Forum Replies Created

-

AuthorPosts

-

Rich ToscanoKeymaster

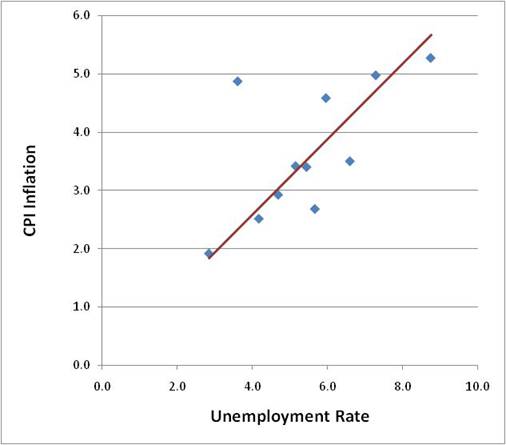

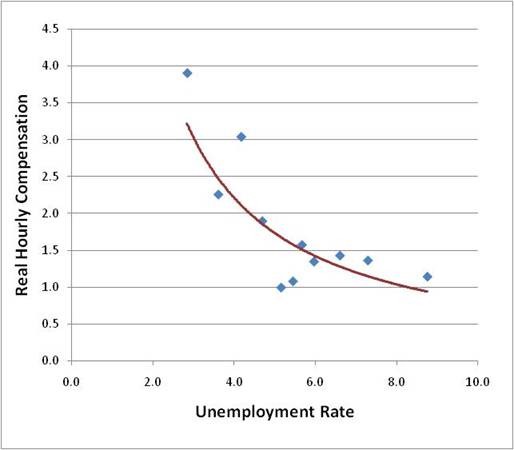

Rich ToscanoKeymasterActually the Hussman article from which I quoted has more good stuff, including some graphs… whole thing is here but this (along with what I quoted above) is the meat:

The charts below are based on data since 1947. Monthly unemployment rates were sorted from highest to lowest, divided into equal groups, and the average unemployment rate and year-over-year CPI inflation rate were plotted for each group. What we observe in the data is strikingly opposite to the standard (mis)interpretation of the Phillips Curve. Indeed, higher unemployment is generally associated with higher, not lower general price inflation.

Contrast this with what I would assert is the real Phillips curve, which is simply a statement about labor scarcity. It says, in a very unadorned way, that when labor is scarce (low unemployment), the price of labor tends to rise relative to the price of other things (thus we observe real wage inflation). In contrast, when labor is plentiful (high unemployment), the price of labor tends to stagnate relative to the price of other things (real wages stagnate). Since productivity growth tends to be positive over time, it turns out that real wages actually fall on a productivity-adjusted basis when unemployment is high. From this perspective, it is no surprise that real wages fell by 1.6% in 2009, even as reported productivity grew.

Rich ToscanoKeymaster

Rich ToscanoKeymasterActually the Hussman article from which I quoted has more good stuff, including some graphs… whole thing is here but this (along with what I quoted above) is the meat:

The charts below are based on data since 1947. Monthly unemployment rates were sorted from highest to lowest, divided into equal groups, and the average unemployment rate and year-over-year CPI inflation rate were plotted for each group. What we observe in the data is strikingly opposite to the standard (mis)interpretation of the Phillips Curve. Indeed, higher unemployment is generally associated with higher, not lower general price inflation.

Contrast this with what I would assert is the real Phillips curve, which is simply a statement about labor scarcity. It says, in a very unadorned way, that when labor is scarce (low unemployment), the price of labor tends to rise relative to the price of other things (thus we observe real wage inflation). In contrast, when labor is plentiful (high unemployment), the price of labor tends to stagnate relative to the price of other things (real wages stagnate). Since productivity growth tends to be positive over time, it turns out that real wages actually fall on a productivity-adjusted basis when unemployment is high. From this perspective, it is no surprise that real wages fell by 1.6% in 2009, even as reported productivity grew.

Rich ToscanoKeymasterActually the Hussman article from which I quoted has more good stuff, including some graphs… whole thing is here but this (along with what I quoted above) is the meat:

The charts below are based on data since 1947. Monthly unemployment rates were sorted from highest to lowest, divided into equal groups, and the average unemployment rate and year-over-year CPI inflation rate were plotted for each group. What we observe in the data is strikingly opposite to the standard (mis)interpretation of the Phillips Curve. Indeed, higher unemployment is generally associated with higher, not lower general price inflation.

Contrast this with what I would assert is the real Phillips curve, which is simply a statement about labor scarcity. It says, in a very unadorned way, that when labor is scarce (low unemployment), the price of labor tends to rise relative to the price of other things (thus we observe real wage inflation). In contrast, when labor is plentiful (high unemployment), the price of labor tends to stagnate relative to the price of other things (real wages stagnate). Since productivity growth tends to be positive over time, it turns out that real wages actually fall on a productivity-adjusted basis when unemployment is high. From this perspective, it is no surprise that real wages fell by 1.6% in 2009, even as reported productivity grew.

