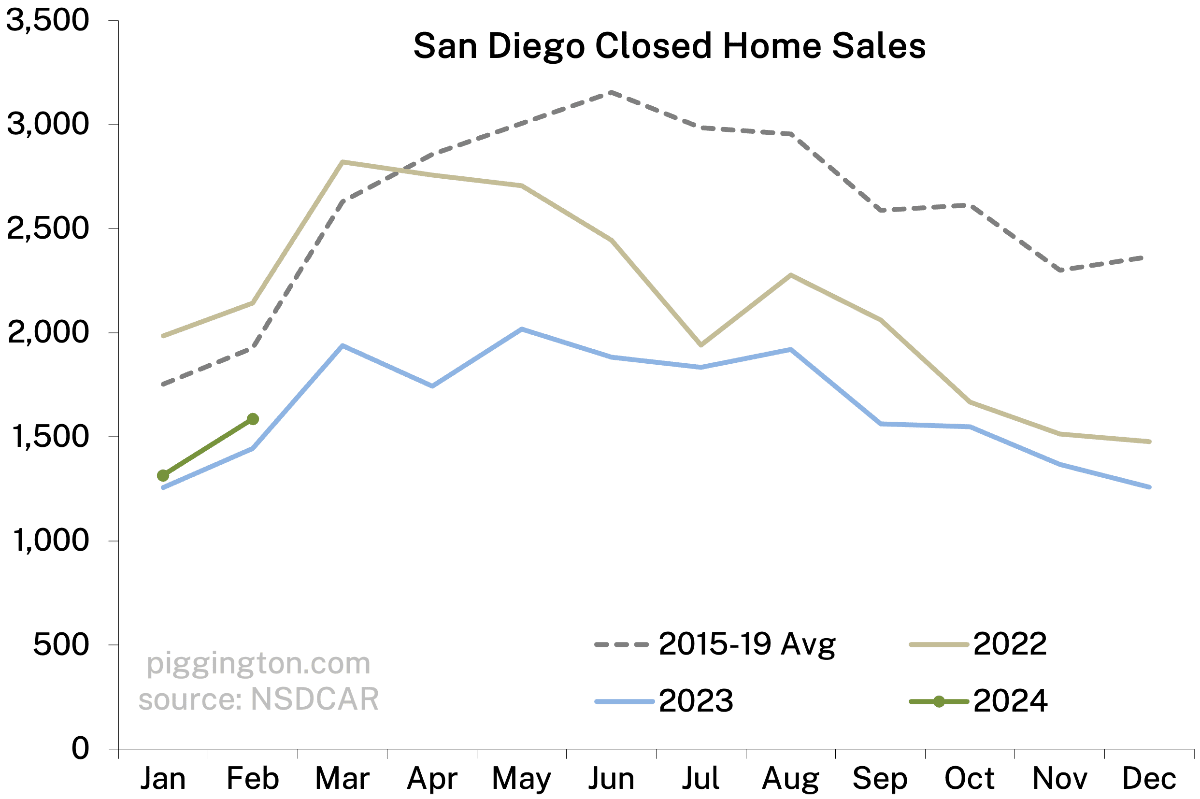

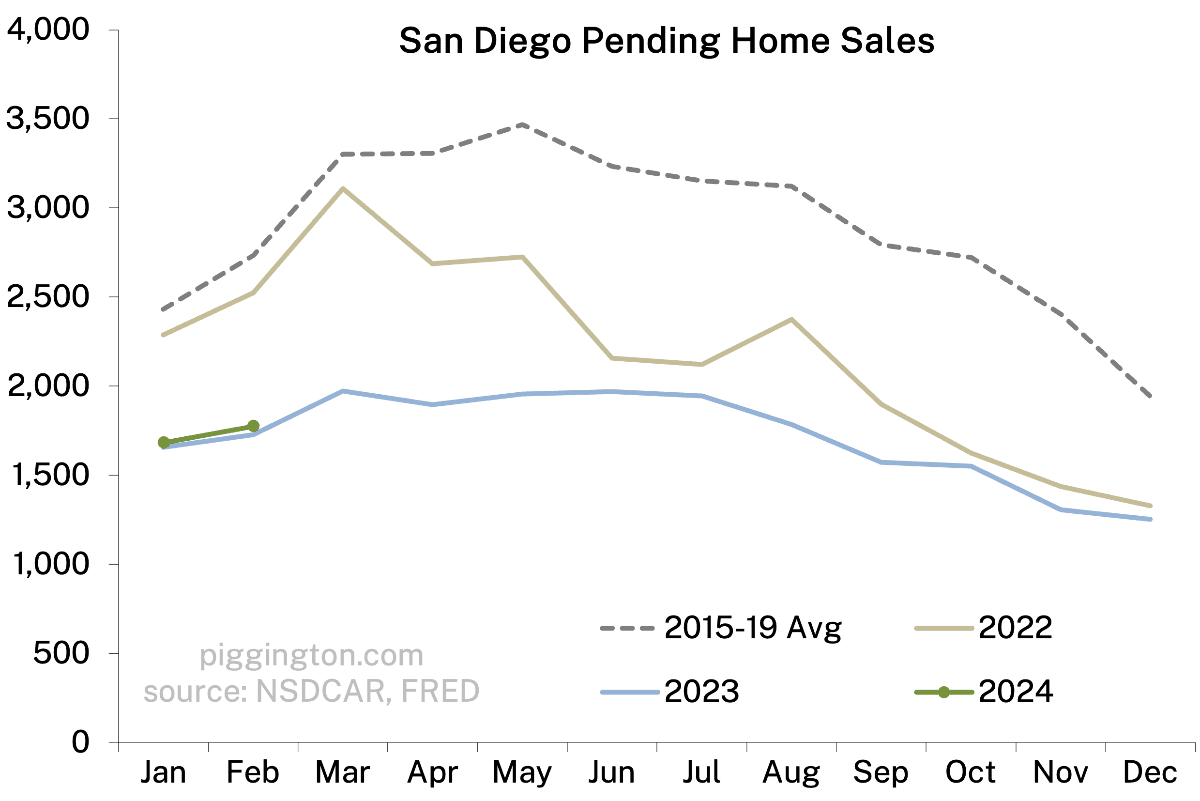

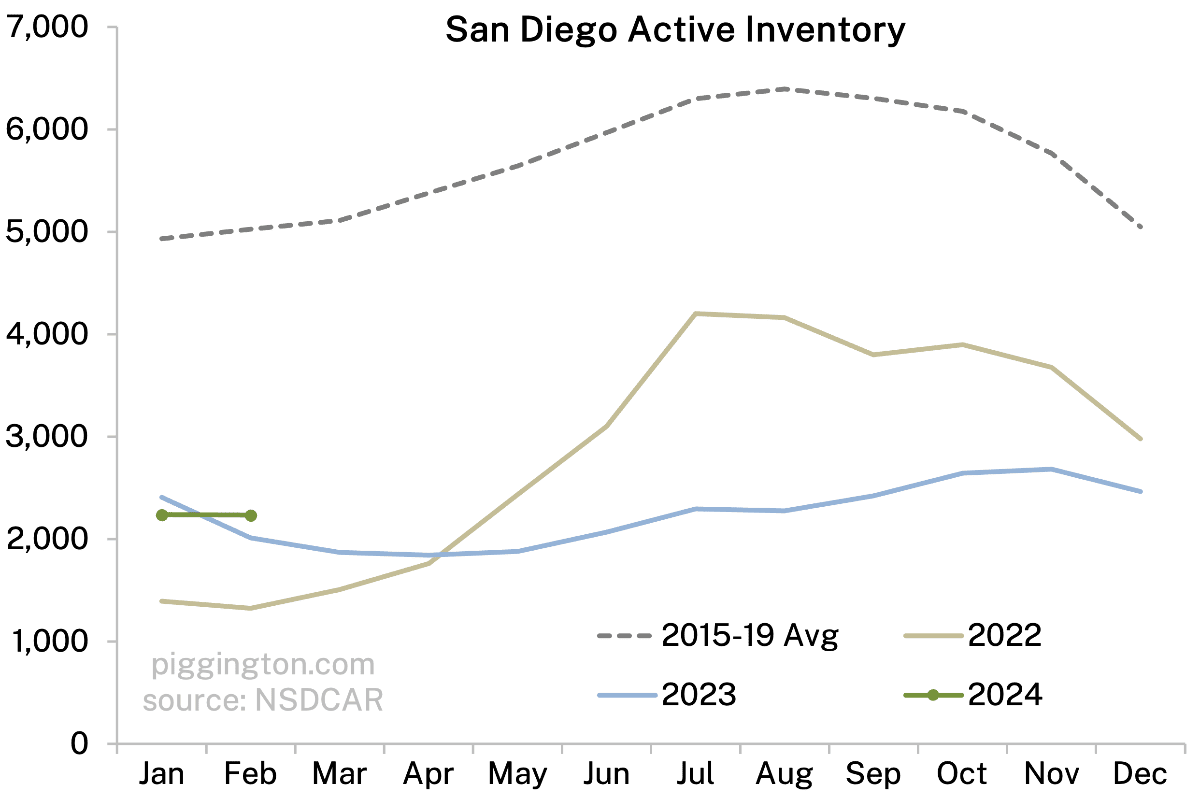

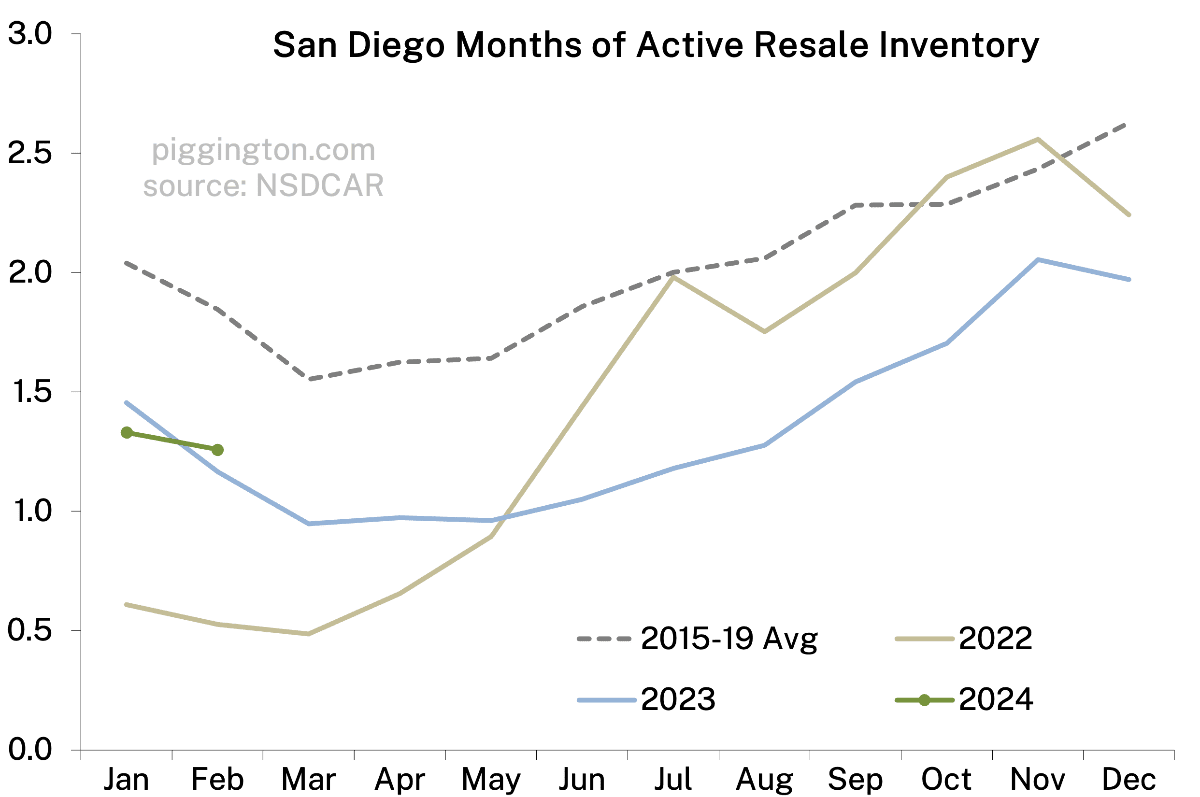

Based on a good idea by pigg sdrealtor, I made the following change to the “month by month” graphs: instead of showing the past 4 years, I show the past three years, plus a dotted line showing the average for 2015-2019. This shows how recent years stack up to a pre-pandemic average, and also gives a better idea of seasonal tendencies.

