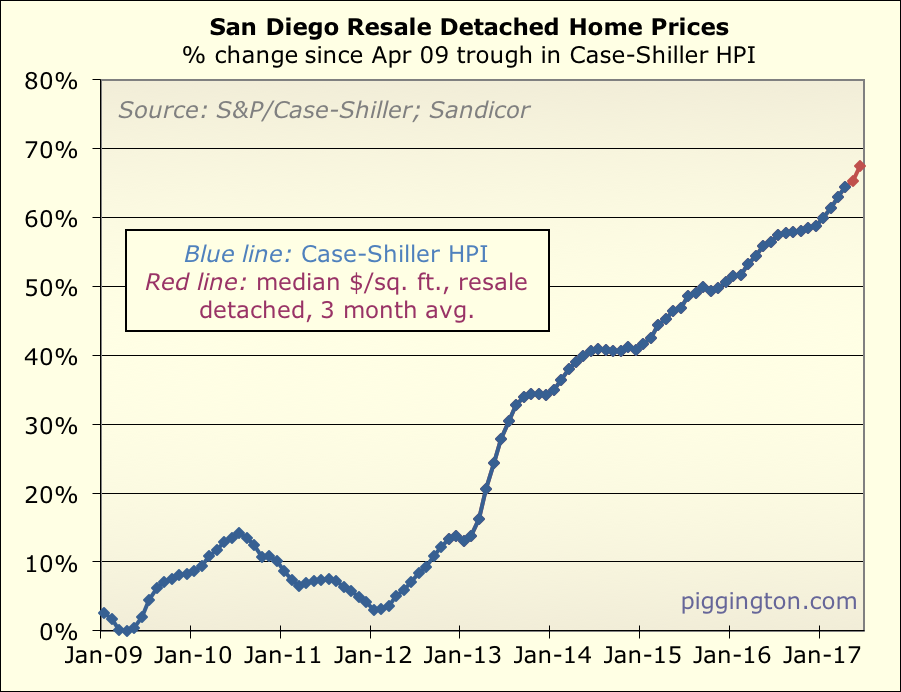

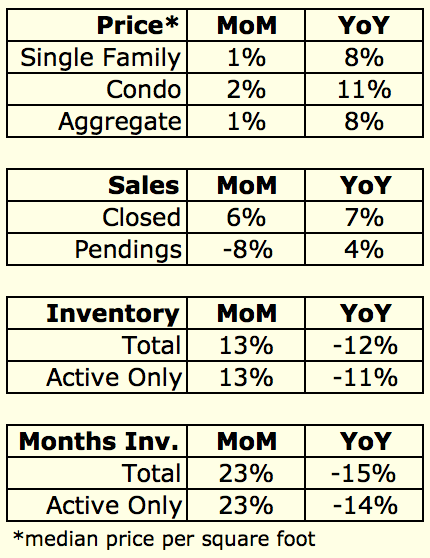

Home prices drifted further upward in June:

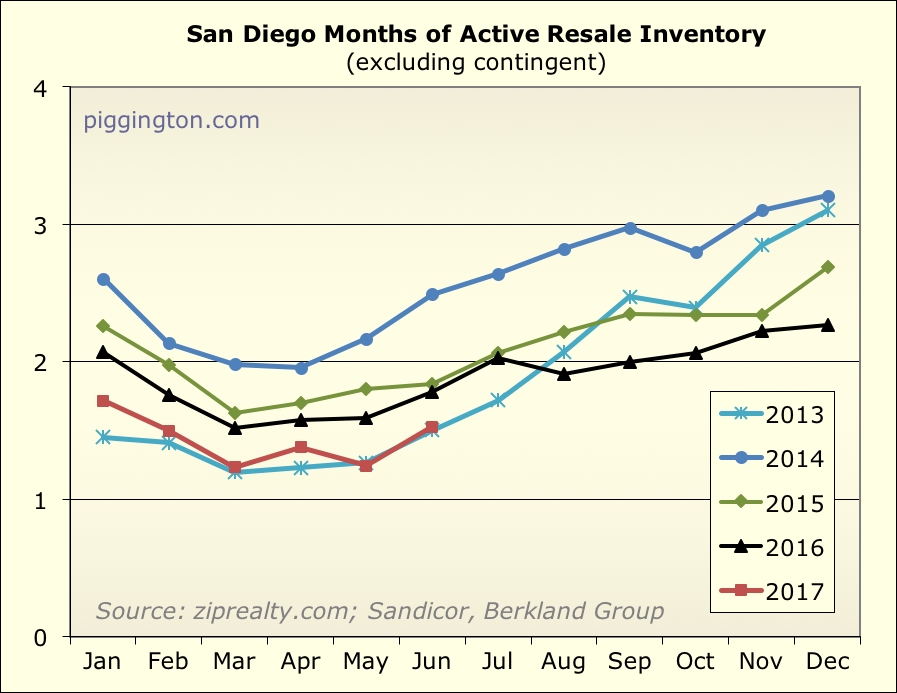

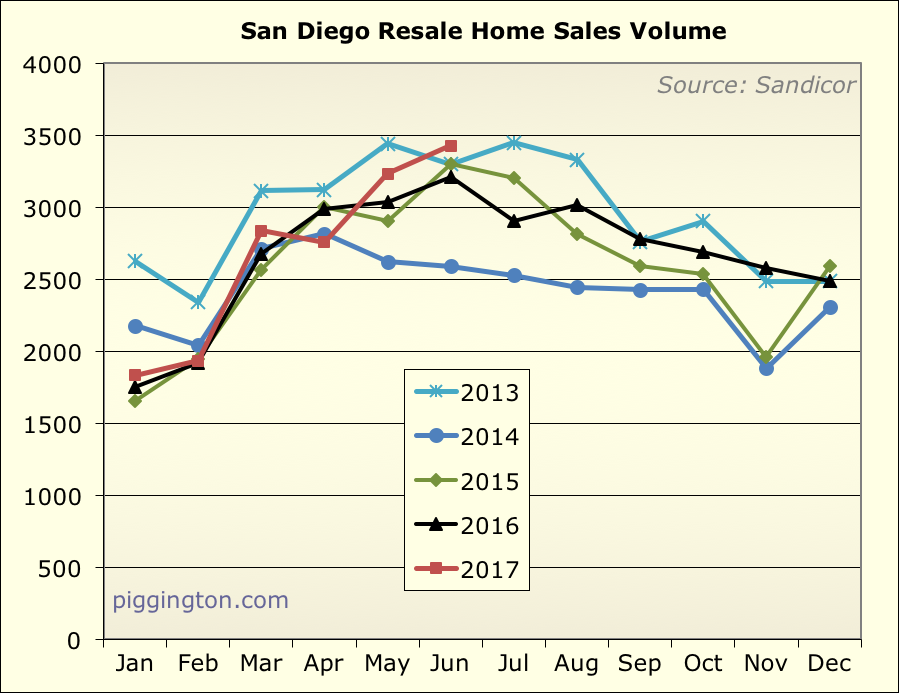

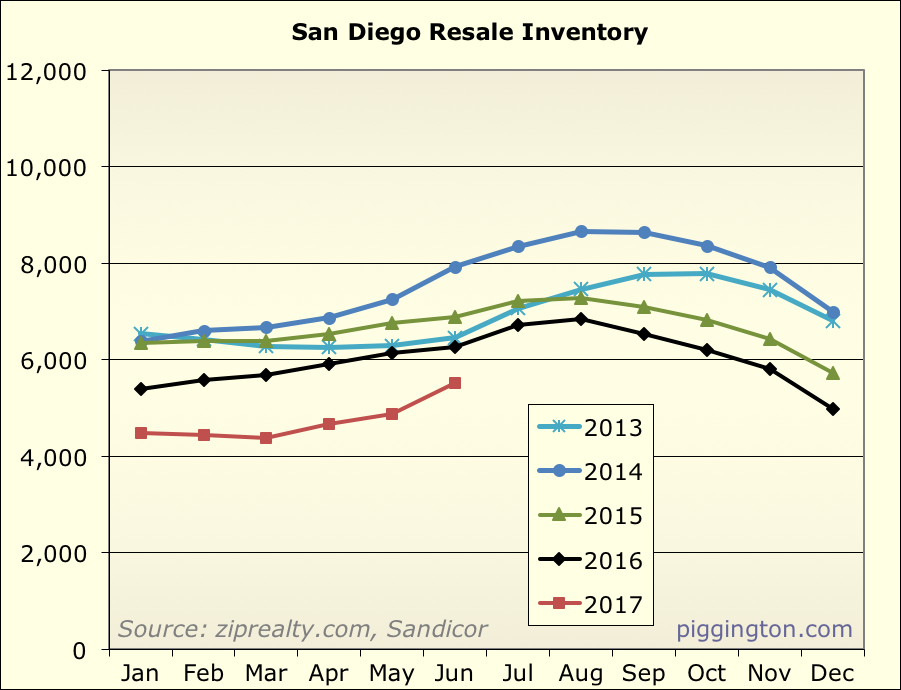

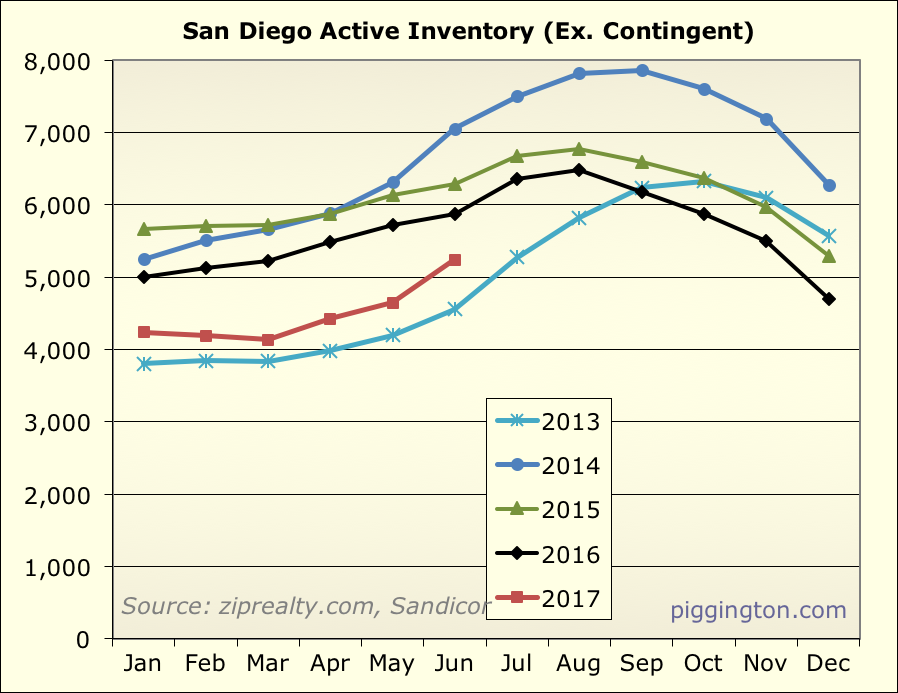

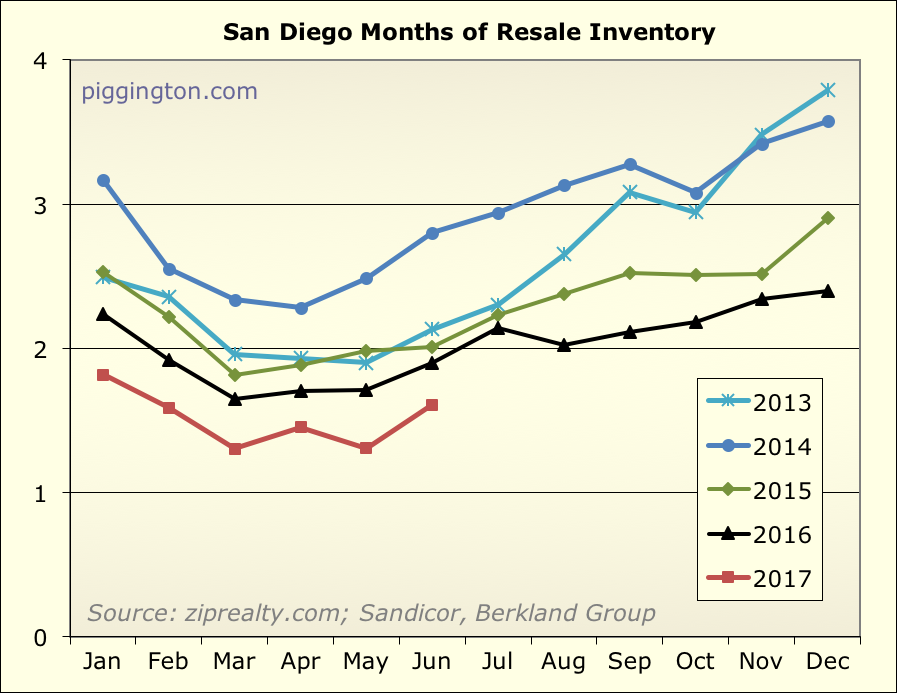

But in some good-ish news for potential buyers, inventory made a bit of

a comeback, with months of active inventory increasing from 1.3 to 1.6

months:

Interestingly, that’s the second month in a row that months of active

inventory was right on top of where it was in 2013. That year saw a

steep rise in inventory in the latter half of the year, but it was also

accompanied by a huge first-half price rise that brought out a lot of

sellers later in the year. The price increase this time around, while

solid, has not been nearly as big as in 2013.

