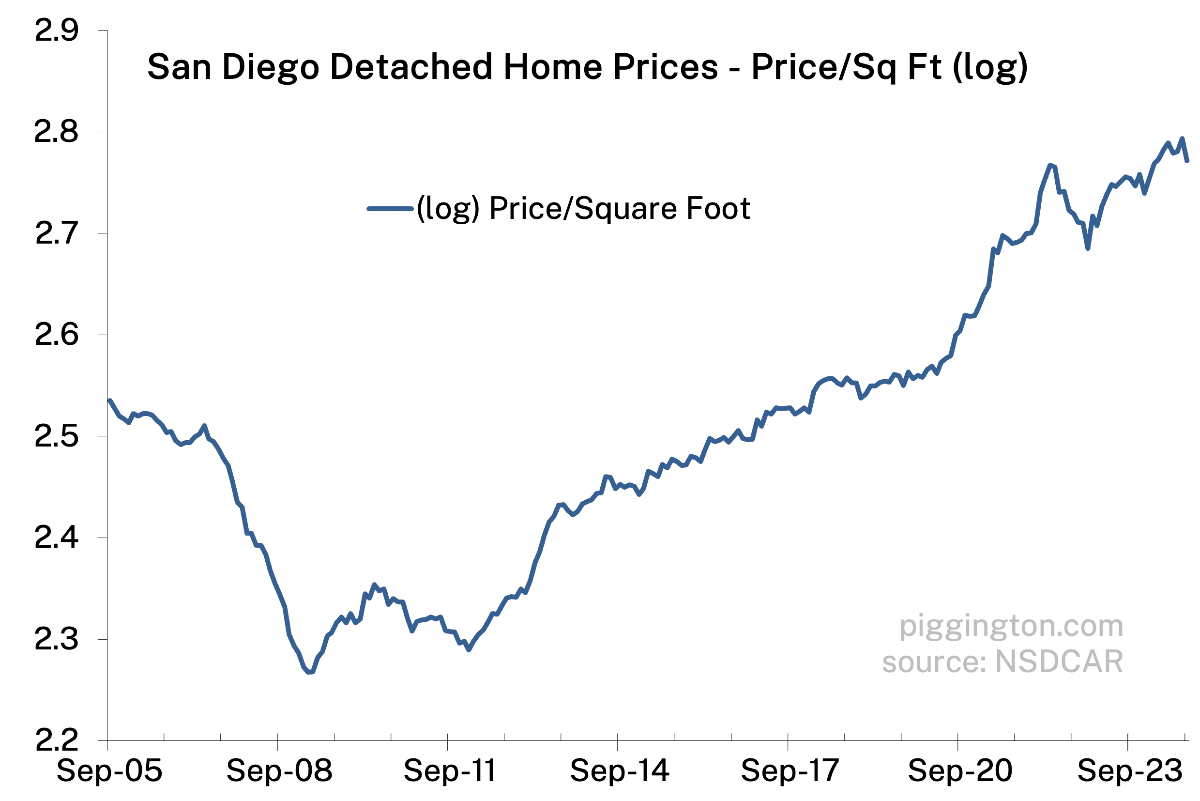

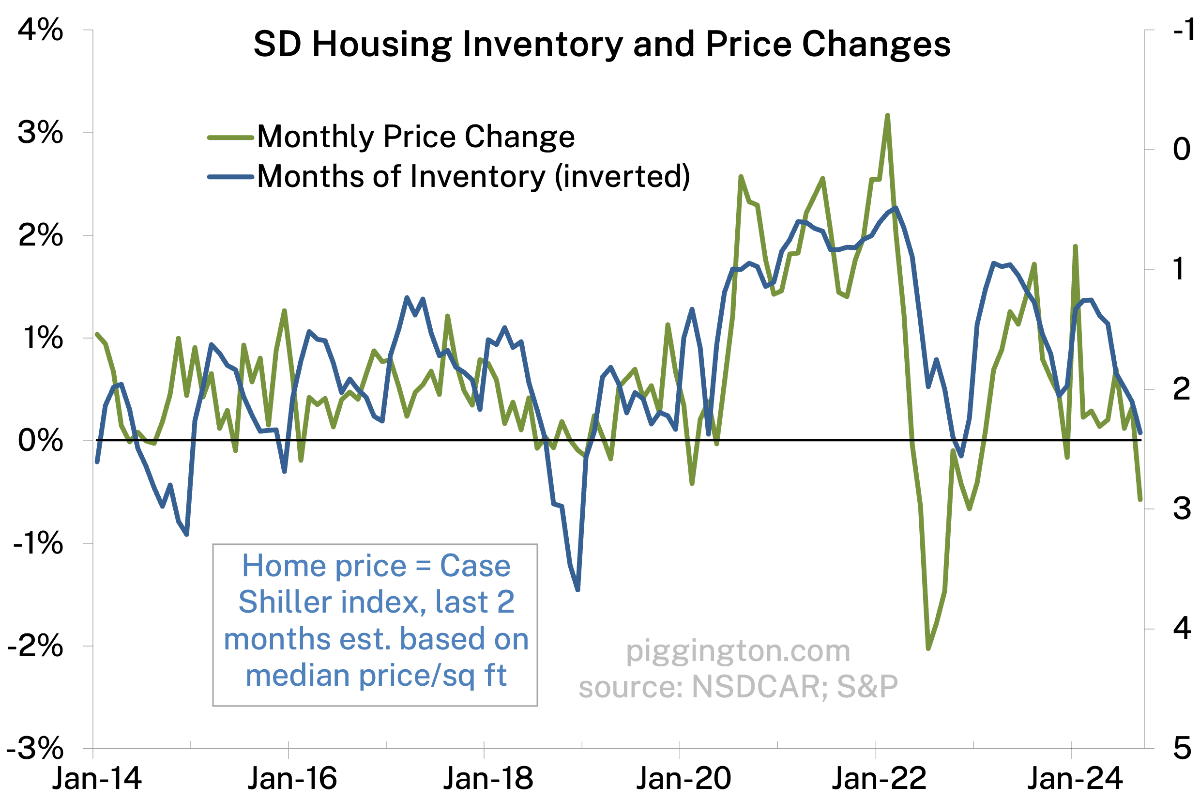

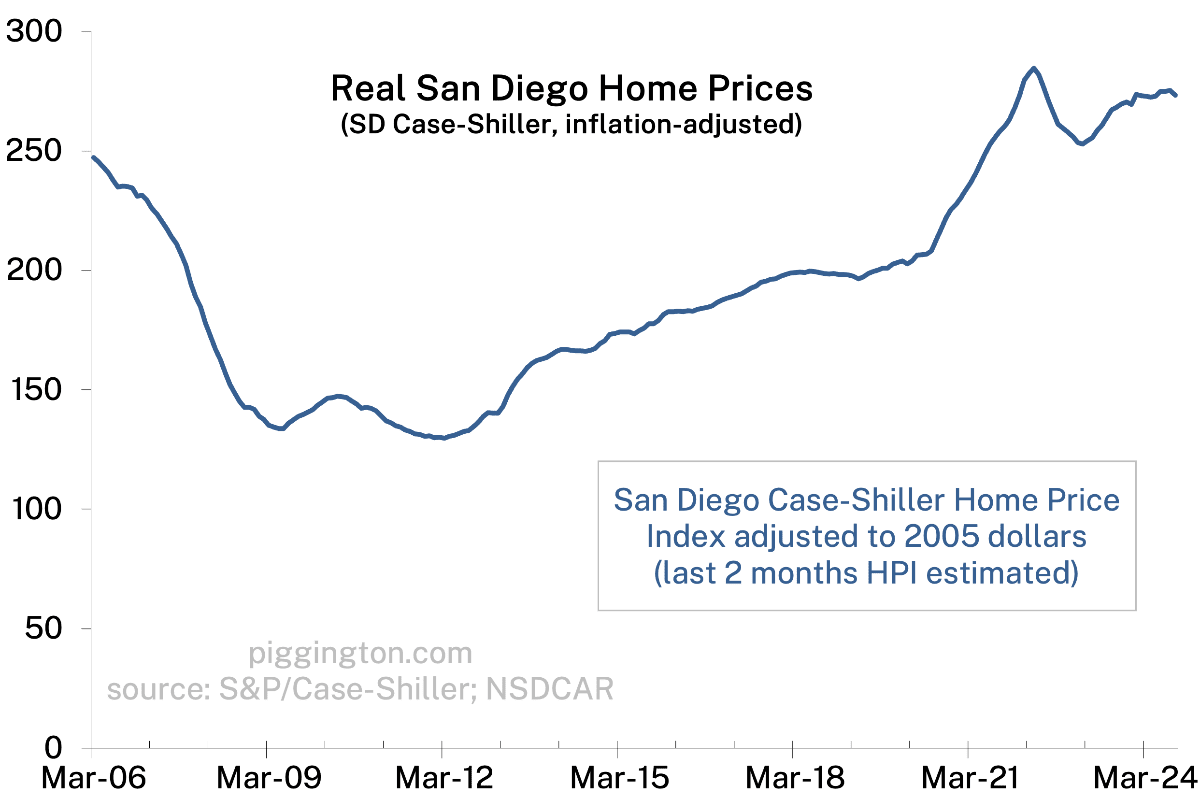

The median price per square foot was quite weak last month, but (like I said last month when prices made a big move in the other direction) it is a noisy series.