You can see that sales are lower, and inventory is dramatically lower, than in the pre-Covid period. This is the standoff, low supply and low demand at these prices, and for now it looks like more of the same.

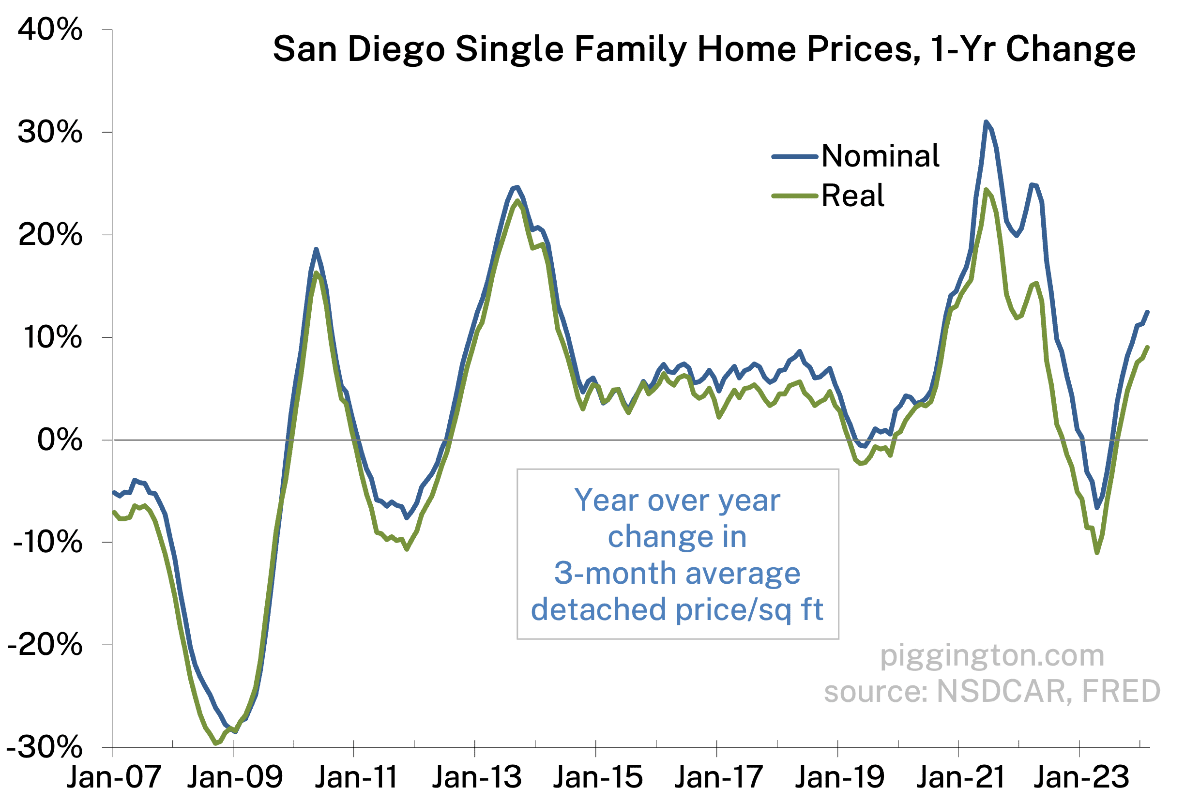

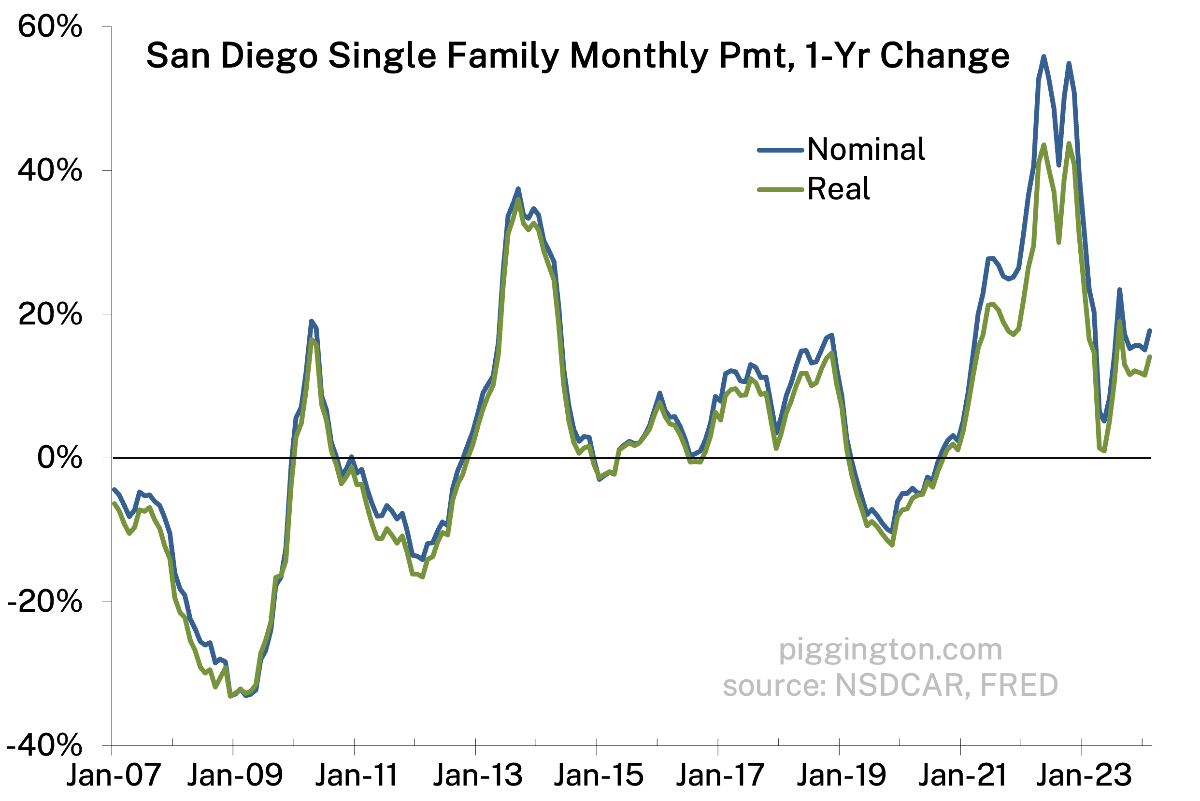

On that topic, Bill McBride just wrote an interesting article on the effects of mortgage rate lock-in. He cites a study finding that “for every percentage point that market mortgage rates exceed the origination interest rate, the probability of sale is decreased by 18.1%.” That’s even bigger than I would have guessed, and it’s clearly a major driver behind the lack of inventory. As Bill notes, this dynamic will fade over time, but (depending on the path of mortgage rates) that could be a long process.

More graphs below…

Standoff or new normal?? I dont see the old folks who bought their homes 20+years ago selling for any reason (other than being forced to move for personal life reasons) when interest rates are this high and their property tax rate is likely 1/10th or less than what it should be. At the same, inflation is showing to be very very sticky at this point, so rates dropping in any significant way soon is unlikely. Even if rates do drop, the property tax incentive to not sell is way to high at this point. People can’t afford homes and people can’t afford to sell homes, that’s the new normal in California

sincerely,

extremely jaded millenial who makes well over 6 figures and still cant afford to buy a home in my hometown/where I grew up

PS. I can tell you from experience that there are a significant proportion (like the majority) of my age group basically praying for a recession right now to reset all this bull shit

I don’t know if it’s the majority, since millennials are now between 28-43 years old. Which means that the majority could have bought a house any time before 2021.

But I do understand your frustration. I don’t know if a recession will fix it though unless you’re also betting that rent will also drop dramatically due to the recession (which it didn’t do in the 2008 great recession). Let’s play out the scenario where there’s a recession and a bunch of people lose their jobs (assuming that you’re not part of that group). As a homeowner who bought two years ago with rates in the 2.x% and 3.x%, their mortgage would be lower than current rent. Which means that they can hunker down, rent out the rooms to get some income to pay the mortgage while waiting out the storm. The other option is to sell, pay tax on some of those gains, take the gain and rent (probably a house that’s less desirable), while hoping that the economy will come back before you run out of cash.

