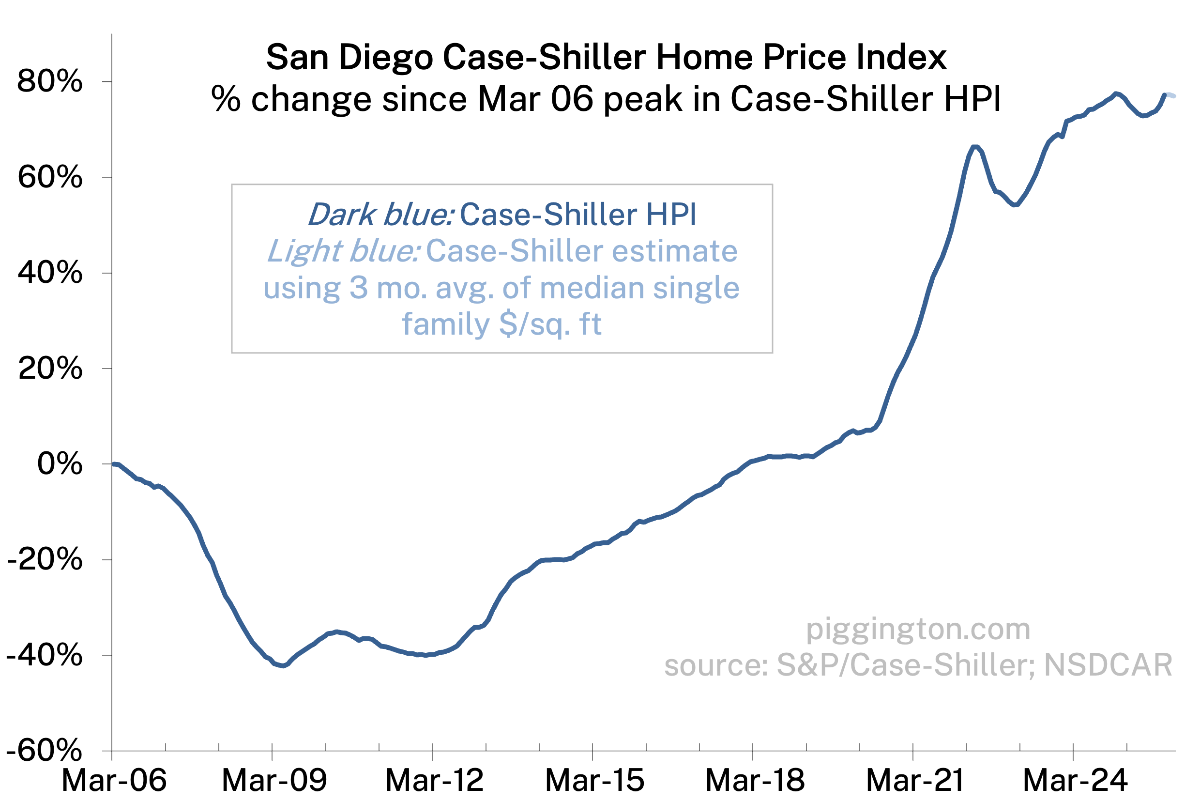

Hi – My view is that there will be a long slog of prices going nowhere until affordability improves quite a bit (basically allowing incomes to catch up). If there’s a serious economic downturn that could speed things along and result in sharper price declines for a bit. But I think the base case is a long period of (nominal) price stagnation.

I think we have had a bout 4 years of slogging already with mostly flat prices in the face of continued wage inflation. A little more wage inflation and some help with interest rates and affordability should return in a few more years. Like Ive always said there is nothing more powerful than the passage of time. What seems impossible becomes reality through the passage of time

PBDude

1 month ago

Thanks for the data update Rich. I am curious as to your opinion of the different (imho) mostly wacky housing market ideas that have popped up recently:

50 year mortgagesBanning institutional (more than 100 properties) investorsPortable mortgagesAssumable mortagesOpening Federal Land to housing development401k for down paymentsFederal Reserve MBS program to push down ratesTightening FHA residency standardsSpeeding up HUD salesMost of the above to me feel like financial engineering to prop up a market but don’t solve the underlying issue. None seem like they would impact SD significantly

Agreed with your general take on a lot of these… anything that subsidizes demand isn’t going to improve affordability.

These all seem to fall into the category of subsidizing demand:

401k for down payments

Federal Reserve MBS program to push down rates

50 year mortgages

Banning instituitions is a nothingburger, because they own just a tiny fraction of homes. Popular scapegoat that isn’t backed by the data.

The ones that seem like they could move the dial are mortgage portability and assumability. The mortgage lock-in is a big factor behind low for sale inventory. Those two (esp portability) could really unleash a lot of inventory.

