for the remainder of the year? If it’s the latter, I think we may be looking at price declines.

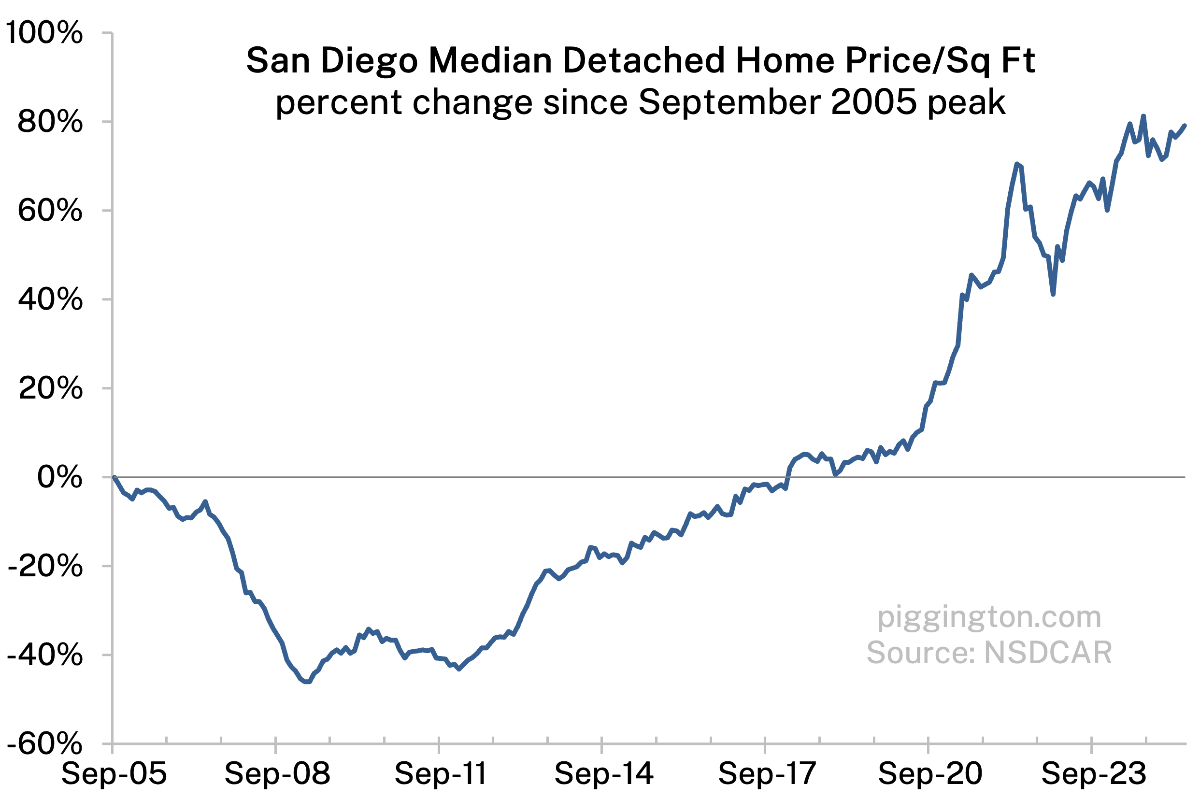

But for now, prices have hung in there:

Let’s keep an eye on that inventory in the months go come. Meanwhile, more graphs below…

I can rent this house for $6,400

https://www.zillow.com/homedetails/4861-Carriage-Run-Dr-San-Diego-CA-92130/79571258_zpid/

I can buy this house for 2,200,000. Probably about $14,500 (PITI) with 20% down.

https://www.redfin.com/CA/San-Diego/4849-Carriage-Run-Dr-92130/home/12155028

Seems very like 2005/2006 to me. I struggle to think that buying makes any sort of financial sense? Help me out Rich.

Maybe rents rise to match purchase price? With biotech/tech/universities all getting slammed at the moment i wonder who can afford much more.

Still interest rates might come down a bit. At 5% the mortgage PITI is ‘only’ $12k.

try this: hey chatGPT, why have single family homes become a wealth asset and what is the typical monthly payment premium versus equivalent rent in high-demand markets?

For giggles I actually entered that prompt. The answer was not good imo, but it’s what I would have expected as it seems to be the conventional wisdom. Which is: enumerate why housing has been a good investments, and project that forward, without accounting for the windfall valuation increase that led us here.

