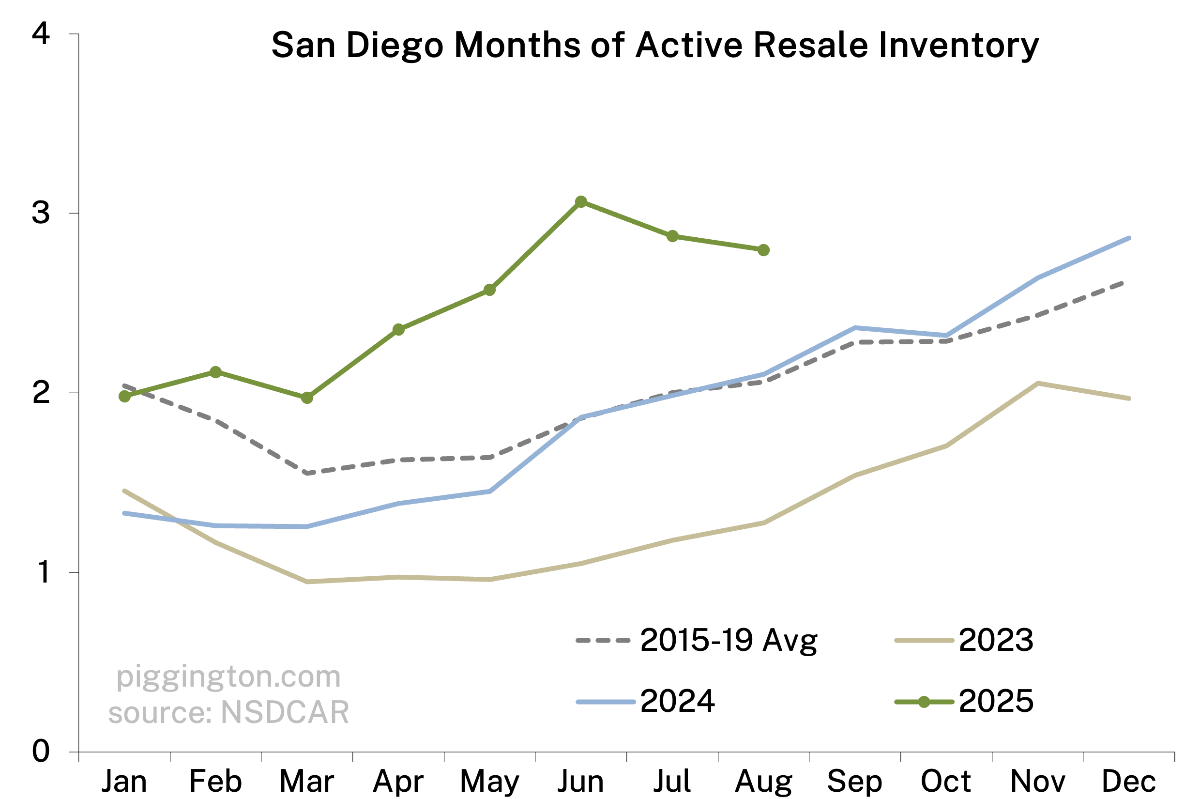

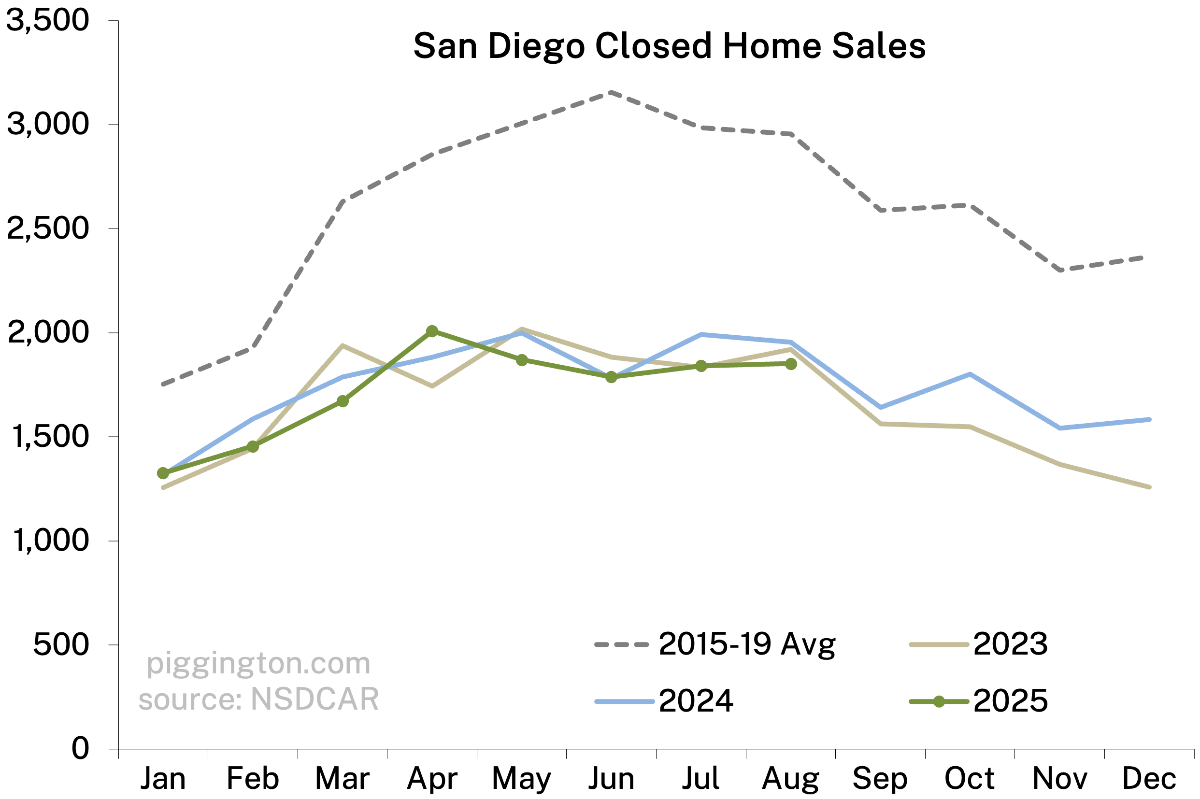

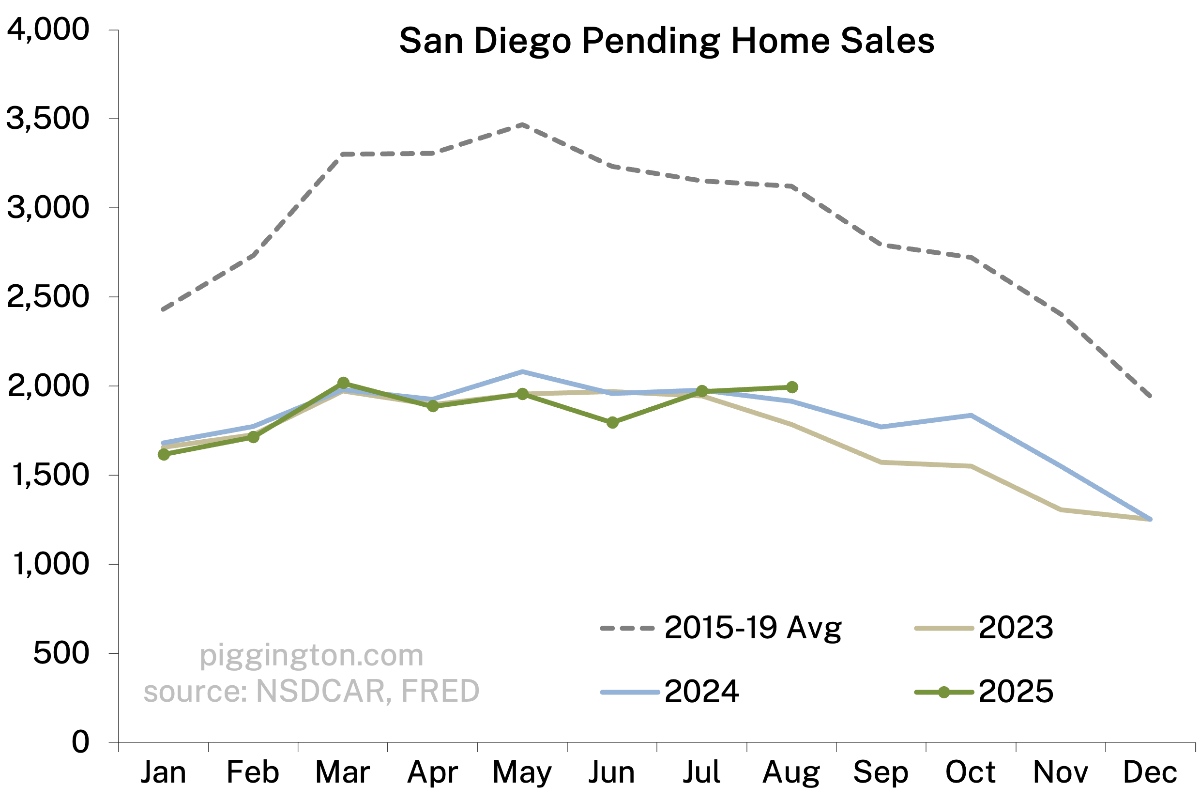

