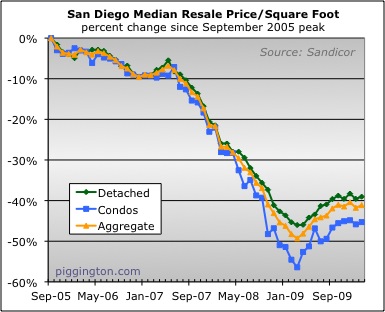

The median price per square foot was up about 1% in February, but

that’s a smaller amount that its January decline. So I would

characterize prices by this measure as continuing to go nowhere, as

they have done since September.

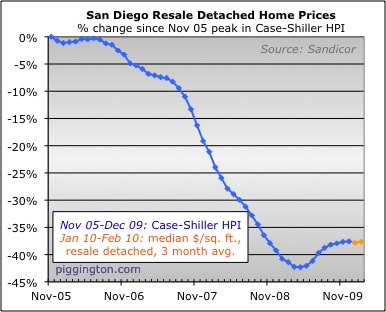

This can be seen on the Case-Shiller proxy, which has pretty much been

flatlined, and (if the latest estimates are accurate) continued to be

last month.

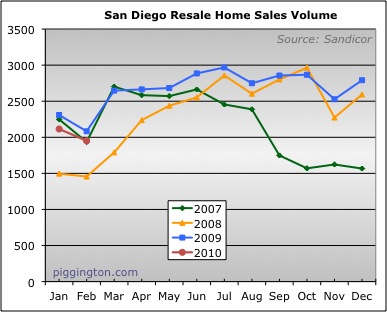

Volume dropped as it always does in February (it’s a short month and in

the slow season to boot). As with last month, we are below

year-ago sales numbers, whereas most of 2009 was spent above the

figures from a year prior. If my post-fake tax credit expiration,

pre-alleged future tax credit expiration lull theory holds (I’m still

working on the name for that one), sales will pick up soon enough.

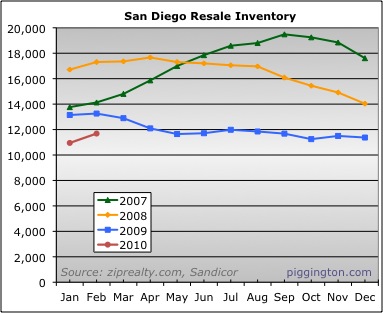

Inventory for sale picked up but is still low on an absolute basis:

This led to a bump in months of

inventory, which is also a normal thing to see in February:

inventory, which is also a normal thing to see in February:

As of February, it had been 11 months

since the recovery in the median price per square foot began. Now

we are almost at the strong season once again, and we’ve got even less

supply compared to demand than at this time last year. At the

same time there is some serious macro risk in the form of the Fed’s

threatened March exit from the MBS market. I suspect that they

will jump right back in if rates rise too much when they bail, but it

could make for at least a period of ugliness in the mortgage and

housing markets. Also, the tax credit is supposed to end in

April, if memory serves, so that could goose things in the next couple

of months as well.

since the recovery in the median price per square foot began. Now

we are almost at the strong season once again, and we’ve got even less

supply compared to demand than at this time last year. At the

same time there is some serious macro risk in the form of the Fed’s

threatened March exit from the MBS market. I suspect that they

will jump right back in if rates rise too much when they bail, but it

could make for at least a period of ugliness in the mortgage and

housing markets. Also, the tax credit is supposed to end in

April, if memory serves, so that could goose things in the next couple

of months as well.

There are a lot of moving parts, as always. Things could get

exciting depending on what happens with the Fed and the MBS market —

but there’s no excitement yet, as last month was more of the same.

Subscribe

Log in

Please login to comment

0 Comments

Oldest