I think the first option seems like a more prudent and less risky thing to do.

Id say a new normal but not forever its just gonna take another 5 to 10 years to get back to normalcy and those in the prime homebuying age range are the unfortunate victims of bad timing/luck.

I don’t think of myself as old quite yet but I’ve been here 25 years. My property taxes are nowhere near 1/10th. My next door neighbors bought a couple years ago. Its more like 1/3. I’m not complaining and feel fortunate but that’s not a problem. I can move my real estate tax basis to another house with prop 60/90.

The problem is capital gains/income taxes! The capital gain exclusion hasn’t changed from 250k single/500k couple in about 25 years. If they would increase that substantially it would get a lot more of my cohort moving. As it stands I would have a taxable gain well into 7 figures.

No, I don’t think this is the new normal. It’s unsustainable for several reasons imo. First, the rate lock-in will recede over time (even if rates don’t go down — eg it mechanically becomes a smaller factor each year as people pay down their principals on the 2021 vintage loans. And also per the CR article, some people will eventually get tired of waiting to make the move they want to make). Obviously if rates go down, that would reduce the lock-in further.

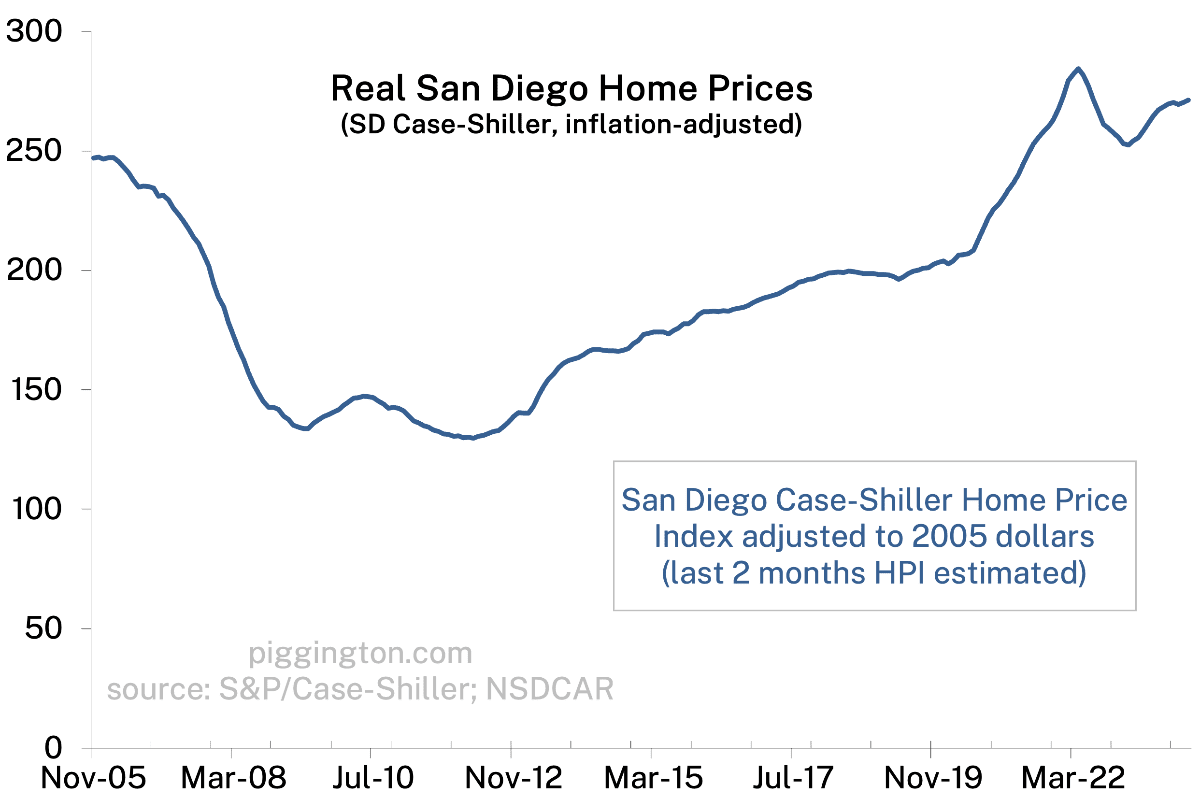

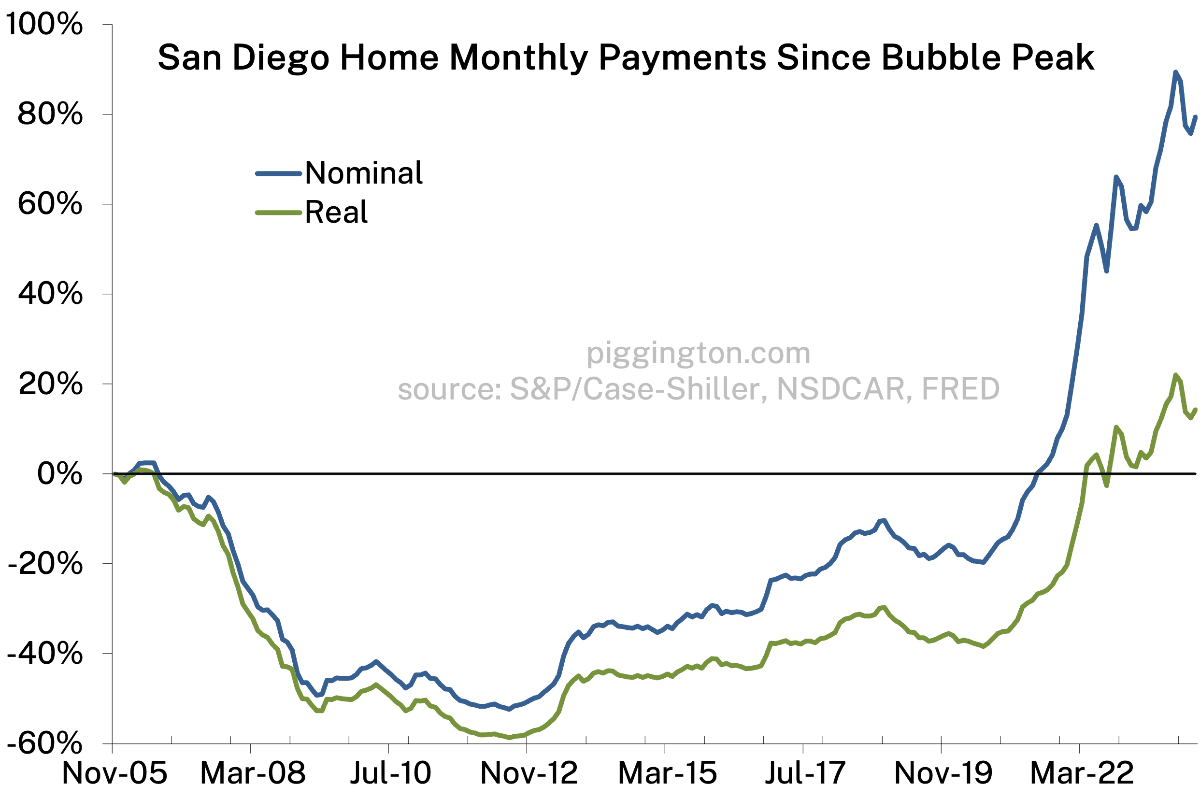

The other thing is valuation. IMO this lack of affordability is not sustainable. There has to be some combination of declining rates and declining REAL home prices, in my view.

BTW your observation on inflation doesn’t line up with the idea of a new normal. Inflation has indeed been sticky, but that’s not necessarily a permanent thing. So yes, perhaps rates won’t come down very quickly, but “new normal” implies a new indefinite state of affairs. A couple years of higher rates is not the same as new normal. And if inflation does persist for many years, that will improve affordability if price growth trails inflation, which I would expect.