Nonetheless, the 2013 months of inventory pattern has held up thus far.

We’ll see what the year has in store.

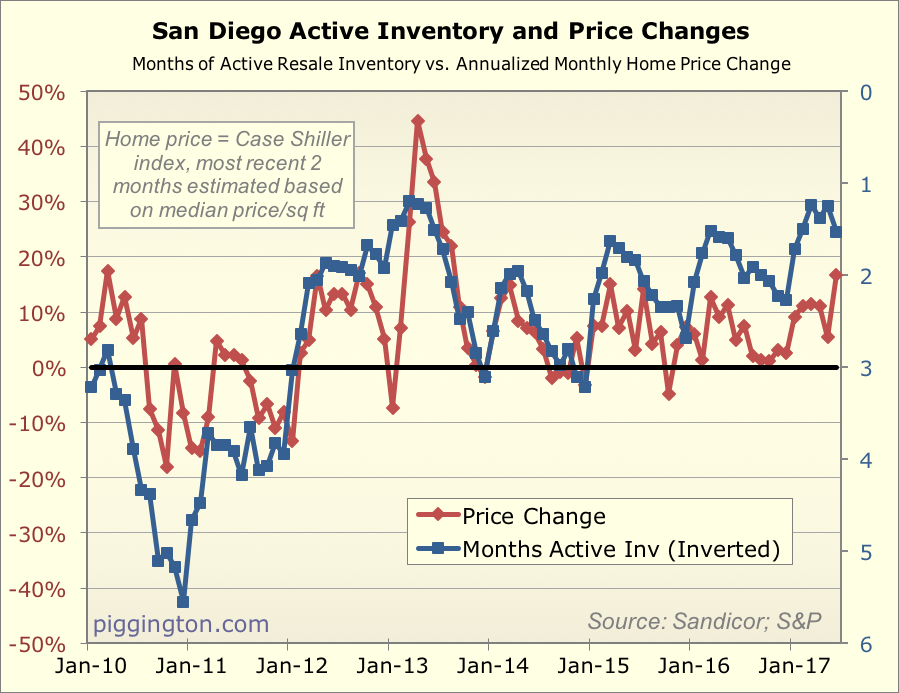

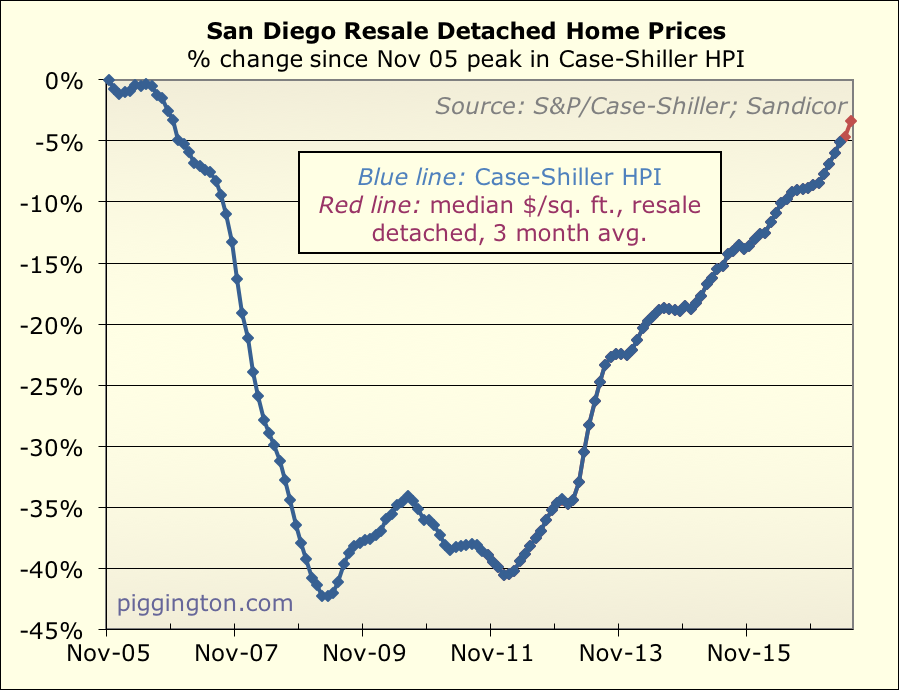

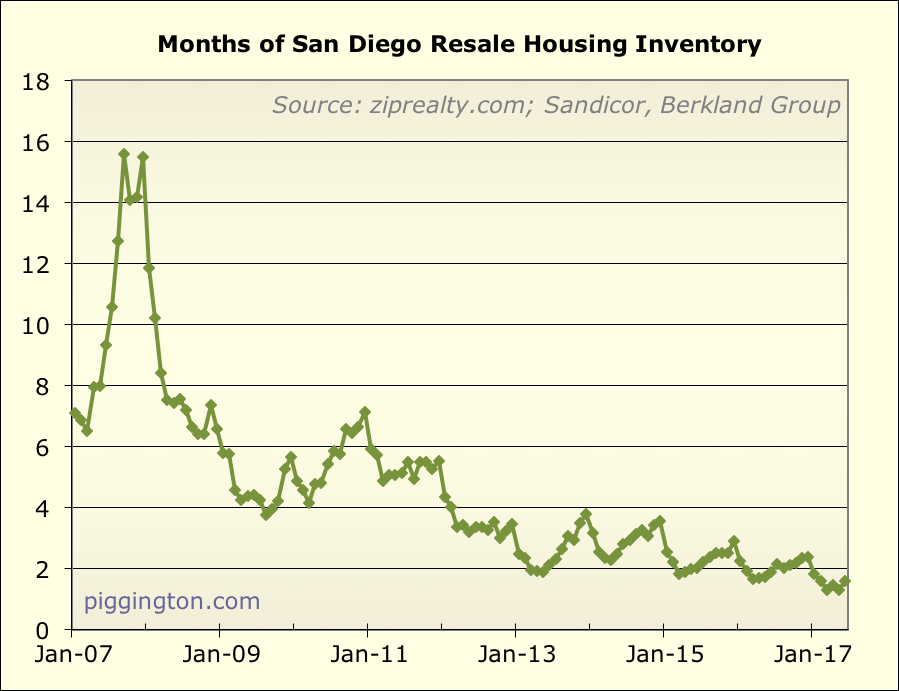

