- This topic has 1,162 replies, 30 voices, and was last updated 5 years, 10 months ago by

Anonymous.

-

AuthorPosts

-

March 8, 2020 at 3:11 PM #815244March 8, 2020 at 3:46 PM #815245

an

Participant[quote=FlyerInHi]AN, someone cares enough you resurrect this old thread.

He has he benefit of hindsight. He should have known what the bottom was yet he argued that 2012 was not the bottom.The person who wrote the article was accurate in his prediction. Simple.

Maybe you don’t care but that’s besides the point. Ok, you’re successful, you made your own bottom whenever. The bottom was still 2012.[/quote]

It doesn’t matter when the bottom is if there’s nothing you want to buy at the bottom. Also, not all zip code have the same bottom.March 8, 2020 at 3:47 PM #815246FlyerInHi

Guest[quote=DumpsterDiver]

The bottom was simply a moving target. Calling January 2012 the bottom is just a statistical calculation and has nothing to do when was the right time to buy a given house. The house that any particular person wanted was not likely to be available at the exact moment somebody declared a bottom. What matters is buying a house [/quote]Ha! A moving target! We are talking about the economy statistics do matter.

If you’re talking moving target, then the period after the bottom is just as good. You picked 2009-2011, why?

The topic is the economy. Not individual performance. Bottom is still 2012 no matter what you say. The time to argue “moving target” is during, not years later when everything is laid out for you to see.

March 8, 2020 at 3:51 PM #815247Guest[quote=AN][quote=FlyerInHi]

It doesn’t matter when the bottom is if there’s nothing you want to buy at the bottom. Also, not all zip code have the same bottom.[/quote]Read the LA article posted in the header. What you say has no bearing and not the point, especially 10 years later.

March 8, 2020 at 4:17 PM #815249Participant[quote=flu]

So AN, as BG use to say “inquiring minds what know know”!!! Since handing over the title to you as “serial refinancer”……when are you planning to refinance again??? And how much in rebates are you milking this time, lol…You totally killed it with the ridiculously low below monthly loan payments, I’m guessing.As they say in Star Trek. Live long and prosper.[/quote]

I just started 2 more refi on Friday. My primary will be at 3.125% and my SFR rental will be at 3.625% @30 years fixed. Just refi my condo rental 9 months ago @ 4.125% @15 years fixed. I only do either no cost or with extra rebate to cover taxes and insurance. A few years ago, I went several years w/out paying property taxes or insurance, because the refi would cover taxes and insurance for those years.For my primary residence with the new rate, I’ll be paying less on interest + taxes + insurance than a 1/1 condo around here. I can’t believe I’ll be in this position after just 12 years. Sucks for all the new home buyers, but I’m definitely sitting pretty. Especially with minimum wage go to $15/hr. I think it’s getting close to the point where I can afford my house on a minimum wage salary.

With Trump’s new tax plan, I have to readjust my portfolio. But I can’t complain. Thanks to CA’s strict regulations, rent are sky rocketing. Also, w/ the new rent cap, I’m starting to increase rent on my good tenants. I feel bad for them, but I told them, the State twisted my arms on this one, sorry.

Here’s hoping this “pandemic” continue to get overblown and the Fed will cut rate some more. Would be awesome if I can lock in 30 years fixed at <2%.

March 8, 2020 at 4:19 PM #815248Participant[quote=FlyerInHi][quote=AN][quote=FlyerInHi]

It doesn’t matter when the bottom is if there’s nothing you want to buy at the bottom. Also, not all zip code have the same bottom.[/quote]Read the LA article posted in the header. What you say has no bearing and not the point, especially 10 years later.[/quote]Article doesn’t exist anymore. Back when I was young and foolish, I would believe these articles and economists. If I did, I would have lost out on thousands of $ waiting ’til 2012 and not be able to buy the kinds of house in the area I want. Hindsight is awesome and I’m glad I didn’t listen.

So, who really cares when the exact statistical bottom is other than economist and internet armchair economist.

March 8, 2020 at 4:25 PM #815251Guest[quote=AN]

So, who really cares when the exact statistical bottom is other than economist and internet armchair economist.[/quote]

Somebody predicted the bottom right on the money. Maybe you don’t care. But he’s still right.

You’re deflecting and changing the topic. The fact that you did well and “won’” changes nothing. At this point you’re just bragging in a put down attempt that’s all too familiar these days.

