Over at my day job, we wrote a long piece attempting to get our heads around what’s going on with housing. Check that out and if you’re still awake at the end, here are a few bonus graphs:

Over at my day job, we wrote a long piece attempting to get our heads around what’s going on with housing. Check that out and if you’re still awake at the end, here are a few bonus graphs:

I’d be curious to see what

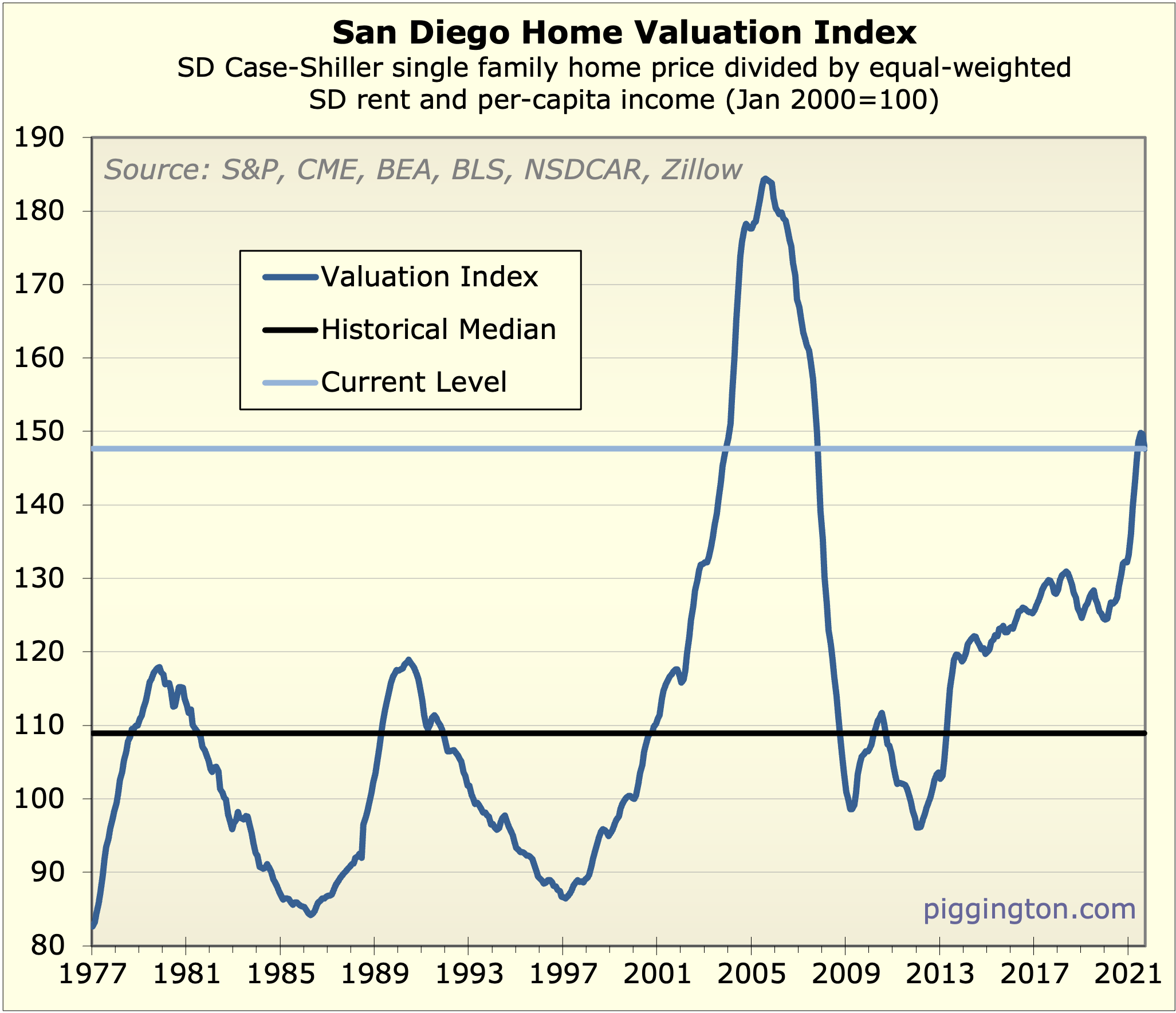

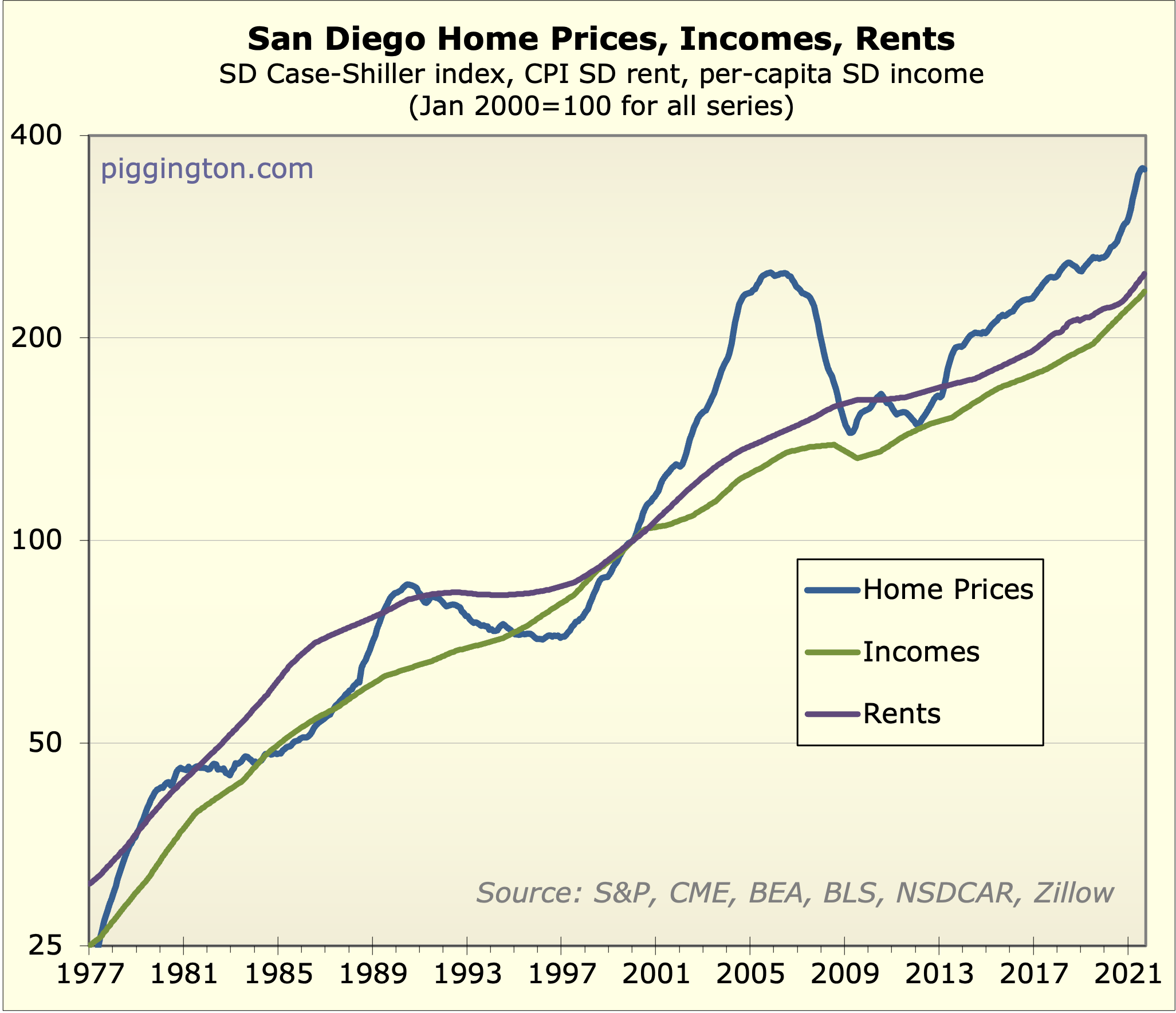

I’d be curious to see what these graphs look like if the oughties bubble peak was brought down to previous peaks. My point being that the last bubble had such a huge impact on the median values over the period that it makes the current bubble appear less innocuous. Only in comparison with the last (truly amazing) bubble is the current bubble not incredible. Of course, hey… maybe it’s no bubble at all. I’ve lost my ability to tell, frankly.

Totally, if we took out the

Totally, if we took out the bubble, current valuations would dwarf prior peaks.

But I’m not sure that chart alone can prove it’s a bubble. For one thing, I could see there being a long term uptrend in the “fair” or sustainable valuation (due to supply constraints, globalization of the housing markets, or what have you).

