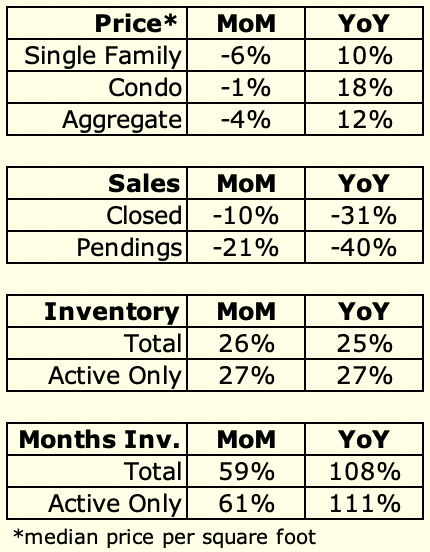

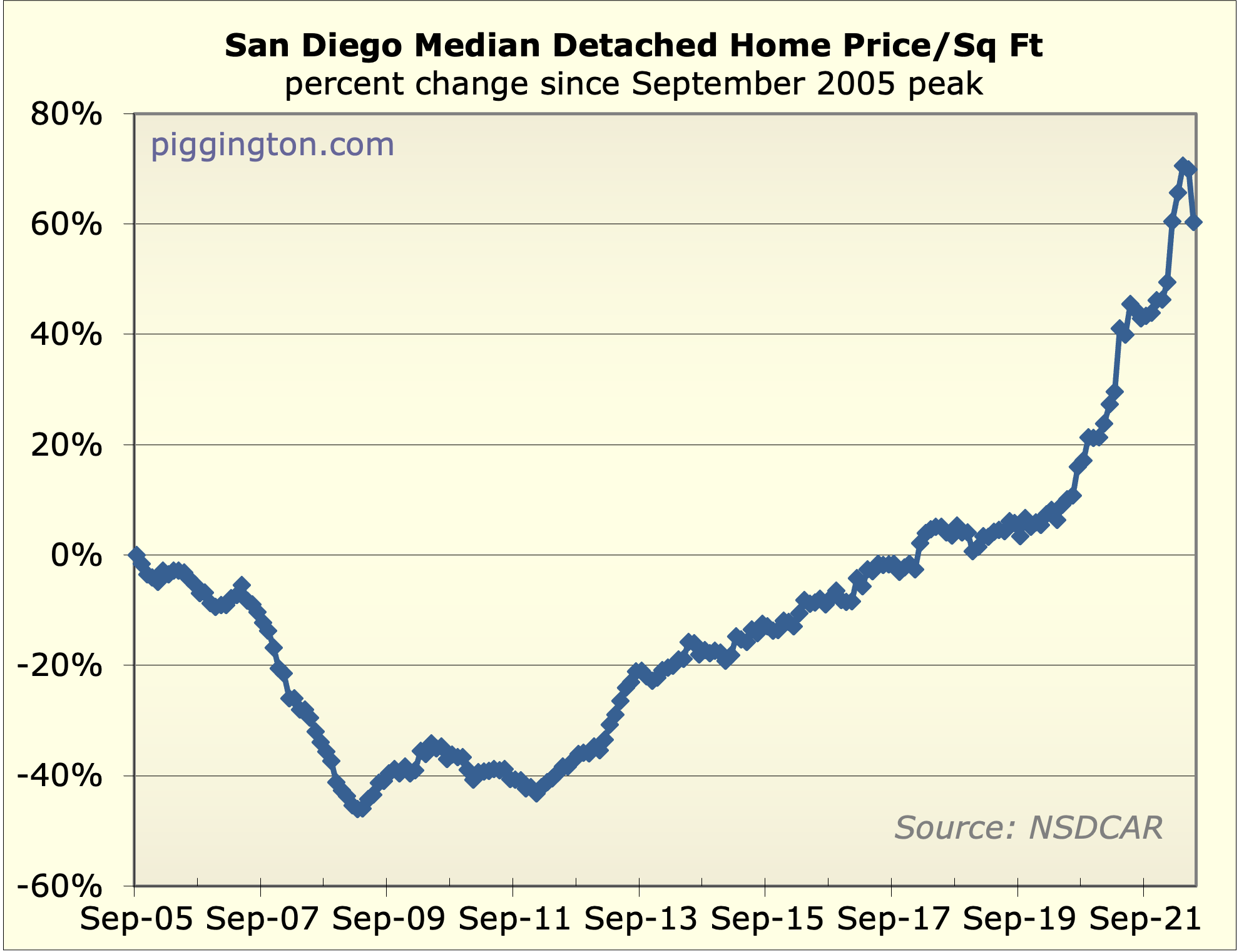

Well… single family home prices look like they dropped a lot last

month, but I suspect there is a lot of noise in that data point. In

specific — the price per square foot was down 5.6% from May. Though

I think current valuations are unsustainable and wouldn’t be

surprised by declining prices, that’s just too big a decline in one

month to be “genuine.”* Supporting this idea is the fact that condos

(usually much more volatile than single family homes) only dropped

1.5% in price/sq ft terms.

*(What I mean by this is, the price per square foot is a pretty

crude proxy for how much a given house has changed in value. It can

get thrown off by compositional effects such as people buying more

low price/sqft homes in cheaper areas, or fewer homes in expensive

areas, etc. This is what I’m talking about when I allude to “noise”

or the decline not being entirely “genuine.”)

So let’s wait for the Case-Shiller index on this one, and in the

meantime say that prices likely dropped last month but not as much

as that stat makes it seem.

