Forum Replies Created

-

AuthorPosts

-

July 17, 2009 at 10:22 AM in reply to: OT- ‘Since when does our great free-market country punish success’… #432734July 17, 2009 at 10:22 AM in reply to: OT- ‘Since when does our great free-market country punish success’… #433034

SK in CV

Participant[quote=EconProf]SK: When tax rates change it takes a while for the actors in the economy to change their behavior, then the hiring, investing, building etc. to increase or decrease, then output and incomes to change, then the tax revenues approaching the following year’s tax deadline of April 15 to change. These time lags are why it is difficult to ascribe a change in government revenues to an earlier change in the tax rate. And that’s why I gave you the six-year result after the tax rates were changed under Kennedy and then Reagan.[/quote]

I don’t disagree with you at all on this. I don’t know that it’s 6 years. It may be 4, it may be 10. But given that there are so many other variables affecting the cyclical economy (we’ve had 7 recessions in the last 40 years, roughly 1 every 6 years on average, ranging from 2 quarters to the current recession, which is likely to last 8 or 9 quarters), I’m still looking for compelling evidence that tax cuts are stimulative to government revenues, or that tax increases are depressive. There is none that i’ve found, either way.

July 17, 2009 at 10:22 AM in reply to: OT- ‘Since when does our great free-market country punish success’… #433105Participant[quote=EconProf]SK: When tax rates change it takes a while for the actors in the economy to change their behavior, then the hiring, investing, building etc. to increase or decrease, then output and incomes to change, then the tax revenues approaching the following year’s tax deadline of April 15 to change. These time lags are why it is difficult to ascribe a change in government revenues to an earlier change in the tax rate. And that’s why I gave you the six-year result after the tax rates were changed under Kennedy and then Reagan.[/quote]

I don’t disagree with you at all on this. I don’t know that it’s 6 years. It may be 4, it may be 10. But given that there are so many other variables affecting the cyclical economy (we’ve had 7 recessions in the last 40 years, roughly 1 every 6 years on average, ranging from 2 quarters to the current recession, which is likely to last 8 or 9 quarters), I’m still looking for compelling evidence that tax cuts are stimulative to government revenues, or that tax increases are depressive. There is none that i’ve found, either way.

July 17, 2009 at 10:22 AM in reply to: OT- ‘Since when does our great free-market country punish success’… #433268Participant[quote=EconProf]SK: When tax rates change it takes a while for the actors in the economy to change their behavior, then the hiring, investing, building etc. to increase or decrease, then output and incomes to change, then the tax revenues approaching the following year’s tax deadline of April 15 to change. These time lags are why it is difficult to ascribe a change in government revenues to an earlier change in the tax rate. And that’s why I gave you the six-year result after the tax rates were changed under Kennedy and then Reagan.[/quote]

I don’t disagree with you at all on this. I don’t know that it’s 6 years. It may be 4, it may be 10. But given that there are so many other variables affecting the cyclical economy (we’ve had 7 recessions in the last 40 years, roughly 1 every 6 years on average, ranging from 2 quarters to the current recession, which is likely to last 8 or 9 quarters), I’m still looking for compelling evidence that tax cuts are stimulative to government revenues, or that tax increases are depressive. There is none that i’ve found, either way.

Participant[quote=AN]Really? 56%? You must be making some serious dough. $10k in health insurance? My effective tax rate is well below 35% and I’m paying ~2500-3500/year in health insurance for a family of 3 w/ $10 co-pay & excellent coverage.[/quote]

You got a great deal on your insurance. Is your employer picking up a piece of that cost you’re not including? Aetna’s small group rate (10-50 employees) for San Diego family coverage for their $10 copay plan ranges from $1,290 a month for 30-34 year old to $1,559 per month for 50-54 year old. That’s almost $15,500 to $18,700 per year.

For their $10 copay plan with a step down in providers (as an example, Scripps Clinic doesn’t qualify), with similar benefits, the cost is $12,804 to $15,500 per year for comparable numbers.

I shopped 1/2 a dozen other insurance companies, they were the very close to the lowest I could find for similar coverage.

Participant[quote=AN]Really? 56%? You must be making some serious dough. $10k in health insurance? My effective tax rate is well below 35% and I’m paying ~2500-3500/year in health insurance for a family of 3 w/ $10 co-pay & excellent coverage.[/quote]

You got a great deal on your insurance. Is your employer picking up a piece of that cost you’re not including? Aetna’s small group rate (10-50 employees) for San Diego family coverage for their $10 copay plan ranges from $1,290 a month for 30-34 year old to $1,559 per month for 50-54 year old. That’s almost $15,500 to $18,700 per year.