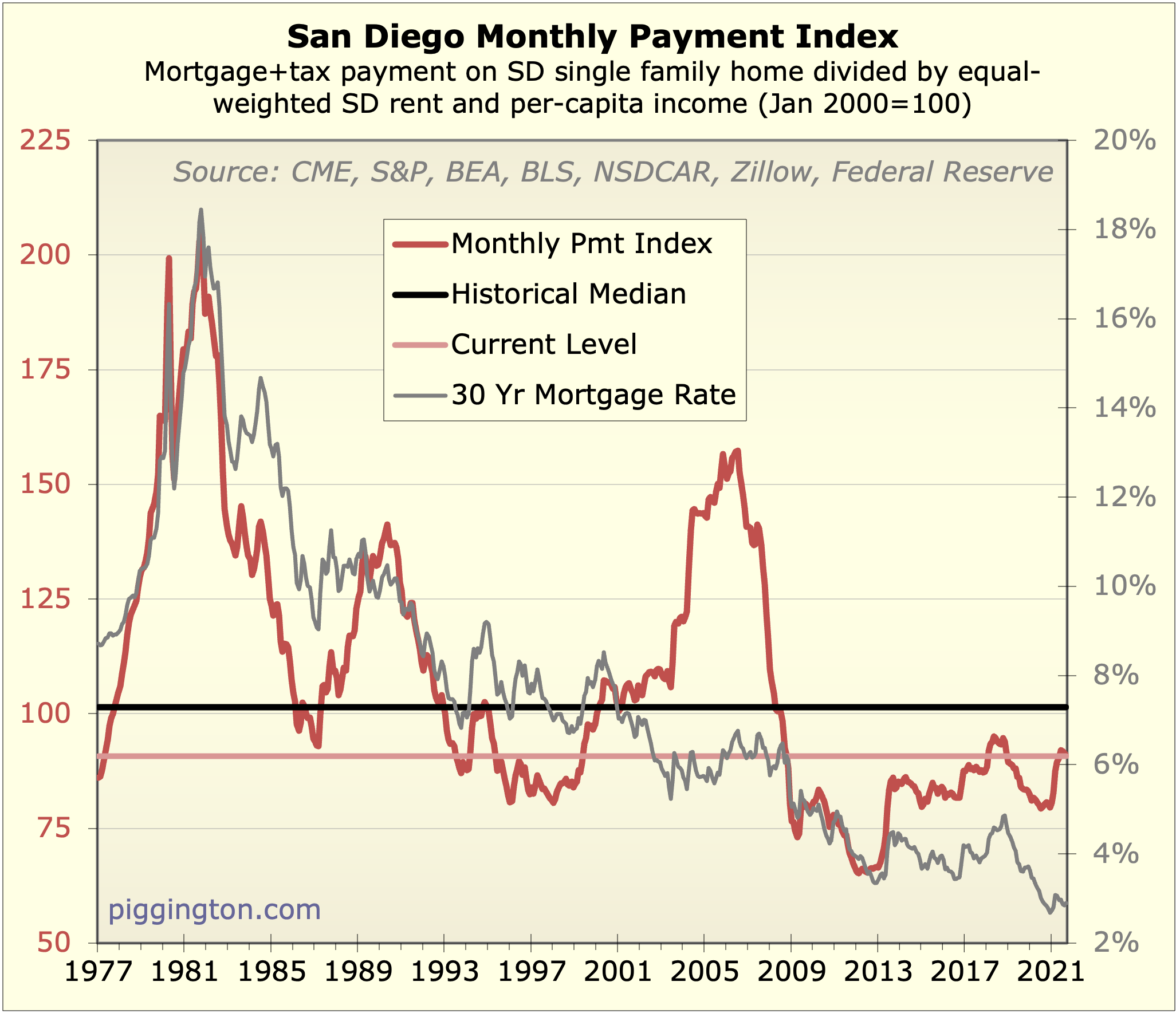

But a much bigger thing is the interest rate factor. Given that people finance their purchases with fixed rate mortgages, and that rates are super low, it could be rational in some cases to buy at these prices. (See the monthly payment graph). And if it’s rational to buy, at least sometimes, can it truly be a bubble?

My take is: it’s expensive, and if rates go up, it will likely prove to have been unsustainably expensive. But that’s not the same as a speculative bubble, which in my view requires a certain level of behavioral craziness we aren’t seeing, and also (in my view) implies an inevitable price crash.

Thoughts?

Just for giggles here is your requested graph. It doesn’t change the median; it would change the historical average but I don’t chart that. However, it changes the historical standard deviation quite a bit, so taking away the prior bubble would put us comfortably above Grantham’s “2 sigma” rule of thumb for bubble-spotting. For what that’s worth…

30 years mortgage has been

30 years mortgage has been declining for 40 years. I don’t expect the trend to suddenly change, unless we have massive inflation for several years, akin to the mid to late 70s. Back then, when rates rise dramatically, it didn’t cause a housing crash. So, I’m not sure you can assume that it’ll crash it this time.