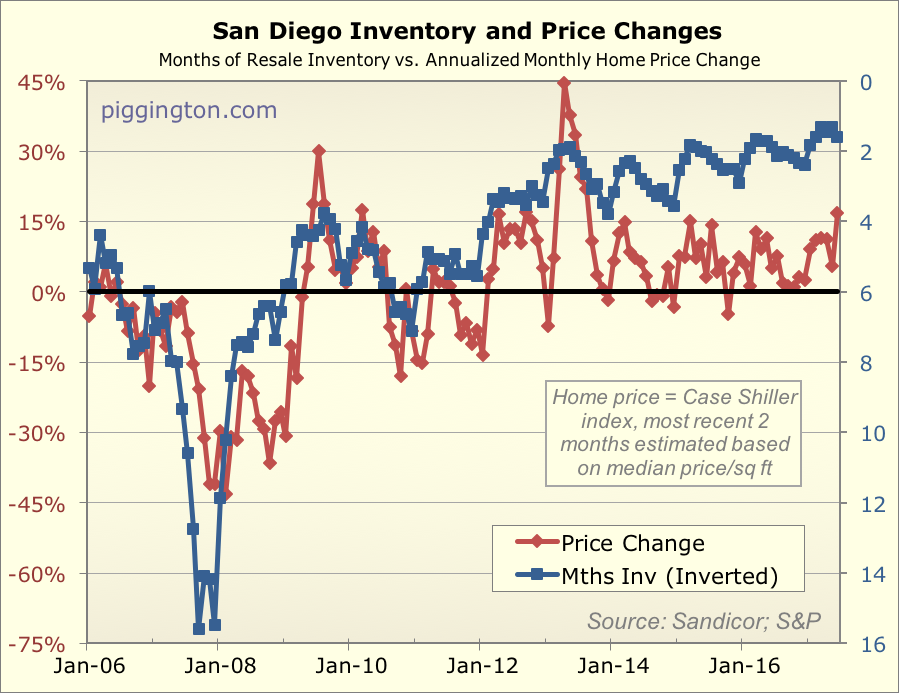

Here are price changes and months of inventory mapped together. This

puts the inventory improvement in perspective: it’s still a very

undersupplied market. Prices will likely be pressured further upward

unless this changes.

