- This topic has 70 replies, 26 voices, and was last updated 12 years, 8 months ago by

CA renter.

-

AuthorPosts

-

May 21, 2013 at 12:25 PM #762146May 22, 2013 at 7:21 PM #762166

kev374

ParticipantThese guys say all is good

May 23, 2013 at 6:05 PM #762183earlyretirement

Participant[quote=SD Realtor]

People thinking there will be big price drops are incorrect. Price drops will be due to inaccurately priced homes that were listed to high to begin with. Once the supply normalizes compared to previous years the only major source for depreciation in San Diego will be due to the lending rates. You may see a small depreciation that will accompany the “normalizing” of the market but that is not a trend setter. The larger declines will be only tied to lending. That will be off in the future, but not in the short term.[/quote]

I agree with you SD Realtor that there shouldn’t be HUGE price drops like back during the Great Recession. People have to understand what we had going on was the “perfect storm” of events all happening at the same time. I still kind of laugh when people try to say that what happened the last time was a normal Recession. That isn’t true.

While I do think prices can dip again, I don’t really see a situation like the last time around where prices fell so precipitously. I do agree that once interest rates go up, prices can depreciate but I don’t see it happening so fast and hard like last time.

Most of the people I know that are looking to buy aren’t buying to “flip”. They want to buy a home to live in to raise their families. I do see more and more inventory coming on the market now so that should help slow things down.

I do NOT think it is healthy to see the drastic price increases so quickly. But still, this time around is totally different vs. the last crash.

[quote=CA renter]

You do not need NINJA loans in order to create a bubble, IMO. You just need a lot of speculative activity where a critical mass of buyers are buying with the expectation that they will sell at some future date for a higher price. I also believe that there is a LOT more leverage in the housing market than people think. Just because they aren’t using traditional purchase mortgages does NOT mean that these buyers are un-leveraged.

FWIW, many homes in our area are being listed at **above-peak** prices, and many are selling for those amounts. This is a bubble as far as I’m concerned.[/quote]

Absolutely I totally agree CAR. You don’t need NINJA loans to create a bubble but it sure does help! LOL. I do agree some people are speculating but I still say this go around is MUCH different vs. the last crash. Today’s buyers are at least “qualified” for the most part. This is FAR different vs. the last time.

Absolutely I do agree with you that there is more leverage in the market than people think but still, it’s nothing compared to during the bubble no-doc stated income years.

I do think prices can dip again but I agree with SD Realtor that I don’t see them crashing like last time. I actually wouldn’t mind seeing things take a break and slow down which we should see from the increased inventory numbers now.

Also, a big part of the real estate market going up is simple the “wealth effect” because people feel wealthier from their stock portfolios going back up. Most people I know right now feel really good with their portfolios having fully recovered for the most part. People just feel richer.

The market can’t keep going up at this pace forever. The Fed has done a number to force people into the stock market. Personally, I’ll be ready to short sell the market again if it continues going up the rest of this year I’ll be ready to short-sell the market again by Thanksgiving.

May 24, 2013 at 12:56 AM #762199CA renter

ParticipantAgree, ER, it’s not as bad as having everyone and their gardener qualify for multiple $500K+ houses without any income or asset documentation. Still, there are too many “investors” in the market, IMHO. Many of them are not the “mom and pop” landlord types who plan to hold onto these homes in retirement.

I just think that high interest rates will not only make traditional, owner-occupier buyers want to pay less, it will also likely draw all of these institutional players out of the housing market. It’s entirely possible that they will want to sell around the same time. Everything I’ve seen and heard shows a 5-7 year disposition plan. What if all of the people behind these investment groups decide to cash in at the same time that interest rates go up?

It just seems like there is an awful lot of leverage still out there, and too much money going after too few investments that offer too-low returns for the risks that lurk when/if something goes wrong.

Of course, I could certainly be wrong about all of it, and we could see long-term massive inflation, instead. It would be nice if the Fed would step back for a bit so that we could all see what the markets would look like without all of the central bank interventions. It’s incredibly distorted right now, IMHO.

May 24, 2013 at 10:10 AM #762203The-Shoveler

ParticipantOK let say the fed takes the foot off the gas,

Who is going to tell china and Japan to do the same ?

China Accounts For Nearly Half Of World’s New Money Supply.

Japan is trying to beat them.

I don’t see the foot coming off the gas anytime soon!!

May 25, 2013 at 1:06 PM #762215curiousmind

ParticipantSoliciting borrowers as an artifice to value. Suckers rally. Who knows what the outcome will be, I think credit will be much more expensive when outlook actually improves.

