- This topic has 72 replies, 22 voices, and was last updated 10 years, 9 months ago by

fun4vnay2.

-

AuthorPosts

-

April 28, 2015 at 7:08 AM #785415April 28, 2015 at 7:11 AM #785416

Rich ToscanoKeymaster

Rich ToscanoKeymaster[quote=svelte]

We shall see if prices are truly rising…and what has happened to the monthly Housing Data Rodeos, Rich? Looks like you’re getting bored of those, or maybe too busy?[/quote]That second thing… just been really busy lately. Sorry. I’ll put up a double feature once the April numbers are available. Also, I think we’re due for an update on the “shambling towards affordability” series (looking at valuation ratios).

April 28, 2015 at 7:22 AM #785418fun4vnay2

ParticipantThe market is indeed hot. No doubt about it.

We’d see how long this madness continues or if this time is different.

I can see prices touching/surpassing their peak values.April 28, 2015 at 10:05 AM #785427spdrun

ParticipantMatches with what I saw when I helped with the purchase in Jan also – multiple offers on properties within a week of listing.

I see a lot of units sitting with price drops within 1-2 mi of where I own my rental. NOT a fast-moving market. Secondly, I was at a few well-priced open houses last week and there was virtually no traffic.

I think the higher end is still going gangbusters, with low to middle end pre-1980s property moving much slower. It certainly won’t surpass 2006 nominal levels, at least not this year.

April 28, 2015 at 10:06 PM #785474utcsox

ParticipantI think the rental property is on fire. My colleague found a place through craigslist in one of the large apartment complex in UTC. He is paying over $1,000 a month to share a 2-bedroom units with a couple.

April 28, 2015 at 10:15 PM #785477Participant^^^

One born every minute? He can find a 1-bedroom in the low 1000s. Why would he pay the same to share?

April 28, 2015 at 10:44 PM #785479Escoguy

ParticipantPersonal theory, Rich may have liked watching the market go down while it did, and of course seeing a recovery is also interesting up to the normal level, but then it keeps going. Somehow it seems distasteful that the same scenario could play out again. But it takes a lot of work to show why 2015 is different from 2005.

Higher population, tighter lending, lower energy prices, lower interest rates.Makes for a mix which any rational economist may find annoying and unpredictable, but when all’s said and done, the Fed is afraid to raise rates, the stock market keeps going, there is not enough new supply and more and more folks both legal and illegal are coming into Cali.

So, no I don’t think Rich is bored, I just think it’s hard for him to be excited about seeing things develop exactly the way they are because it doesn’t quite fit with the world view. Just thoughts.April 28, 2015 at 11:53 PM #785480ParticipantWho says it is keeping going? Per the PPSF chart posted on here, prices per sf aren’t much different from last year. The real run-up was in 2013, and that’s past history.

Likely, the fun will begin anew soon as “people’s” HELOCs “reset” and the sales delayed by the Homerenter’s Bill of Wrongs move forward… tick-tock-tick-tock…

https://www.mainstreet.com/article/brace-for-flood-of-foreclosures-when-boom-era-helocs-turn-10

http://www.latimes.com/business/realestate/la-fi-foreclosures-surge-20150212-story.htmlApril 29, 2015 at 11:13 AM #785510Rich ToscanoKeymaster[quote=Escoguy]Personal theory, Rich may have liked watching the market go down while it did, and of course seeing a recovery is also interesting up to the normal level, but then it keeps going. Somehow it seems distasteful that the same scenario could play out again. But it takes a lot of work to show why 2015 is different from 2005.

Higher population, tighter lending, lower energy prices, lower interest rates.Makes for a mix which any rational economist may find annoying and unpredictable, but when all’s said and done, the Fed is afraid to raise rates, the stock market keeps going, there is not enough new supply and more and more folks both legal and illegal are coming into Cali.

So, no I don’t think Rich is bored, I just think it’s hard for him to be excited about seeing things develop exactly the way they are because it doesn’t quite fit with the world view. Just thoughts.[/quote]Hi Escoguy — Yeah, I’ve been pretty up front about the fact that the RE market isn’t as interesting as it used to be… first it was an insane bubble, then it was an unprecedented crash that followed that bubble. Now the whole thing is a bit more pedestrian.