I’ve been saying this since 2008 but monthly payment matters more to most people than the absolute price of the house. Mortgage payment today is still much lower than the historical average.

an wrote:Back then, when

[quote=an]Back then, when rates rise dramatically, it didn’t cause a housing crash. [/quote]

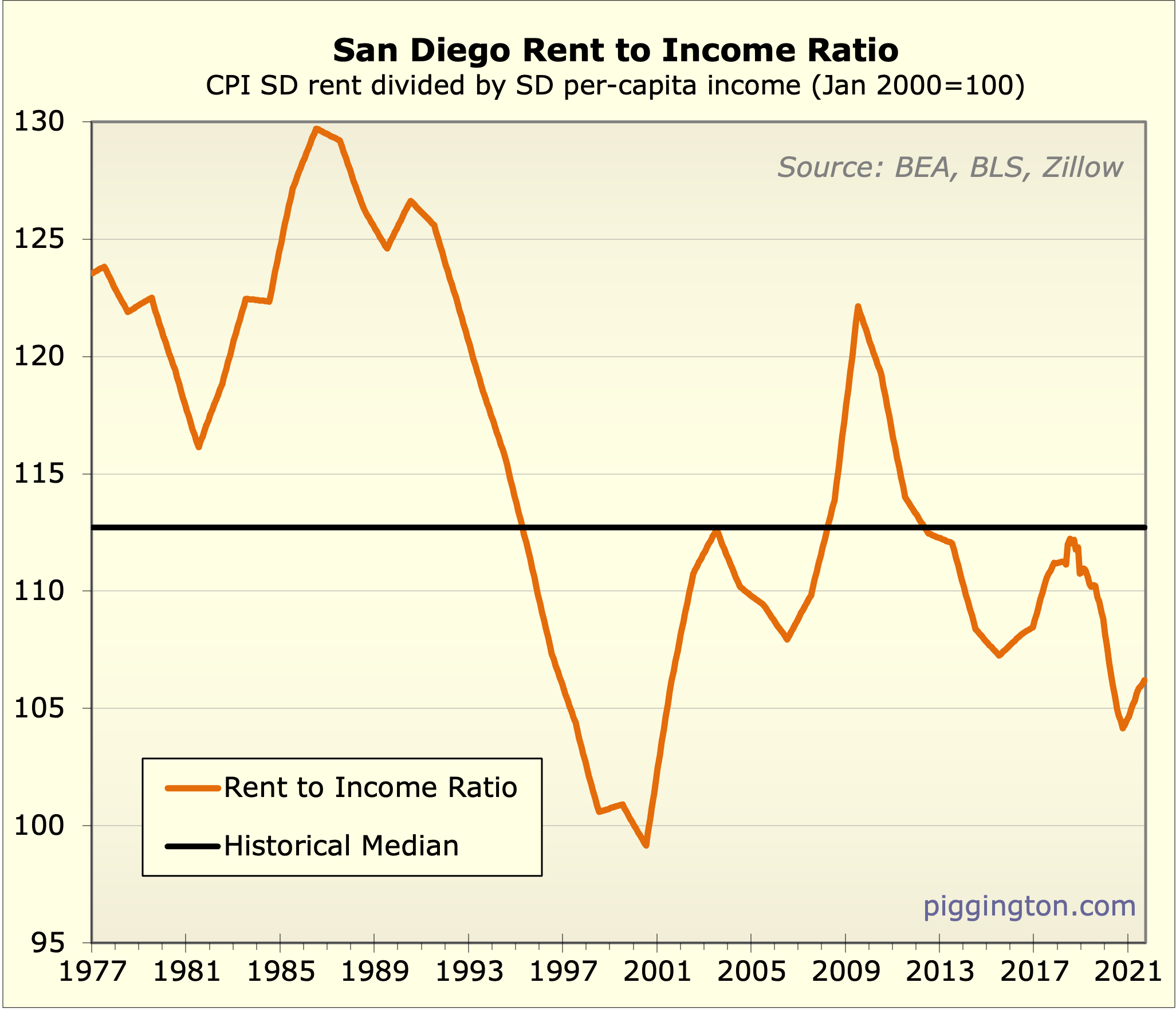

I don’t know about a crash but valuations dropped 25% in the early 80s (and it’s worth noting that they began that period a lot lower than they are now).

Rich Toscano wrote:an

[quote=Rich Toscano][quote=an]Back then, when rates rise dramatically, it didn’t cause a housing crash. [/quote]

I don’t know about a crash but valuations dropped 25% in the early 80s (and it’s worth noting that they began that period a lot lower than they are now).[/quote]

Really? I don’t see any drop in your chart above between 77-85. When rate increased from 77-81, price also went up. Am I reading your chart wrong?