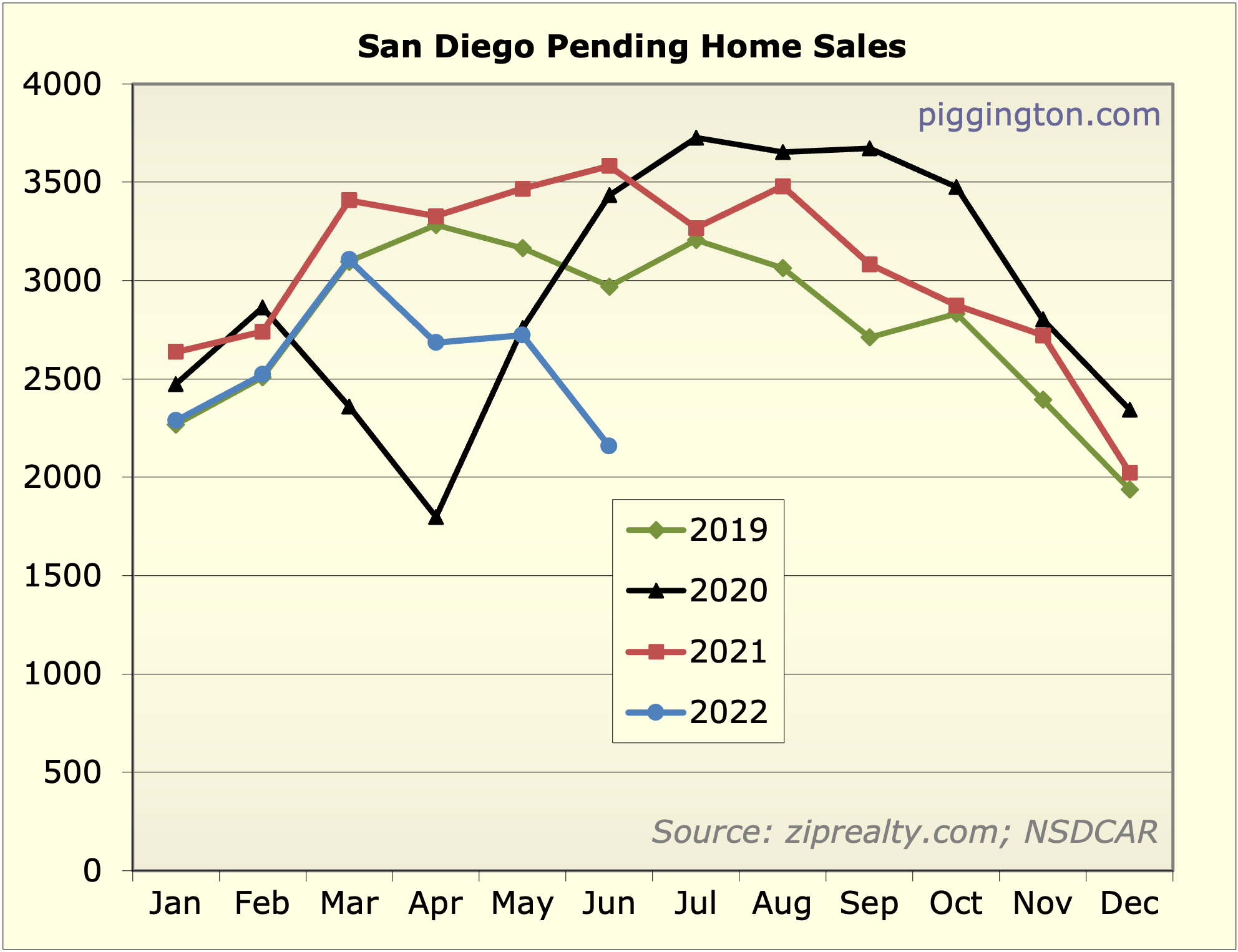

Anyway! Interest rates are biting in other areas too. Here’s pending

sales — down 21% from the prior month, and 40% from a year ago:

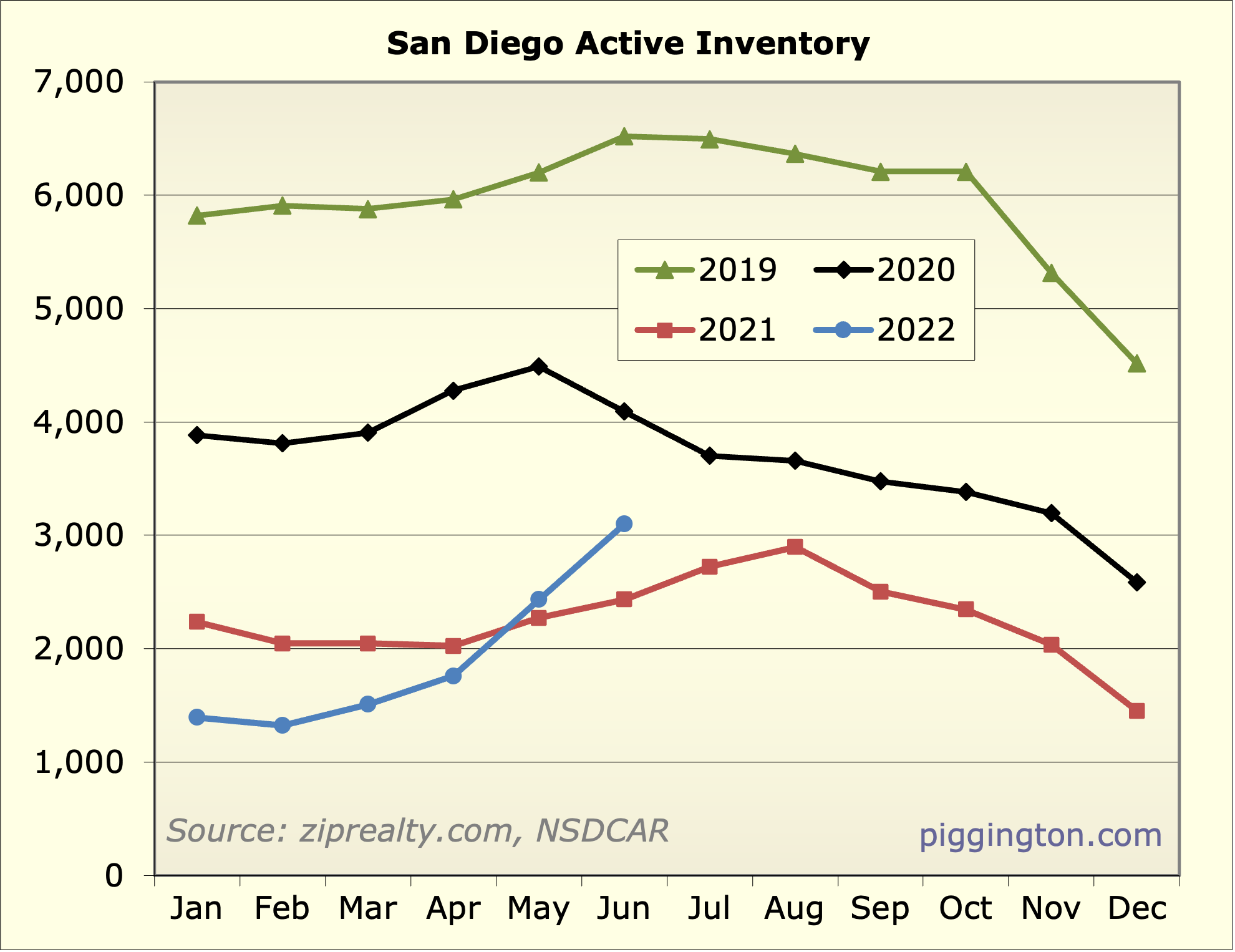

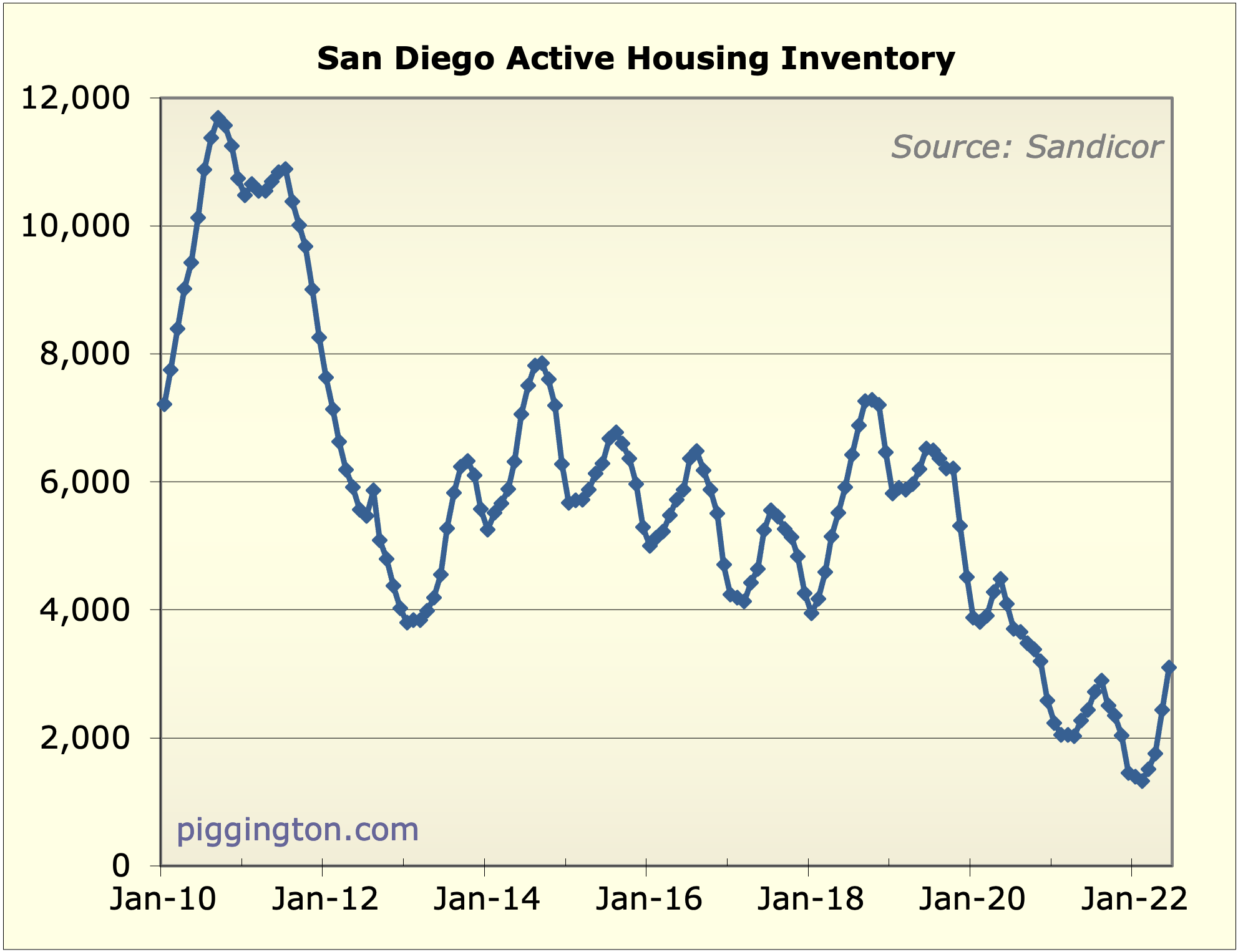

Inventory — up 27% for the month and also (by coincidence) for the

year:

