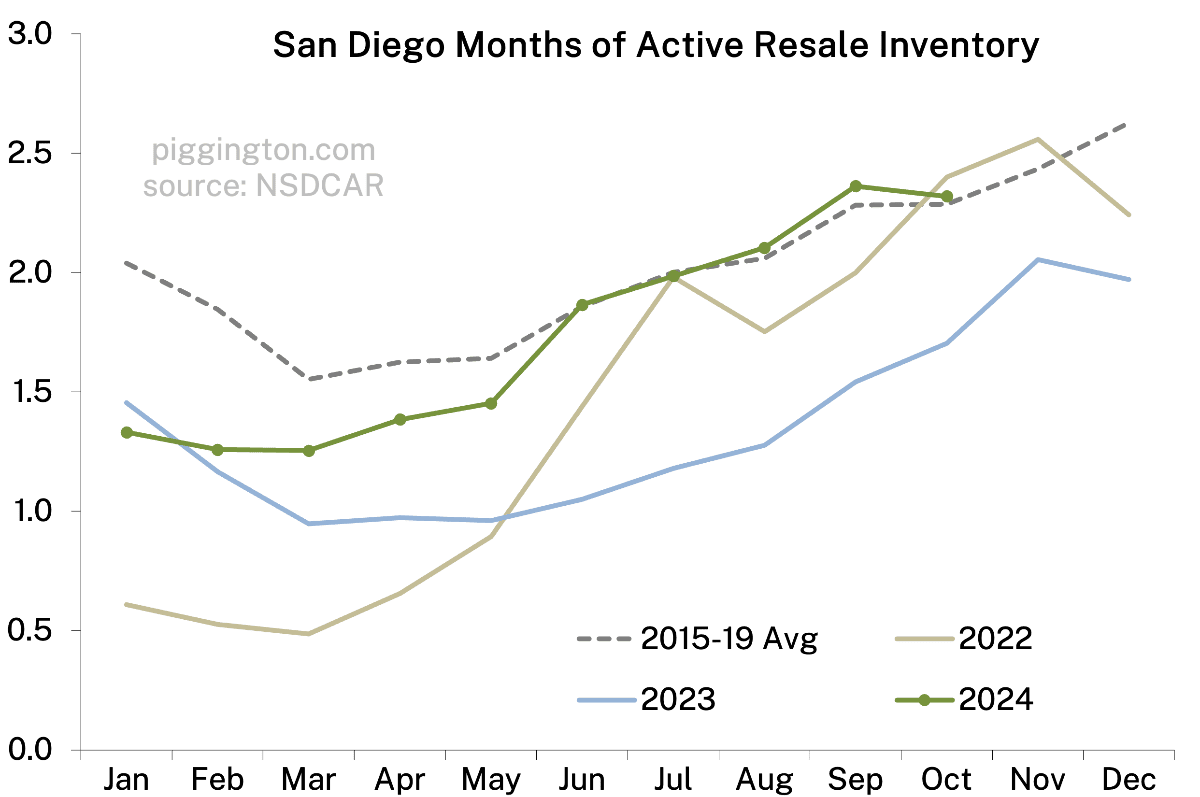

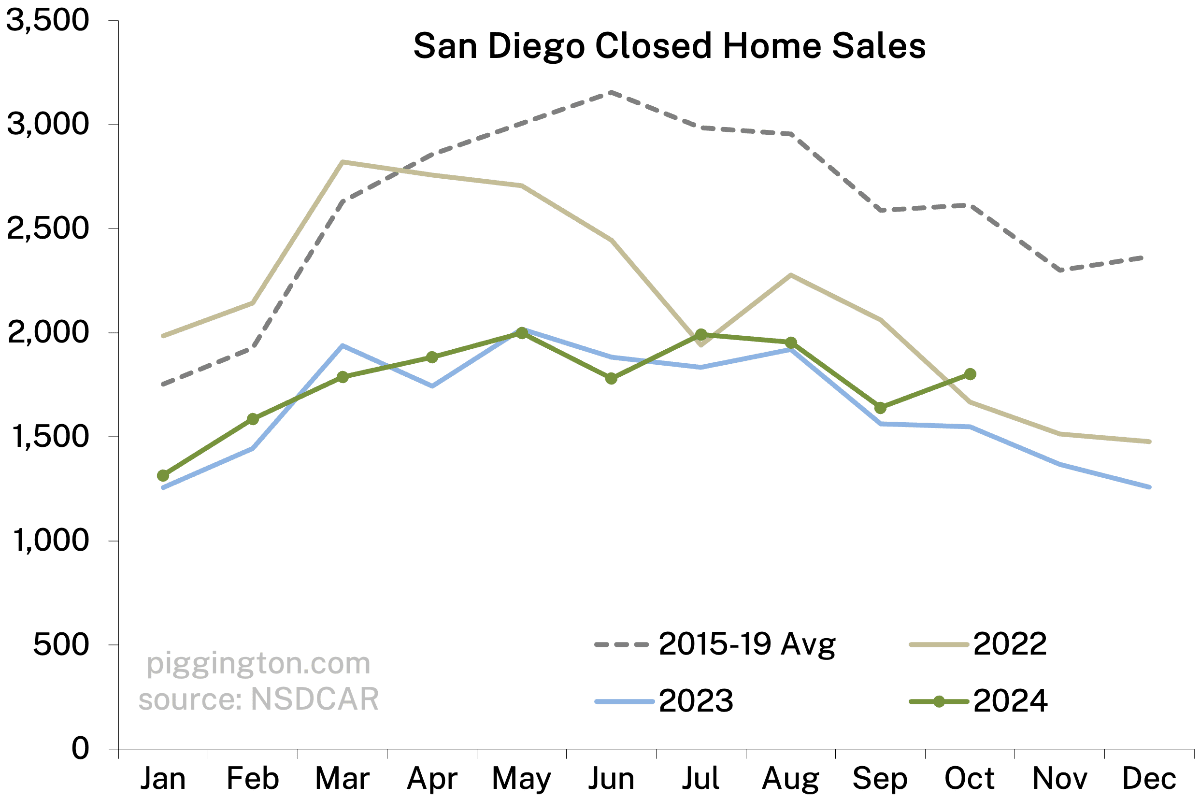

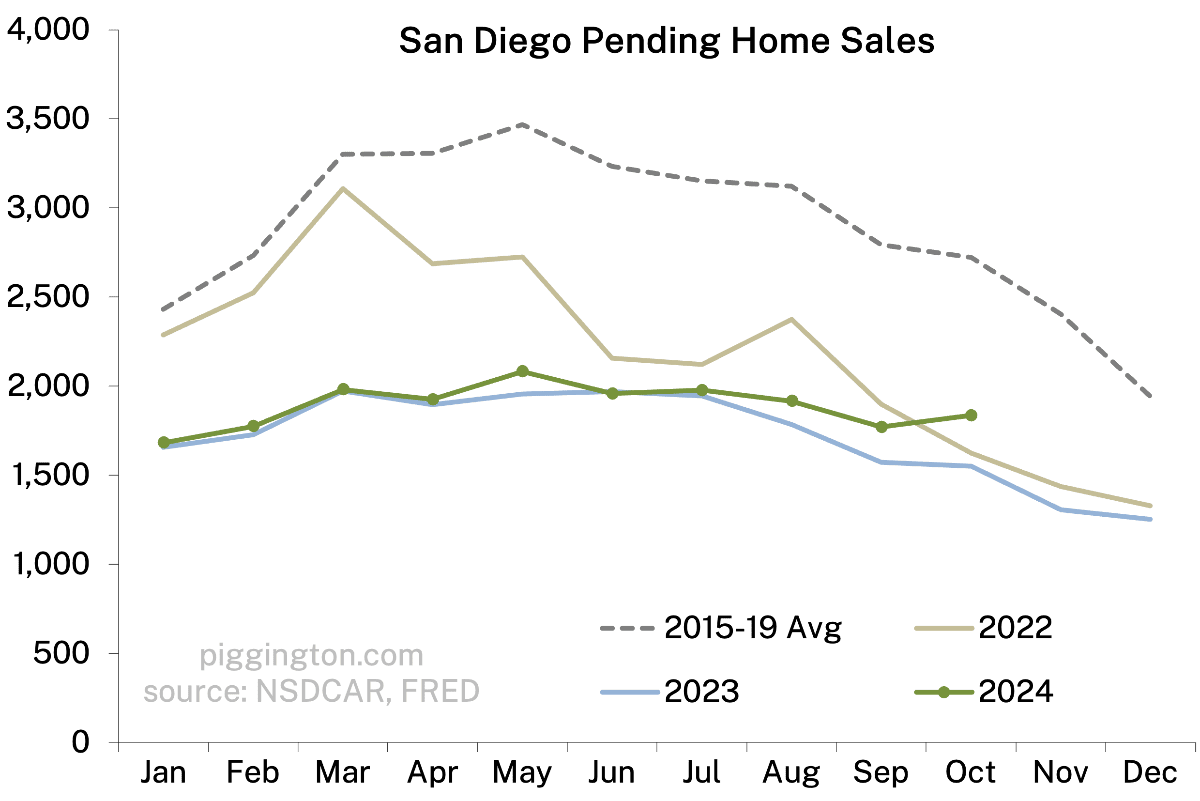

In some mildly good news for sellers, months of inventory pulled back a bit returning just about to the pre-pandemic average for the month of October:

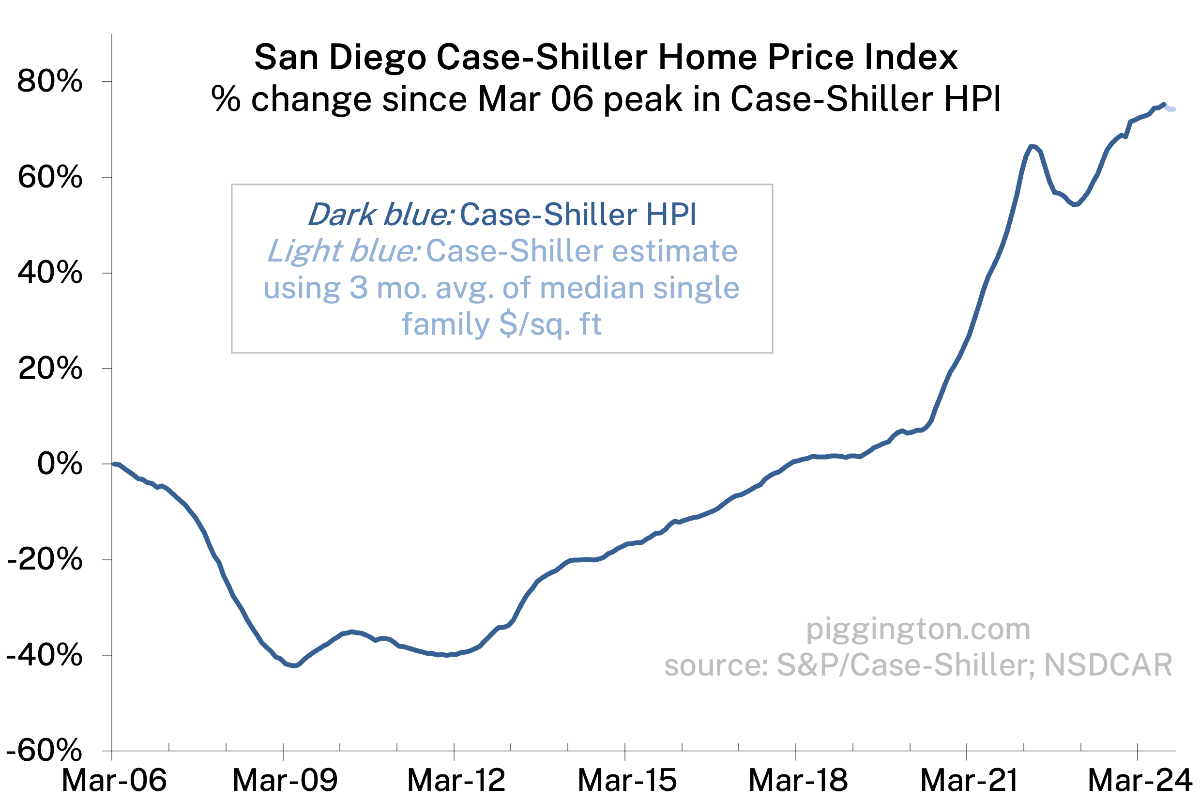

Prices bounced a bit, after a drop last month, after an increase the month before, and so on… they don’t seem to be going much of anywhere.