I don’t know enough to comment on the others you mentioned.

Another one I’ve seen mentioned is reducing the capital gains tax. This could also have a big impact on (though at an obvious cost of lost tax revenue).

One thing worth noting on all these is that the main way to really restore affordability is for home prices to decline — and this is not a desirable outcome for a lot of people!

Politicizing corporate ownership of SF homes is sexy but a myth here in SD and most of coastal SoCal. Most SFR rentals are owned by mom and pop landlords actually nearly all. And if you dont believe me its about the easiest possible to prove. Search for the 10 largest owners of SFR rentals in the USA. Then go to their websites where they rent their homes out. Search for a rental in SD. You will find virtually none because they dont own them! Some bought a small handful a decade or so ago until quickly realizing the price vs rent equation made no sense here for corporate ownership of homes outside of apartment complexes

I’ll give yoou a head start with the two biggest

Progress residential. They list none in California

I agree with you both on all accounts. On corporate ownership specifically, the most useful view would be a distribution plot of properties owned per entity after rolling up related LLCs, because “investor-owned” is not the same thing as “large institutional.” Nationally, the biggest institutional players are a small slice of the overall single-family stock (under 1% of all SFH), even if investors as a broad category can be a meaningful share of purchases in a given quarter.

My guess is San Diego’s long history as a vacation/second-home market means it was “investorized” earlier, with a larger share of rentals held by smaller owners (1-10) versus markets where the recent surge was more tied to post-2008 institutional scaling. I think investor appetite in SD continues to and will always be strong, so if we want policy that actually targets the behavior that shows up in pricing pressure, we would be better served to look at incentives/penalties that scale with portfolio size and designed to be hard to evade via entity splitting. But it’s more politically palatable to attack big corpos than ‘Mom and Pop’, so here we are.

One drag on prices that I don’t think gets enough attention is insurance costs. They are rising quickly! Our HOA insurance policy went up over 40% in just the 2 years I was on the board. This will highlight the risks of owning a home here and I think over time help to fight the notion of housing as a great investment thus helping to lower prices.

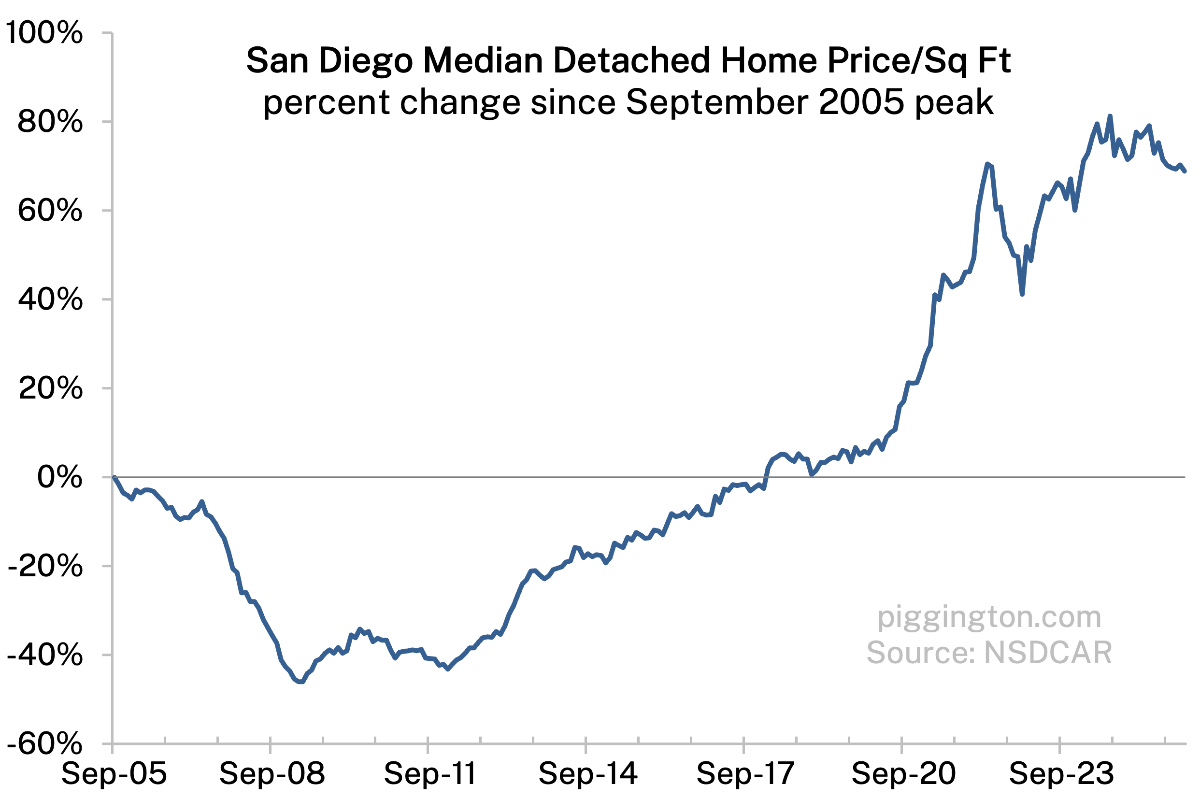

Thanks as always Rich! Looks like things are holding steady for the last few months.