PS I am working on an article addressing this topic, but it’s been taking me forever because I have a lot to say and it’s hard to strike the balance between what I want to say, and it not being a wall of text. Hopefully soon!

PPS Since my article touches on conventional wisdom (as I perceive it), it’s a good idea to ask these questions of an LLM. But I hadn’t thought to do that, so thanks for the idea!

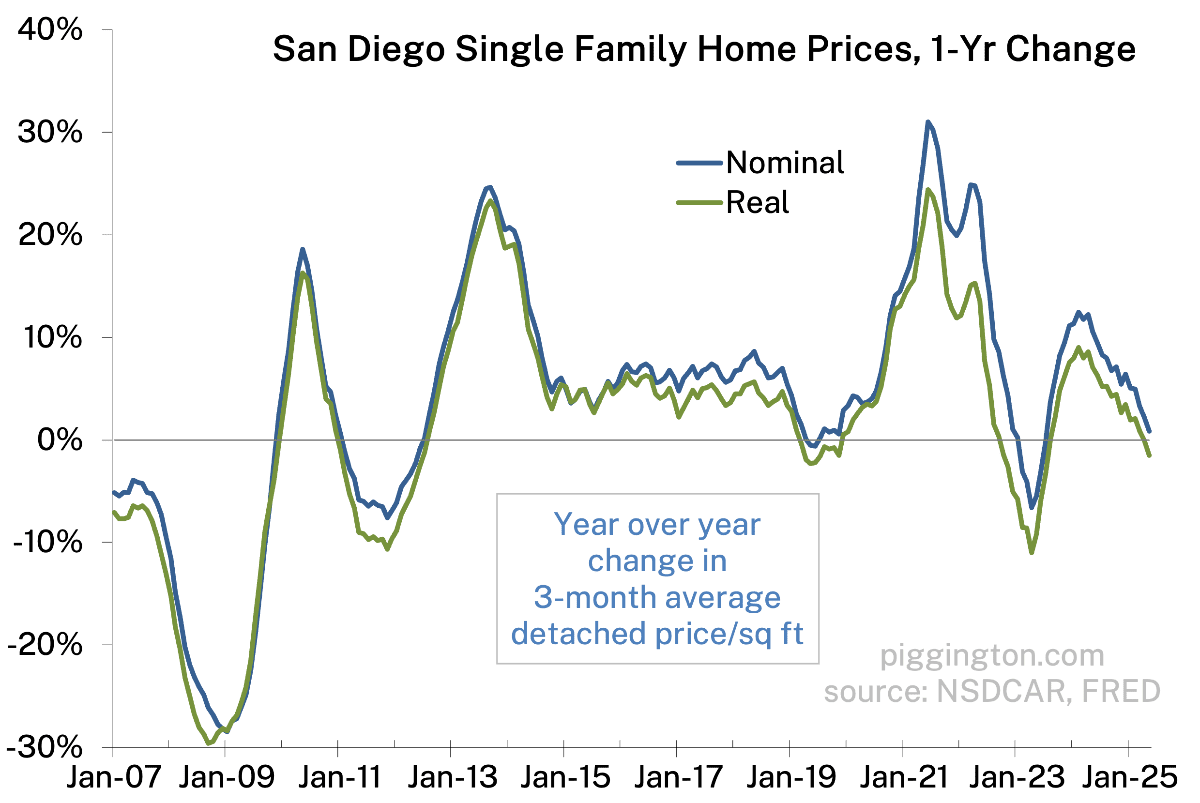

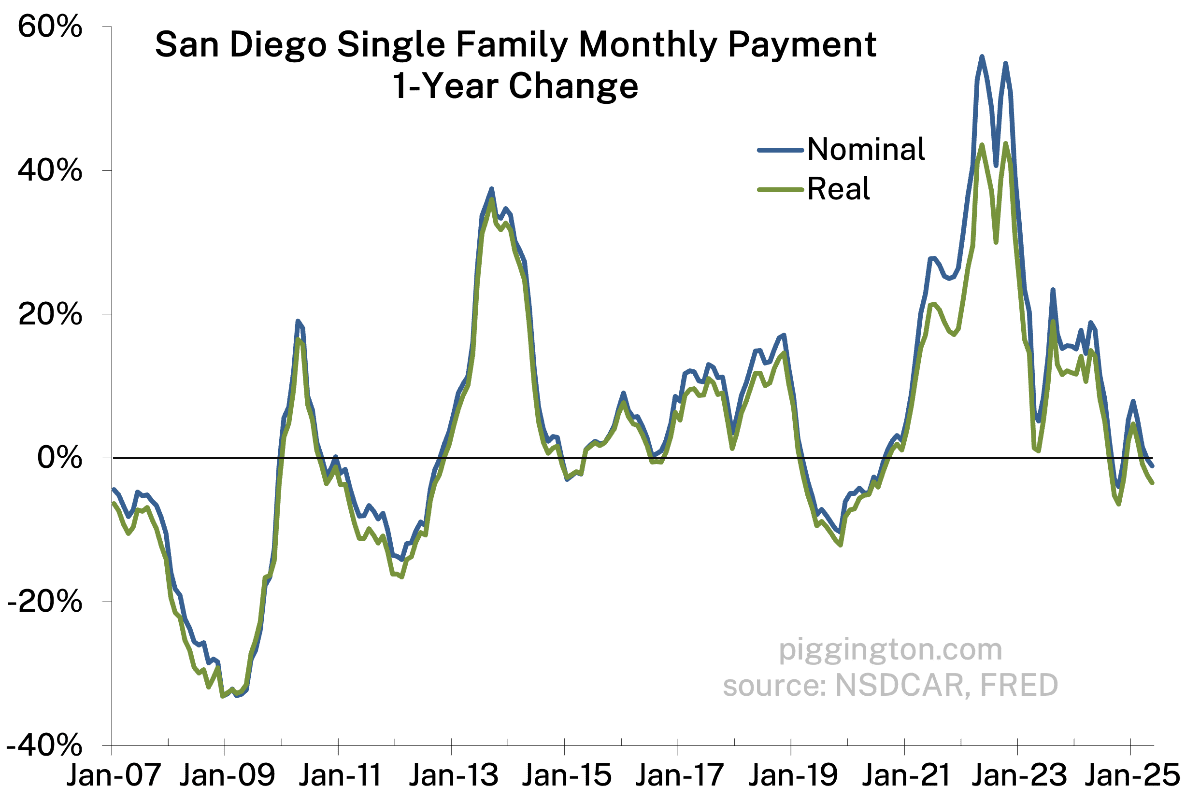

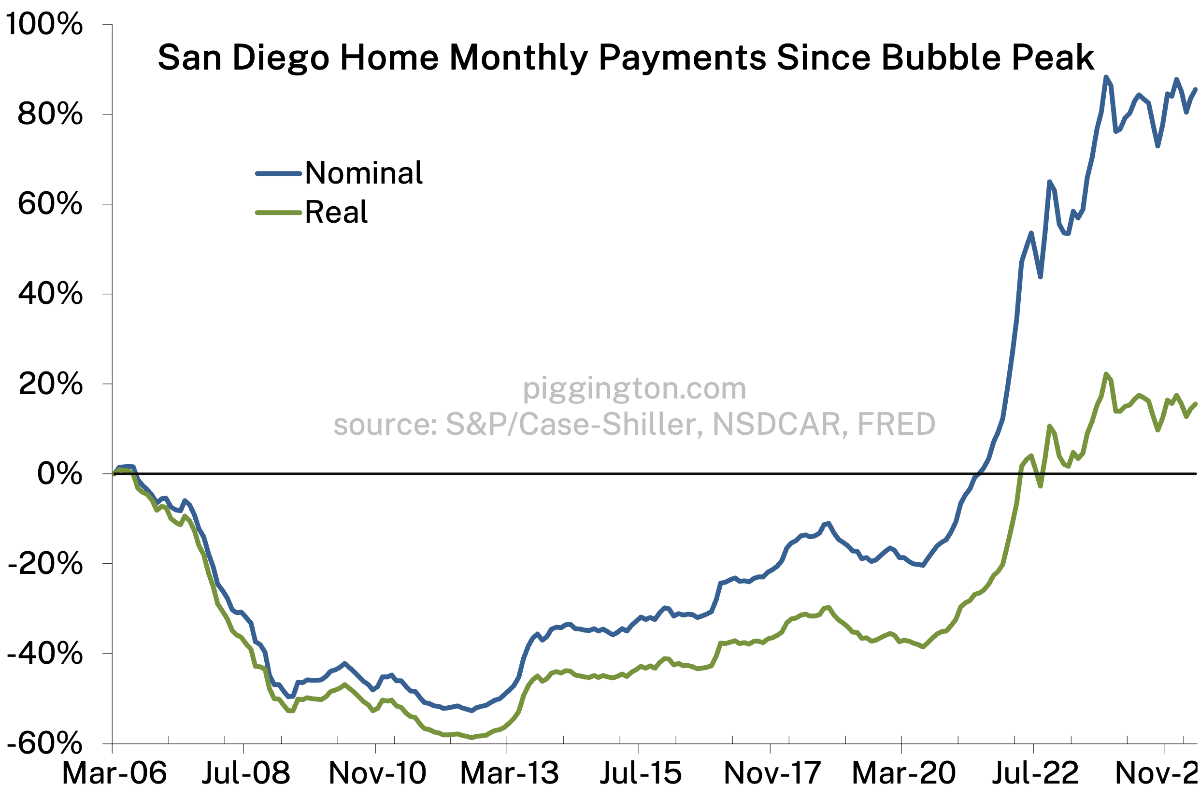

I agree this feels pretty unsustainable. The specific case you described can more broadly be seen here which shows that real monthly payments are higher than they were in the bubble.

I don’t really think it’s predictable how it will play out as it’s path dependent on, eg, whether/when a recession happens and how bad it is. I do think rents catching up will be a big part of it; there may also be some declines but that’s the part that’s hard to predict. I don’t expect this relative pricing to hold up though, one way or the other.

Thanks, Rich – interesting times for sure. People compare this to how it felt in 2005-ish but what is missing here is the 1-2 punch. IMO this spells out slight price declines over the foreseeable future.

I think monthly payment vs. rental value is an important metric, however anecdotally I’ve seen a lot of people “moving up” in terms of selling their condos/starter homes to move into larger SFH, and rolling that large equity into the newer home to reduce monthly payment. Is data there to show what people’s actual monthly payments are compared to rent?