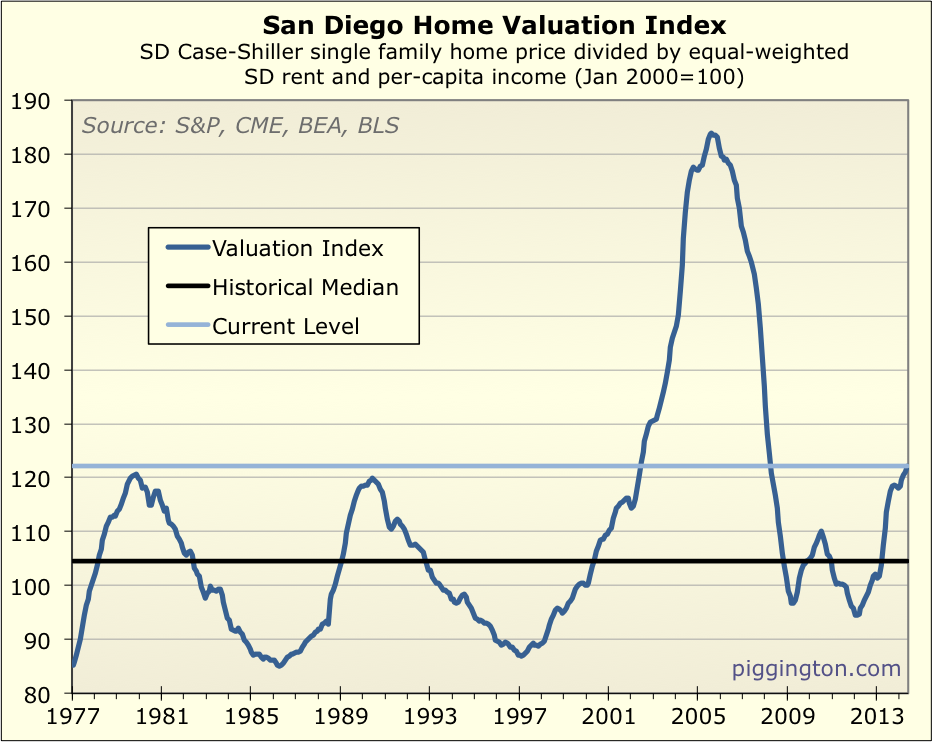

However, I don’t agree that the current situation is even remotely comparable to 2005. Homes are nowhere near as overvalued as they were at the 2005 peak:

(more here: http://piggington.com/shambling_towards_affordability_housing_valuations_surpass – btw this is from last year, but it hasn’t changed all that much since then)

Eyeballing it, aggregate home prices would have to rise 50% from here — with no commensurate increase in incomes or rents — to become as expensive as they were at the 2005 peak. 50%! (That’s before even considering the impact of low rates… which could very well be transitory, but for as long as they do last, it’s plausible that they could support a higher-than-normal level of valuations).

Yes, the market is overvalued compared to its history for sure — but it doesn’t hold a candle to 2005.

You seem to be ascribing a “world view” to me… I’m not sure what that might be, but as it relates to this kind of thing, I would sum up my views thusly: market prices frequently become dramatically disconnected from their fundamentals… and when they do, it’s really interesting.

Because bubbles don’t usually hit the same market twice in a row, a 2005-style housing bubble would be surprising to me — but it certainly would not be boring! 🙂

April 29, 2015 at 6:27 PM #785515 svelteParticipant

svelteParticipant[quote=spdrun]Who says it is keeping going? Per the PPSF chart posted on here, prices per sf aren’t much different from last year. The real run-up was in 2013, and that’s past history.

https://www.mainstreet.com/article/brace-for-flood-of-foreclosures-when-boom-era-helocs-turn-10

http://www.latimes.com/business/realestate/la-fi-foreclosures-surge-20150212-story.html%5B/quote%5DWe’re not talking about LA here, we’re talking about San Diego…

[quote=spdrun]I see a lot of units sitting with price drops within 1-2 mi of where I own my rental. NOT a fast-moving market. Secondly, I was at a few well-priced open houses last week and there was virtually no traffic.[/quote]

So now, since you quoted LA stats above, are you now talking LA area, or SD? Because if it’s SD, you must live nowhere close to where I live.

[quote=svelte]Spoke with a realtor friend this weekend – he’s been closing one sale every 1 to 2 weeks. Yikes! He says it feels like a seller’s market as he has more buyers…Realtor said this week he is getting multiple offers right now too.[/quote]

Let’s see what the stats are telling us:

http://www.utsandiego.com/news/2015/apr/16/dataquick-march-realestate-home-sales-mortgage/

“San Diego County’s housing market surged in March, seeing its biggest annual increase in sales in nearly two years.”

Wow. Sounds a lot like I was saying above…

“Last month, 3,467 real-estate transactions closed in the county, a 13.4 percent jump from March 2014, real estate tracker CoreLogic reported Thursday. It was the biggest annual increase in sales since they rose more than 19 percent from July 2012 to July 2013.”

Again, kinda matches what I’m saying not what you’re saying…

“CoreLogic analyst Andrew LePage said inventory still remains an issue holding back the housing market. In March, there were 6,101 active listings in the county, the San Diego Association of Realtors reports. That represents fewer than two months of supply, which bodes well for sellers.