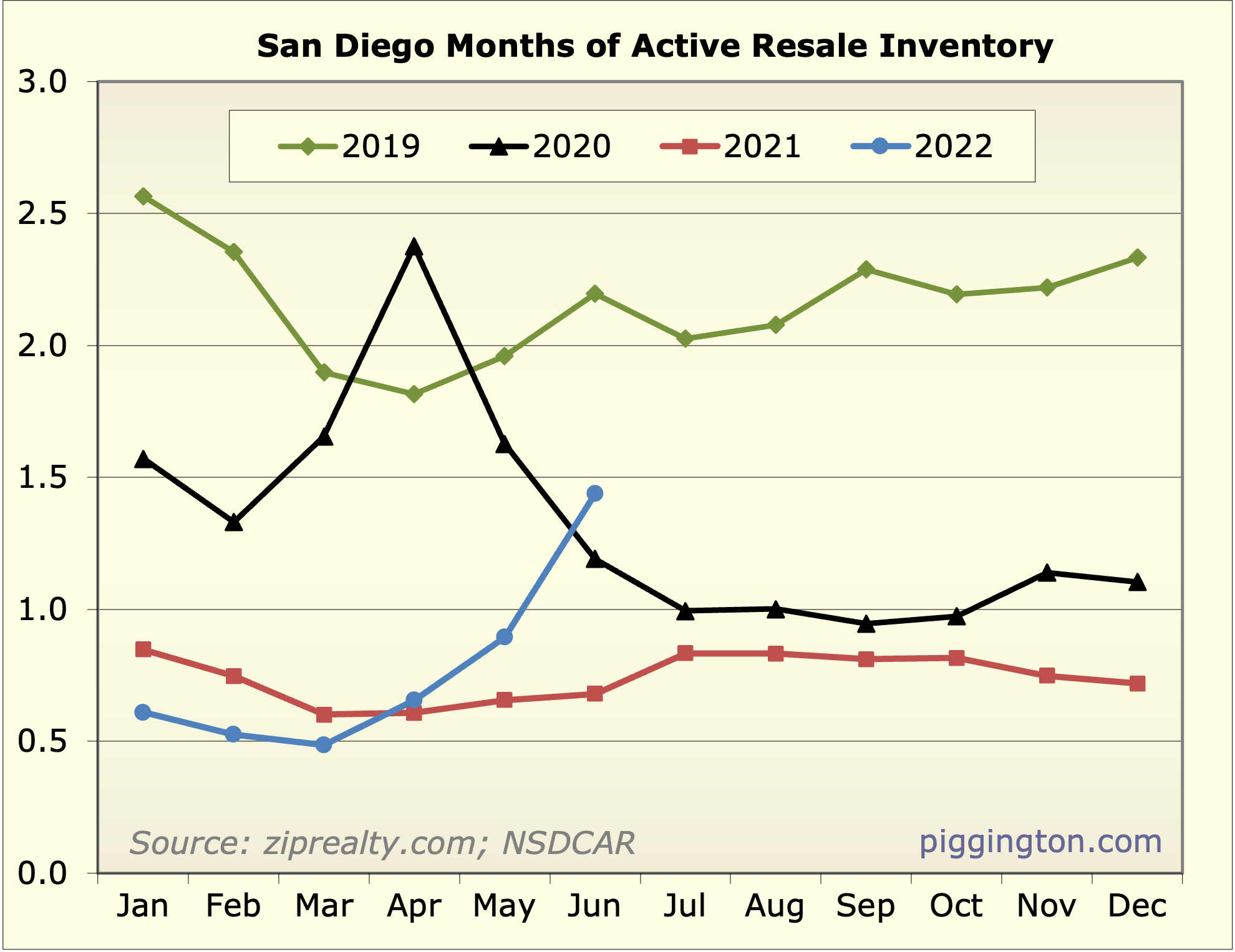

And months of inventory, up 61% for the month and 111% from last

year.

Now those are some pretty eye-popping numbers, but it must be

remembered that months of inventory started out VERY low, so an

increase can be huge in % terms without being all that big in

absolute terms. So, let’s put that into historical perspective:

The increase is quite dramatic, but the absolute level is still on

the low side of the post-crash period. This is actually a fairly

healthy level of inventory. The question is whether that line keeps

moving up. My guess is that, at this combination of prices

and rates, it will.