Just to clarify, I’m not suggesting this is like 2005. Yes, homes are expensive – by some measures as expensive as they were back then. But that was 20 years ago and some of that valuation increase may be warranted (eg Covid, imo, likely caused a permanent increase in housing valuations). Also — that was all speculative euphoria, crazy borrowing, etc… none of that is going on here.

I don’t think I really follow on your second paragraph. The housing ladder has always been a thing. Perhaps now, the rungs are steeper (to stretch that metaphor) due to the pandemic appreciation. But even then it shouldn’t matter much… making a big payment entails opportunity cost for the money you are putting down, so there’s a “cost” to buying an expensive house whether it shows up as mortgage payment, or forfeiting the income you could have made on the down payment. And anyway the ladder only works if first time buyings can get on the bottom rung.

I do think the phenomenom you describe could smooth things out, ie extend the amount of time it takes to get back towards normal. But I don’t see changeable the level of valuation that is sustainable.

Thanks. It has been a while since i have been renting. I do not know the demand for rentals at the moment.

I am curious if you think there is any chance of a crash? Everything feels unsustainable but San Diego is a popular place. And there are no toxic mortgages this time to force people to sell?

I recall reading pacificbeachbubble back when i was renting.

Found it on wayback and fascinating to reread.

https://web.archive.org/web/20070707234137/http://pacificbeachbubble.blogspot.com/

He says:

He was was thinking 2004 boom was toxic mortgages, but i can’t put my fingers on what has caused this recent boom? Low interest rates? higher wages? inflation? private companies buying SFH?

I do think this statement is true: “property can’t go up forever because eventually no-one would be able to afford anything”

Not sure if we are on this timeline now (I do recall Florida was first to decline in 2004 and it is in severe decline now).

Hard to envision a 2000s style crash happening, imo. It would take a bad downturn, and even then we don’t have the bad debts that led to so many forced liquidations. I do think price declines are possibly in the cards (and real price declines likely) but a “crash”… hard to see it without some serious exogenous nastiness.

I will say that even tho these current loans aren’t necessarily predatory, they are for sure risky if there is a recession/layoffs. For example, my fiance and I make about 200k together, we were pre approved for an a million dollar loan with a monthly payment somewhere near 10k.. if we were dumb enough to actually use that and either of us lost our jobs (ai, recession, etc) we would for sure have to sell pretty rapidly…

I think there a loooottt of people that have bought in the last few years that are in this situation.

i can’t put my fingers on what has caused this recent boom? Low interest rates? higher wages? inflation? private companies buying SFH?

