Once again, the traditional “Shambling Towards Affordability” title

for this series proves inapt. The market does have a bit of a

shamble to its step, but the direction in which it lumbers is

distinctly un-affordable. (In price terms, anyway… low rates

do ease the sting, but that’s a separate topic to be addressed

below).

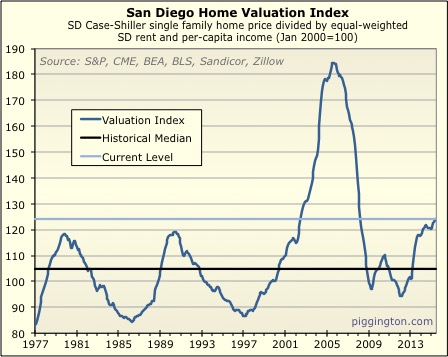

While valuations have crept up a bit over the past year, the big

picture hasn’t changed much: home prices are significantly higher,

when compared with local rents and incomes, than they typically have

been over the almost 4-decade history of the data:

Yet they are nowhere near the heights they reached in the bubble

that, incidentally, topped out almost exactly a decade ago. (Wow!

Ten years… so many thoughts in response to that. Most of

them relating to how elderly and decrepit I am.) As of last

month, San Diego home valuations stood 18% over the historical

median — absolutely nothing next to the towering 76% overvaluation

of mid-2005. Still, the market is currently more expensive

than it’s ever been outside of that mid-aughts bubbliness.

I don’t believe that the market must necessarily revert to

the median valuation of the past any time soon (or maybe even

ever). While I’m generally a big believer in the

mean-reversion of financial market valuations, local real estate

markets are a weird enough animal that once in a great while, “this

time” actually is “different,” to at least some

degree. Structural factors like land constraints,

changing demography, etc. could conceivably justify an indefinitely

higher (or lower) valuation than the historical norm, and I think it

would be irresponsible to just dismiss this possibility.

Nevertheless, it is an objective fact that San Diego housing is

significantly more expensive than it typically has been in recent

decades. This warrants caution, at the very least.

And while I think we should be open to the idea that higher

valuations could be sustainable in the future, I also think that

anyone claiming that “this time is different” needs to bring proof

to the table, and not just point to current valuations as

justification (as we can see, the market sometimes gets it

wrong). Given the complexity of the market, this is not an

easy thing to prove, nor for that matter to disprove.

As a reminder, I use incomes and rents as the denominator for the

valuation ratio because they represent the two most important

fundamentals to home prices: how much potential home buyers are

earning, and how much a home could be rented out for. The

highly mean-reverting nature of the above graph shows that this has

been a very solid valuation measure throughout the history of the

data. Ignore it at your peril!

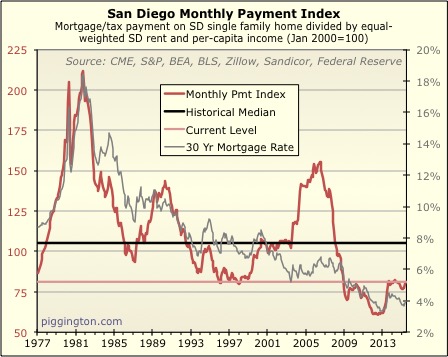

The Effect of Mortgage Rates

Now let’s zoom in on one factor that’s almost certainly helping to

keep valuations aloft right now: interest rates. The chart

below shows the ratio of monthly payments to rents and incomes:

What this graph shows is that rates are low enough to more than

offset high housing valuations, resulting in monthly payments that

are, despite unusually expensive purchase prices, lower than the

historical norm.

Now, there are a couple of issues with the idea that low rates

justify sustainably higher valuations:

- They may be lowering monthly payments right now, but that only

lasts as long as the low rates themselves. And while

everyone seems to have an opinion about the future of interest

rates, the fact is that nobody really knows for sure. - For interest rates to stay low indefinitely would require

inflation to remain low indefinitely. And part of the

“value” of buying a house is the inflation protection (against

rising rents, in specific) afforded by owning your own

home. If buyers came to expect permanently low inflation,

the inflation protection premium embedded in home prices would

be reduced.

I believe that these two factors help to explain why the first

chart, which just looks at prices vs. the fundamentals without

taking rates into account, has been highly mean-reverting even

across a wide variety of interest rate climates.

But those are long-term considerations. For now people want

to buy, and low rates are helping them to pay higher prices while

keeping the monthly payments reasonable. So homes are

expensive, and they may stay that way for quite a while if low

rates stick around. But I think this factor is a bit

overrated, and I am also skeptical of the new (apparent) consensus

that low rates are a permanent fixture — so I consider it to be a

pretty big gamble to depend on low rates propping up home

valuations indefinitely.

Thanks for all this data and

Thanks for all this data and nice graphs.