March 8, 2020 at 4:27 PM #815252Participant[quote=FlyerInHi][quote=DumpsterDiver]

The bottom was simply a moving target. Calling January 2012 the bottom is just a statistical calculation and has nothing to do when was the right time to buy a given house. The house that any particular person wanted was not likely to be available at the exact moment somebody declared a bottom. What matters is buying a house [/quote]Ha! A moving target! We are talking about the economy statistics do matter.

If you’re talking moving target, then the period after the bottom is just as good. You picked 2009-2011, why?

The topic is the economy. Not individual performance. Bottom is still 2012 no matter what you say. The time to argue “moving target” is during, not years later when everything is laid out for you to see.[/quote]

This is what he said

[quote=Burns]Burns, the economist, believes that the housing market overall is headed back toward 2002 price levels, on grounds that the gains seen over the last year or so will be reversed as a new flood of foreclosures and short sales hit the market.[/quote]

I rather buy a condo in Jan 2009 than Jan 2012.March 8, 2020 at 4:29 PM #815253Participant

I rather buy a condo in Jan 2009 than Jan 2012.March 8, 2020 at 4:29 PM #815253Participant[quote=FlyerInHi][quote=AN]

So, who really cares when the exact statistical bottom is other than economist and internet armchair economist.[/quote]

Somebody predicted the bottom right on the money. Maybe you don’t care. But he’s still right.

You’re deflecting and changing the topic. The fact that you did well and “won’” changes nothing. At this point you’re just bragging in a put down attempt that’s all too familiar these days.[/quote]

Nope Data doesn’t lie.

March 8, 2020 at 5:41 PM #815256Anonymous

GuestExactly early 2009 price level is 20% below late 2012 prices. But in his mind 2012 is somehow the magical bottom! How many did liar revisionist Brian buy?

March 8, 2020 at 6:16 PM #815257 CoronitaParticipant

CoronitaParticipant[quote=AN][quote=flu]

So AN, as BG use to say “inquiring minds what know know”!!! Since handing over the title to you as “serial refinancer”……when are you planning to refinance again??? And how much in rebates are you milking this time, lol…You totally killed it with the ridiculously low below monthly loan payments, I’m guessing.As they say in Star Trek. Live long and prosper.[/quote]

I just started 2 more refi on Friday. My primary will be at 3.125% and my SFR rental will be at 3.625% @30 years fixed. Just refi my condo rental 9 months ago @ 4.125% @15 years fixed. I only do either no cost or with extra rebate to cover taxes and insurance. A few years ago, I went several years w/out paying property taxes or insurance, because the refi would cover taxes and insurance for those years.For my primary residence with the new rate, I’ll be paying less on interest + taxes + insurance than a 1/1 condo around here. I can’t believe I’ll be in this position after just 12 years. Sucks for all the new home buyers, but I’m definitely sitting pretty. Especially with minimum wage go to $15/hr. I think it’s getting close to the point where I can afford my house on a minimum wage salary.

With Trump’s new tax plan, I have to readjust my portfolio. But I can’t complain. Thanks to CA’s strict regulations, rent are sky rocketing. Also, w/ the new rent cap, I’m starting to increase rent on my good tenants. I feel bad for them, but I told them, the State twisted my arms on this one, sorry.

Here’s hoping this “pandemic” continue to get overblown and the Fed will cut rate some more. Would be awesome if I can lock in 30 years fixed at <2%.[/quote]

Great job on the low low loan rates.

Unfortunately,I didn't keep my loans. Drat. I guess I played it too safe. So I'm stuck with very positive cash flow that's sitting in the bank. I'm trying to find another 2 rentals but inventory isnt great, price isn't great... But then again maybe with low rates it might not be a bad option.

Nice job on the refis. Can you PM who you got the loans from. just curious.