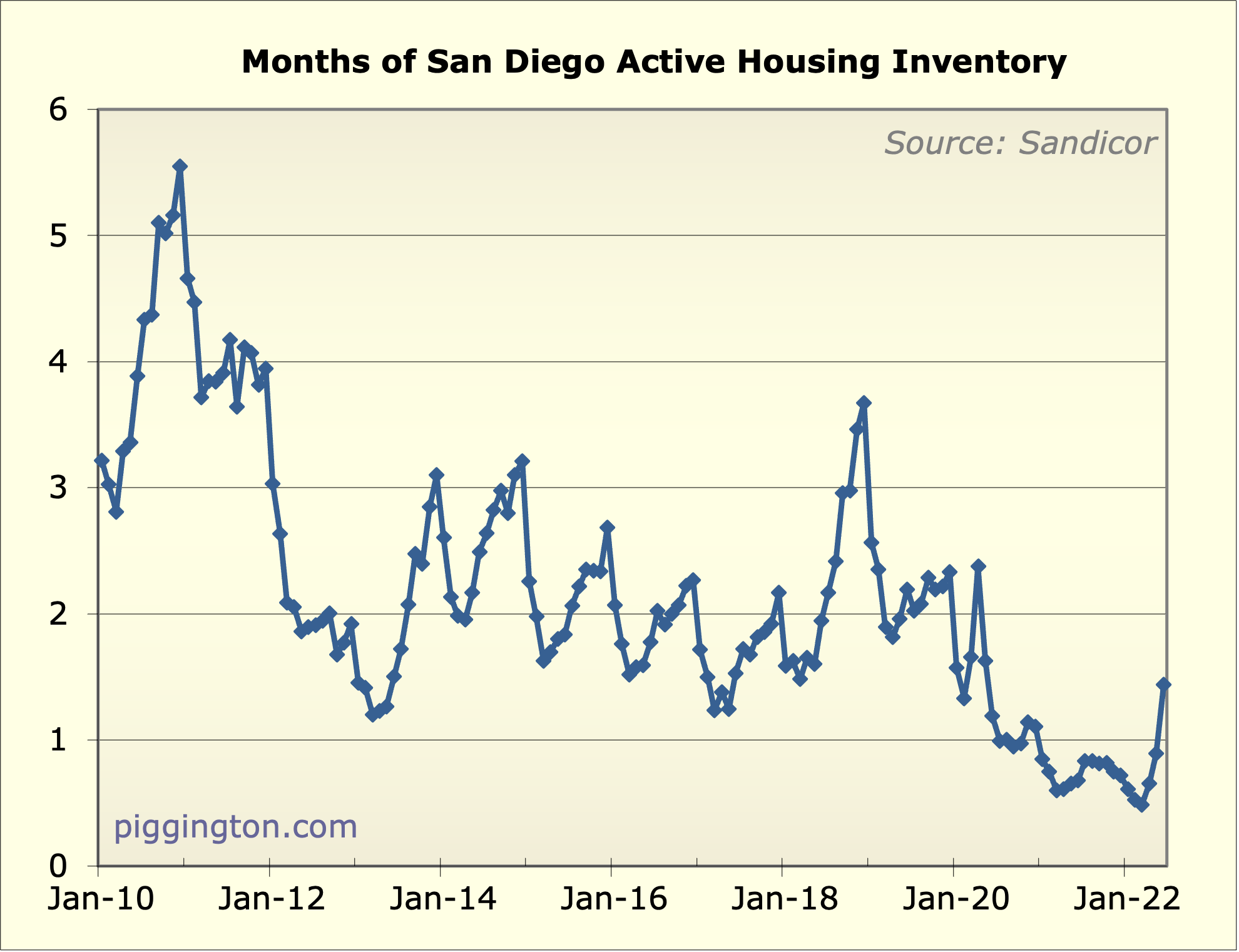

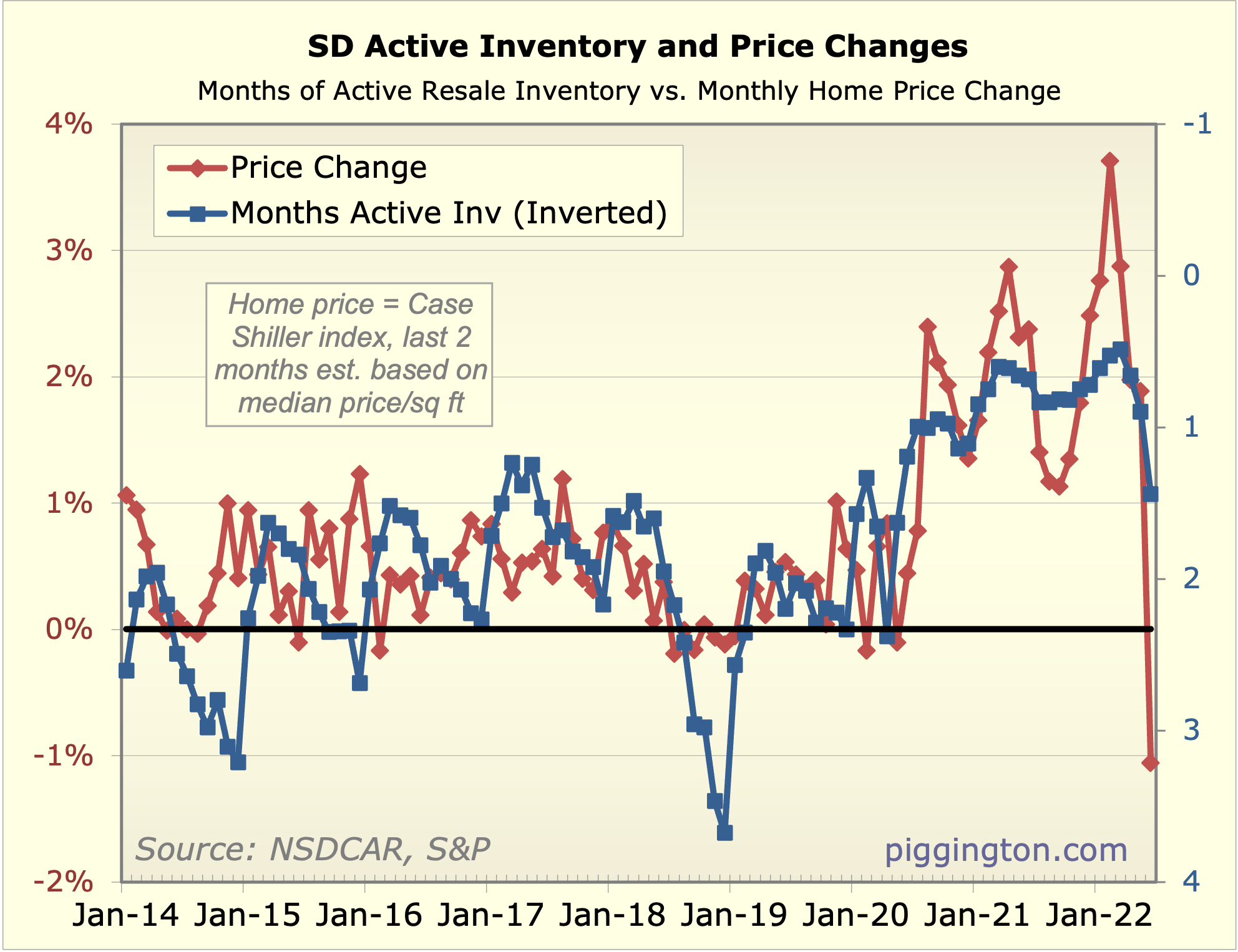

Here’s a look at months of inventory and its impact on prices. In

the graph below, months of inventory is inverted (a lower line means

more inventory) — this is done to accentuate the strong

relationship with price changes, denoted by the red line.

You can see that these have tracked pretty well together for the

most part, until recent months’ wild swings. The abrupt drop in

prices (the red line) last month doesn’t really match up with the

level of inventory (the blue line) is, which is another reason I

suspect that the drop is not totally for real. However, note that in

prior months, prices went up faster than inventory would have

suggested — so we should expect to see some “give-back” as the

market digests the price overshoot.

Back to the main point here… the current level of inventory is on

the low side (high on the graph), but in the range of normalcy and

conducive to higher prices. But this metric has been rising fast,

and if that continues, it’s a bad sign for prices.

Let’s see, what else… hey! Rates came down a bit. Which helps, but

this graph shows that it wasn’t really enough to make a difference.

The inflation-adjusted monthly payment remains near record levels.

And inflation continues to rage, just hitting a new high. This is

negative in terms of its potential rate effects, but positive in the

sense that rising nominal rents and incomes help reduce home

valuations with nominal prices having to decline.