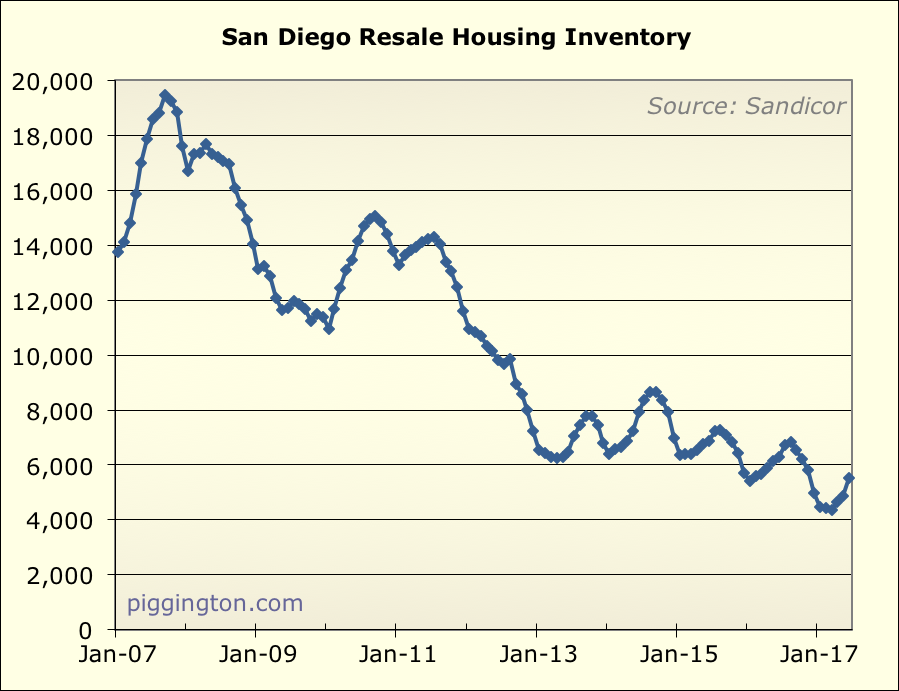

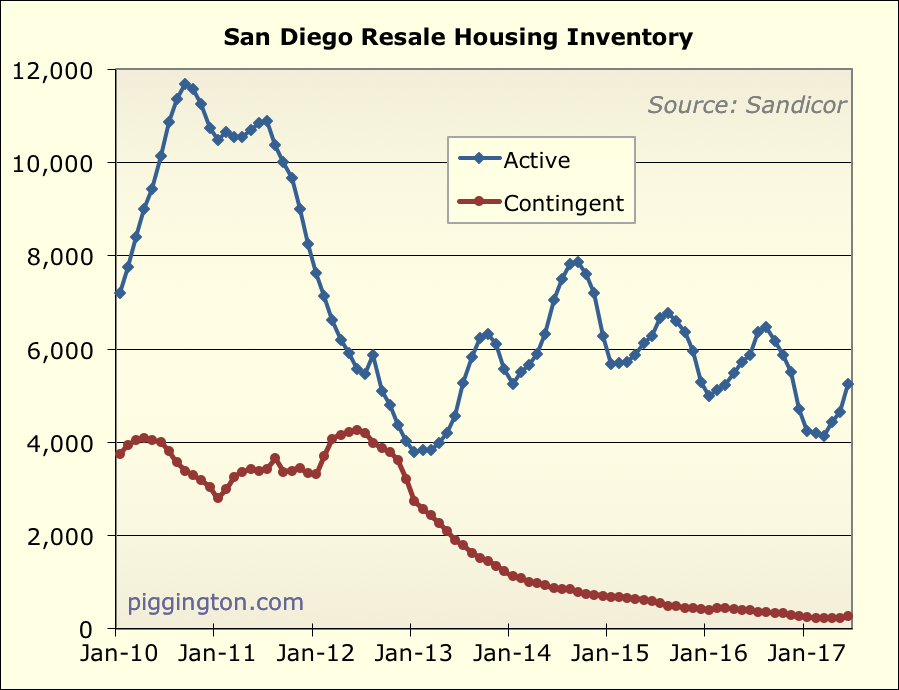

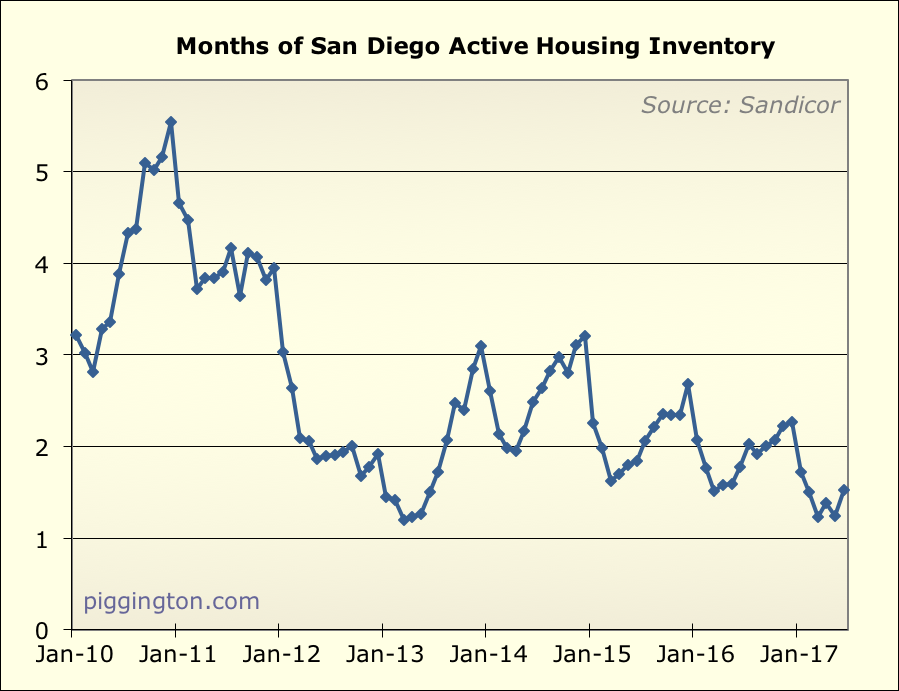

More charts below. One technical note: the MLS property database has

started to include San Diego properties listed in other MLS systems.

This resulted in a small (~3%) boost to inventory and sales in recent

months. It doesn’t impact the months of inventory ratio, but sales and

inventory figures on their own are a bit higher than they would have

been otherwise. Keep that in mind when making historical comparisons.