LePage said as a general rule between three and six months of supply would render the market neutral, while any more would turn the tide in favor of buyers.”

Wow…now…who was it saying it’s a seller’s market, me or you?

“Housing demand has been stoked over the last year by job growth mainly, to some extent some income growth, and increased job security,” LePage said.

From February to March sales rose 35 percent in the county, while the median home sales price was up from $440,000.”

Again…points strongly in my direction…not a tanking market.

April 29, 2015 at 8:44 PM #785518ParticipantRich,

Thanks for the charts and analysis, for those of us who were able to buy a few years ago when the market was soft, websites like this are very valuable pieces of information. Perhaps world view is too much, rather just market perspective.

I always think a certain amount of skepticism is healthy and would of helped avoid the 2005 scenario.

When I say it takes a lot of work to figure out the market, specifically, it would be interesting to know what effect interest rates have or population growth in isolation. That may be unknowable, but for now it seems like rates will stay low for the near to mid term and demand is there. Even as an investor, I’d prefer gently rising markets of 2%/year for the next decade than 4-5%/then potentially down again. As such I’ll stay a dedicated reader if only to check my own “world view”

April 29, 2015 at 9:13 PM #785520ParticipantAs an investor, I’d prefer another slowdown combined with a correction to somewhere between 2009 lows and today.

April 29, 2015 at 9:44 PM #785521HLS

ParticipantThere will always be people looking to rent regardless of price or interest rates.

Many people cannot qualify for a loan so it’s pointless to compare rent vs. buy.

Many other people just don’t care.Market rent is market rent, period.

Anybody who bases what rent should be based on their payment is a fool.If interest rates were higher, I don’t see how house prices will hold up. There will be a drawn out period of denial, but reality will eventually win. It will be even more difficult to qualify for a loan.

The auto industry has sold millions of cars based on nothing more than the monthly payment.

The housing market has followed this foolishness.Most people do not care how much they are paying for a house or a car, they only care about their monthly payment.

Millions have become complacent about the stock market & housing market. If/when the next crash occurs, 99.9% of people will be saying “Nobody saw this coming”

If you do a search online for $3500++ a month rentals, in many cases it’s much cheaper to rent than to buy. The market rent does usually not increase proportionately based on the increase in value of a house.

If home prices did fall, market rent probably wouldn’t change much.

April 29, 2015 at 11:50 PM #785528bearishgurl

Participant[quote=svelte][quote=spdrun]Who says it is keeping going? Per the PPSF chart posted on here, prices per sf aren’t much different from last year. The real run-up was in 2013, and that’s past history.

https://www.mainstreet.com/article/brace-for-flood-of-foreclosures-when-boom-era-helocs-turn-10

http://www.latimes.com/business/realestate/la-fi-foreclosures-surge-20150212-story.html%5B/quote%5DWe’re not talking about LA here, we’re talking about San Diego…

[quote=spdrun]I see a lot of units sitting with price drops within 1-2 mi of where I own my rental. NOT a fast-moving market. Secondly, I was at a few well-priced open houses last week and there was virtually no traffic.[/quote]

So now, since you quoted LA stats above, are you now talking LA area, or SD? Because if it’s SD, you must live nowhere close to where I live.

[quote=svelte]Spoke with a realtor friend this weekend – he’s been closing one sale every 1 to 2 weeks. Yikes! He says it feels like a seller’s market as he has more buyers…Realtor said this week he is getting multiple offers right now too.[/quote]

Let’s see what the stats are telling us:

http://www.utsandiego.com/news/2015/apr/16/dataquick-march-realestate-home-sales-mortgage/

“San Diego County’s housing market surged in March, seeing its biggest annual increase in sales in nearly two years.”

Wow. Sounds a lot like I was saying above…

“Last month, 3,467 real-estate transactions closed in the county, a 13.4 percent jump from March 2014, real estate tracker CoreLogic reported Thursday. It was the biggest annual increase in sales since they rose more than 19 percent from July 2012 to July 2013.”

Again, kinda matches what I’m saying not what you’re saying…

“CoreLogic analyst Andrew LePage said inventory still remains an issue holding back the housing market. In March, there were 6,101 active listings in the county, the San Diego Association of Realtors reports. That represents fewer than two months of supply, which bodes well for sellers.

LePage said as a general rule between three and six months of supply would render the market neutral, while any more would turn the tide in favor of buyers.”

Wow…now…who was it saying it’s a seller’s market, me or you?

“Housing demand has been stoked over the last year by job growth mainly, to some extent some income growth, and increased job security,” LePage said.

From February to March sales rose 35 percent in the county, while the median home sales price was up from $440,000.”