This is my take:

Single family homes are an endangered species. Every detached SFR converted to ADU investment property or torn down to build an apartment building is one less detached on the market. Couple prop13, solar, 2.5% fixed mortgages, etc. and you have a market that can be cold for a long time.

Likely outcome is price declines in real terms while nominal bounces around.

My September 2022 detached purchase will breakeven as a rental at 60-70% LTV, which is great for SD. It helped getting a discount, NEM2 solar, AC, hot tub, and EV compatible.

Hey, I’ve seen you make similar points a few times here, and I get that you have strong convictions — it sounds like you’ve made moves in the market and feel good about your position. I’m on the other end of that equation, and while I respect your take, the constant “SFHs are forever rare and therefore guaranteed to rise forever and ever” framing can get a little repetitive.

I think it’s worth keeping in mind that there are scenarios — backed by real data — where SFHs don’t just endlessly appreciate. A few things to consider:

San Diego’s population has actually been flat or even declined a bit since 2020, depending on the source. So the idea that supply constraints alone explain recent price jumps doesn’t tell the whole story.

The city’s median age is around 40, and the population skews older. With birth rates down and fewer young families forming, long-term demand growth may not be as reliable as it once was. (data from 2020 census)

Investors have made up about a quarter of home purchases recently (source). If price growth slows or reverses, it’s reasonable to expect at least some of them to exit, which could shift dynamics quickly.

And like I mentioned in a previous response, while today’s loans aren’t necessarily predatory like in 2008, they’re still highly leveraged. I was pre-approved for a $1M loan, and if either my fiancée or I lost our job, we’d be in a tough spot and would probably need to sell if we couldnt find another job quickly. I think a lot of people are in similarly fragile positions, even if they don’t realize it yet. That along with all the pressures from AI/tariffs/other nonsense, and it seems like there is more fragility here than a lot of people realize.

Look at home prices in Japan and other areas (parts of Italy, parts of Germany) of the world where population has started to decline to see a potential picture of what could happen here, especially if immigration slows as well as birth rates.

I’m not saying prices will necessarily crash — just that the picture is more nuanced than “SFHs are inherently bulletproof, are endangered, will never fall, blah blah” Reasonable people can disagree, of course — just offering a counterpoint.

If price growth slows or reverses, I think it’ll bring in even more investors. These investors aren’t flippers like in 2008. They buy SFR and stick as many ADU as they can into them. Go here to see how much it cost to build a builder grade ADU: ADU Builder San Diego – Snap ADU Design Build Contractor. You’ll see that if you’re able to stick 2 ADU on a lot or convert a garage into a JADU and build 1 ADU, you can probably break even.

So, while flippers were playing musical chairs, today’s investors are in it for the long run. Which means if price falls, their value prop will get even better. If recession hits and rates fall, their value prop gets even better.

Also, keep in mind that for every property that an investor bought and does this ADU game, that’s one SFR removed from the supply side. Just drive around older areas of San Diego that doesn’t have HOA and you’ll see the scale of these investors.

Here’s one example I put together very quickly, if you buy this house https://redf.in/x26lGU for $1.2m and build this ADU in the backyard Duplex Two Story 3 Bed 2 Bath ADU Design, which you have enough space to do. Your total cost will be about $1.9m. At $1.9m, your PITI would be about $12k/month. Each of those duplex can rent for about $3500-4000. So, you’re raking in $7k-8k in rent. Which means you just need to come up w/ $4k-5k to live in that house. Which is about the cost of rent for that house. This is before any tax deduction.

Not sure I understand your example, if you are planning to live in the house then you by definition aren’t an investor… Also your 12k a month excludes property and home insurance costs.

Even if you put the whole 1.9 mil down as cash and I took all your numbers (4k for each duplex, 4500 for the house as rent), it would take a whooping 12.5 years to make your money back, and that’s not even including the property tax and home insurance costs, how long it takes to build the ADU, I’m sure there is extra costs associated with it on top the advertised price, etc ..

Also even if you held the house for those whole 12 years where you potentially start making money, the house would have to appreciate by 190+k a year because you would make ~10% a year on that 1.9 a mil every year. So I don’t see what the value proposition you see for holding these for long times, especially if price stagnates

Sorry forgot to include the reasoning for that ~10%, that’s the standard return in the stock market, so if you took that 1.9 mil and instead just invested it, that’s how much you could expect to make on it.

