Due to time constraints I am going to do a graph-only version of the

rodeo this month. Except for this part, I guess.

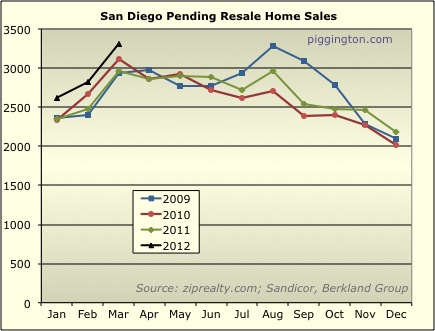

I will quickly note the following:

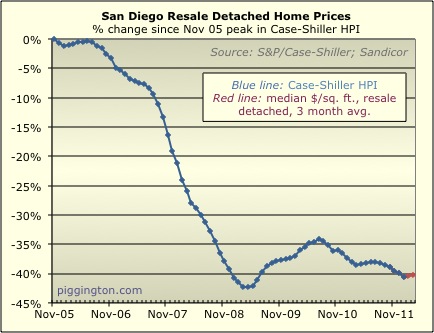

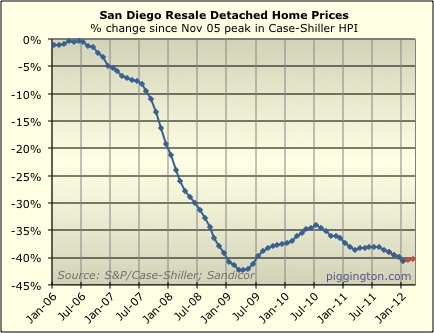

- The median price per square foot did rise last month, as the

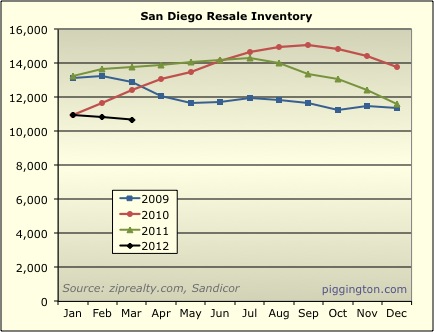

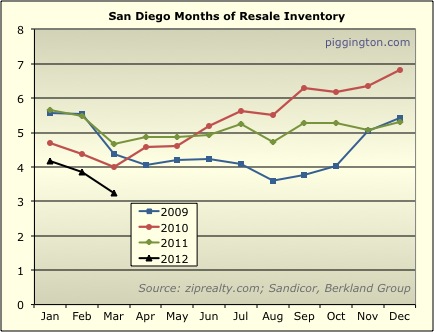

low months-of-inventory figure suggested might happen - Months of inventory (final graph) is 30% lower than last year,

and the lowest it’s been in at least 6 years (as far back as my

data goes for this series) - If the typical historical relationship between months of

inventory and prices is still in place, inventory at these

levels strongly suggests near term price rises - Housing bears please note the use of the phrase “near term”

before flaming me in the comments

I have my cheap BIC lighter

I have my cheap BIC lighter going, can you provide a magnifying glass so I can see how much the MPPSF went up?

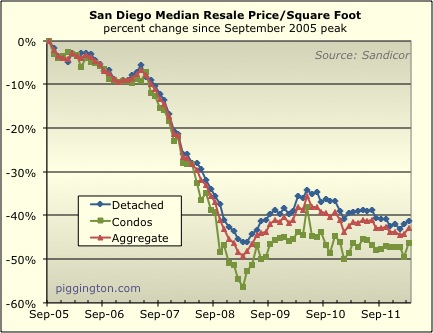

Up 1.5% for detached

Up 6.2%

Up 1.5% for detached

Up 6.2% for condos (not a typo)

Volume-weighted aggregate up 2.8%

PS forgot to update the

PS forgot to update the inventory-vs-price changes chart:

With inventory so low and an

With inventory so low and an (median) uptick in prices, I’d put any plans to buy on the back boiler until things improve. Good time to borrow, bad time to buy.

Funny Jazzman, I’m currently

Funny Jazzman, I’m currently living that statement. After looking around in my hood at condos and even making offers, I realized its not going to happen in the next few months.

If there are real price increases, it seems like they will be short lived. Inventory will increase at some point but I just don’t get the sense that the buyer pool is that deep, except for the cheap seats.

Josh

Lower the interest rate to

Lower the interest rate to the floor and do the same to the inventory…..TPTB are positively brilliant.

I have mixed feelings on

I have mixed feelings on that.

I agree that the instability makes standing back appealing (I certainly would) but I suspect this particular price rise may have more staying power.

The reason I believe this is that this demand increase is underpinned by more cash buyers and sensible leverage.

Same reason I doubt a Chinese housing crash is looming.

That may be less true on the higher end but I can’t say with any real confidence.

Also, the same was somewhat true with the mid-2010 peak (though that was better correlated to specific tax incentives).

What I do know is that the banks and buyers are much more confident at the lower end and that price increases that push above conservative appraisals (at least the ones that I see) are being driven by buyers with more than 20% cash.

That is happening simultaneous with jobs numbers that seem to be on an upward megatrend (broadly defined).

That is (kind of by definition) far less speculative than previous price increases.

However, those components are both minimum, necessary conditions to any future housing inflation.

If we lose jobs or if we lose low-leverage buyers then this price increase just looks like a fleeting jiggle on the graph.

Anyway…my two bits.

And again, a lot of my guide

And again, a lot of my guide here is anecdotal which has more limited utility.