Rate rise between 77-81 and price went up. Rate dropped between 81-85 and price flat line.

an wrote:Really? I don’t see

[quote=an]Really? I don’t see any drop in your chart above between 77-85. When rate increased from 77-81, price also went up. Am I reading your chart wrong?[/quote]

Couple clarifications here. First, I was talking about the period starting when rates went really high in 1981. Second, I was talking about valuations, not nominal prices. Very high inflation “absorbed” the drop in valuations. But it was a pretty big drop.

Rich Toscano wrote:an

[quote=Rich Toscano][quote=an]Really? I don’t see any drop in your chart above between 77-85. When rate increased from 77-81, price also went up. Am I reading your chart wrong?[/quote]

Couple clarifications here. First, I was talking about the period starting when rates went really high in 1981. Second, I was talking about valuations, not nominal prices. Very high inflation “absorbed” the drop in valuations. But it was a pretty big drop.[/quote]

Thanks for clarification. Although 1981 is the peak of rate in the last 45 years, 77-80 is still VERY HIGH compare to rates over the last 45 years. I also wasn’t talking about absolute rate but the direction of rate change. My point is that, while rate increased drastically between 77-81, price did not decline. So, just because price is high now, there’s no guarantee that price will fall if we see rates increase at the same rate as between 77-81.

I, as a buyer of real estate, don’t care about valuations like nominal price. So, making a point regarding rate might increase doesn’t matter to me (and I have to guess most other buyers) if it doesn’t cause a decrease in nominal price.

an wrote:30 years mortgage

[quote=an]30 years mortgage has been declining for 40 years. I don’t expect the trend to suddenly change, unless we have massive inflation for several years, akin to the mid to late 70s. Back then, when rates rise dramatically, it didn’t cause a housing crash. So, I’m not sure you can assume that it’ll crash it this time.

I’ve been saying this since 2008 but monthly payment matters more to most people than the absolute price of the house. Mortgage payment today is still much lower than the historical average.[/quote]

I dont disagree but wonder what happens as the market gets even more expensive? Homes are more and more sold based upon assets (aka cash reserves, equity from prior home) rather than income. I wonder how that will play out if prices continue their ascent? I dont have the answer

Rich Toscano wrote:

My take

[quote=Rich Toscano]

My take is: it’s expensive, and if rates go up, it will likely prove to have been unsustainably expensive. But that’s not the same as a speculative bubble, which in my view requires a certain level of behavioral craziness we aren’t seeing, and also (in my view) implies an inevitable price crash. [/quote]

Nice job with the graph, sir! I would argue we are seeing *some* behavioral craziness although not nearly the level as pre-Financial Crisis. There’s a whole lotta flippin’ goin’ on, although you don’t see the “buy 10 houses” craziness. Arguably… merely the widespread willingness to pay these prices – despite the “monthly payment” argument – indicates a bit of nuttiness. But… it’s not nearly the level of last time.

Maybe rates will stay low forever. Where would Paul Volcker’s Fed have short-term rates right now? 7%-8%? I think the Fed has become such a political animal that adverse selection where the governors are concerned is a permanent feature. Everything now is a popularity contest and that means low rates forever (if that can be engineered)… inflation be damned. Is anyone other than central banks buying long-dated treasuries now? How does an investment manager justify an imbedded negative real return of several percentage points? Philosophical questions for my betters to contemplate…

If I run a search

If I run a search for

3BR+

1750 sf

in a box from the border to highway 76 coast to 10 miles west of i-15,

only 445 homes on market for less than 1.25M on zillow

At the rate things are going, they might be gone in a month and we may have a new median 10-20K higher.

It kind of becomes a momentum game for everyone at a certain point.

Some can’t sell because they need a place to live.

Some don’t want to sell because it’s doing well and why fight the Fed/market.

Some will sell when they depart the earth or their heirs will inherit.

In any event, in the era of relatively cheap money, holding on to real estate locally seems to be a winning bet.

When I read about incomes rising in San Diego with the influx of tech workers and how prices here are still meaningfully lower than LA/Bay Area, it’s hard to see things letting up.

Rich Toscano wrote:Totally,

[quote=Rich Toscano]Totally, if we took out the bubble, current valuations would dwarf prior peaks.

But I’m not sure that chart alone can prove it’s a bubble. For one thing, I could see there being a long term uptrend in the “fair” or sustainable valuation (due to supply constraints, globalization of the housing markets, or what have you).