I think you’re underplaying the significance of low rates however. Payments are low, and can be locked in for 30 years. So sure, you’d suffer if rates rise and prices fall, but if the property at least breaks even on rent/expenses, you can look forward to owning the place at the end of the mortgage.

I also think rates are just as likely to go down rather than up. Have a look at interest rates around the developed world and you’ll see that in the USA, they are close to the highest. Rates are negative up to 11 years in Switzerland and 7 years in Germany. The number of creditworthy people who want to borrow money keeps going down as western economies stagnate and age. Whoever is buying bonds at a guaranteed loss in Germany might start finding the 2% 10-year treasury yield pretty attractive.

“And part of the “value” of buying a house is the inflation protection (against rising rents, in specific) afforded by owning your own home. If buyers came to expect permanently low inflation, the inflation protection premium embedded in home prices would be reduced.”

I doubt more than 10% of home buyers think this way. Moreover, rents, like manufactured goods, commodities, tuition, and medical services, has long decoupled from the general inflation rate.

I think the more relevant hedge, at least for California real estate purposes, is the one in which Chinese and Korean buyers want someplace to stash their wealth and families, and eventually themselves, if their own country goes to crap. Or in China’s case, continues its trend of becoming so polluted it is unsafe to live in its major cities.

gzz wrote:Thanks for all this

[quote=gzz]Thanks for all this data and nice graphs.

I think you’re underplaying the significance of low rates however. [/quote]

You are welcome! But I think you are misunderstanding my argument.

[quote=gzz]Payments are low, and can be locked in for 30 years. So sure, you’d suffer if rates rise and prices fall, but if the property at least breaks even on rent/expenses, you can look forward to owning the place at the end of the mortgage. [/quote]

Completely agree. That’s why I bought a house. But that is not the same as saying that low rates justify INDEFINITELY higher home valuations. IE, the fact that rates are low now, does not remove the valuation risk that comes from homes being 18% more expensive than usual. It’s kind of a subtle distinction I admit. But it’s not about the “should someone buy now” question, but the “what’s the upside/downside risk to prices” question, which are 2 different topics. I should have made that distinction more clear.

[quote=gzz]I also think rates are just as likely to go down rather than up. Have a look at interest rates around the developed world and you’ll see that in the USA, they are close to the highest. Rates are negative up to 11 years in Switzerland and 7 years in Germany. The number of creditworthy people who want to borrow money keeps going down as western economies stagnate and age. Whoever is buying bonds at a guaranteed loss in Germany might start finding the 2% 10-year treasury yield pretty attractive.[/quote]

Yes, this is the new consensus view that I referred to. I personally am skeptical, but that’s beside the point. The point is that nobody really knows what interest rates will do in the near future — so if you put yourself in a position where you depend on them staying low, you are taking a gamble. Unless you truly can predict interest rate movements. In which case — can I come hang out on your yacht? 😉

[quote=gzz]”And part of the “value” of buying a house is the inflation protection (against rising rents, in specific) afforded by owning your own home. If buyers came to expect permanently low inflation, the inflation protection premium embedded in home prices would be reduced.”

I doubt more than 10% of home buyers think this way. [/quote]

Maybe. So tell me this: why is it that the interest rate-unaware valuation ratio (price to incomes+rents) has tended towards a central value across vastly different interest rate climates?

[quote=gzz]Moreover, rents, like manufactured goods, commodities, tuition, and medical services, has long decoupled from the general inflation rate. [/quote]

Rents have tended to increase faster than inflation, here in San Diego, but that’s not the same as decoupling — all things equal, higher inflation will correlate with higher rents. The cost of housing (which is all computed via rent prices, either outright rent or homeowner’s equivalent rent) is 40% of CPI, after all — how decoupled could they get?

[quote=gzz]I think the more relevant hedge, at least for California real estate purposes, is the one in which Chinese and Korean buyers want someplace to stash their wealth and families, and eventually themselves, if their own country goes to crap. Or in China’s case, continues its trend of becoming so polluted it is unsafe to live in its major cities.[/quote]

That could be one of the “different this time” reasons that could, conceivably, justify permanently higher values. I don’t understand what it has to do with the conversation about rates, though.

This time is truly different.

This time is truly different. I am not saying this but a lot of folks on this board are saying this as they have already bought houses during the last down turn..

One key difference since 2013

One key difference since 2013 vs 2003-2007.

Today as a landlord, I can raise rents 3%-6% year depending on how much the property is below market. In the 2003-2007 period so many renters wanted to buy that raising rents was actually more difficult as the banks would throw money at them to buy at the overinflated prices.

As many former owners are only slowly repairing their credit and generally down-payments/documentation requirements are more rigorous, the threat of a renter leaving is much less today. So while yes, I’ve been able to lock in rates of 3.7% for 30 years on investment property, what is more important today is the ability to keep raising rents on a consistent basis.