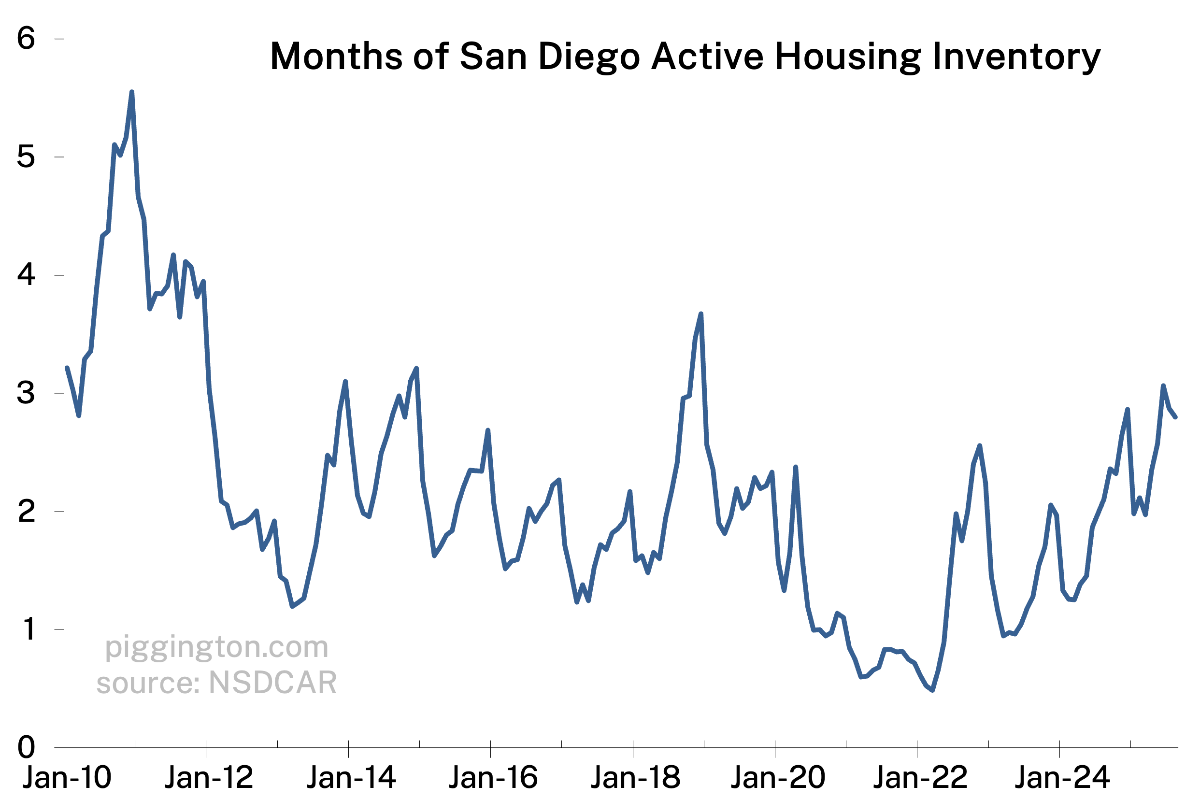

The spring surge in months of inventory has backed off a bit, but still remains above the norm for this time of year:

It remains to be seen which way this will break — continued backing off, or assuming the normal seasonal pattern from here.