Also upon looking at that example closer, I dont even think that ADU you linked would fit in that yard, and even if it did, it would take the whole thing up and I think probably decrease the value of the property…

Regarding comparing return to the stock market, do you think these investors haven’t done their due diligence? If you have $2m in cash, don’t you think that person would have analyzed all the options at their disposal to see which path would yield them the highest return? We’re not in the age of neg am loans anymore, so these are people w/ skins in the game.

Whether it decreases the value of the house or not, as long as the investors make a profit from rent, do you think they care if their goals are long term rentals? However, from a macro picture as a homeowner of a SFR, as long as there are investors who are doing this, they’re decreasing the supply of SFR. Do you think price pressure will go up or down when you decrease supply?

Even if you’re right and these businesses will all go under and that group of demand will disappear, all the SFR that they bought up and built ADUs on cannot be undone cheaply. So, supply of SFR is decreasing because of these ADUs.

That’s just one example, but not a great one, since that house is at the high end of the price range for that size because it’s fully remodeled. Take ones that’s not remodeled, and you can get it for mid to high 900k. It was just a rough example of how you can make it work as an owner who doesn’tt care about a yard. If you’re talking about investors, then they would rent it out.

You really don’t need to dissect my example. You just have to believe all the investors who are buying up SFR and putting ADU on them have done their due diligence and the numbers work. That’s why they’re doing it. These are not flippers. You need cash to build ADUs. It’s not like 2005 where people were buying wo no doc loans to flip the house. If you had a few million to do these projects, do you think they wouldn’t have done their due diligence and ran the numbers? It must make sense for them to commit that kind of $ to the project. Also, keep in mind these investors tend to have their own crew as well, which mean they’ll be building them for even cheaper than what SnapADU are doing them fore, since SnapADU are making a profit building them too.

So, if you tell me their costs are going down, do you think they’ll do more or less of similar projects? My vote would be that they’ll do more of it.

I think what I can get from this discussion as well as overall consensus is the following:

IMO what it comes down to is the age old adage of if you have the funds/desire to get a home and don’t plan on moving in foreseeable future, and you feel your job is secure enough then go ahead and make the purchase. Would it have been better to purchase in the past with lower prices/rates? Of course.

Is it a good investment, at least in the short term? Probably not, but long term likely will net positive for you if you plan on staying in SD.

I think you’re both circling the right possibilities for San Diego’s housing market. Sure, population growth has been flat, but SD is still a vacation hot-spot with world class universities and job opportunities and that keeps rental investors interested—especially at the upper end.

The real question for me is whether something external shows up that forces investors (or older, fixed-income owners) to unload single-family homes. Without a real shock, prices probably just bump along the top of the affordability range instead of falling hard.

Here are the three shocks I keep an eye on:

Barring one of those, home prices probably stay “sticky.” Supply is still tight, demand (both local and investor-driven) isn’t going away, and building new inventory here is a slog. I actually think the STR backlash is the most likely near-term catalyst—neighbors are getting louder.

Happy to hear other scenarios, but that’s how I see the risk stack right now.

I appreciate your response and the points you made, just want to contradict the point about current supply and demand (ie. “supply is still tight and demand isnt going away”). Based on the graphs Rich posted (thanks Rich!), it does seem that supply is rapidly returning to 2015-2019 norms while demand is currently abysmal (based on months of inventory, sales charts, etc…).

So is it reasonable for houses to be double the price as they were in 2019, when demand is much lower, supply is potentially higher or the same, and interest rates are much higher than then? We may find out

As the saying goes, all RE are local. While San Diego as a whole is seeing a rapid increase in supply, thanks to sdrealtor for posting inventory of 92126 from 2021, it’s not the case for 92126. This time 4 years ago, there were 18 SFR with median price of $825k. Today, there are 22 SFR with median price of $1.19m. So, supply here hasn’t increased much while median has increased 45% over the last 4 years.

I totally hear you on inventory climbing fast. I’m not disputing that—it’s clear from Rich’s charts that supply is rising and demand is pretty muted. My earlier point was more about what it would take to move prices in a significant way, not whether the conditions are shifting.