Do you have a feel if one side or the other is going to give?

Hi – My view is that there will be a long slog of prices going nowhere until affordability improves quite a bit (basically allowing incomes to catch up). If there’s a serious economic downturn that could speed things along and result in sharper price declines for a bit. But I think the base case is a long period of (nominal) price stagnation.

I think we have had a bout 4 years of slogging already with mostly flat prices in the face of continued wage inflation. A little more wage inflation and some help with interest rates and affordability should return in a few more years. Like Ive always said there is nothing more powerful than the passage of time. What seems impossible becomes reality through the passage of time

Thanks for the data update Rich. I am curious as to your opinion of the different (imho) mostly wacky housing market ideas that have popped up recently:

50 year mortgagesBanning institutional (more than 100 properties) investorsPortable mortgagesAssumable mortagesOpening Federal Land to housing development401k for down paymentsFederal Reserve MBS program to push down ratesTightening FHA residency standardsSpeeding up HUD salesMost of the above to me feel like financial engineering to prop up a market but don’t solve the underlying issue. None seem like they would impact SD significantly

Agreed with your general take on a lot of these… anything that subsidizes demand isn’t going to improve affordability.

These all seem to fall into the category of subsidizing demand:

Banning instituitions is a nothingburger, because they own just a tiny fraction of homes. Popular scapegoat that isn’t backed by the data.

The ones that seem like they could move the dial are mortgage portability and assumability. The mortgage lock-in is a big factor behind low for sale inventory. Those two (esp portability) could really unleash a lot of inventory.

I don’t know enough to comment on the others you mentioned.

Another one I’ve seen mentioned is reducing the capital gains tax. This could also have a big impact on (though at an obvious cost of lost tax revenue).

One thing worth noting on all these is that the main way to really restore affordability is for home prices to decline — and this is not a desirable outcome for a lot of people!

Politicizing corporate ownership of SF homes is sexy but a myth here in SD and most of coastal SoCal. Most SFR rentals are owned by mom and pop landlords actually nearly all. And if you dont believe me its about the easiest possible to prove. Search for the 10 largest owners of SFR rentals in the USA. Then go to their websites where they rent their homes out. Search for a rental in SD. You will find virtually none because they dont own them! Some bought a small handful a decade or so ago until quickly realizing the price vs rent equation made no sense here for corporate ownership of homes outside of apartment complexes

I’ll give yoou a head start with the two biggest

Progress residential. They list none in California

https://rentprogress.com/homes-for-rent

Invitation Homes- they currently have one house for rent in Chula Vista

https://www.invitationhomes.com/search/houses-for-rent

House for rent at 1869 Petaluma Drive.

https://www.zillow.com/homedetails/1869-Petaluma-Dr-Chula-Vista-CA-91913/59312362_zpid/

that house was last sold (to them in 2013)

Corporate ownership of single family rental homes is a myth in SD County.

I rest my case

I agree with you both on all accounts. On corporate ownership specifically, the most useful view would be a distribution plot of properties owned per entity after rolling up related LLCs, because “investor-owned” is not the same thing as “large institutional.” Nationally, the biggest institutional players are a small slice of the overall single-family stock (under 1% of all SFH), even if investors as a broad category can be a meaningful share of purchases in a given quarter.

My guess is San Diego’s long history as a vacation/second-home market means it was “investorized” earlier, with a larger share of rentals held by smaller owners (1-10) versus markets where the recent surge was more tied to post-2008 institutional scaling. I think investor appetite in SD continues to and will always be strong, so if we want policy that actually targets the behavior that shows up in pricing pressure, we would be better served to look at incentives/penalties that scale with portfolio size and designed to be hard to evade via entity splitting. But it’s more politically palatable to attack big corpos than ‘Mom and Pop’, so here we are.

One drag on prices that I don’t think gets enough attention is insurance costs. They are rising quickly! Our HOA insurance policy went up over 40% in just the 2 years I was on the board. This will highlight the risks of owning a home here and I think over time help to fight the notion of housing as a great investment thus helping to lower prices.

https://piggington.com/inventory-declines-but-still-on-the-high-side-prices-weaken/#comment-68619

I agree