But a much bigger thing is the interest rate factor. Given that people finance their purchases with fixed rate mortgages, and that rates are super low, it could be rational in some cases to buy at these prices. (See the monthly payment graph). And if it’s rational to buy, at least sometimes, can it truly be a bubble?

My take is: it’s expensive, and if rates go up, it will likely prove to have been unsustainably expensive. But that’s not the same as a speculative bubble, which in my view requires a certain level of behavioral craziness we aren’t seeing, and also (in my view) implies an inevitable price crash.

Thoughts?

Just for giggles here is your requested graph. It doesn’t change the median; it would change the historical average but I don’t chart that. However, it changes the historical standard deviation quite a bit, so taking away the prior bubble would put us comfortably above Grantham’s “2 sigma” rule of thumb for bubble-spotting. For what that’s worth…

what we are seeing w/ local RE prices “rising” makes sense IMHO because I am thinking about the dollar being the global reserve currency

IOW since the dollar is the global reserve currency, this means the world needs dollars to settle accounts,… so the amount of “credit” dollars out there is ever growing,… when there are more “credit” dollars out there chasing a limited supply of RE (as in the case here in San Diego) the price of RE goes up

BUT we have to consider the idea that all good things come to an end (i.e. some day the dollar will no longer be the global reserve currency)

https://www.bis.org/publ/work684.pdf

I’ve also been I’ve been wondering about is RE prices during the 1930’s Great Depression,… where we see RE prices as expected during the roaring 1920’s went up and during the depression, prices of RE went down

https://www.hbs.edu/ris/Publication%20Files/Anna_tom_59f6af5f-72f2-4a72-9ffa-c604d236cc98.pdf

the reason I bring the idea up of RE prices during the 1930’s Great Recession is because I’m pretty sure if the dollar was not the global reserve currency,… prices of local San Diego RE (as well as RE in other parts of the USA) would not be as high as they are now

phaster][quote=Rich Toscano

[quote=phaster][quote=Rich Toscano]

the reason I bring the idea up of RE prices during the 1930’s Great Recession is because I’m pretty sure if the dollar was not the global reserve currency,… prices of local San Diego RE (as well as RE in other parts of the USA) would not be as high as they are now[/quote]

You have it backwards, the actual reserve currency of the USA is San Diego real estate.

Escoguy wrote:phaster

[quote=Escoguy][quote=phaster]

the reason I bring the idea up of RE prices during the 1930’s Great Recession is because I’m pretty sure if the dollar was not the global reserve currency,… prices of local San Diego RE (as well as RE in other parts of the USA) would not be as high as they are now[/quote]

You have it backwards, the actual reserve currency of the USA is San Diego real estate.[/quote]

if memory serves,… money has three basic characteristics:

1) medium of exchange

2) unit of account

3) a store of value

SD RE is a store of value,… so item (3) fits

as for items (1) and (2),… think it would not be practical to exchange a fraction of SD RE for a meal at a restaurant or a tankful of gasoline

as for SD RE,… seems agents here in town are really upping their game

I say that because this week in the mail I received a pretty slick catalog of local SD RE for sale,… I guessing it was sent to me because a home a few doors away(on the website) is being listed AND/OR perhaps somehow I’m on the mailing list because they think I might be interested in selling,…

anyway was sent a 28 page “first go at print” brochure that remind me of an mini architectural digest magazine or even a nemien Markus

“we hope you keep these lookbooks as coffee table magazines; something to share with out-of-town guests curious about San Diego’s architecture offerings”

https://www.agentsofarch.com

Latest data in y-o-y detached

Latest data in y-o-y detached homes up 5 to 7% depending upon what part of town. They were up close to 20% y-o-y 3 months ago