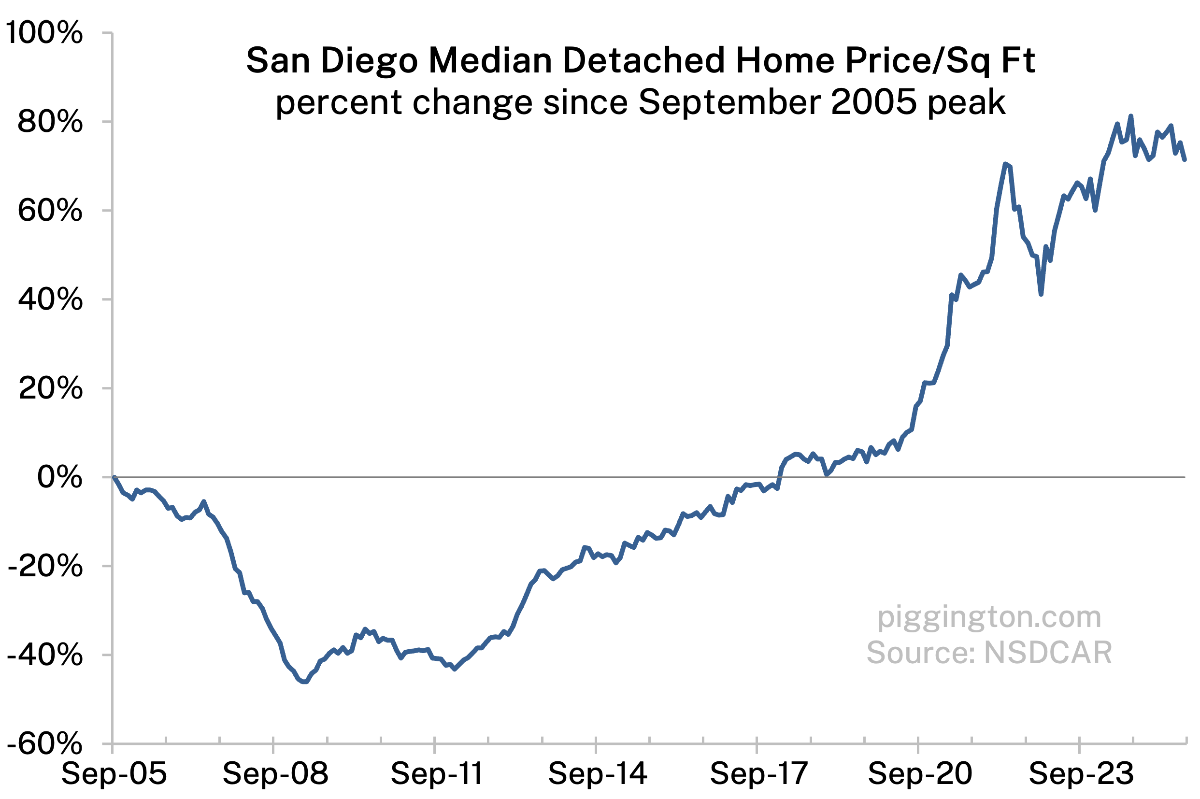

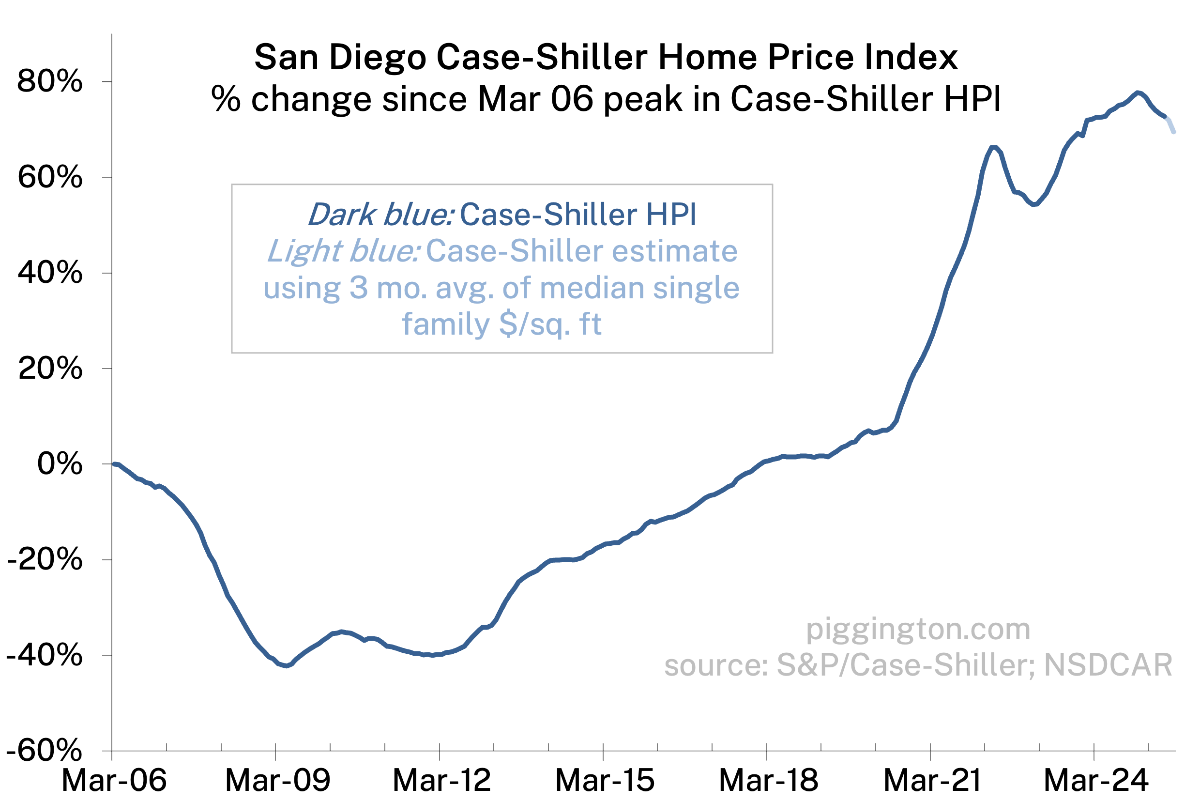

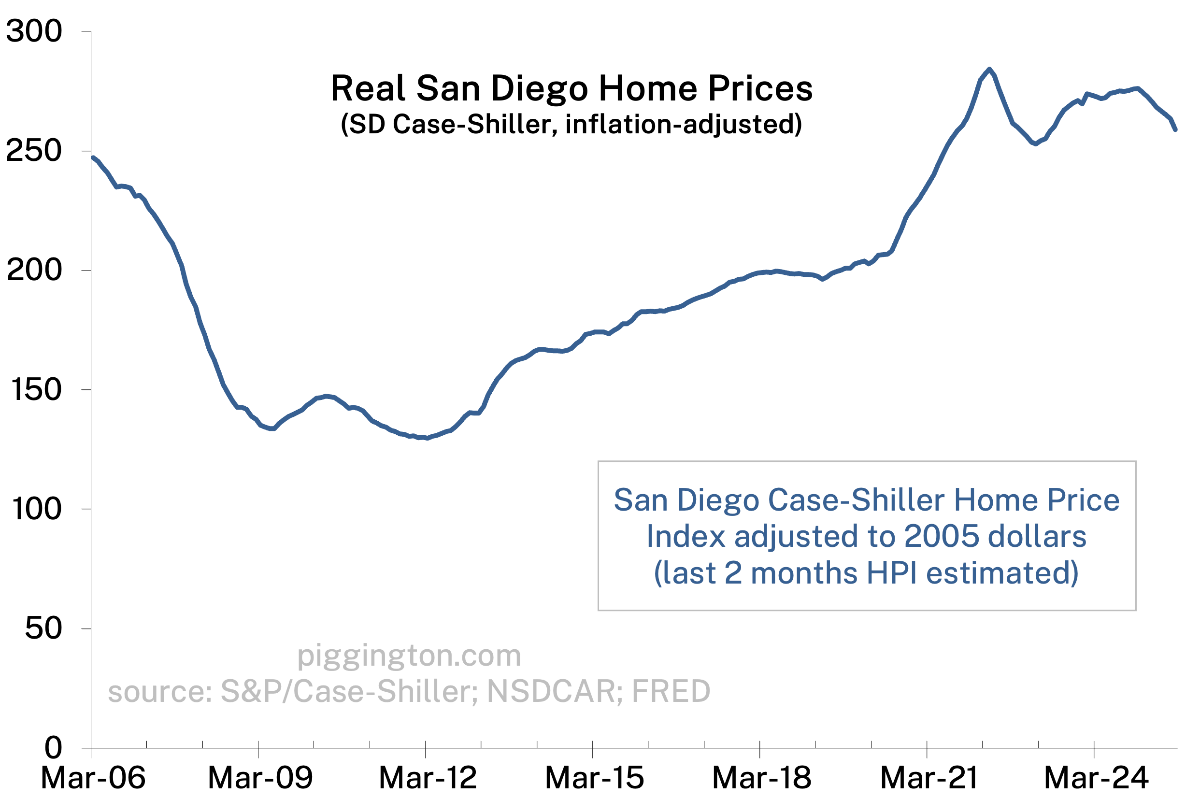

Prices were pretty weak. The price/square foot was down, and the (mild) downtrend for the Case-Shiller index is pretty established:

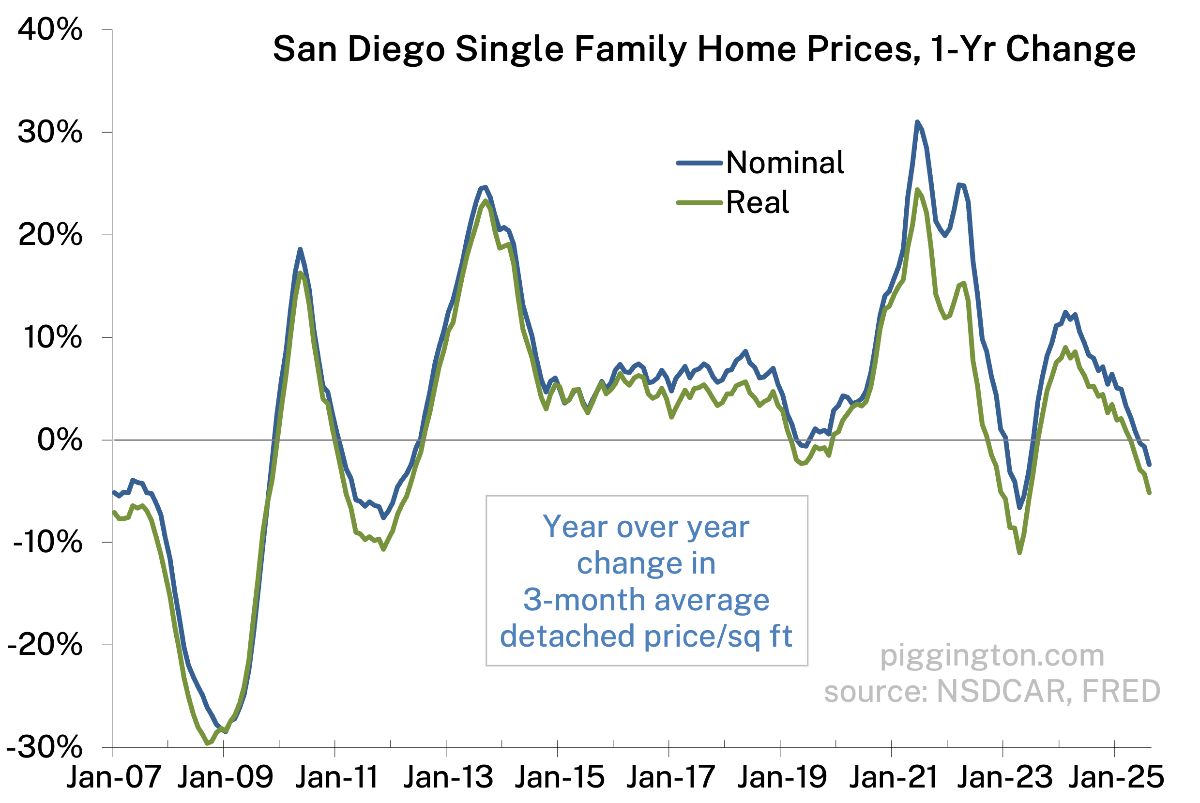

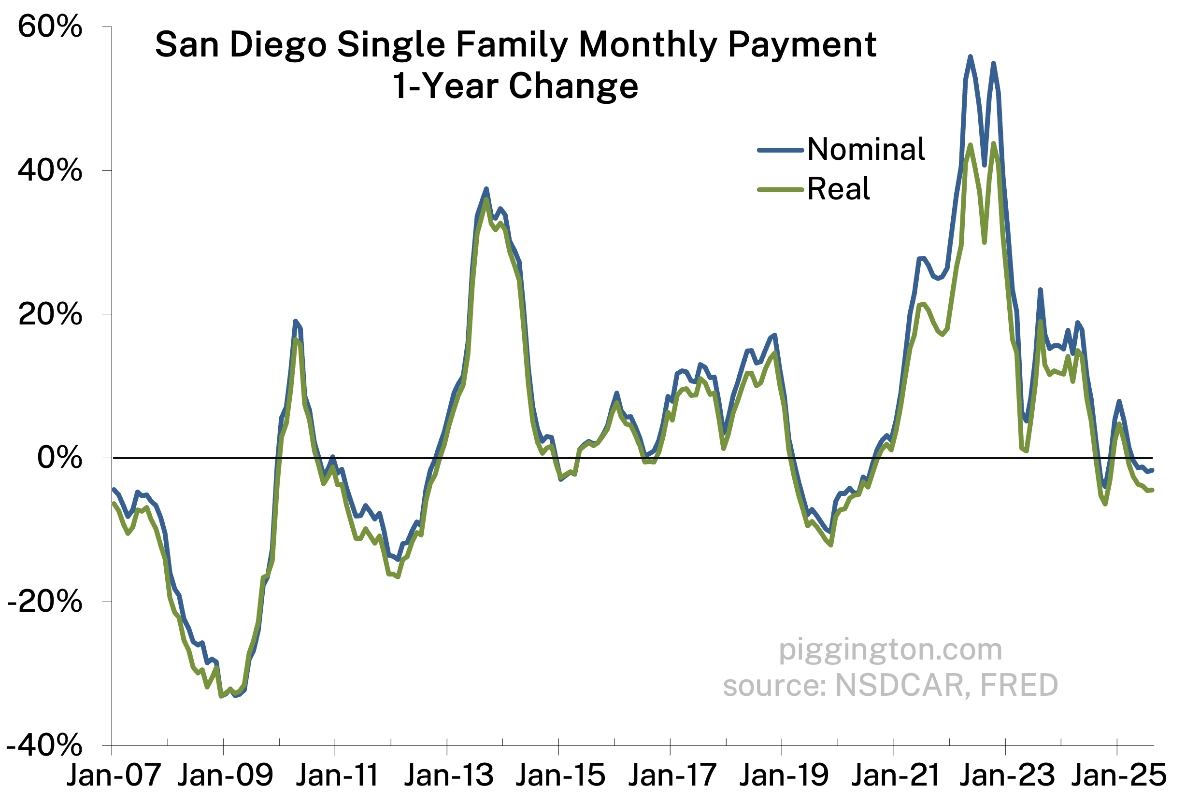

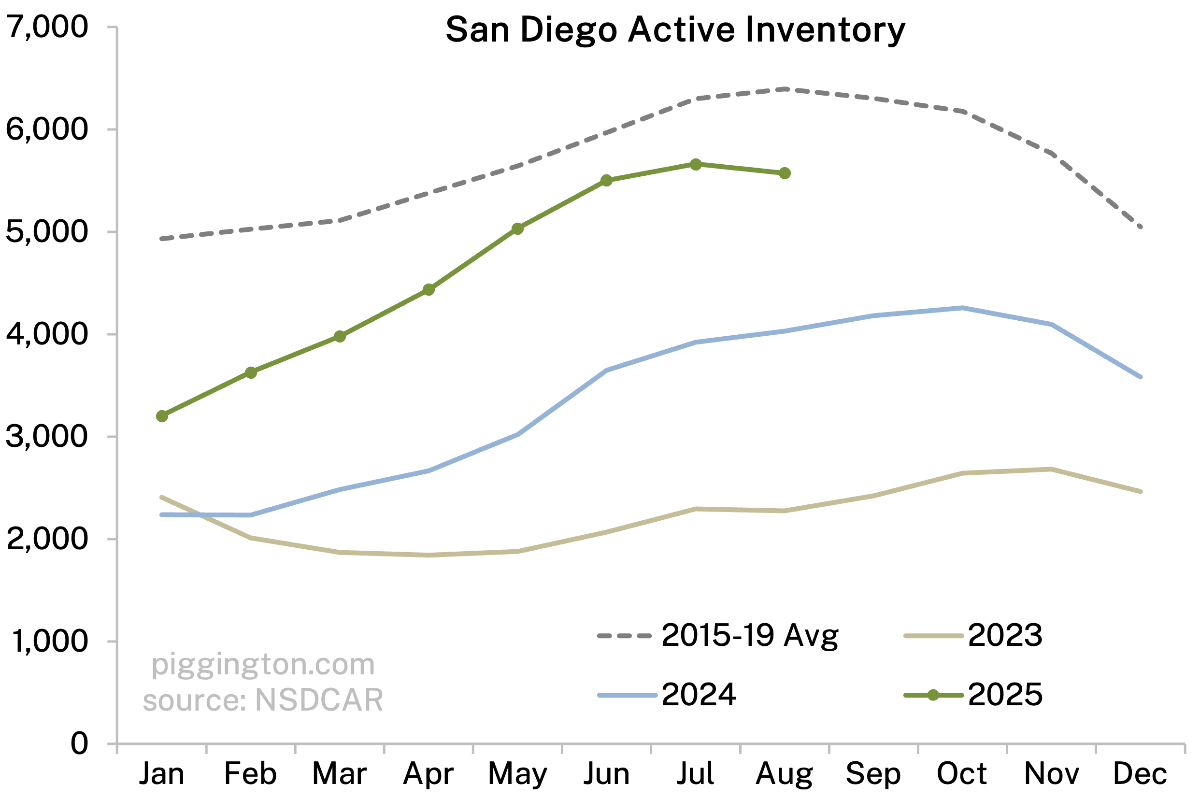

Here are a few I haven’t highlighted in a while… year over year charts:

Here are a few I haven’t highlighted in a while… year over year charts:

And below, inflation-adjusted monthly payments. These have improved a bit due to small declines in real prices and in mortgage rates, but they remain at historically very high levels:

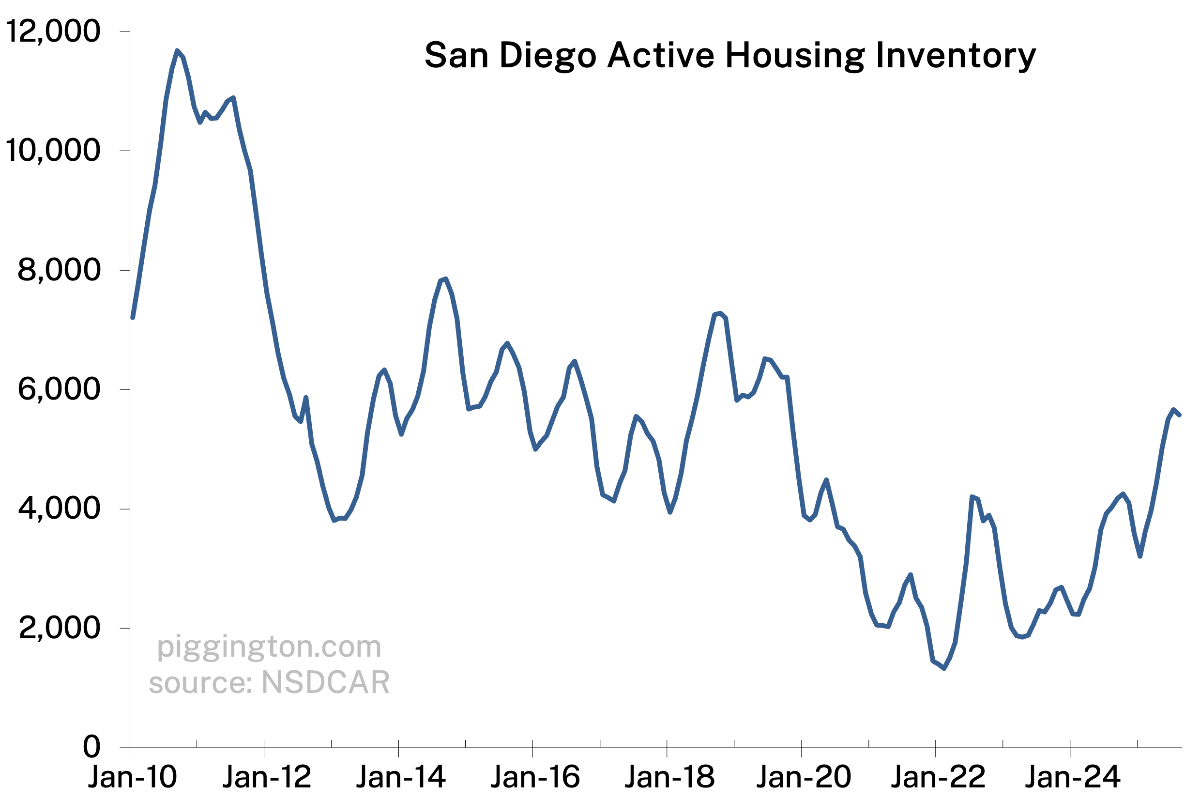

More charts below…

mortgage rates are experiencing more than just small declines, they are pretty close to 6 percent now after being stuck around 7 for a long time. Incidentally most of the houses for sale in my neighborhood that were sitting are all pending now. Rates will probably come down a bit more now that employment numbers have taken a bad turn and everyone is betting the fed will start the rate cutting cycle again as a result (at least temporarily until the tariffs eventually bring inflation back with a vengeance). Who’s ready for stagflation?

Fair point on my word choice there… I guess it depends how you are thinking about it. The peak to trough decline in rates has been significant in an absolute sense; at the same time we are not that far off the middle of the post-2022 range. I had the latter idea in mind but I take your point as well. I’ve attached a 5 year graph of rates for context.

Totally agree with you on the long-view timescale we are very much going to be stuck in the higher rate world depicted by the graph; was more thinking about how changes on the order of months can strongly affect rate-sensitive buyers waiting for a window of opportunity.

Anecdotally, I’ve definitely seen some weakness in my ‘hood (92011). A couple houses down the street set records about 6 months ago. Same models were listed recently with better upgrades, one with a pool, and couldn’t achieve the pricing of those that sold earlier in the year. One pulled off the market, we’ll see what they do next.

Another great article, thanks Rich! The growing list of things I am tracking for housing:

Housing Supply Up Factors (Downward price pressure)

— Aging-owner turnover gradually increases listings (oldest homeowners on average in US)

— Insurance cost increases may push some fixed income to sell

Housing Supply Down (Upward price pressure)

— Lock-in/shadow inventory persists (ultra-low mortgages + Prop-13). The ‘can’t afford to move anywhere I like’ group

— Zoning/permitting frictions limit SFH additions

Housing Demand Down (Downward price pressure)

— Payments remain elevated; affordability strained

— High home values create a burdensome property tax jump from prior Prop 13 rates. SALT deductions can help here, but its not enough at current values

— Consumer-debt headwinds tighten DTIs (College Loan repayments restarted, Auto Loan Defaults rising)

— Insurance premiums lift total monthly cost in risk-exposed areas

— Softer rents reduce urgency to buy

— Builder rate buydowns pull demand toward new construction while incentives last

— If prices slip and margins compress, builders’ buydown budgets shrink leading to fewer below-market rate offers leading to weaker new-home demand

Housing Demand Up (Upward price pressure)

— Probable rate-cut cycle that meaningfully lowers 30-yr fixed (if curve cooperates) makes current prices more attractive

— Resilient high-income buyers (select SD pockets)

— Institutional bid where yields pencil

Pricing cross-current to watch

— New-home median now at a discount to existing (mix + incentives); durability depends on incentives/margins

Current Prediction: Flat to modestly softer overall absent a negative catalyst for the foreseeable future; bigger discounts for older/repair-heavy and inland/risk-exposed homes, while prime coastal/renovated stock holds up better. Key swing: at what price level will ‘Millennial’ age households be able to purchase in volume?

Good stuff!

We recently moved out of the home (92123) we purchased in 2014 to rent something in a better neighborhood, closer to good schools. We are currently working to list the house for sale.

There are a lot of factors involved, and we seriously considered renting it out, but we decided to sell. If we cannot sell it for a price we are willing to accept, we may go looking for renters. We will see. Really appreciate your analysis since 2010!