From my view, once we hit around 3.5 months of inventory, we might start seeing some downward pressure on prices. But even then, I’d expect more of a slow melt than a sharp drop. There are still plenty of buyers on the sidelines—investors, downsizers, people with locked-in equity—who jump in when something gets priced just under the comps. So unless there’s a real shock, those price cuts get absorbed pretty quickly.

This is a good overview, I largely think of it this way too. I think a recession is the biggest risk… they do happen sometimes! And it’s not the end of the world if they do, but it can often be a catalyst for overvalued investments to correct back towards normal. Of course the longer we can go without one the more “work” can be done by prices just bouncing along as inflation etc catches up.

In an ironic twist, the goal of increasing housing is actually propping up detached SFR values. The new ADU rules (even after partial rollback) favors converting detached SFR to rental properties. That reduces supply of detached SFR that a family could choose from and afford because investors base their purchases on what a property COULD do, not what it is.

Investors are buying up detached SFR to rent them out with new ADUs, look at the silly 17 unit clairemont property highlighted the ADU backlash.

Does this suck for regular families? Of course. Absent a prop13 rollback and legal mechanisms to stop investors buying SFR I don’t see how this stops.

You will own nothing and be happy is true. I’ve been watching my predictions happen in real time, we’re in Neo feudalism for detached. They can always build more cubes that will help keep a lid on appreciation for detached and condo, but it’ll only blunt the price action.

Use this link to see it live.

https://altos.re/r/cf071f91-3fd8-4451-9fc6-52f243001ddc

Ask chatGPT this exact question:

“Are San Diego ADU laws making detached homes less affordable to buy? Ignore whether it makes rents cheaper for population as a whole, as I’m a buyer, not a renter.”

It’s also important to remember that detached SFR is an aspirational purchase versus condo/townhome. You own the land with detached. You can build whatever you want later. You can have no HOA if you want. Most people will accept a condo/townhome because that’s what fits their budget, but most would take detached if they could.

I kept my townhome – converted to rental when I bought detached. I went from flights of stairs to ranch style, I can’t get that in condo unless I go ground floor. What happens when I’m 80 and can’t use stairs?

There’s a real argument that monthly-payment-to-rent ratio is out of whack, but that assumes you’re a small time investor needing leverage. It also assumes rates stay where they and that I don’t add an ADU or two.

San Diego is land constrained with an unfavorable need to increase housing which can only come from new cubes. More people in cubes equals more people competing to get out of cubes.

Redfin Survey: 1 in 3 Baby Boomers Say They’ll Never Sell Their Home

My September 2022 detached purchase will breakeven as a rental at 60-70% LTV, which is great for SD.

That doesn’t seem great to me? Maybe I’m misunderstanding your metric. I’m thinking through an example…. let’s say you put down $650k on a 1 mil place (middle of your LTV) range. You are making 0 net cash flow, so all you get is the appreciation on the $1 million place… obviously that’s unknown but IMO you are lucky to keep up with inflation from these valuation levels.

If home prices merely keep up with inflation, that translates to a nominal total return of 1.54x inflation (due to your leverage). That’s not very good… 10 year inflation breakevens are 2.3% so if we use that as an inflation metric, your nominal return is 3.5% and your real return is 1.2%. For this to be great, you have to be betting on home prices significantly outpacing inflation, or inflation VERY significantly outpacing consensus expectations.

It’d a great ratio for SD. Right now, most folks would be around 40-45% LTV at same market rates and loan program I bought at. Traditionally, SD has always required higher down payments than lower cost of living areas. If you think 60-70% LTV to break even (cash flow not counting principal reduction) then check San Jose or other HCOL areas.

One of the first signs of the popping bubble in 2008 was the courthouse auctions downtown everyday. I used to eat at sushi deli 2 everyday and watch it go from 1 to 5 to 10 to 50 per day. Is anyone tracking this data or is there a graph ?

Decades of SD foreclosure stats.

http://www.foreclosureforum.com/stats.html

I have a mortgage on a townhouse in Mira Mesa.

I originally paid $729,000 and had $490,000 mortgage at 2.5%

My current mortgage payment is $1936 a month.

This is a 3 bed, 3.5 bath townhouse for $1936 mortgage.

Compare that equivalent rent would be around $4500 a month.

You can’t even rent a 1 bedroom for under $2500 now.

My actual housing expense is much higher because I have $400 association fee and $900 a month in property taxes I pay separate.