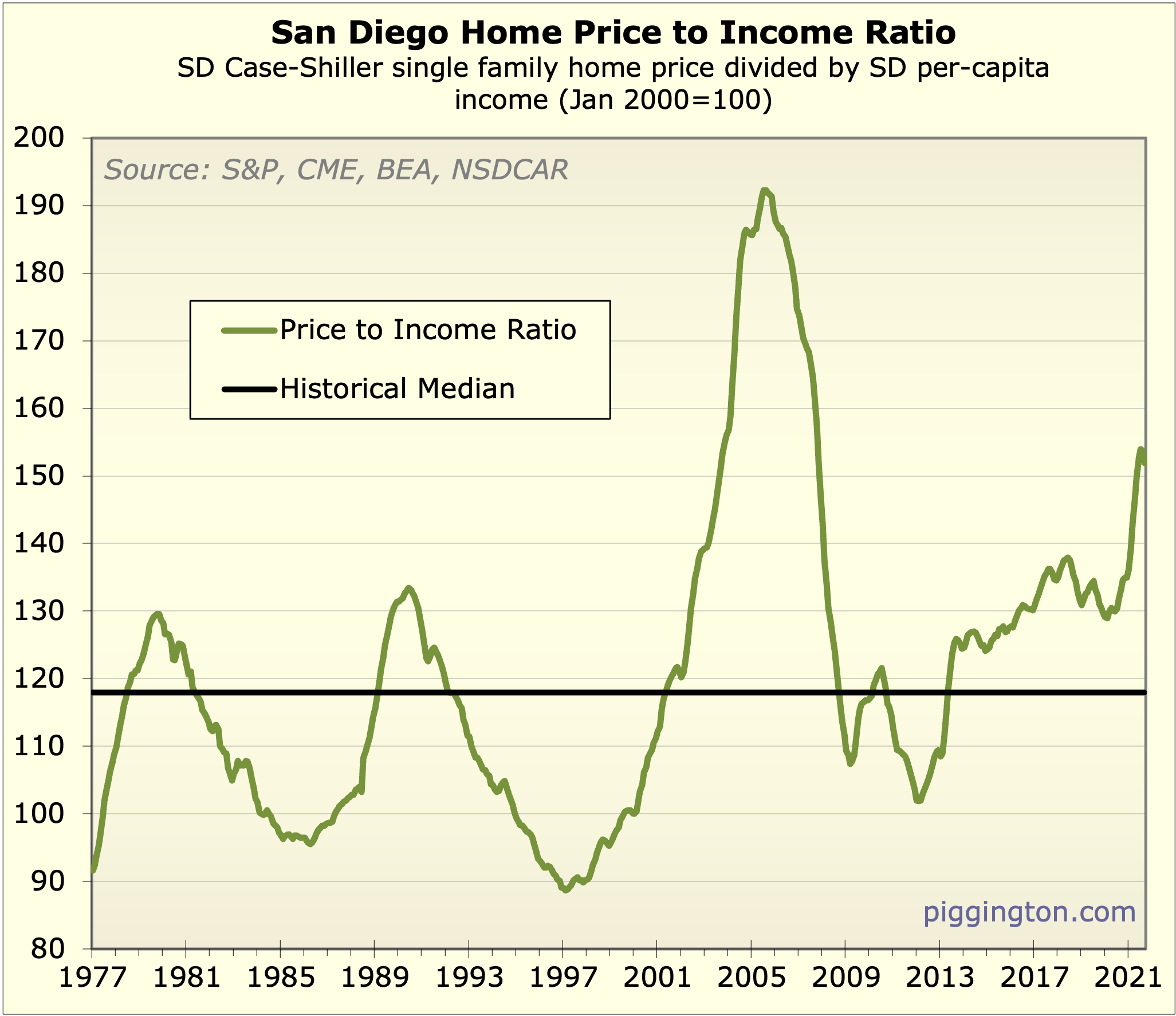

Prices aren’t just lower than

Prices aren’t just lower than SF/LA, also lower than Seattle, NY, London, and all the major east asian cities. Meanwhile we have the best weather and lowest crime in the West plus lots of big city amenities.