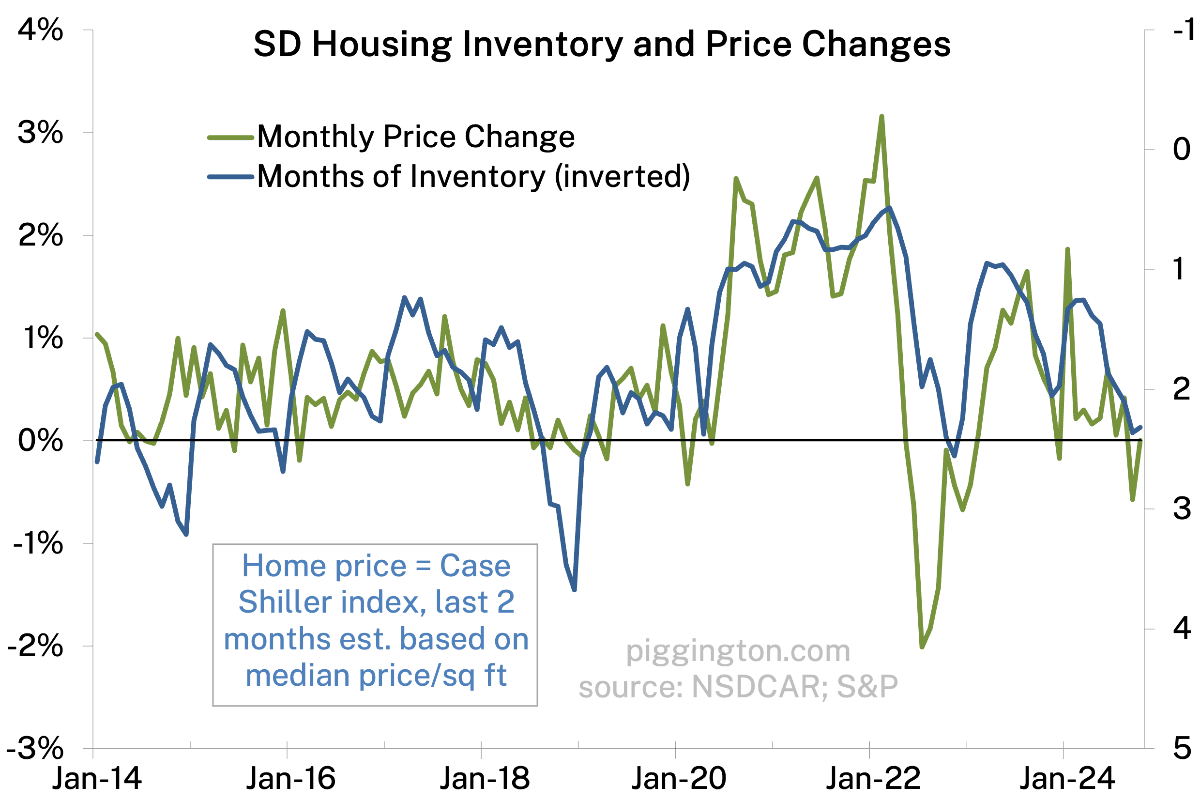

The past decade’s relationship between months of inventory and near-term price changes suggests that they will continue to not go much of anywhere for a bit:

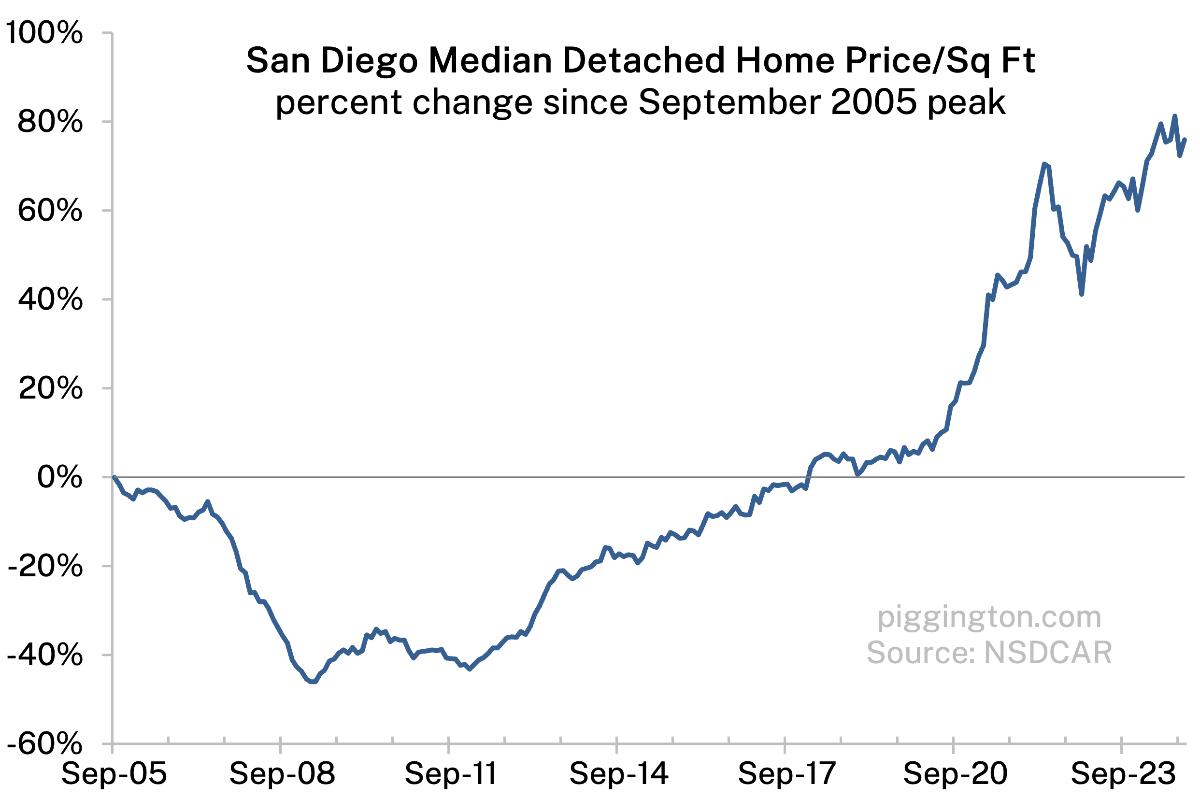

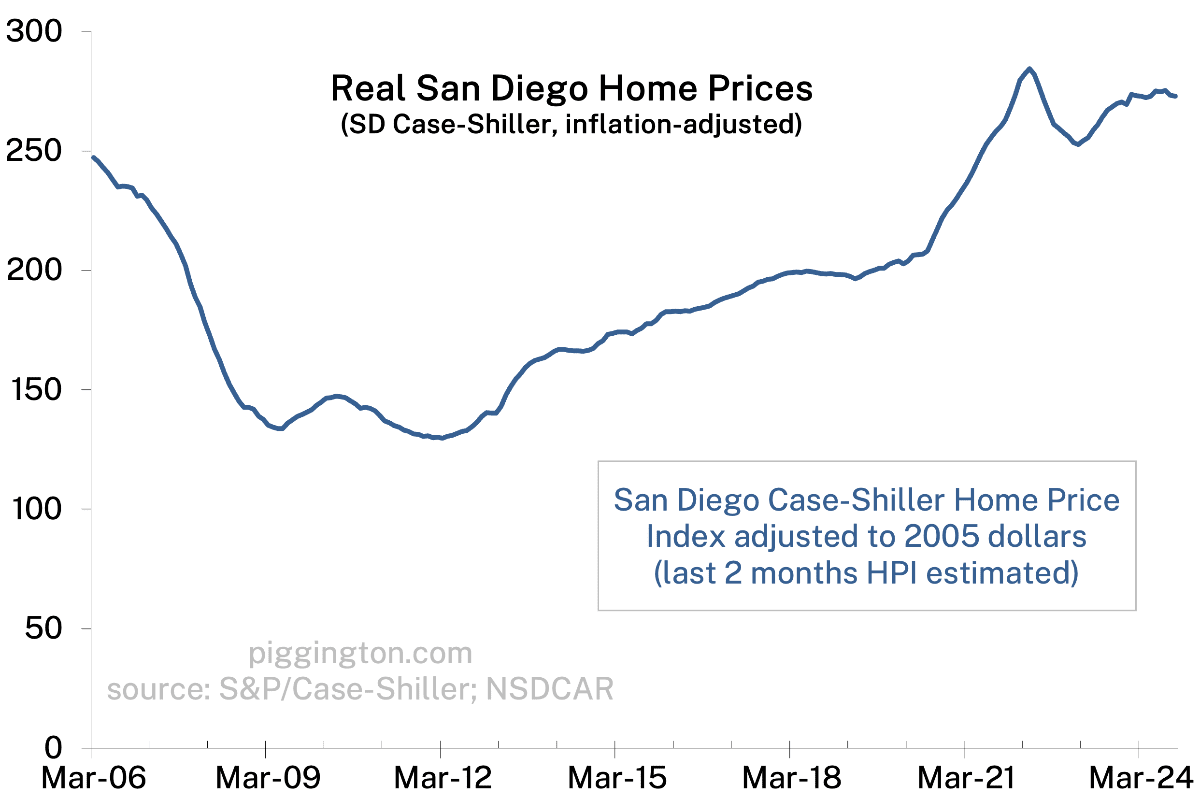