Again…points strongly in my direction…not a tanking market.[/quote]

svelte, spdrun is correct in that there are pockets of SD County which haven’t quite recovered yet:

As an example, see: http://www.realtor.com/realestateandhomes-search/91910/beds-2/baths-1/type-single-family-home/price-na-400000/sqft-4/pfbm-900

The link above reflects that the problem is present in the SFR market at the lower end of 91910 (and also includes 91911). I haven’t yet spot-checked in East County (LG, EC and SV) but I suspect 91945, 92120, 92121, and 91977 (and possibly 92071 as well) have similar issues in pockets. Not to mention that just as many zip codes in North County are still affected by underwater borrowers (esp in Esc and Vista).

In addition, 92154, 92173 and 91932 (int’l border areas) may still have problems as well but I know for a FACT that residential property in 92154 was heavily purchased during the downturn of 2009 thru 2011 for deep discounts by several deep-pocketed buy-and hold investor teams (incl REITs) plus individuals. (A large portion of SFRs in that zip code are over 1900+ sf.)

From my findings when looking deeper into the problem in South County, it’s not HELOCs that are the problem, as spdrun suggests. Perhaps resetting HELOCS will still be a problem in East LA (pockets), San Bern and RIV counties, which all still have a backlog of delinquencies and failed mods leading to FC, but in SD County, the problem appears to me to be cash-out refinancing (often repeatedly) with the last transaction occurring no later than the first half of 2007. In my spot checks in LA county, about 8 zip codes I studied had more SS and FC listings than traditional-sale listings in the current SFR market as recently as last week, often completely eclipsing “traditional sale” listings. For the most part, these homes were 60+ years old, situated on 7,500 to 13,000 sf lots.

I think many owners in the lower-end SoCal areas (or those owners of lower-end homes in moderate and middle-class areas) have tried mightily over the years to hang onto their homes since removing equity from them or paying too much for them years ago, but just like spdrun stated, the “(CA) Homeowner’s Bill of Rights” (Assembly Bill 278) essentially put a “monkey wrench” in the processing of FC’s in a timely manner in CA as determined by the statute (section 2924 of the Civil Code as it read PRIOR to when the Homeowner’s Bill of Rights was enacted).

CURRENT WORDING OF STATUTE: http://codes.lp.findlaw.com/cacode/CIV/5/d3/4/14/2/1/s2924

RAMIFICATIONS UPON CA HOMEOWNER’S BOA UPON STATUTE: http://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=201120120AB278

The CA Homeowner’s BOR (above) has a couple of provisions that I wholeheartedly agree with. Those are, the elimination of “dual tracking” of foreclosures (I witnessed this firsthand with homeowners who THOUGHT they were in the process of applying for a mod ALL THE WHILE the mechanisms for FC were actually systematically being put in place against them BY THE SAME LENDER who claimed to the borrower that they were collecting documents for a prospective loan mod). This practice was just ba-a-a-a-d and totally dishonest/duplicit (on the part of the lenders on so many fronts) in putting these borrowers thru the wringer while giving them false hope that they may be able to “save” their home. The second provision I agree with is the “single point of contact” for a borrower who is applying for and sending in documents for a loan modification (or in foreclosure). During the downturn, I worked with a handful of borrowers who were (mostly) submitting documents (as requested by the lender) for a mod but who got a different person EVERY TIME they called the same Big Banks’ loss mitigation or “collections” department. That person clearly had no idea what the last person they talked to told them to submit and denied receiving ANY of the documents they had already submitted (upon the bank’s request). It turned out to be a complete clusterfvck which these delinquent borrowers ended up navigating only to discover that it was a no-win proposition for them offering little incentive to continue to cooperate with the lenders’ demands.

It’s now “showtime” for many of these longtime “beleaguered” CA homeowners and it appears to me from the listings I actually recently viewed that a good portion of them DID spend some of their cashed-out equity on home improvements, but, to this day, cannot yet recover enough from sale to pay off their current encumbrances. In other words, they’re still “underwater” at this late date.

Aside from being located more than 20 miles from high-paying white-collar jobs and in “older” areas, there is really nothing wrong with the above SD County zip codes. IMO, it’s a dirty shame that these pockets haven’t fully recovered in value by now. This problem is keeping many well-above-water and even free-and-clear owners from listing in this market due to having to compete with current listings with (approved or non-approved) artifically-low asking prices. I personally KNOW free-and-clear owners who have recently chosen to RENT OUT rather than compete with artificially-low listing prices (“wishful” owners of SS listings) in this market.

April 29, 2015 at 11:57 PM #785529an

ParticipantBG, did you list 92121 by accident?

-

AuthorPosts

- You must be logged in to reply to this topic.