May 25, 2013 at 6:19 PM #762216spdrun

ParticipantSo I got a condo in SD at a nice short-sale price, about 25-30% below current market. Questions are should I:

(1) Rent it — can easily do an 8.5% cap after repair costs.

(2) Rent it and mortgage it to the tits, attempting to use the extra equity as a down-payment to buy something in NJ, where foreclosure chickens are finally coming home to roost, en masse. Braaak! Braaaak!

(3) Sell it and use the nice profit to buy something bigger and even better cash-flowing on the East Coast.As far as Zimbabwe Ben and friends — asset/stock prices can fall even during a period of QE. Look at Nikkei, down 7.9% on Thursday. Hopefully, US markets will be hit with a similar awesome shock in the next few months. It would be fun to watch, especially from a vantage point in NYC.

May 28, 2013 at 10:46 AM #762252ParticipantThis one in my development listed and went into escrow in only 2 days. 2 DAYS.

http://www.redfin.com/CA/San-Diego/14422-Caminito-Lazanja-92127/home/6462570

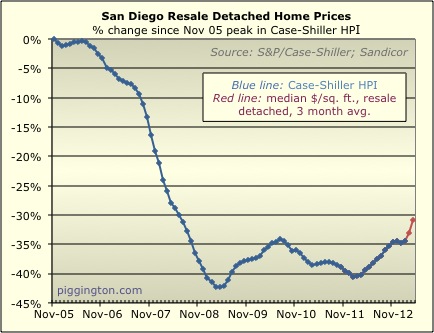

May 29, 2013 at 11:18 PM #762294ParticipantHome prices at 4.5 year high.

http://www.utsandiego.com/news/2013/may/29/tp-home-prices-hit-45-year-high/

May 30, 2013 at 12:50 AM #762296thebazman

Participant[quote=earlyretirement]Home prices at 4.5 year high.

http://www.utsandiego.com/news/2013/may/29/tp-home-prices-hit-45-year-high/%5B/quote%5D

Maybe those people buying at “record highs” from 2003 to 2007 weren’t crazy after all. It’s just like riding out the highs and lows of the stock market. This looks almost the same as what my 401(k) did a few years ago.

I’m being slightly sarcastic, but there might be some truth there if the prices stay on the current trajectory.

Thanks for the link to the article.

May 30, 2013 at 8:50 AM #762299 Rich ToscanoKeymaster

Rich ToscanoKeymaster[quote=thebazman]

Maybe those people buying at “record highs” from 2003 to 2007 weren’t crazy after all. It’s just like riding out the highs and lows of the stock market. This looks almost the same as what my 401(k) did a few years ago.

I’m being slightly sarcastic, but there might be some truth there if the prices stay on the current trajectory.

Thanks for the link to the article.[/quote]

(YMMV for different sub-markets, but that is the aggregate picture)

May 30, 2013 at 8:55 PM #762320ParticipantThank you for the graph, Rich, I guess I had forgotten. It looks like we still have quite a ways to go.

June 3, 2013 at 5:05 PM #762397ParticipantThe median home price in Orange County, California in May 1998 was $221,000, median income was $58,000.

Fast forward to today: Median home price $505,000 and the median income is $71,000.

I will let you look at the two pieces of data above and ask why the price to income was 3.8 in 1998 and why it is 7.1 today? I would like to hear opinions?

My view is that given the current state of the economy, with unemployment high, lower job stability, declining real incomes, higher commodity costs (fuel/food etc.) the sustainable ratio would be closer to 3.5 reflecting a median of around $250,000.

My belief is that a 7.1 ratio is only due to a speculative frenzy fueled by cheap money and investor zeal. These kinds of things are not sustainable long term.

Again, I would like to hear opinions as to why people think that a median price of 7.1 times income is now sustainable long term in an negative economic environment while in the past such a ratio has never been sustainable.

I am looking at solidly blue collar neighborhoods like Buena Park, California where asking prices for entry level single family homes, many of them 30+ year old homes, less than 2000 sqft, are north of $500,000. Are home prices north of half a million dollars in blue collar neighborhoods sustainable? If so, why? The current figures indicate Buena Park has a median income of $58,000 yet has a median home prices of almost 7.2X at $420,000. Realistic? Sustainable?