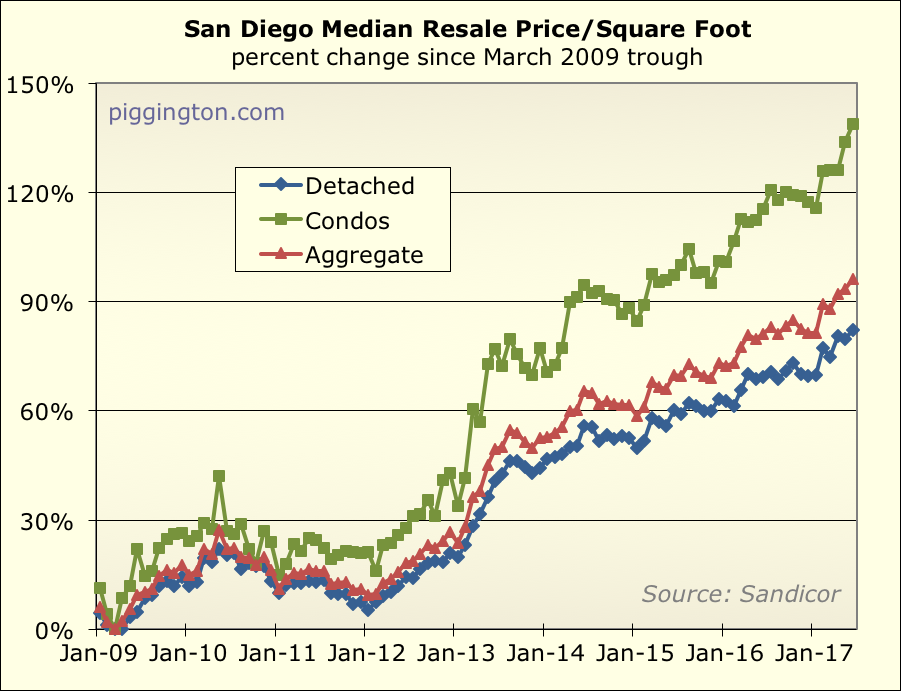

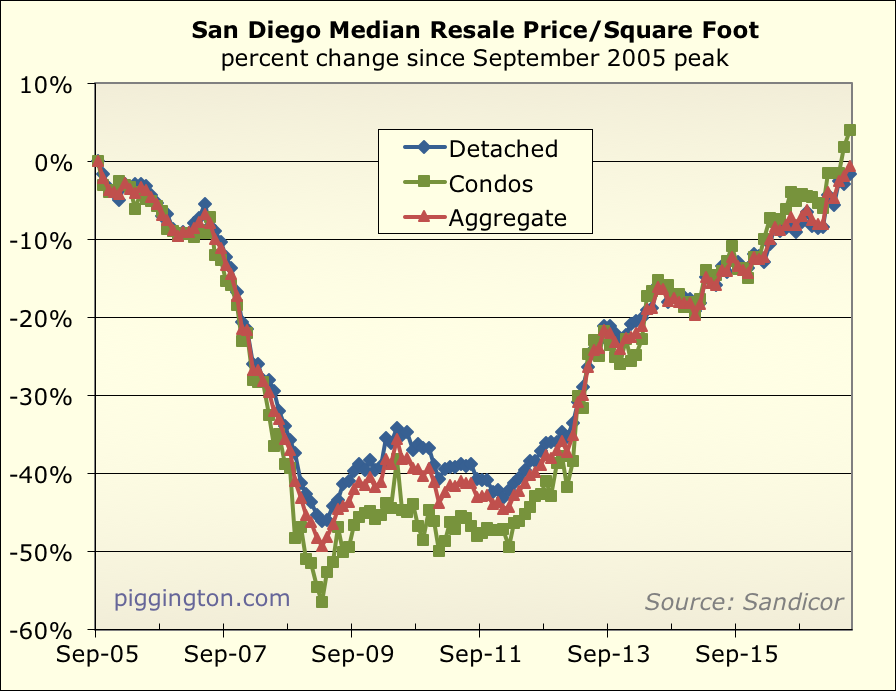

Interesting that the

Interesting that the price/sq. ft. for condos is actually higher than it was at the last peak and yet prices are lower. Is the average condo smaller these days? or is it just that the smaller ones are selling easier because they are cheaper? If one looks solely at price/sq. ft. then it looks like we are back at the peak, of course this doesn’t take inflation into account.

The median condo price is

The median condo price is right back at the peak at this point, so it’s a pretty small disparity fwiw (about 4%).

Thanks for the updated info.

Thanks for the updated info. Looks like Month over Month is the biggest jump in the past 30 or so months, or tied for it. And year over year is now double digits for condos and ticked up to 8% for houses.

Looking forward, I think strong price increases are still likely based on the following:

1. Mortgage payments remain low compared to rent

2. San Diego increases are not just lagging SF and LA, but also a lot of other 2nd tier markets like Seattle, Denver, etc.

3. Ultralow resale supply and very low new construction.

So my prediction is continued strong increases this year and next, but perhaps moderating in 2019 as valuations start to better reflect rent.

On the other hand, one year after another of steady profits for home buyers can be fuel for aggressive lending and speculation, so perhaps 2019 will not be the year of the moderation, but the start of bubble valuations.

Zillow says my place

Zillow says my place increased in value while Redfin says it decreased, doesn’t really matter to me as I’m not taking any equity out or selling.

… aaaaaand, we’re assuming

… aaaaaand, we’re assuming constant growth, forever. US has pretty much never gone 10 years w/o a recession, and we’re on year 8.

Much of the stimulus response

Much of the stimulus response from the 2008 recession is still working through the system.

My low interest rates are fixed for 30 years.

Your payment for the next 30