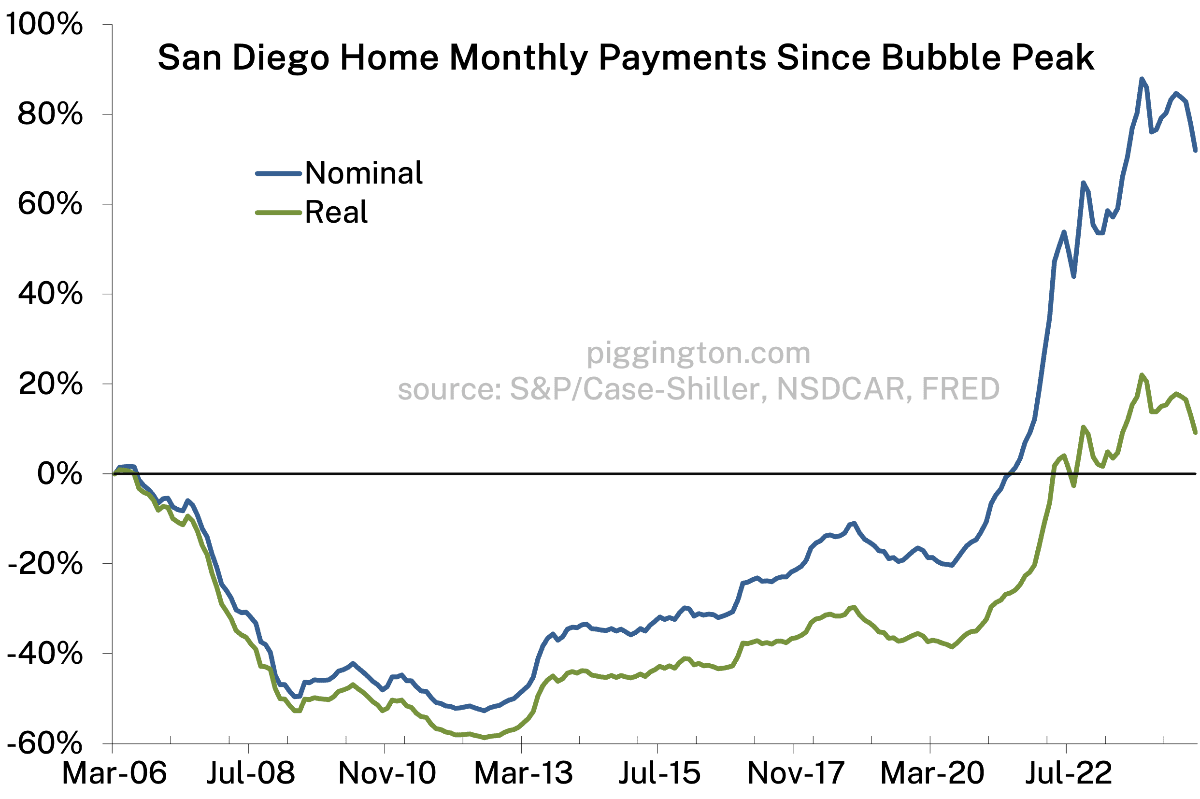

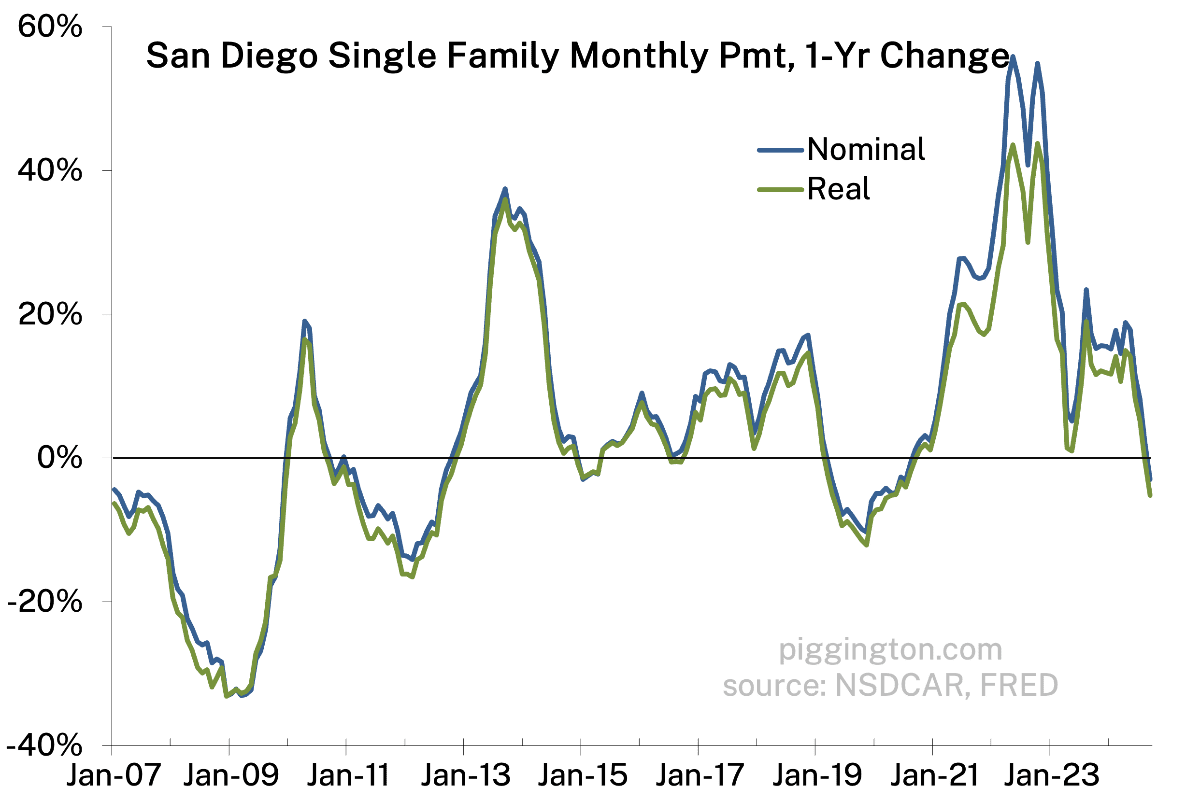

The decline in rates brought some relief on the monthly payment front as well, but the picture there is still pretty ugly.

