- This topic has 23 replies, 16 voices, and was last updated 19 years, 7 months ago by

powayseller.

-

AuthorPosts

-

June 28, 2006 at 4:47 AM #27492June 28, 2006 at 5:06 AM #27493

powayseller

ParticipantI am sorry I asked anyone how much their home went down last week. That was a horrible thing to say. I’m really sorry.

June 28, 2006 at 6:45 AM #27497PD

ParticipantI think zillow is an excellent tool for the average person. The estimate is usually off but it enables people to see comps in the neighborhood and do their own estimate. If you know the neighborhood and understand which houses have premiums, you can come pretty close to figuring out what the house is worth. I say hurray! for sites like zillow which empower the average person and take the information monopoly away from realtors.

June 28, 2006 at 1:40 PM #27514bubba99

ParticipantAnother worry is the fed funds rate vs the prime rate. Although the prime rate was in the 4 plus percent range, the fed funds rate was 1 percent. Money left in savings accounts did almost nothing. The 1 percent return forced money into the stock market and (you guessed it) housing. Money now has a safe haven at 5% just sitting in a World Savings account. The savings rates will continue to rise as the fed raises interest rates driving more investors out of the volatility of stocks and housing. Leading to a downward “explosion” in the housing market.

I have trouble not seeing a depression like decline in the general economy as housing declines. If borrowing against the house is not available as values decline, where does the money come from to fuel consumer spending?

It is so obvious, one wonders how it will be avoided?

June 28, 2006 at 5:51 PM #27527Participantbubba99- you are so right! Even flat home values will cause a recession, since 70% of GDP is consumer spending, which comes from MEW.

I hope everyone else here gets this point. 70% of GDP is dependent on this one fact: rising home values and borrowers’ ability to borrow it freely to spend.

Flat prices or high interest rates will break the cycle.

What could help: rising wages. This would be possible if we erected trade barriers with low-wage Asian exporters. That strategy would also cause massive inflation, as the low-cost goods they provide has caused deflation in goods.

The key for everyone in this country is to realize that even flat home prices will cause a recession, about 9 months – 18 months after the prices stop rising. It takes consumers 9 months to spend the equity loan, and 9 months for reduced spending to show up in less capital spending and lower stock prices.

By the end of 2007, the full-blown recession will be here.

Can another asset bubble save it? Globally, central banks are tightening and withdrawing liquidity. Even Japan, whichh had 0% interest for decades (I think) is raising interest rates. Even China is raising interest rates and bank reserve requirements to reduce inflation.

The gig is up. Prepare yourselves for a period of saving, possible job loss. Be frugal for the next few years. Then you can handle this recession with less pain.

June 28, 2006 at 6:27 PM #27529carlislematthew

ParticipantWhat is included in the 70%? Food? If so, will people stop buying food when they can no longer refinance and take more money out of their house? Will they stop buying printer paper? Cat litter?

I’m not sure how *much* of the 70% has been funded by MEW (I’m sure it’s a substantial portion), but it’s certainly not all of it and I don’t believe that the entire 70% of GDP is dependant on MEW.

I do however agree with you regarding a recession and your advice regarding being frugal and saving – that’s my plan too. I also feel a recession coming, and have just landed myself a job at a company with money in the bank, a fairly stable outlook, and conservative growth plans. I’m hoping I can weather the storm (however severe or mild it is) and come out the other side with savings intact. If possible, I’m hoping to have the courage to buy a house in the middle of it all!

June 28, 2006 at 9:37 PM #27534North County Jim

ParticipantCM,

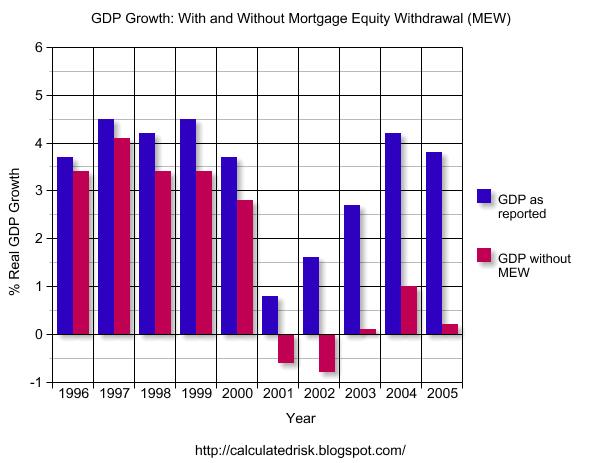

There have been estimates made of the MEW contribution to GDP growth. Here’s a link to a chart from Calculated Risk showing GDP growth with and without MEW.

He used an assumption that 2/3 of MEW flows through to personal consumption.

June 29, 2006 at 12:50 AM #27537masayako

ParticipantFrom the housing bubble burst in Japan the past decade, which is very similar to ours, I think the huge pricing drop is imminent.

June 29, 2006 at 6:01 AM #27546ParticipantI wrote an employment piece a week or so ago. Did anyone read it? I put the employment figures back to pre-MEW times, so the year 2001.

Spending will drop in the categories mentioned in that story I wrote: retail, construction, restaurant. People will cut back at least 75% (a guess) on remodeling, shopping at Home Depot/Ethan Allen, buying new cars, jewelry, boats, ATVs, iPods, clothes, take fewer trips/meals out, and so on.

You listed consumer staples, but those things will not go away. Those are cheap things that everyone needs.And read the CR thread from above.

-

AuthorPosts

{kind=link}

- You must be logged in to reply to this topic.