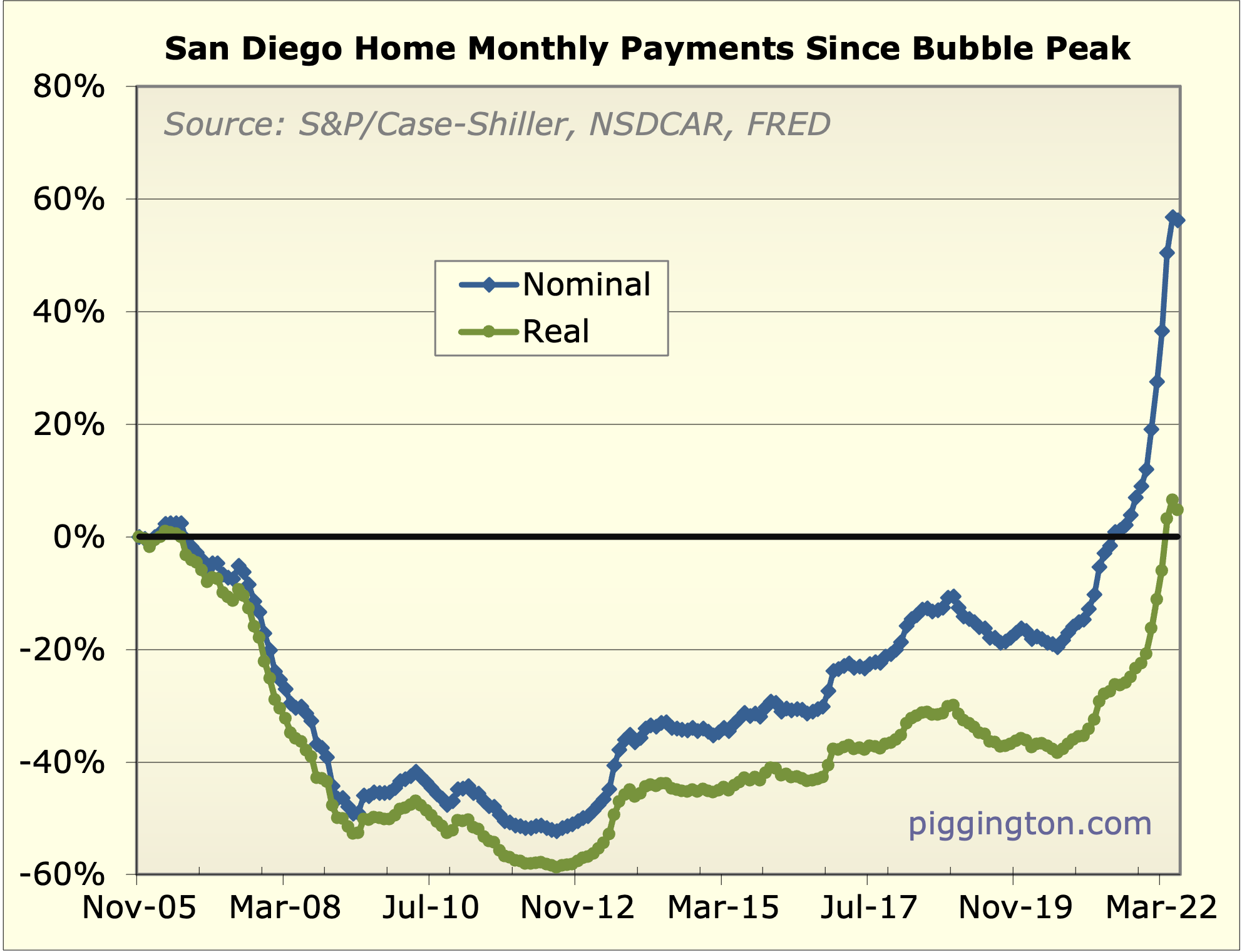

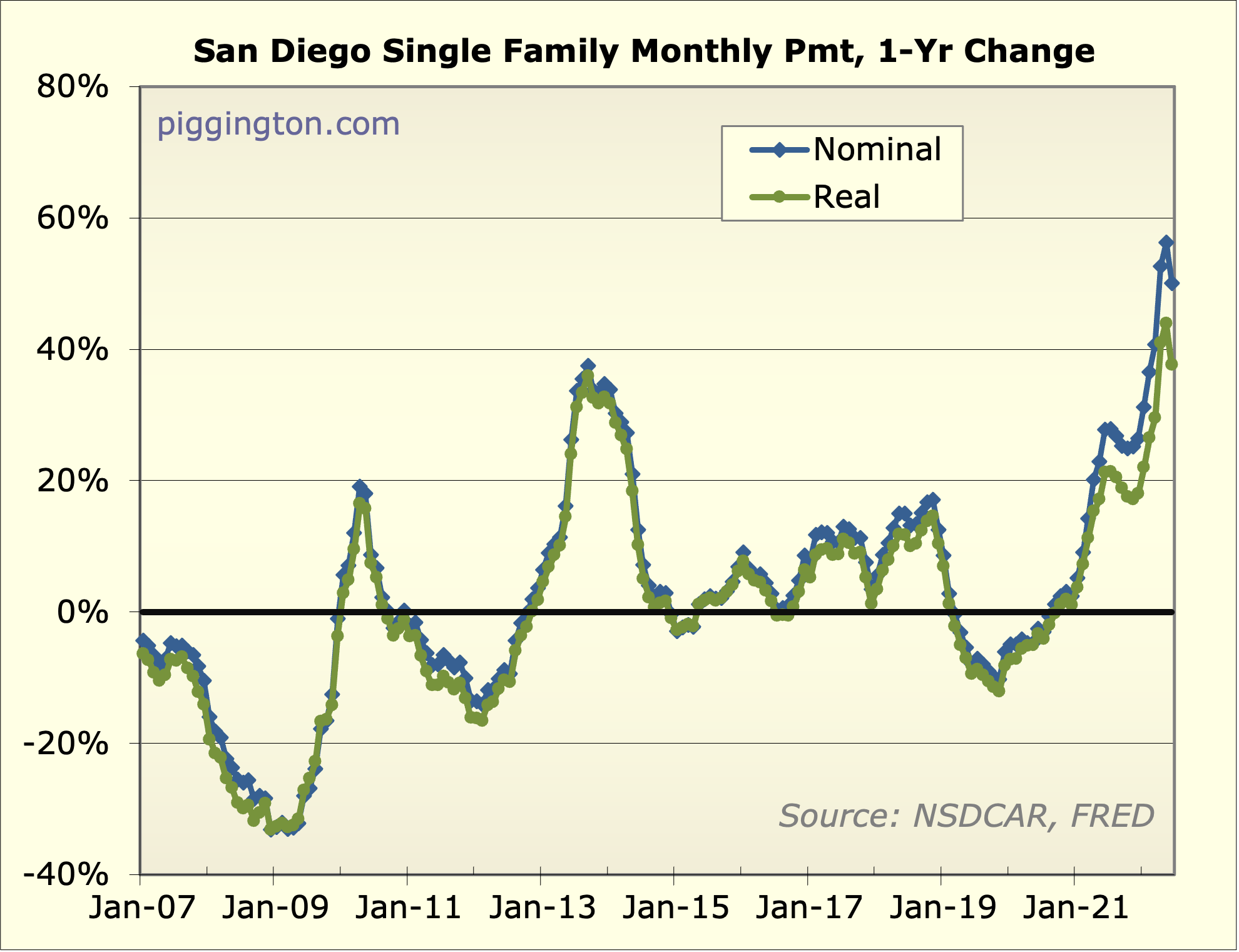

This chart is actually the one that I find nuttiest: combining the

effects of home prices changes, and interest rates, the monthly

payment on the same home has increased by 50% from a year

ago. (If you were lucky enough to have your incomes keep up with

inflation, which the average person has not been, then they are up

“only” 38%).

We did have high-30s percent (real) annual monthly payment increases

in 2013, so it’s not unprecedented. But now go and look at the prior

graph, and you will see that because that surge started from such a

low level, it ended with real monthly payments ~45% below current

levels. So back then, there was a lot of room to grow. Not so much

now.

May you live in interesting times, and all that.

More graphs below.

Rich – thanks for the update!

Rich – thanks for the update! You duplicated the Active Inventory count chart, second one should be months of inventory.

evolusd wrote:Rich – thanks

[quote=evolusd]Rich – thanks for the update! You duplicated the Active Inventory count chart, second one should be months of inventory.[/quote]

Eek! Fixed… thanks for letting me know!

Interesting. I’ve seen

Interesting. I’ve seen support for those kinds of drops some places but not others. Very sporadic how its impacting thus far

sdrealtor wrote:Interesting.