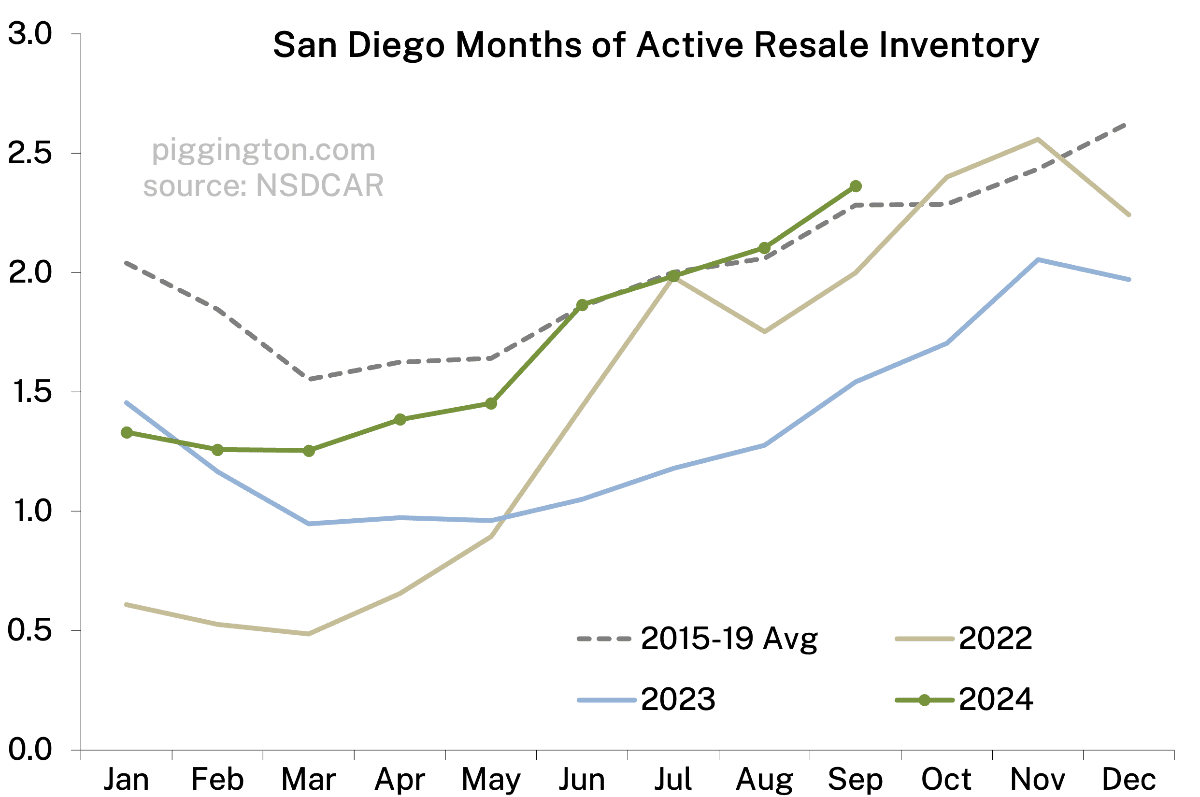

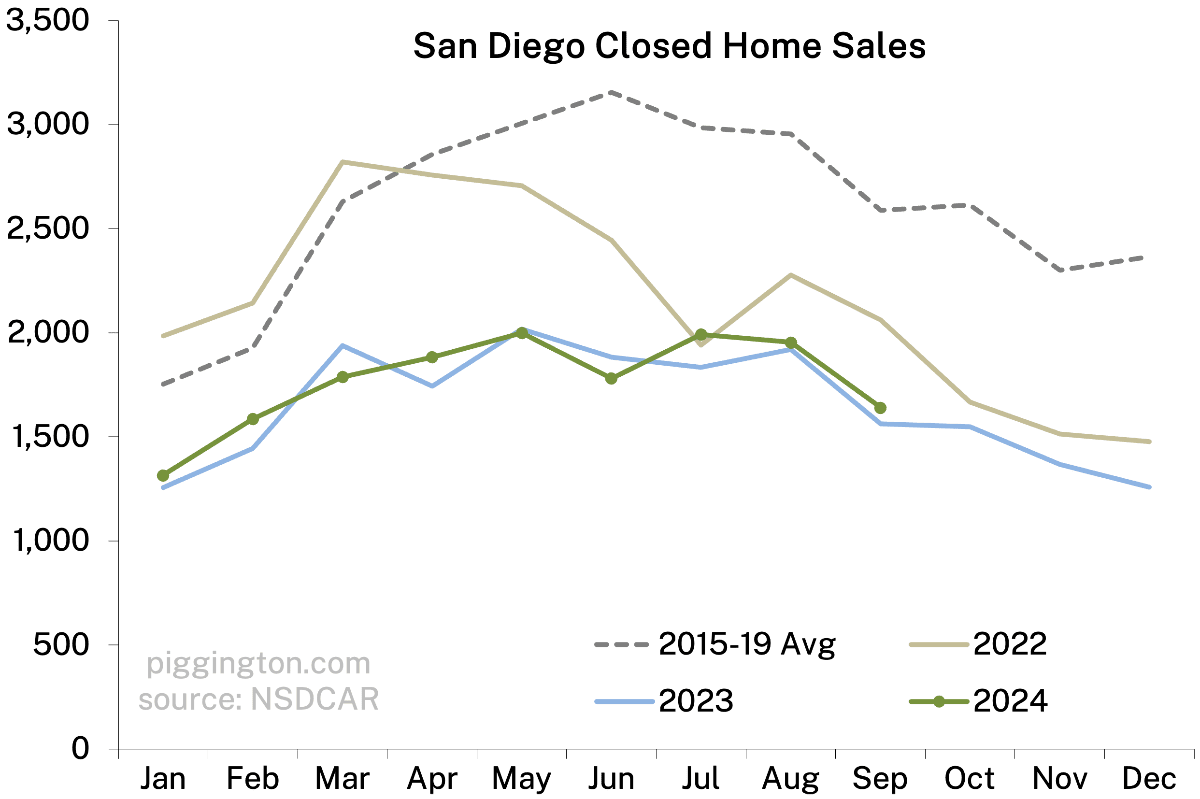

Meanwhile months of inventory actually exceeded the pre-Covid average (by more than a smidge this time):