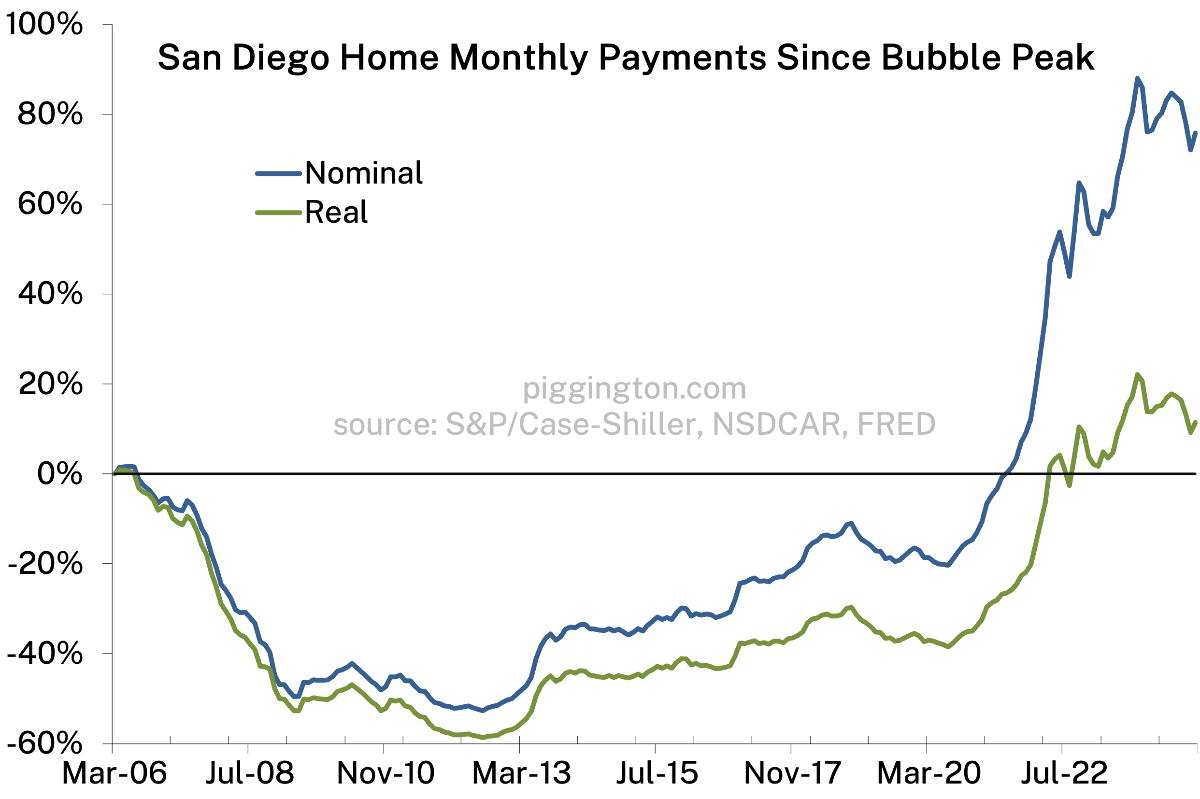

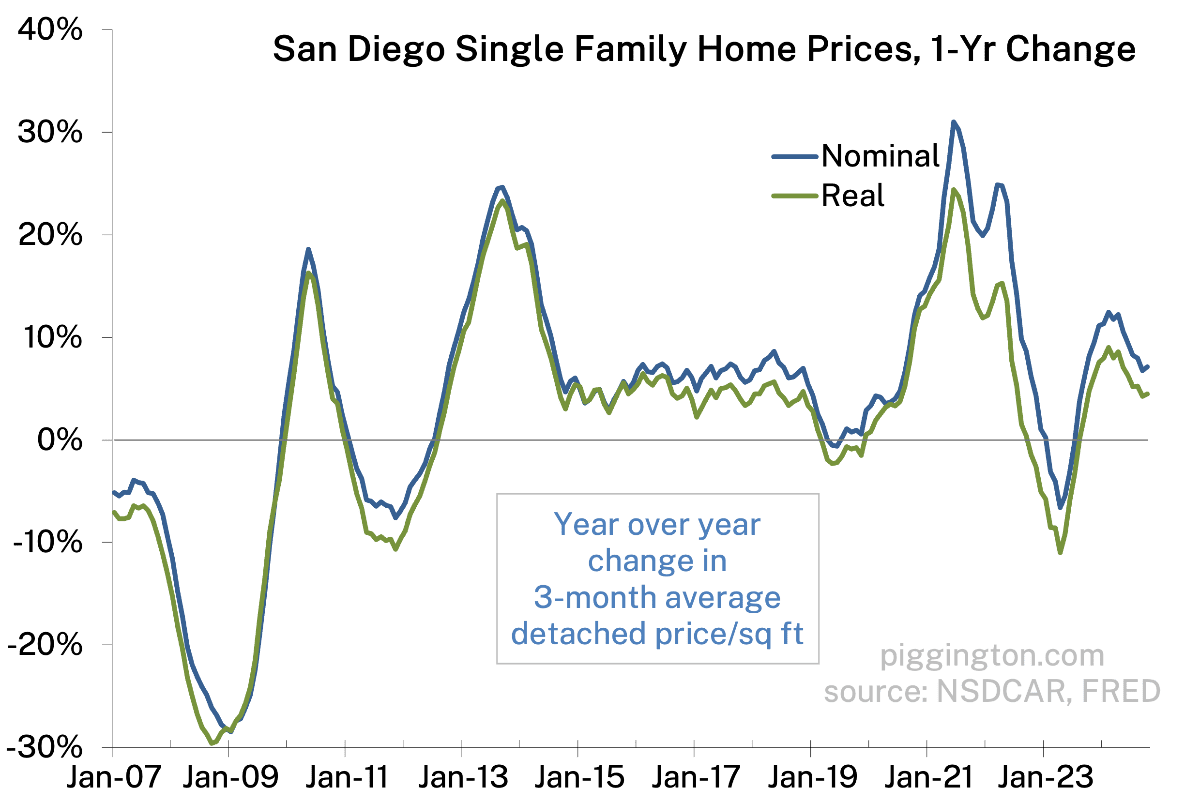

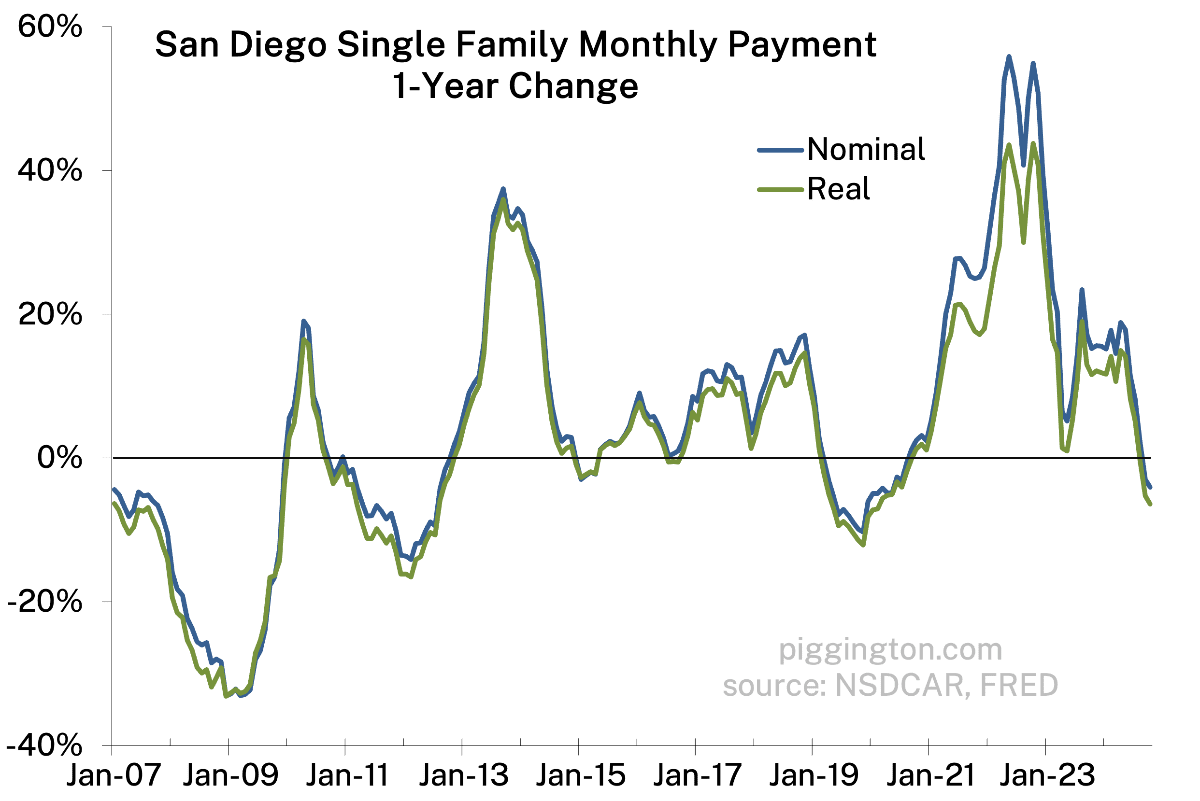

Longer term, inflation-adjusted prices and monthly payments remain very high:

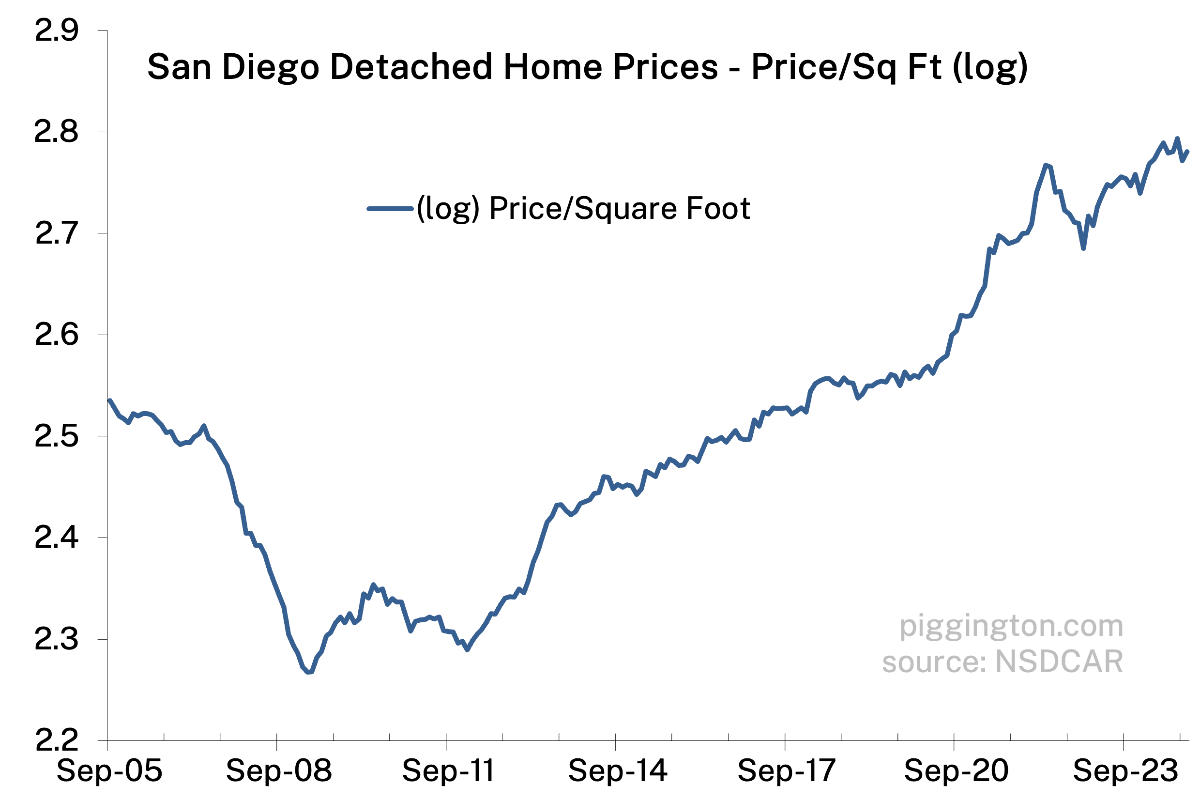

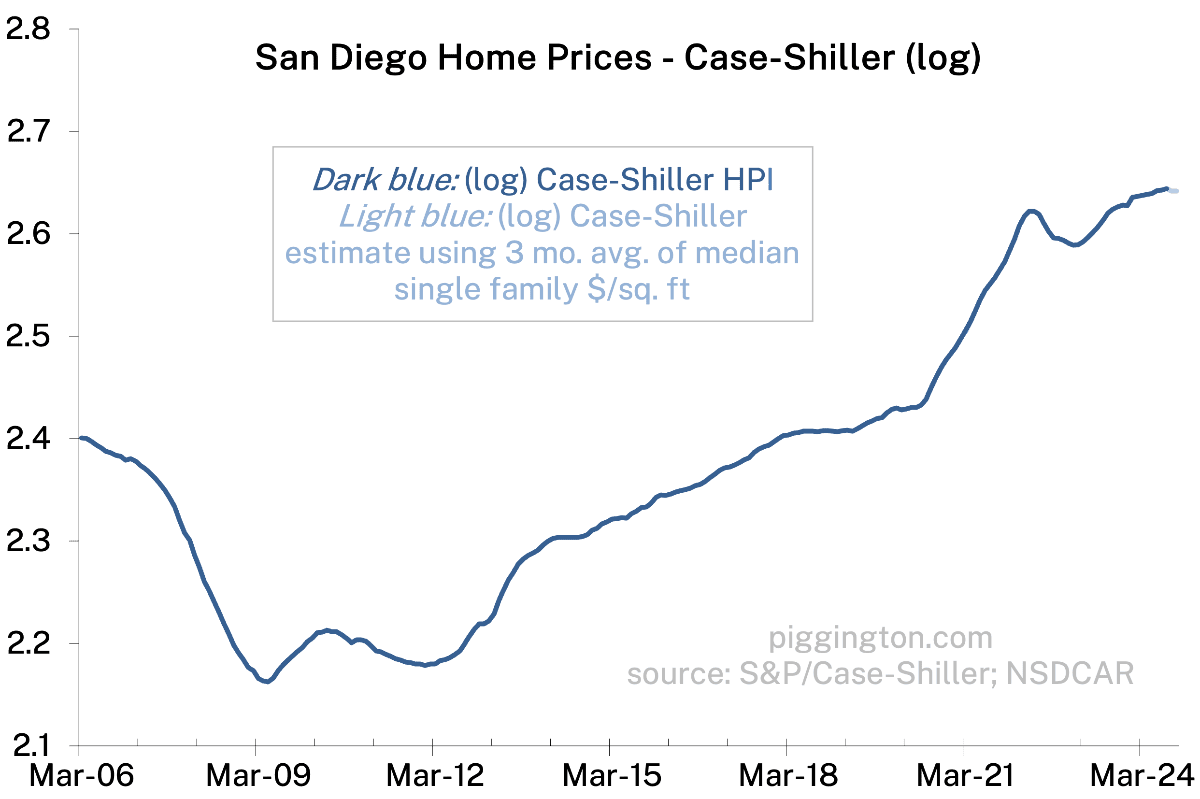

More charts below…

Thank you, Rich, for all the updates. The inventory has grown significantly since last year. With rates still high, what are your expectations for January? Last January, the market was iinsane due to such low inventory, but things started to shift as inventory levels increased in March.

Sorry, I don’t have a good answer to that one… I am kind of expecting more of the same, but I don’t really have a view on how things will change month to month. I guess the one thing I would note is that the recent pop in sales (which helped bring down months of inventory despite rising inventory) was aided by the decline in rates, which has since reversed… so we may see that months of inventory number continue to outpace the pre-pandemic norm.

Rates are an interesting thing right now. Looking back to 2012-2019, the Fed was goosing the economy with low rates to keep it from sinking. Now, they’re simply trying to keep the economy from overheating and goose it down every so often knowing they could unleash rampant speculation into fixed rate loans.

I see sideways action in SD and see rates as a lid.