[quote=sdrealtor]Interesting. I’ve seen support for those kinds of drops some places but not others. Very sporadic how its impacting thus far[/quote]

What factors do you think are in play? The single family inventory in Carmel Valley has been doubling every month since March; would you expect more drops in this area?

https://www.sdlookup.com/Market-92130-Carmel-Valley

observer wrote:sdrealtor

[quote=observer][quote=sdrealtor]Interesting. I’ve seen support for those kinds of drops some places but not others. Very sporadic how its impacting thus far[/quote]

What factors do you think are in play? The single family inventory in Carmel Valley has been doubling every month since March; would you expect more drops in this area?

https://www.sdlookup.com/Market-92130-Carmel-Valley%5B/quote%5D

I think saying it’s doubled is a bit misleading as it was coming from an extreme record low. I think it should start leveling soon if historical patterns hold. I also think the last leg up was the result of that record low inventory and will likely go back to where we were about 6-12 months ago. Beyond that I’m a lot less certain

Very nice work, Rich. Yep,

Very nice work, Rich. Yep, times are a changing…

Thanks Rich for the update!

Thanks Rich for the update! After patiently compiling this blog throughout the years, times are finally interesting again! Prices going to soften seems well accepted all around except not yet by sellers. Monthly payment pre-pandemic is probably 70 to 80% as 2020 to 2021 was up a lot too? Since rates pre-pandemic was lower than today, I don’t see how this can be sustainable, unless prices in 2019 was way too cheap or you think rates will fall right back down (neither of which I believe). Maybe how long rates and inflation stay up will determine how severe this drop is? Interesting note is multifamily prices have not dropped much (though REITs have), guess all the MF owners are doesn’t need to sell until their rates reset. If we any get desperate seller to the mix (ie recession/job loss), watch out below for SFR. Am curious Rich what is your base case prediction on how things pan out from here?

Given how high rates have

Given how high rates have gone up. Houses have to go down 40-50% from peak in my area, just so monthly payment can go back to where it was in Winter 2021. This is assuming we’re not seeing another 100 basis points rate increase soon. It’ll be very interesting to see if we’ll see price crash 50% in the next couple of years.

I hope it does.

SD investor wrote:Am curious

[quote=SD investor]Am curious Rich what is your base case prediction on how things pan out from here?[/quote]

I don’t have a base case prediction, but this is what I said the last update:

In all, my view is that something probably has to give here: if rates don’t come down, valuations likely will. (Or some combination of the two).

If that forecast is right, it still leaves open a lot of questions: Will it be rates, valuations, or both? If valuations decline, how much of that will be from nominal price declines vs. incomes catching up to prices? Over what timeline will this all happen? Etc. I don’t pretend to know the answer to any of these. But I do have a pretty strong feeling that this current combination of valuations and mortgage rates cannot be sustained.

Thanks Rich, makes sense.

Thanks Rich, makes sense. Guess how much pain is coming depends on if it is rates or price that comes down. Suppose that is the case for most capital assets. If we are at the beginning of a secular shift/increase interest rates for decades is what I am afraid of but prepared for.

SD investor wrote:Thanks

[quote=SD investor]Thanks Rich, makes sense. Guess how much pain is coming depends on if it is rates or price that comes down. Suppose that is the case for most capital assets. If we are at the beginning of a secular shift/increase interest rates for decades is what I am afraid of but prepared for.[/quote]

If you buy a home to live in long term and you locked in a 30 years mortgage, even if price drop, if the current mortgage payment is still higher than when you bought, would that be considered pain?

Based on current rate, if we don’t see a declining in rates, price would have to drop 30-50% just to have parity in monthly payment as someone who bought in December of 2021. So, if you are living in a place you don’t like, then I guess that would be considered pain. But for those who bought a home and are happy to be in there for the next decade or more, you’re still sitting happy, even if price drop dramatically.

If anything, this might be setting up for another OOAL for those who have the cash to take advantage of a potential massive price drop.

Fed hiked rates in mid March.

Fed hiked rates in mid March. 90 day rate locks expired in mid June. July data will show the full effect of that rate hike.

Fed will likely hike rates again at their next meeting on July 27th. The next month to watch will be November after July’s 90 day rate locks expire.

Today, I’m seeing a number or articles speculating a 100 basis point increase instead of the 75 points predicted earlier this year, and the hike would land during the weakest time of the year for sellers. With inflation at 9.1% for June, there’s a decent chance that 100 point increase materializes.

JPJones wrote:Fed hiked rates

[quote=JPJones]Fed hiked rates in mid March. 90 day rate locks expired in mid June. July data will show the full effect of that rate hike.

Fed will likely hike rates again at their next meeting on July 27th. The next month to watch will be November after July’s 90 day rate locks expire.

Today, I’m seeing a number or articles speculating a 100 basis point increase instead of the 75 points predicted earlier this year, and the hike would land during the weakest time of the year for sellers. With inflation at 9.1% for June, there’s a decent chance that 100 point increase materializes.[/quote]

The Fed funds rate isn’t the driver here though; it’s the mortgage rate, and there haven’t been discreet jumps in that. See https://fred.stlouisfed.org/series/MORTGAGE30US/ – it was a steady uptrend from the start of the year thru april, and then a bouncier/milder uptrend since then. So I don’t think the timing of Fed moves vs. rate locks is all that meaningful here.

However, your point on rate locks is interesting… if indeed 90 days is the norm, then the end of that initial straight-line runup (which ended early may) will happen in august.

Rich Toscano wrote:JPJones

[quote=Rich Toscano][quote=JPJones]Fed hiked rates in mid March. 90 day rate locks expired in mid June. July data will show the full effect of that rate hike.

Fed will likely hike rates again at their next meeting on July 27th. The next month to watch will be November after July’s 90 day rate locks expire.

Today, I’m seeing a number or articles speculating a 100 basis point increase instead of the 75 points predicted earlier this year, and the hike would land during the weakest time of the year for sellers. With inflation at 9.1% for June, there’s a decent chance that 100 point increase materializes.[/quote]

The Fed funds rate isn’t the driver here though; it’s the mortgage rate, and there haven’t been discreet jumps in that. See https://fred.stlouisfed.org/series/MORTGAGE30US/ – it was a steady uptrend from the start of the year thru april, and then a bouncier/milder uptrend since then. So I don’t think the timing of Fed moves vs. rate locks is all that meaningful here.

However, your point on rate locks is interesting… if indeed 90 days is the norm, then the end of that initial straight-line runup (which ended early may) will happen in august.[/quote]

This is probably my inexperience showing through here, but aren’t mortgage rates tied at least loosely to the fed rate? It seemed to me that as soon as the fed rate changes are made official, mortgage rates move accordingly around the same time in a way similar to how gas prices follow the price of oil (oil up, immediate increase; oil down, gradual decrease)

Someone else will have to speak more definitively to the 90 day rate locks. That was my and my friends’ experiences buying our homes over the past 12 years or so. The pre-qualification papers always listed the approved rate as valid for up to 90 days, so I’ve been using that as my indicator of roughly when a rate hike would potentially affect mortgage rates.