March 8, 2020 at 6:28 PM #815258Guest[quote=FlyerInHi]I don’t have time to read old stuff.[/quote]

How did we all miss this gem? You post a few dozen times nearly every single day for over 10 years and you don’t have time to read your old stuff? ROTFLMAO

March 8, 2020 at 7:15 PM #815259Participant[quote=flu][quote=AN][quote=flu]

So AN, as BG use to say “inquiring minds what know know”!!! Since handing over the title to you as “serial refinancer”……when are you planning to refinance again??? And how much in rebates are you milking this time, lol…You totally killed it with the ridiculously low below monthly loan payments, I’m guessing.As they say in Star Trek. Live long and prosper.[/quote]

I just started 2 more refi on Friday. My primary will be at 3.125% and my SFR rental will be at 3.625% @30 years fixed. Just refi my condo rental 9 months ago @ 4.125% @15 years fixed. I only do either no cost or with extra rebate to cover taxes and insurance. A few years ago, I went several years w/out paying property taxes or insurance, because the refi would cover taxes and insurance for those years.For my primary residence with the new rate, I’ll be paying less on interest + taxes + insurance than a 1/1 condo around here. I can’t believe I’ll be in this position after just 12 years. Sucks for all the new home buyers, but I’m definitely sitting pretty. Especially with minimum wage go to $15/hr. I think it’s getting close to the point where I can afford my house on a minimum wage salary.

With Trump’s new tax plan, I have to readjust my portfolio. But I can’t complain. Thanks to CA’s strict regulations, rent are sky rocketing. Also, w/ the new rent cap, I’m starting to increase rent on my good tenants. I feel bad for them, but I told them, the State twisted my arms on this one, sorry.

Here’s hoping this “pandemic” continue to get overblown and the Fed will cut rate some more. Would be awesome if I can lock in 30 years fixed at <2%.[/quote]

Great job on the low low loan rates.

Unfortunately,I didn't keep my loans. Drat. I guess I played it too safe. So I'm stuck with very positive cash flow that's sitting in the bank. I'm trying to find another 2 rentals but inventory isnt great, price isn't great... But then again maybe with low rates it might not be a bad option.

Nice job on the refis. Can you PM who you got the loans from. just curious.[/quote]I think you have to be creative in this environment. SFR + 2 Adu might make sense number wise.

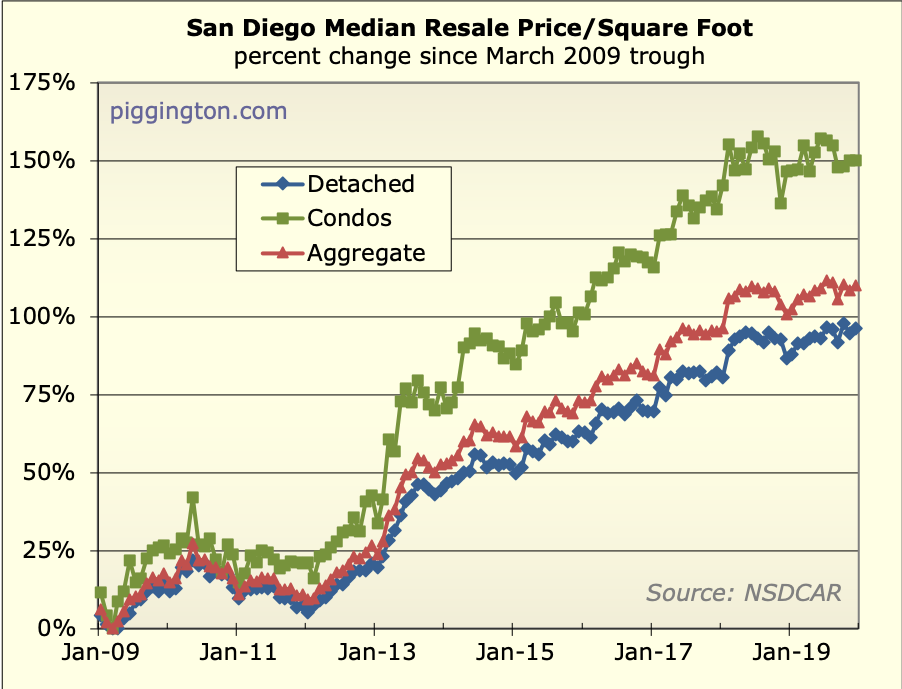

March 8, 2020 at 9:05 PM #815266GuestActually, AN, you’re wrong. You found that chart and you seize on it to prove a point which you rejected earlier.

Case Shiller says the bottom is 2012. Case Shiller adjusts for house quality. If you’d recall, the argument was that the shithole houses would fall first and the more premium houses would fall later.

Hard to believe that some of you want to relitigate something that’s already been settled!

March 8, 2020 at 9:46 PM #815271GuestLet me just put more words into more random people’s mouth.

-

AuthorPosts

- You must be logged in to reply to this topic.