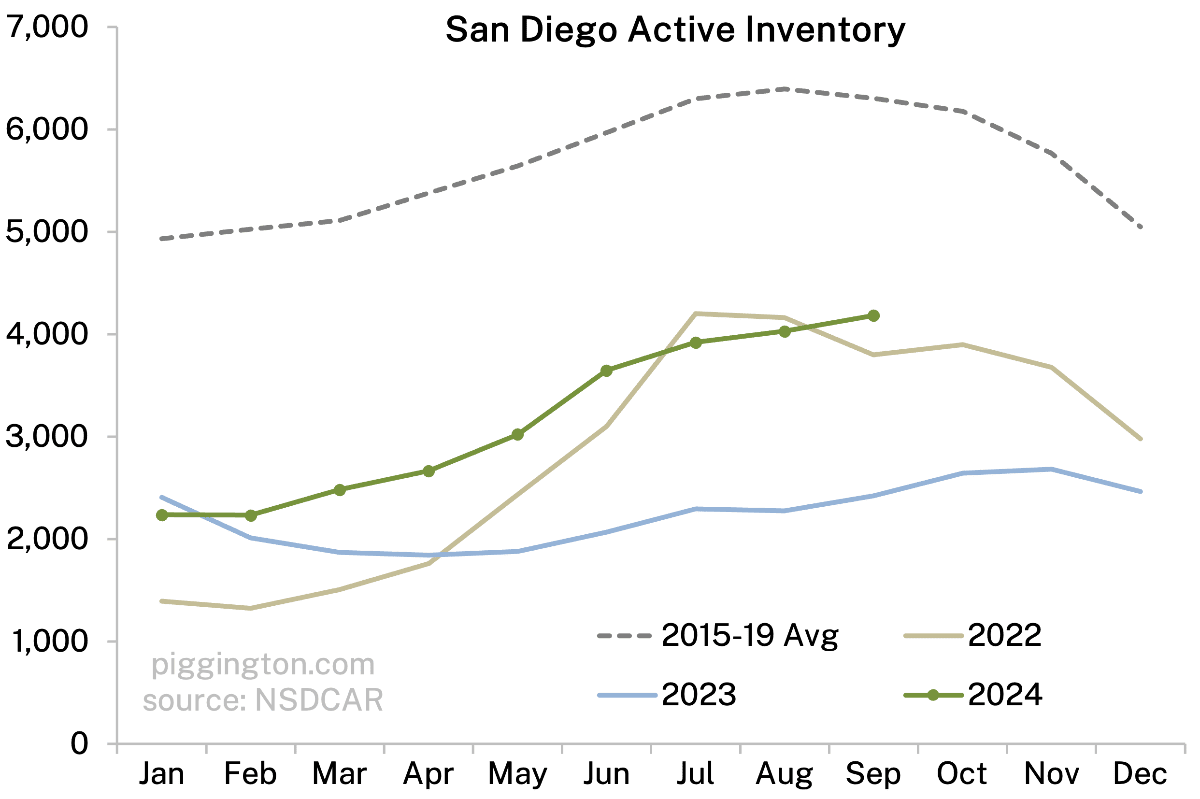

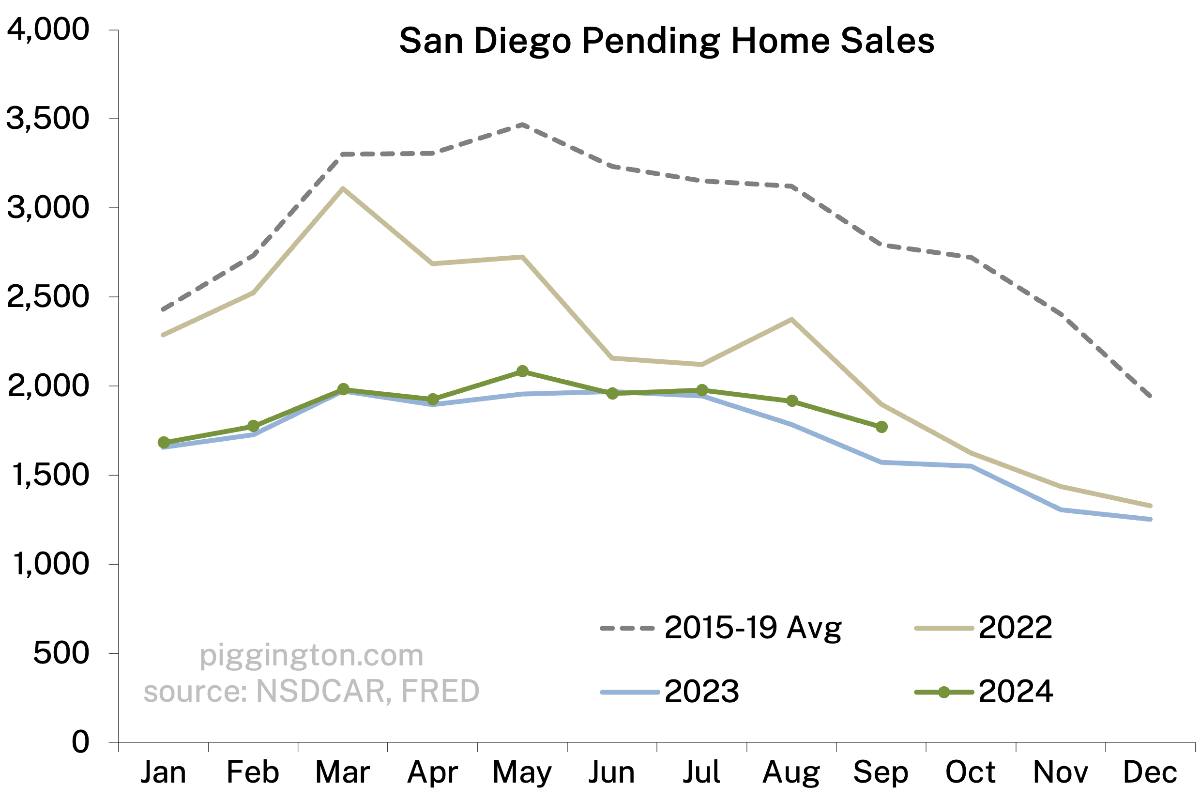

As usual, both inventory and sales are still well below 2015-19 levels. But inventory has risen a lot, against flatlining sales volume, so that the combined months-of-inventory measure has risen substantially.

This chart of prices vs. months’ inventory suggests weak prices ahead.

More charts below…

This is purely anecdotal, but I was looking at zillow today at rentals and it really seems like rents have/are dropping significantly. Seeing solid sized houses with yards in clairemont and bay park for 3000-3500, which was unheard of last year when I was moving.

I expect this will put downward pressure on home prices.

Just want to thank Rich for doing this all these years! I remembered emailing him in 2004 or 2005 with questions a about buying and he recommended holding off, I did and bought in 2009. But just amazing he posts all this data all these years. My uneducated guess is that this is the start of the correction, I was beginning to think we were more like Hawaii where prices don’t really correct much at all because we are “destination city”. But seeing lots of for sale signs, and people pulling there house of the market makes me think the correction has started, the flippers seem to have moved to the sidelines as well. I wonder if there is a stat of closed sales dates that shows houses sold twice in six months to track flippers. Lack of flipping seems like it would be a good indicator….

Thanks for the kind words… and glad the site was of help to you!

(PS I don’t have that data on repeat sales… fwiw I think flipping might be a lagging indicator vs. a leading one, but that’s just a guess).