The prequal papers say the

The prequal papers say the pre approval is good for 90 days but that is not a rate lock it’s an informal statement that the buyer has been partially vetted based upon a set of assumptions but it’s pretty worthless. Most rate locks are 30 days or less too my knowledge but a lender can correct me if I’m not correct. When you lock you give a credit card and pay a fee to commit to that mortgage

sdrealtor wrote:The prequal

[quote=sdrealtor]The prequal papers say the pre approval is good for 90 days but that is not a rate lock it’s an informal statement that the buyer has been partially vetted based upon a set of assumptions but it’s pretty worthless. Most rate locks are 30 days or less too my knowledge but a lender can correct me if I’m not correct. When you lock you give a credit card and pay a fee to commit to that mortgage[/quote]

My bad. I misspoke. I meant pre-approval, not pre-qualification. I didn’t even know there was a different until I did a few google searches. According to The Internet, pre-approval rate locks are typically 90-120 days, but we were only ever offered 90 days.

FWIW most letters State the

FWIW most letters State the pre approval is good for that long based upon an assumed interest rate. I’m not so sure that is an actual rate lock which is not typically done until a property is in escrow and a payment is made for that lock. Would love to see an actual lender comment as they would know for sure

“ but aren’t mortgage rates

“ but aren’t mortgage rates tied at least loosely to the fed rate?”

The fed only officially sets short term rates, which are not much tied to mortgage rates. The traditional 30-year mortgage rate is most correlated to the 10-year treasury rate. The reason it is the 10 year and not the 30 year bond is that 30 year mortgages in reality last closer to 10 years because of prepayments. And even when they are held to the end, they are heavily paid off by year 20. So the economic meat of a 30 year mortgage is closer to a 10 year federal bond than the 30 year federal bond, which is also different because its principal doesn’t amortize.

Again speaking loosely, the ten year bond approximates the market’s expectations of what the short-term rate set by the fed will average over the next ten years. So that’s what feeds mortgage rates the most.

One reason that the expected next fed funds hike of 0.75 will have little to no impact on the mortgage rate is that the market expects a recession next year to cause the fed to lower rates, and then for them to stay low-ish as inflation recedes.

gzz wrote:“ but aren’t

[quote=gzz]“ but aren’t mortgage rates tied at least loosely to the fed rate?”

The fed only officially sets short term rates, which are not much tied to mortgage rates. The traditional 30-year mortgage rate is most correlated to the 10-year treasury rate. The reason it is the 10 year and not the 30 year bond is that 30 year mortgages in reality last closer to 10 years because of prepayments. And even when they are held to the end, they are heavily paid off by year 20. So the economic meat of a 30 year mortgage is closer to a 10 year federal bond than the 30 year federal bond, which is also different because its principal doesn’t amortize.

Again speaking loosely, the ten year bond approximates the market’s expectations of what the short-term rate set by the fed will average over the next ten years. So that’s what feeds mortgage rates the most.

One reason that the expected next fed funds hike of 0.75 will have little to no impact on the mortgage rate is that the market expects a recession next year to cause the fed to lower rates, and then for them to stay low-ish as inflation recedes.[/quote]

That midde bit is the explanation I was missing. It explains why the gas vs oil price analogy fits so well. I disagree with the last paragraph, though, for the same reason that oil companies will use any excuse they can to raise gas prices immediately but always drag their feet on reductions. I looked up charts for the fed rate and mortgage rates back to the 70s and the behavior matches.

90-day locks you have to pay

90-day locks you have to pay extra for. I have never done one that long in many purchases and refis.

While I am sure they exist, I don’t think they are driving the market.

Rich, congrats on your quotes

Rich, congrats on your quotes in yesterday’s Union-Tribune article on falling home prices here in San Diego:

https://www.sandiegouniontribune.com/business/story/2022-07-19/san-diego-home-price-drops

Great to see, and I hope they regularly check in with you as folks navigate these tricky waters we are now in.

Me, I see a waterfall up ahead, just like the one we fell over back in ’06-’09…

FWIW I came across as more

FWIW I came across as more bearish in that article than I actually I am.

Re SF, I don’t see it as a harbinger for SD. First, the remote work thing is bad for SF, and good for SD. I can’t quantify how big a factor that is, but whatever it is, SF and SD have the opposite sign.

Second, the (imo) bursting growth stock bubble will hit SF a lot harder. Growth stocks and tech stocks aren’t the same thing, but there is a substantial overlap, and SF is much more dependent on the tech industry.

I presume that the Bay Area

I presume that the Bay Area is a harbinger of what we will see here in SoCal and San Diego. Areas within the Bay Area are now seeing drops in year-over-year prices:

https://wolfstreet.com/2022/07/19/san-francisco-bay-area-southern-california-home-sales-crater-prices-begin-to-drop-california-pending-sales-collapse-40/

You may be right, that there

You may be right, that there are probably important differences between the SD and SF economies, such as economic activity from technology vs. defense, attractiveness of work from home, etc.

But, over the last 25 years, the timing, slope, and magnitude of the ups — and downs — in housing prices are remarkably similar:

[img_assist|nid=27704|title=|desc=|link=node|align=center|width=518|height=200]

Maybe the differences between SD and SF will show themselves in this now-underway downturn in home prices. Or, maybe those differences will be swamped by the negative effects from shared factors, such as rising interest rates, sky-high price-to-income ratios, slowing in the national economy, etc.

Yes, it is going to be an ‘interesting’ next three-to-five years, for sure.

Would be interesting to see

Would be interesting to see the % down payment between SF vs SD and DTI.

Interesting data point on

Interesting data point on Sunday from ZeroHedge (ZH), that California tax receipts from personal withholding and estimated tax payments were 20% lower in June than they were one year ago:

https://www.zerohedge.com/personal-finance/california-recession-incoming

I went to the Dept. of Finance (DOF) website and analyzed 18 months of tax receipt data. It appears that the downturn, year-over-year, in personal withholding and estimated tax payments, started in April, and continued in May and June.

On the other hand, sales and use tax and corporate tax payments are still running above last year’s collections.

Also, the DOF just announced, and ZH reported, that real GDP (i.e., adjusted down for inflation) contracted 1.0% in Q1 22.

It seems like we may have crested the peak on the economic roller coaster ride here in California, and the front car has just begun to inch its way down.

Authored by John Seiler via

Authored by John Seiler via The Epoch Times

Just wondering if it’s your article?

I am a different John S.,

I am a different John S., born760. I have no blog and do not write articles, and am just a simple local fellow avidly following SD residential real estate at the behest of my wife.