For their $10 copay plan with a step down in providers (as an example, Scripps Clinic doesn’t qualify), with similar benefits, the cost is $12,804 to $15,500 per year for comparable numbers.

I shopped 1/2 a dozen other insurance companies, they were the very close to the lowest I could find for similar coverage.

Participant[quote=AN]Really? 56%? You must be making some serious dough. $10k in health insurance? My effective tax rate is well below 35% and I’m paying ~2500-3500/year in health insurance for a family of 3 w/ $10 co-pay & excellent coverage.[/quote]

You got a great deal on your insurance. Is your employer picking up a piece of that cost you’re not including? Aetna’s small group rate (10-50 employees) for San Diego family coverage for their $10 copay plan ranges from $1,290 a month for 30-34 year old to $1,559 per month for 50-54 year old. That’s almost $15,500 to $18,700 per year.

For their $10 copay plan with a step down in providers (as an example, Scripps Clinic doesn’t qualify), with similar benefits, the cost is $12,804 to $15,500 per year for comparable numbers.

I shopped 1/2 a dozen other insurance companies, they were the very close to the lowest I could find for similar coverage.

Participant[quote=AN]Really? 56%? You must be making some serious dough. $10k in health insurance? My effective tax rate is well below 35% and I’m paying ~2500-3500/year in health insurance for a family of 3 w/ $10 co-pay & excellent coverage.[/quote]

You got a great deal on your insurance. Is your employer picking up a piece of that cost you’re not including? Aetna’s small group rate (10-50 employees) for San Diego family coverage for their $10 copay plan ranges from $1,290 a month for 30-34 year old to $1,559 per month for 50-54 year old. That’s almost $15,500 to $18,700 per year.

For their $10 copay plan with a step down in providers (as an example, Scripps Clinic doesn’t qualify), with similar benefits, the cost is $12,804 to $15,500 per year for comparable numbers.

I shopped 1/2 a dozen other insurance companies, they were the very close to the lowest I could find for similar coverage.

Participant[quote=AN]Really? 56%? You must be making some serious dough. $10k in health insurance? My effective tax rate is well below 35% and I’m paying ~2500-3500/year in health insurance for a family of 3 w/ $10 co-pay & excellent coverage.[/quote]

You got a great deal on your insurance. Is your employer picking up a piece of that cost you’re not including? Aetna’s small group rate (10-50 employees) for San Diego family coverage for their $10 copay plan ranges from $1,290 a month for 30-34 year old to $1,559 per month for 50-54 year old. That’s almost $15,500 to $18,700 per year.

For their $10 copay plan with a step down in providers (as an example, Scripps Clinic doesn’t qualify), with similar benefits, the cost is $12,804 to $15,500 per year for comparable numbers.

I shopped 1/2 a dozen other insurance companies, they were the very close to the lowest I could find for similar coverage.

July 17, 2009 at 8:06 AM in reply to: Ethical considerations (none) for defaulting on non-recourse loan. #432320ParticipantGreat post analyst.

When homebuyers and lenders enter into mortgage contracts, each side takes on risks. Included in the risk that the lender assumes, is that the collateral will maintain value in excess of the loan amount. When that doesn’t happen and a homeowner continues to make payments, for whatever reason, they are performing above and beyond the implied expectations of the contract.

I find it no more immoral for borrowers to stop paying in these circumstances than for the lender to foreclose. (Actually, I don’t think ethics or morals should even be a consideration. Lender corporations, despite the courts treatment of them as a “person”, rarely act out of ethical or moral considerations. They act based of legal considerations.)

Things get a little bit dicier for recourse loans, risks are greater for the borrrower, more options exist for the lender. But morals and ethics still don’t come into play in any greater degree. Risks are still taken by the lender. And the legal consequences of failing to pay are spelled out in the contract. Both borrower and lender have to live with those consequences.

July 17, 2009 at 8:06 AM in reply to: Ethical considerations (none) for defaulting on non-recourse loan. #432533ParticipantGreat post analyst.

When homebuyers and lenders enter into mortgage contracts, each side takes on risks. Included in the risk that the lender assumes, is that the collateral will maintain value in excess of the loan amount. When that doesn’t happen and a homeowner continues to make payments, for whatever reason, they are performing above and beyond the implied expectations of the contract.

I find it no more immoral for borrowers to stop paying in these circumstances than for the lender to foreclose. (Actually, I don’t think ethics or morals should even be a consideration. Lender corporations, despite the courts treatment of them as a “person”, rarely act out of ethical or moral considerations. They act based of legal considerations.)