Rich ToscanoKeymasterAs far as slack and all that goes, I agree with John Hussman’s view:

“The Phillips Curve is simply a standard economic argument about relative scarcity. It says that when the labor markets are tight, nominal wages rise faster than the rate of general inflation (i.e. real wages rise), and when unemployment is high, nominal wages rise slower than the rate of general inflation (i.e. real wages fall). As we observed in the 1970’s, high unemployment can exist in concert with high rates of inflation. All that happens, in that case, is that wages tend to rise slower than prices. Assuming labor productivity is growing as well, real wages don’t keep pace with productivity growth. In any event, unemployment emphatically does not prevent the inflationary consequences of reckless creation of government liabilities.”

Rich ToscanoKeymasterAs far as slack and all that goes, I agree with John Hussman’s view:

“The Phillips Curve is simply a standard economic argument about relative scarcity. It says that when the labor markets are tight, nominal wages rise faster than the rate of general inflation (i.e. real wages rise), and when unemployment is high, nominal wages rise slower than the rate of general inflation (i.e. real wages fall). As we observed in the 1970’s, high unemployment can exist in concert with high rates of inflation. All that happens, in that case, is that wages tend to rise slower than prices. Assuming labor productivity is growing as well, real wages don’t keep pace with productivity growth. In any event, unemployment emphatically does not prevent the inflationary consequences of reckless creation of government liabilities.”

Rich ToscanoKeymasterAs far as slack and all that goes, I agree with John Hussman’s view:

“The Phillips Curve is simply a standard economic argument about relative scarcity. It says that when the labor markets are tight, nominal wages rise faster than the rate of general inflation (i.e. real wages rise), and when unemployment is high, nominal wages rise slower than the rate of general inflation (i.e. real wages fall). As we observed in the 1970’s, high unemployment can exist in concert with high rates of inflation. All that happens, in that case, is that wages tend to rise slower than prices. Assuming labor productivity is growing as well, real wages don’t keep pace with productivity growth. In any event, unemployment emphatically does not prevent the inflationary consequences of reckless creation of government liabilities.”

Rich ToscanoKeymasterAs far as slack and all that goes, I agree with John Hussman’s view:

“The Phillips Curve is simply a standard economic argument about relative scarcity. It says that when the labor markets are tight, nominal wages rise faster than the rate of general inflation (i.e. real wages rise), and when unemployment is high, nominal wages rise slower than the rate of general inflation (i.e. real wages fall). As we observed in the 1970’s, high unemployment can exist in concert with high rates of inflation. All that happens, in that case, is that wages tend to rise slower than prices. Assuming labor productivity is growing as well, real wages don’t keep pace with productivity growth. In any event, unemployment emphatically does not prevent the inflationary consequences of reckless creation of government liabilities.”

Rich ToscanoKeymasterAs far as slack and all that goes, I agree with John Hussman’s view:

“The Phillips Curve is simply a standard economic argument about relative scarcity. It says that when the labor markets are tight, nominal wages rise faster than the rate of general inflation (i.e. real wages rise), and when unemployment is high, nominal wages rise slower than the rate of general inflation (i.e. real wages fall). As we observed in the 1970’s, high unemployment can exist in concert with high rates of inflation. All that happens, in that case, is that wages tend to rise slower than prices. Assuming labor productivity is growing as well, real wages don’t keep pace with productivity growth. In any event, unemployment emphatically does not prevent the inflationary consequences of reckless creation of government liabilities.”

Rich ToscanoKeymasterNot a mortgage expert but as far as I know, HELOCs are always variable while some reverse mortgages are fixed. This is a huge difference IMHO as the latter protect you from the risk of increasing interest rates.

Rich ToscanoKeymasterNot a mortgage expert but as far as I know, HELOCs are always variable while some reverse mortgages are fixed. This is a huge difference IMHO as the latter protect you from the risk of increasing interest rates.

Rich ToscanoKeymasterNot a mortgage expert but as far as I know, HELOCs are always variable while some reverse mortgages are fixed. This is a huge difference IMHO as the latter protect you from the risk of increasing interest rates.

Rich ToscanoKeymasterNot a mortgage expert but as far as I know, HELOCs are always variable while some reverse mortgages are fixed. This is a huge difference IMHO as the latter protect you from the risk of increasing interest rates.

Rich ToscanoKeymasterNot a mortgage expert but as far as I know, HELOCs are always variable while some reverse mortgages are fixed. This is a huge difference IMHO as the latter protect you from the risk of increasing interest rates.

Rich ToscanoKeymaster[quote=bearishgurl][quote=LuckyInOC]PS: I just realized the spell checker on this site does not understand ‘affordability’ – kind of ironic when most of the users do…[/quote]

There’s a spell-checker on this site??[/quote]

No… if there’s any spell checking taking place your browser is doing it.

-

AuthorPosts