June 3, 2013 at 9:49 PM #762402bearishgurl

Participant[quote=kev374] . . . I am looking at solidly blue collar neighborhoods like Buena Park, California where asking prices for entry level single family homes, many of them 30+ year old homes, less than 2000 sqft, are north of $500,000. Are home prices north of half a million dollars in blue collar neighborhoods sustainable? If so, why? The current figures indicate Buena Park has a median income of $58,000 yet has a median home prices of almost 7.2X at $420,000. Realistic? Sustainable?[/quote]

kev, it is sustainable and will continue to be sustainable because your “statistics” don’t tell you that the median income includes a very large portion of retirees who paid 1/10th or less of $505K in the 40+ yo areas. But the house they bought THEN is very likely not the same house NOW (which is ostensibly “worth” $450-$525K). It has likely been remodeled one or more times over the years and/or has had many replacements, including the installation of newer, more modern systems.

This is the case in EVERY well-established town and city in CA and the disparity in incomes of adjoining neighbors is more pronounced in coastal counties. It is due to Prop 13 and its progeny, Props 58 and 193, which have a chilling effect on potential listings, leading to higher asking and sold prices. A dearth of listings in the most convenient areas like Buena Park (read: very well-established), along with the historically low fixed mortgage rates of recent years, pushed the prices up to what you see today.

The buyers in Buena Park today making $90K+ are getting a lower fixed interest rate than buyers of any generation before them. Today’s buyers making ~$100K and today’s renters making ~$75K in Buena Park are averaged in with today’s retirees in Buena Park with as low as $15K annual incomes to arrive at that $58-71K median income. Yes, you read this correctly. A retiree owning their own modest home outright in a coastal CA county can actually live on a modest SS income if they don’t use too much water for landscaping, have a ~$400 annual tax bill, have basic cable or “rabbit ears” and have “lifeline utilities.” They may not be able to waste a lot of gas driving around or travel too much, but they can easily live in their home until they become incapacitated or pass away. If that retiree’s partner and co-owner is still alive, their collective monthly SS might be $25K, which would allow them to occasionally travel to visit relatives where they will stay free. These are residents who have little to no other income besides SS and there are many millions of them. A very high proportion of them are homeowners.

In addition, many of these retirees have current annual property-tax bills ranging from $400 to $800 (yes, hundreds).

Thousands of well-established communities in CA have extremely low-income homeowners living a *comparable* lifestyle to their worker-bee neighbors except for the typically newer vehicles and electronics owned by the worker bees. The retired homeowners’ income levels skew the income levels for the community which “seems” to be too high-priced for its “median” income level but it is actually not given the composition of actual wealth (equity) of its longtime residents and current buying conditions.

For example, some of these retirees may have purchased their home new for $33K in 1975 and qualified for it with a $8-$12K annual income at a time when 10% fixed mortgage interest rates prevailed. Everything is relative.

If you haven’t read thru this recent thread, please do. It explains the reasons behind what you are complaining about better than I can:

Monthly Payment Ratios, May 2013: Homes May Not Be Cheap, But Mortgages Sure Are

kev, I really believe you can find a suitable property to buy in the inland OC areas you have been looking in. I don’t think you’ll end up with “buyer’s remorse” for buying in any of the locations you’ve posted about here. Convenience wise and proximity to job centers, it doesn’t get any better, especially in the price range you are shopping in. These are way better-located communities for the money than can be found in established, urban SD at that price point. Have you made any offers yet, and, if so, what was the result?

June 3, 2013 at 10:09 PM #762406Participant[quote=kev374]The median home price in Orange County, California in May 1998 was $221,000, median income was $58,000.

Fast forward to today: Median home price $505,000 and the median income is $71,000.

I will let you look at the two pieces of data above and ask why the price to income was 3.8 in 1998 and why it is 7.1 today? I would like to hear opinions?

My view is that given the current state of the economy, with unemployment high, lower job stability, declining real incomes, higher commodity costs (fuel/food etc.) the sustainable ratio would be closer to 3.5 reflecting a median of around $250,000.

My belief is that a 7.1 ratio is only due to a speculative frenzy fueled by cheap money and investor zeal. These kinds of things are not sustainable long term.

Again, I would like to hear opinions as to why people think that a median price of 7.1 times income is now sustainable long term in an negative economic environment while in the past such a ratio has never been sustainable.

I am looking at solidly blue collar neighborhoods like Buena Park, California where asking prices for entry level single family homes, many of them 30+ year old homes, less than 2000 sqft, are north of $500,000. Are home prices north of half a million dollars in blue collar neighborhoods sustainable? If so, why? The current figures indicate Buena Park has a median income of $58,000 yet has a median home prices of almost 7.2X at $420,000. Realistic? Sustainable?[/quote]

Nope, not sustainable, but likely to last for as long as mortgages are so cheap. IMHO, the credit bubble is alive and well, and asset prices are being grossly distorted as a result.

Stay strong!

-

AuthorPosts

- You must be logged in to reply to this topic.