Your payment for the next 30 years has little to do with whether your home is worth a given price. The only thing that matters is the buyer’s payment or ability to pay.

Ok, let’s look at that.

I

Ok, let’s look at that.

I bought my home in 2013 for 580K, a home across the street is listed at 1.1M

My payment is $1780/month + property tax. Rate is 3.1% 30 yr fixed.

So for a payment less than a 2BR apartment today, I live in a 1M+ home.

If I bought today, the payment would be at least $2,400/month more.

So every month I live here, I have imputed income of $2,400 which I can spend elsewhere. And of course I’m not the only one, there are millions more like me who are loathe to move.

So in that sense, I have almost 30K of stimulus over the next 29 years (did refi after Brexit in 2016).

I get your point about today’s home worth, but I really don’t care. I live a great lifestyle at a modest cost. Hope this makes sense.

More to the point, my other spending perhaps makes up for some of the lack of spending who have to spend a greater portion of their income on housing.

But what about your

But what about your opportunity cost? That 1M+ asset could easily generate $4000+/month in tax free income. So the way I look at it is you are paying a price to own and live in that home. And don’t forget your maintenance costs on the deteriorating asset.

Perhaps putting the equity into a tax free money making bond fund will let a person live for free in their rented home. I am assuming you have quite a bit of equity and could leverage to get the full 1M+ buying power.

Yes, I am a renter. I wuold say you are ‘spending’ $50K+/year to live in your home.

Just interviewed a lady today

Just interviewed a lady today for a position.

She moved to SD from Seattle.

She had an offer on her house before they put their bags in their car as they were leaving.

They got a nice premium which would allow them to pay cash in Vista.

She said she was going to talk with her friends about how much more value one gets in SD vs Seattle and encourage them to move as well.