The property tax thing is an issue for sure but I don’t see it as enough to overcome the massive weight of the affordability mismatch. As I’ve said in the valuation updates — the only times affordability was this bad in the past was when something crazy and temporary was happening (inflation crisis in the early 80s bringing rates way up, then bubble in the aughts bringing valuations way up). I’m also open to the idea that the population is skewing towards more wealthy but — aside from the fact that this should show up at least partly in income-based affordability ratios — it’s just not enough to offset the crushing lack of affordability.

So no I don’t see this as a new normal at all, though I agree halfway with sdr that it could take a while to get back to a normal, healthy market. The halfway agreement is that I suspect it will take a lot less than 10 years, which was the high end of his estimate. Your hoped-for recession would probably do it pretty quickly by bringing rates down and also bringing more inventory on line from motivated sellers, but even lacking recession I think things are so out of balance that it won’t take super long to normalize.

Just my two cents and a lot of low-confidence guessing about the future…

With regard to unsustainable lack of affordability, isn’t all of this data focused on detached single-family homes? SD is simply not building any more of these compared to multi-family construction starts, so I can totally see a long-run scenario where single-family home affordability here remains absurd compared to townhomes/condos.

On the topic of how long the standoff continues, McBride had a good article on “7 years in purgatory”…5 more years to go…

Yeah, that’s another good one by Bill.

Interesting and plausible point on SFH vs. condo. I have doubts about how big that gap could be — I’d think that if as the premium goes, relative demand for SFH would drop putting downward pressure on the premium. But I could definitely see the premium being higher than it is historically.

That said, this is more an issue with my charts than with the broader question of “will I ever be able to buy here.”

Last thought – I know it was hyperbole but surely it’s not the case that they are not building ANY single family. This is something I’d like to look into more — do you (or anyone) have a data source for housing supply, hopefully broken down into SFH vs. multi family?

First Tuesday has a chart that breaks it down linked below (gotta scroll down a ways to find it). After the financial crisis the rates of single vs multi family starts basically flipped, so I feel like now the low rate of single family home construction starts means these will command a significant premium over townhomes/condos

https://journal.firsttuesday.us/san-diego-housing-indicators-2/29246/

Totally agree, with the push to increase density, SFR is becoming a luxury purchase. People “will be able to buy here”, just not the house they might want. We’ll probably have to adjust and think more like European or Japanese

yeah, SD is basically a geographically constrained box with ocean, mountains/desert, camp pendelton and mexico as its borders. higher density is inevitable.

Especially if you want to be w/in 15 minutes of the coast.

My thinking is along the same lines. This is very, very far from normal – could be generational extreme. Once it starts to revert, it will move very quickly. I don’t see a way to predict what can trigger the reversal.

It never moves quickly to the downside

Thanks Rich that’s a big help and improvement. Collectively 15 thru 19 were as normal of a market as we’ve seen around here in a couple decades.

Looking at each graph here are my high level takeaways

Closed sales aren’t off as much as some of the other measures attesting to the strength and desirability of SD Less homes are going on the market but a higher percentage of them are selling. The 2022 line shows how big an impact the interest rate spike in Spring 22 bringing sales way off the the typical trendline. It lines up with the short lived flash crash in pricing we experienced in Fall 2022.

Pending home sales are way down but exhibit less seasonal fluctuations than they should. Its a slow sluggish standoff that goes on all year

Inventory is way down. Its more than 50% below where it should be. This means its harder to find a good one and when you do you shouldn’t be surprised to have lots of company. The best properties that are priced at market in the bottom 2 quartiles attract lots of buyer attention. More inventory will create more ability to negotiate. I think its gonna start increasing but its important to keep a historical perspective that its still tight until we get back close to prior average.

Months of inventory looks better than raw inventory counts because sales counts are way down also. When this gets closer to that 5 year average we’ll be in a much healthier market. This is something to keep a close eye on

Just renewed lease for 2 years, waiting on a market that doesn’t seem so distorted. The cost to buy something similar to what I’m renting was astronomically more expensive, especially when you factor in the lost interest income on the down payment funds (even after tax) and monthly principal paydown (not an expense, but cash flow nonetheless). Then there’s the capex that comes with owning. Sure, maybe a refi to a lower rate down the road is plausible, but a gamble.

Something’s gotta give…if not, guess I’ll look to other markets once kids are through high school. I hear St. George is great (sarcasm).