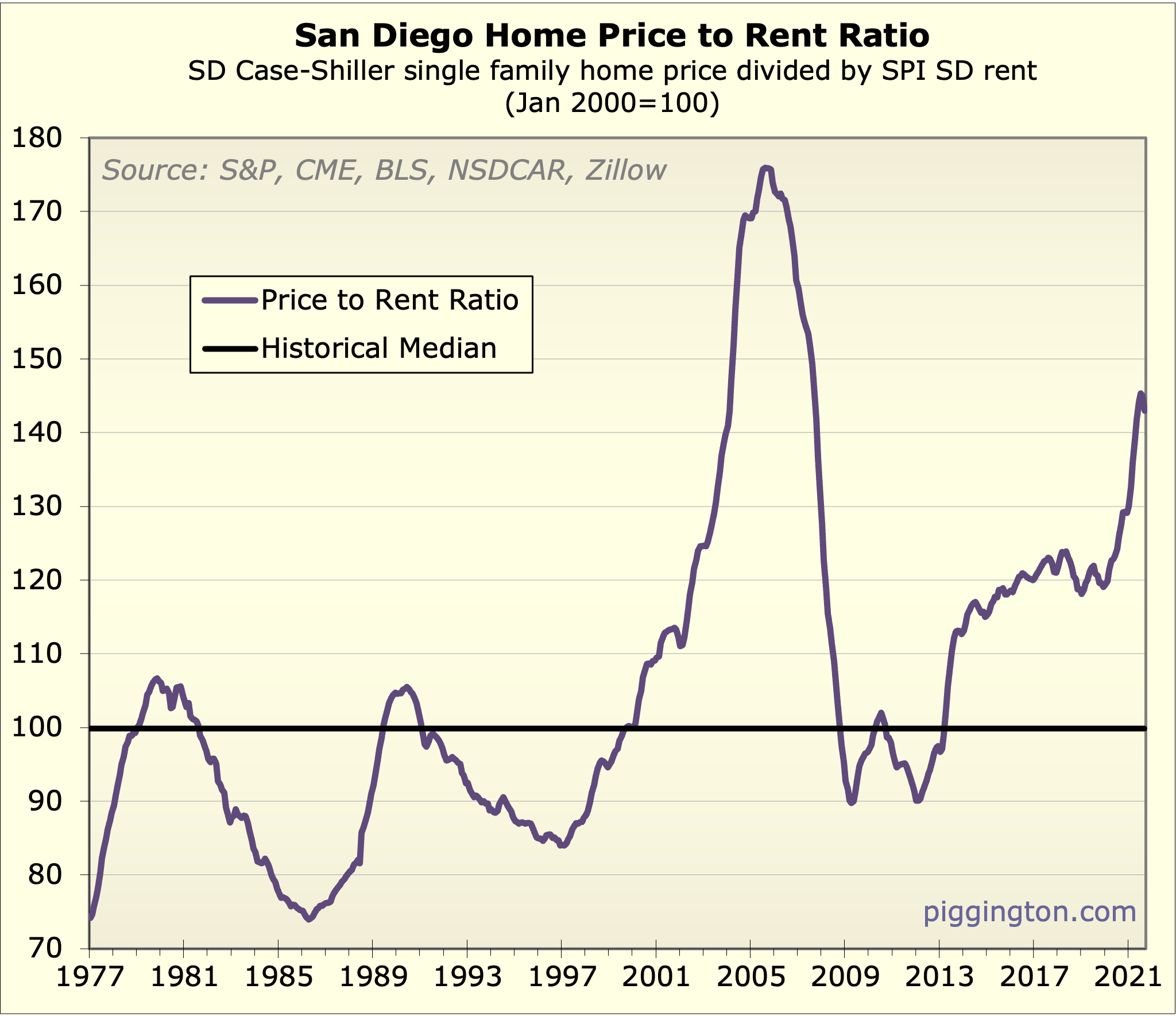

When you look at price/rent and price/median income ratios in Asian markets, you can see that Asian home buyers are used to paying much higher prices than we have locally.

OC is better positioned than San Diego to be the “new Vancouver” for such buyers, but we’re still in the running, and there can be more than one.

The data quality seems iffy,

The data quality seems iffy, but this site suggests San Diego is one of the more affordable large cities in the world.

https://www.numbeo.com/property-investment/rankings.jsp

We’re ranked in the 350s or 360s out of 480 cities in the various measures of affordability, price to rent, and price to income.

Here’s a site with price-rent ratios for 94 US cities. San Diego is tied with several cities at around the 30th percentile. Given how strong our fundamentals are and Prop 13, seems like we’re a great relative value. Tulsa, Knoxville, Tuscaloosa, Reno, SLC, are all more expensive than San Diego compared to rents!

https://www.mashvisor.com/blog/price-to-rent-ratio-by-city-2021/

Here’s the third source on this topic I found.

https://money.cnn.com/real_estate/storysupplement/price_to_rent/

It is out of date (2009), but it interestingly proves a 15 year average price to rent for major cities, 1989-2003. We’re 7 on that ranking, with Oakland, SF, and San Jose the top 3.

IOW since the dollar is the

It is one of several. This year the dollar is 59% of central bank reserves.

The impact of this on the real economy in the USA is pretty small. The US gov gets an interest free loan when foreign banks hold dollars. But guess what, the governments of Japan and most of the EU can also get interest free loans because their bond rates are 0% or less.

Investors in unstable dictatorships like China like to move their money abroad to someplace with lower risk of government seizure, but they rationally just care about total return. Who cares what currency it is measured in, as long as the currency is convertible?

In summary I agree US assets are very attractive to foreigners and will continue to be so. But I don’t think it has much to do with the dollar’s reserve status, and more because of our stable legal system that protects the rights of foreign investors. They like Canada and Ireland too, and would like a hypothetical independent San Diego with its own currency that isn’t held or used elsewhere.