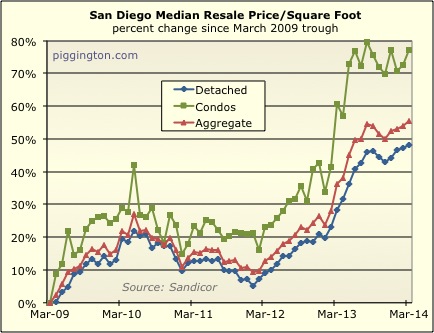

Prices edged up again last month:

Well, they more than edged up for condos, but I prefer the single

family series as it’s a lot less volatile. Even less volatile

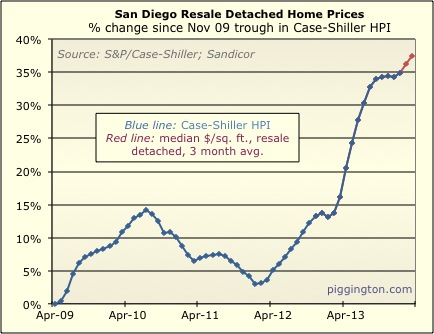

is the Case-Shiller proxy, which uses a 3-month average. This

was up .9% from the month prior, very similar to February’s

increase:

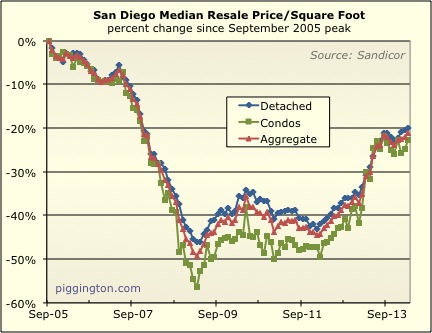

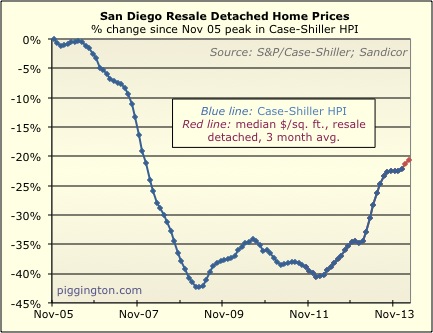

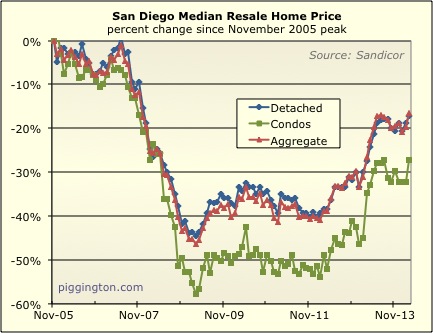

Here are the above two starting from the peak:

Here’s the overall median price:

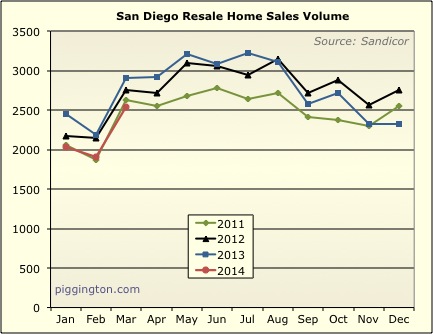

Closed sales were up a very typical amount for March, but are on the

low side of the range of the past few years, and a good amount lower

than during last year’s frenzy:

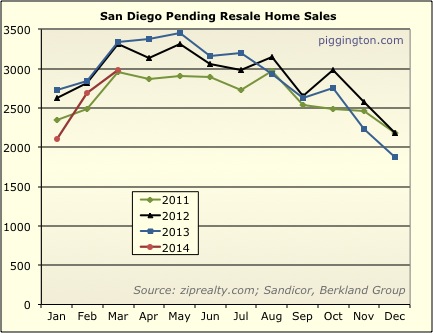

Ditto pendings:

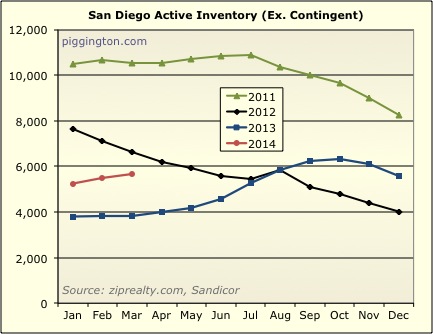

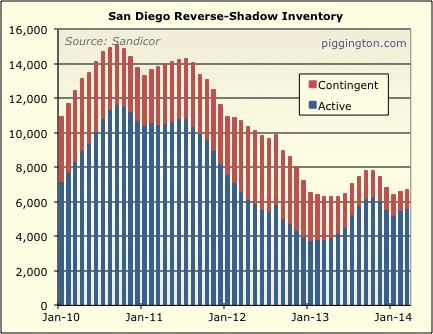

Inventory crept up but remains quite low:

Active-only inventory (no contingent) is still low, but quite a bit

above last year, and rising:

Look how little contingent inventory there is now compared to a

couple years back:

Here’s overall inventory back to 2007, showing how low we are in the

scheme of things:

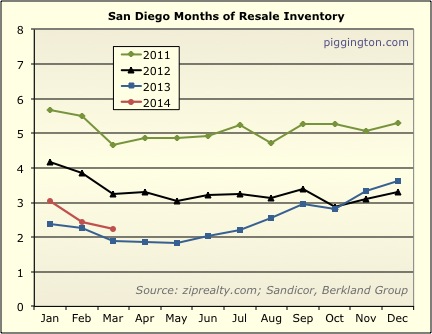

Months of inventory dropped due to the increase in sales, as usually

happens in March:

Months of inventory is above last year’s levels, but not by much,

and is extremely low compared to recent years:

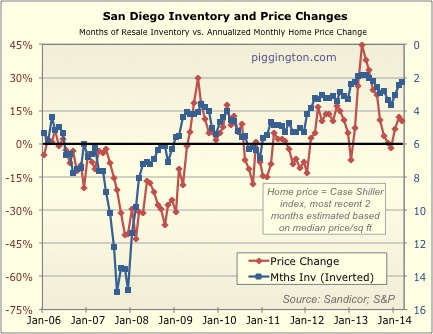

Here’s an overlay of months of inventory (inverted) and price

changes, showing that the two are well-correlated:

Here’s the same thing just using months of active inventory since

2010:

Both of these charts, and the low level of months of inventory,

suggest further upward pressure on prices immediately ahead.

Rich (or others),

Can you

Rich (or others),

Can you comment on your last line, “upward pressure on prices immediately ahead”. Specifically, what time frame did you have in mind for “immediately ahead”? 1 month, 1 year, 10 years? Or, in case you are tempted to write back, “What am I a fortune teller? How the heck would I know.”, let me answer the question in as slightly different way that might illicit a response:

Given the low inventory, how long might it take to get back to normal inventories? Is their historical precedents to look at? Or evidence of massive home construction programs that will provide relief? Why is the inventory low to begin with? As far as I know, the population of San Diego has not noticeably increased in the last 10 years.

This is not just of academic interest to me. I have a house to sell or rent out and am staying up nights trying to figure out what to do. Clearly, a nice problem to have, but a problem nonetheless (see my post on the subject if you are interested).

Thanks and keep up the analysis! It’s appreciated.

Dave

Hi Dave — No, it’s a

Hi Dave — No, it’s a reasonable question.

“immediately ahead” = the next few months or so

I don’t really know the answers to your sub-questions, but fwiw, this is how I look at it.

– The months of inventory data has typically been a pretty good indicator of the direction of prices immediately ahead, ie, within the next few months. But as soon as the supply/demand situation changes, the price pressures could change. So it tells you nothing about what will happen past that immediate timeframe… it just tells you whether supply/demand favors buyers or sellers right now.

– Looking into the distant future, ie several years or more, I think the valuation charts are probably a good indicator… that is to say, if valuations are high, they are more likely to drop, and if they’re low they’re more likely to rise. (Of course, valuations could eg drop without prices dropping, if prices just stagnated while the fundamentals caught up, but you get the idea).

So I’m pretty comfortable making forecasts on these two timeframes:

1. months of inventory gives an idea of which direction prices will move, and possibly to what degree, over the next few months

2. valuations give an idea of which direction valuations will move, and possibly to what degree, over the coming several years

What happens in between, I have no fricking clue.

Right now #1 says price pressure is to the upside, but that doesn’t really impact a decision of whether to sell or not. #2 says homes are pretty overpriced, but not nearly as badly as in the bubble. (Click through to the valuations link for a lot more detail on that…)

Hope this helps…

Rich