Part of this is driven by the lack of new construction over the past seven years.

Unless new construction picks up meaningfully, it looks like there is a permanent gap in the quantity of housing units.

Asian demand can reduce the chance of the gap downs in pricing.

Ironically, the additional immigration keeps wages across the country lower which keeps interest rates lower. Immigration curbs might actually cause modest wage growth in certain non-exportable sectors.

But for now with lack of supply, low rates, Asian demand and job growth with immigration levels where they are, it is almost a landlords dream.

The key drivers of inflation in the past have been energy and labor. Oil looks set to be well oversupplied for the next five years, renewables keep getting cheaper. SDG&E rates are basically flat for the next five years. The shift to Uber/driverless cars may also make transportation cheaper over the next decade giving more disposable income for housing.

Perhaps if the baby boomers retire in mass, then we’ll see wage inflation, but most of those I know in that generation seem to always have another bill to pay which prevents them from amassing true wealth and retiring to plan.

Plugging the pigg in other

Plugging the pigg in other media….

https://www.reddit.com/r/sandiego/comments/3fnox8/buying_my_first_house_in_san_diego/

Someone should really create

Someone should really create a link for the shambling article on the San Diego sub-reddit. Perhaps even a sidebar addition. The reply to your comment suggests not many people know about this site.

I found piggington through Dr. Housing. Rich’s shambling blog from last year really, really helped me decide to buy last year. I am a numbers guy, and his analysis reassured me a lot. Also the forums are a great source for information on San Diego real estate.

Thanks Dan and bewildering…

Thanks Dan and bewildering… glad some folks are still finding this site to be useful!

Rich

The site is extremely

Rich

The site is extremely useful. Especially as the market normalizes.

The key question in this cycle is, do we enter another downturn for some unforeseen event or does the market go back to lower levels of appreciation but not correct.

My view is that we don’t have a serious correction (for a few more years due to supply issues) but I think the question is on everyone’s mind who owns real estate.

There are likely other forums like reddit which could bring in more readers etc for you.

Love the data and commentary

Love the data and commentary on this site. It is very useful. Thank you for publishing.

I was just driving down the 56 and I am surprised to see how much residential construction is occurring right off the highway. We all know that real estate is a supply/demand game. Any ideas of good sources for new supply set to come on line in SD, type of supply (i.e. approx price point) and timing of the new supply?

Everything you see along 56

Everything you see along 56 is 800K to over 1M.

It looks like more than it really is as the builders are very careful about releasing new units. They have whole teams of analysts who make sure they extract every last dollar of value from those who will actually live there. This supply is actually a very bullish sign for the price developments of existing housing stock as the builders won’t take the risk of getting stuck with inventory. They have demonstrated they can ride out the ups and downs of the cycle and hold on to land.

http://www.metrostudyreport.com/category/san-diego-market/

“Starts by Price Range are broadly distributed across all major price ranges, with 26.1% of starts showing up above the $900,000 mark,” said Dennis Handler, Director of Metrostudy’s San Diego market. “Approximately 48% and 56% of housing inventory and VDL inventory falls below the $500k range, respectively.

Single-Family Permit Activity through the first two months of 2015 totaled 687 permits, approximately 27% of total permits that were approved for all of 2014.”

Average resale price for single family detached homes increased from $618,556 in 4Q14 to $655,844 in 1Q15, or +6%. For all product types combined, the average resale price increased from $545,586 in 4Q14 to $582,139 in 1Q15 or +6.7%. New annual average price for single family detached decreased from $960,948 in 4Q14 to $849,869 in 1Q15 or -11.5%. For all product types combined, the average new price decreased from $758,998 in 4Q14 to $713,804 in 1Q15 or -6.0%.

Great stuff as usual. How

Great stuff as usual. How strange that homes are a hedge against inflation yet are a major cost for many of us. So why aren’t they included in the inflation numbers? As you point out, the low monthly nut keeps that cost in check, so are low rates now the new hedge against inflation? I thought they were supposed to encourage inflation. The Fed is torn between an inflation target or cap and the unexpected consequences of extended or permanent low rates. The unknowable becomes increasingly likely as we go on, so how confident are we that the Fed can cope?

Out of curiosity, what does the affordability chart look like when only incomes are used? Rents have been subject to sharp increases, probably fueled by increased home prices. Won’t that make the affordability index look a bit healthier than it is?

Jazzman wrote:

Out of

[quote=Jazzman]

Out of curiosity, what does the affordability chart look like when only incomes are used? Rents have been subject to sharp increases, probably fueled by increased home prices. Won’t that make the affordability index look a bit healthier than it is?[/quote]

As home prices rise and rents rise affordability gets worse.Now that I reread your statement I get it, yes Rich’s charts do not indicate affordability. And any statement that “this time is different” makes me think that someone is in bed with a realtor.