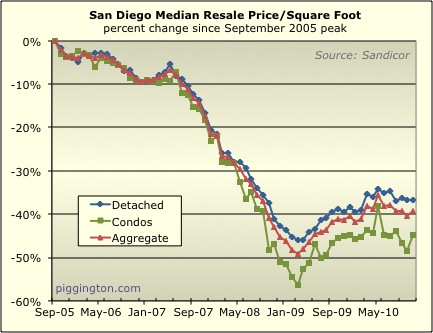

The median price per square foot for detached homes didn’t budge

between October and November. This fit nicely into the

“flat-to-down” home price thesis I’ve been

advancing in recent months. The 7.4% monthly rise in the condo

median made for quite a poorer fit to my theory, however.

The big move up in the condo price was enough to drag the aggregate

median price per square foot up by 1.8 percent for the month.

That said, the condo series tends to jump all over the place so it’s

never wise to make much of a single-month move there.

The plain vanilla median was actually up for both property types: 1.3%

for detached homes, 8.1% for condos, and 1.9% in aggregate.

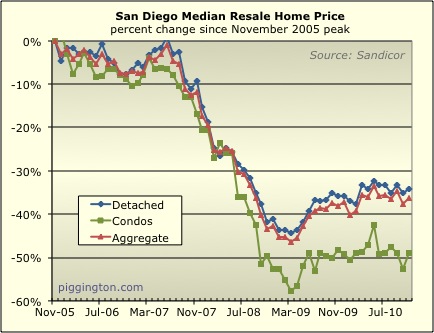

Last month sddude (I’ve decided to drop his extraneous u’s in casual

conversation) requested vertical lines on the price charts to better

evaluate seasonal effects. Thanks to a timely Microsloth Office

upgrade and some advice from Pigg AN, I was able to do that this

month. I created a separate chart so that I could start the time

series in January, making it a bit easier to visualize the seasons.

The spring bounce effect is pretty clear here. Even during the

freefall era, the rate of decline slowed a bit (though this is more

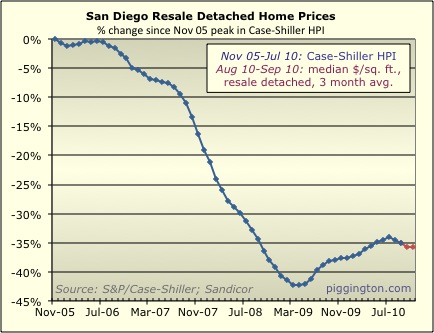

obvious on the Case-Shiller chart below).

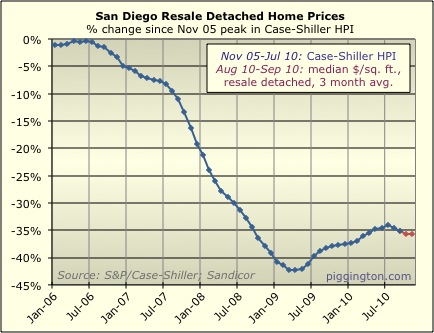

The official Case-Shiller index was down again in September; the

median-based estimate projects a further fall in the October CS index

but then a flattening in November.

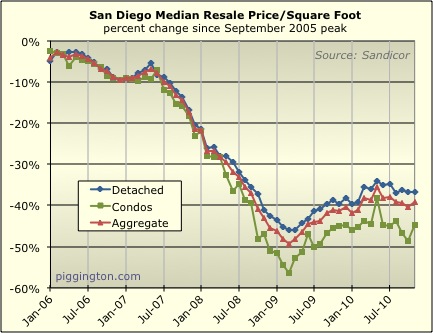

Here’s a calendar-year, vertical-lined look at the CS index since just

after the peak.

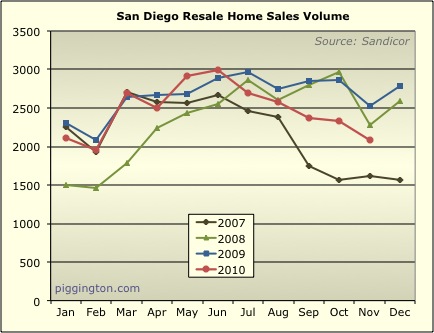

Closed sales declined for the month but this is a fairly typical

seasonal effect.

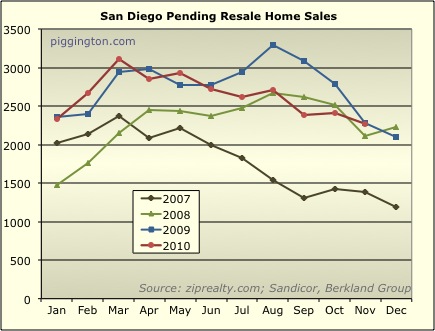

Pending sales were also down, which is also typical for November, but

the decline in pendings was quite a bit milder than that of closings.

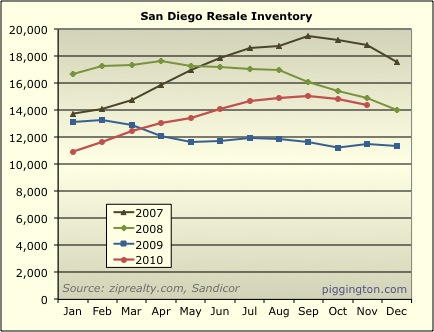

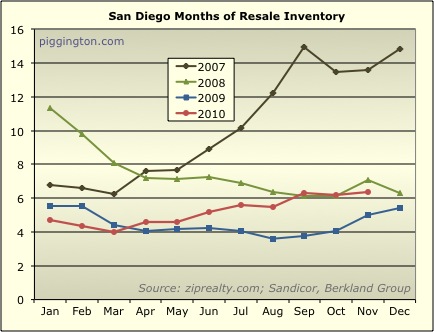

Inventory dropped again after having risen throughout the year until

September.

Months of inventory were ever so slightly up to about 6.3 months.

Aside from inventory at a level that does

not

portend aggregate price increases in the months ahead, the

market now has rising interest rates to deal with. In the past

month, per Freddie Mac, the average 30 year fixed mortgage rate has

gone from 4.17% to 4.61%. Sub-5% mortgages are still laughably

low, but that’s a fairly abrupt jump in rates. The specter of

higher rates could induce some potential buyers to pull the trigger in

the near term, but to the extent that higher rates last they can only

be a headwind to the market.

I firmly disagree with the idea that there is a one-to-one relationship

between rates and prices, such that if rates increase a certain

percent, prices should be expected to decline by that percent or

anywhere near it. The historical data clearly demonstrates that

there is no such correlation. However, there is no question that

sustained higher rates will reduce demand, all other thing being equal,

just as super-low rates have in recent times boosted housing activity

above what it otherwise would have been.

Anyway, the effect of the rate increase to date remains to be seen, but

even if there is no impact from rates, supply and demand levels imply

further stagnation ahead.

Thanks for the upgrade,

Thanks for the upgrade, RchTscn.

This must be a sad news,for

This must be a sad news,for having those progressive declines in the chart of price home detaches data.Maybe this this is also an indication of great mortgages and foreclosures.Just like what is happening right now,in US For too many earnest homeowners, mortgage loan modifications have been dangled, only to be snapped back and replaced by foreclosure. I found this here: False foreclosures More great news for homeowners According to the New York Times, a new thorn has emerged: fake house foreclosures. Imagine people who aren’t behind in their payments being singled out for foreclosure – locks changed, possessions claimed – and you’ve got the right idea.