Things get a little bit dicier for recourse loans, risks are greater for the borrrower, more options exist for the lender. But morals and ethics still don’t come into play in any greater degree. Risks are still taken by the lender. And the legal consequences of failing to pay are spelled out in the contract. Both borrower and lender have to live with those consequences.

July 17, 2009 at 8:06 AM in reply to: Ethical considerations (none) for defaulting on non-recourse loan. #432836ParticipantGreat post analyst.

When homebuyers and lenders enter into mortgage contracts, each side takes on risks. Included in the risk that the lender assumes, is that the collateral will maintain value in excess of the loan amount. When that doesn’t happen and a homeowner continues to make payments, for whatever reason, they are performing above and beyond the implied expectations of the contract.

I find it no more immoral for borrowers to stop paying in these circumstances than for the lender to foreclose. (Actually, I don’t think ethics or morals should even be a consideration. Lender corporations, despite the courts treatment of them as a “person”, rarely act out of ethical or moral considerations. They act based of legal considerations.)

Things get a little bit dicier for recourse loans, risks are greater for the borrrower, more options exist for the lender. But morals and ethics still don’t come into play in any greater degree. Risks are still taken by the lender. And the legal consequences of failing to pay are spelled out in the contract. Both borrower and lender have to live with those consequences.

July 17, 2009 at 8:06 AM in reply to: Ethical considerations (none) for defaulting on non-recourse loan. #432906ParticipantGreat post analyst.

When homebuyers and lenders enter into mortgage contracts, each side takes on risks. Included in the risk that the lender assumes, is that the collateral will maintain value in excess of the loan amount. When that doesn’t happen and a homeowner continues to make payments, for whatever reason, they are performing above and beyond the implied expectations of the contract.

I find it no more immoral for borrowers to stop paying in these circumstances than for the lender to foreclose. (Actually, I don’t think ethics or morals should even be a consideration. Lender corporations, despite the courts treatment of them as a “person”, rarely act out of ethical or moral considerations. They act based of legal considerations.)

Things get a little bit dicier for recourse loans, risks are greater for the borrrower, more options exist for the lender. But morals and ethics still don’t come into play in any greater degree. Risks are still taken by the lender. And the legal consequences of failing to pay are spelled out in the contract. Both borrower and lender have to live with those consequences.

July 17, 2009 at 8:06 AM in reply to: Ethical considerations (none) for defaulting on non-recourse loan. #433068ParticipantGreat post analyst.

When homebuyers and lenders enter into mortgage contracts, each side takes on risks. Included in the risk that the lender assumes, is that the collateral will maintain value in excess of the loan amount. When that doesn’t happen and a homeowner continues to make payments, for whatever reason, they are performing above and beyond the implied expectations of the contract.

I find it no more immoral for borrowers to stop paying in these circumstances than for the lender to foreclose. (Actually, I don’t think ethics or morals should even be a consideration. Lender corporations, despite the courts treatment of them as a “person”, rarely act out of ethical or moral considerations. They act based of legal considerations.)

Things get a little bit dicier for recourse loans, risks are greater for the borrrower, more options exist for the lender. But morals and ethics still don’t come into play in any greater degree. Risks are still taken by the lender. And the legal consequences of failing to pay are spelled out in the contract. Both borrower and lender have to live with those consequences.

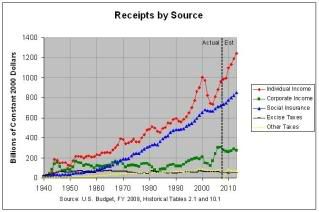

July 16, 2009 at 8:47 PM in reply to: OT- ‘Since when does our great free-market country punish success’… #432049Participant[quote=EconProf]

The clear message: total government revenues collected go UP in the years following the tax cut as the economy expands and people earn more and pay more in our progressive tax rate structure. [/quote]I think that message is far from settled. From US Treasury numbers:

You’ll note that in the years immediately following the Kennedy tax cuts, revenue was relatively flat. In the years following the Reagan tax cuts in 81 and 82, revenues declined, and it took almost 6 years for them to return to levels before the cuts. In the years immediately following the Bush I tax increases, revnues increased. And after a small decline during the recession of the early 90’s, after the Clinton tax increase, revenues sharply increased (as the economy grew at historically high rates). After the Bush II tax cuts, revenues initially fell sharply for 4 years(beginning with the recession of the early part of this decade), and have risen since but still not to the level they were in 2000.

As I said, there is no empirical evidence that tax cuts raise revenues. Historically, that has simply not consistently been the case. Other factors, of course, have been present. The economy is cyclical, and marginal tax rates are not the only factor which drives it. But the perfect model has not been created. At best, supply side theory has provem to be an incomplete model. At worst, a total failure.

-

AuthorPosts