So lets figure my total carrying cost for this 3 bed, 3.5 bath is $3200 a month…..still significantly cheaper than rent.

Even if my 1.1 million condo dropped down in value to the $729,000 I paid for it it would still not be in my best interest to default as renting an equivalent unit would still cost me $1200 more each month.

This is why I feel San Diego is immune to a massive crash because there are too many people with 2-4% mortgages where their payment is significantly cheaper than current rental rates.

Not to mention the huge equity cushion gained in past few years.

I can lose $600,000 in current value and still be above water on my mortgage:

So there is basically no way a crash can force me into forclosure or short sale.

Yep, I think this is true not just for SD but everywhere — for anyone who bought before the big covid runup. I’ll add that even if you lost your ability to service the mortgage, it would not make sense to default – in that case you’d just move into a cheaper rental, and rent your place out for the larger amount. This is why I agree there isn’t much chance of a late-2000s style event.

But it’s a very different picture for people who bought after the runup. They have the high rates/monthly payments, so don’t have the favorable comparison to renting that you do. Also, contra your statement (the only one I disagree with) – they have not gained significant equity; home prices are basically unchanged from 3 years ago. So I think the point raised by another poster above is valid: more recent buyers are vulnerable to a negative financial development in a way that pre-pandemic buyers are not. And that is some degree of risk to the market, though nothing like the late aughts.

Here are the questions for which I wish I had data—ideally sliced by ZIP so we know where stress might show up first:

No solid thesis until we can pin these down—just lining up the ducks.

Some of that is available, but not necessarily specific to SD. California has the worst lock-in effect at 71% below 4%.

https://www.axios.com/2025/05/19/mortgage-rate-state

San Diego is top 10 for LOWEST turnover rate

https://www.redfin.com/news/home-sales-turnover-2024/

Post 2020 loans DQ is too wide as COVID era loans are extremely low delinquency, you’d need mid-2022+, which would take a lot of digging and may not be available by Fannie/Freddie or FHFA.

There was a small window from mid-2022 through Spring 2023 during the flash crash where those folks got a nice drop in price, higher mortgage rate, and could refi down a point or two depending on their initial rate. It’s a relatively small population, but they did benefit buying in that window with getting appreciation and refi potential.

Another signal I would be interested in to gage the potential magnitude of impact of a STR crackdown: What percentage of SFH/all housing was owned by a corporation (LLC, sole prop, whatever) vs. a person/s in the pre 2020 era as opposed to today?

Detached SFR in clairemont pending in 12 days at a price point I figured it would move at. Renovated interior with clean (basic) backyard on a good size lot. It would put my place worth about $1.3m+ range assuming this comp sells at $1.279m, which is on target with realtor.com values (I’m 0.1mi away and a residential lender).

https://www.redfin.com/CA/San-Diego/6863-Tanglewood-Rd-92111/home/5166241?

This is an interesting temperature check. 1.279m home purchased with 20% (255k) down is ~8567/month after tax/mortgage/insurance. Assuming this is a dual income no kids couple both spending 50% of earnings, they would each need to earn >150k/yr before taxes to live on this 7k SQFT lot in east clairemont in a 50+ year old home that appears to have the standard flip or flop motif. I suspect this will turn into another STR and be one less family in San Diego.

Currently, the monthly cost to own is $8,567 at a 7% interest rate. However, if interest rates decline, they could potentially refinance to $6,800/month at 5%. Compared to an estimated rental income of $4,500/month, owning this property seems reasonable, especially when considering the significant cost disparity between renting and owning observed in the Carmel Valley example earlier in the discussion.

For a family assuming 20% down they’d probably need $200k+ to qualify and with any extra debt need $250k+, which isn’t absurd for a two income professional household, but obviously on the higher end. If they’re moving significant equity from a prior home then most of this is moot.

Making $150k household isn’t what it used to be in SD. Median HHI crossed $100k in 2023 to $103.5k from 83.5k in 2019, or a 24% increase.

https://fred.stlouisfed.org/series/MHICA06073A052NCEN

We’re in a similar cohort. Im 42, BS/MS degrees, ~116k/yr, own a 1/1 condo from 2010 with ~250 in equity. If I bought a 1m home using the 25% down, I would be facing 5,304/month or effectively all of my post tax income. Even splitting this with someone would be a struggle then add kid/s and daycare into the mix and it becomes financially irresponsible if not impossible.