Home › Forums › Financial Markets/Economics › Investing in municipal bond funds

- This topic has 43 replies, 10 voices, and was last updated 9 years, 4 months ago by

phaster.

-

AuthorPosts

-

June 16, 2016 at 7:18 PM #22016June 16, 2016 at 7:24 PM #798761

SK in CV

ParticipantThe problem isn’t short term volatility. It’s long term volatility. There are probably still some muni’s out there with >12% coupons. What happens to share value if that happens again?

June 16, 2016 at 8:30 PM #798764ocrenter

ParticipantWould just buy the individual muni bonds, why buy the funds? What’s the rate?

June 16, 2016 at 8:36 PM #798765 CoronitaParticipant

CoronitaParticipant[quote=ocrenter]Would just buy the individual muni bonds, why buy the funds? What’s the rate?[/quote]

June 16, 2016 at 10:29 PM #798766henrysd

ParticipantI have owned Vanguard long term CA muni bond fund since 2009. The fund is so called long term, but it is actually in high spectrum of intermediate term bond fund as the average duration is only 6.4 years. There were many good times to buy it like any time from 2009-2012. The best time was when “star analyst” Whitney called for massive default in muni bond which never happened. True star manager like Bill Gross added massive position in muni bond after Whitney made the call which causeed big selloff in muni bond. My entry point was about 4% YTM and with the yield down to 1.8% now, there is significant risk of losing value when interest goes up. I personally feel it is too late to jump into the boat. Be careful when tempted to the 1.8% yield using bank saving rate as reference.

I am still holding the position, and if Fed raise fed fund rate to 1% (likely in 3 baby steps), I’ll dump the fund and change position to CA muni money fund.

June 17, 2016 at 6:44 AM #798770livinincali

Participant[quote=henrysd]I have owned Vanguard long term CA muni bond fund since 2009. The fund is so called long term, but it is actually in high spectrum of intermediate term bond fund as the average duration is only 6.4 years. There were many good times to buy it like any time from 2009-2012. The best time was when “star analyst” Whitney called for massive default in muni bond which never happened. True star manager like Bill Gross added massive position in muni bond after Whitney made the call which causeed big selloff in muni bond. My entry point was about 4% YTM and with the yield down to 1.8% now, there is significant risk of losing value when interest goes up. I personally feel it is too late to jump into the boat. Be careful when tempted to the 1.8% yield using bank saving rate as reference.

I am still holding the position, and if Fed raise fed fund rate to 1% (likely in 3 baby steps), I’ll dump the fund and change position to CA muni money fund.[/quote]

The math says that eventually some muni bonds will be defaulted on. The problem is when and where. That’s what Whitney got wrong, the timing. It’s obvious that at some point Chicago is going to default on their muni bonds. They are currently paying the bond holders and defaulting on their contractors. CA sort of did the same thing with IOUs in the depths of the recession. You do have somewhat of a cushion because cities seems to value paying the bond holders before some of their other bills.

June 17, 2016 at 8:02 AM #798773Participant[quote=flu][quote=ocrenter]Would just buy the individual muni bonds, why buy the funds? What’s the rate?[/quote]

http://www.morningstar.com/funds/XNAS/VCAIX/quote.html%5B/quote%5D

Not bad, not bad at all

June 17, 2016 at 8:23 AM #798774CoronitaParticipant[quote=ocrenter][quote=flu][quote=ocrenter]Would just buy the individual muni bonds, why buy the funds? What’s the rate?[/quote]

http://www.morningstar.com/funds/XNAS/VCAIX/quote.html%5B/quote%5D

Not bad, not bad at all[/quote]

Its ok, not great. Its in my category of safer things to do. I don’t see many of the CA munis it holds defaulting, lol. It’s also tax free both federal and state. I figure since I already pay a lot of CA state taxes, I might as well get some back, kind of like the idea of paying more taxes and buying section 8 housing to get some of it back. 🙂

In all seriousness, it was where I was parking my money arbitraging against my previous 2.5% mortgage and 4% rental mortgage, before I paid the former off with Broadcom RSU stock after I left.

(I don’t end to keep investments in the sector I work in, lol)

June 18, 2016 at 8:19 AM #798810Participant[quote=flu]

Its ok, not great. Its in my category of safer things to do. I don’t see many of the CA munis it holds defaulting, lol. It’s also tax free both federal and state. I figure since I already pay a lot of CA state taxes, I might as well get some back, kind of like the idea of paying more taxes and buying section 8 housing to get some of it back. 🙂

In all seriousness, it was where I was parking my money arbitraging against my previous 2.5% mortgage and 4% rental mortgage, before I paid the former off with Broadcom RSU stock after I left.

(I don’t end to keep investments in the sector I work in, lol)[/quote]

well, if your tax rate is up to 45% (ca + fed), a 4% return turns into just over a 7% pre-tax investment.

not sure I can find a 7%+ investment vehicle in this climate of perpetual low interest.

June 18, 2016 at 8:32 AM #798812phaster

Participant[quote=FormerOwner]

What does everyone think of municipal bond funds? I’ve got a financial advisor that has recommended a number of municipal bond funds, such as PIMAX and VCLAX; a mix of high-yield/lower credit quality muni funds and lower-yield/higher credit quality muni funds. Overall, the performance looks a heck of a lot better than the 1% I’m getting on my CD’s. I can leave the money there for several years at least, so short-term volatility wouldn’t really be a problem. Any thoughts would be appreciated.

[/quote]just wondering if your financial advisor has pondered how “municipal bond funds” he recommended are going to be affected by an accounting rule which was just put in place (which explicitly states pension liabilities must be included on the balance sheets)

[quote=phaster]FlyerInHi,

I guess its up to me warn of the economic danger(s) since none of the old hands on this forum were able to connected the dots to paint the big picture of a parallel situtation as described in the big short prologue

…long story short

“public pensions and muni bonds” have mutated into a monstrosity that could chaotically collapse the economy and very, very, vary few of the experts, leaders or talking heads in the wider world seem to have a clue

I’m guessing most of you still don’t know what most likely will happen AND truth be told its impossible to predict the future w/ 100% accuracy

yeah you might have some soundbite you repeat so you don’t sound dumb about the state of public finance, but come on (is it actually possible for the “average” taxpayer to trust/verify the figures?)

[quote=CA renter]“Standard And Poor’s Gives San Diego County Its Highest Rating

San Diego County has earned the highest possible rating from all three of the top credit agencies—Fitch, Moody’s, and Standard and Poor’s.”so while most in this country are distracted by political horse$hit (i.e. soap opera media coverage of TRUMP for president)

http://www.npr.org/2016/03/04/469149226/trump-attacked-from-all-sides-in-bitter-chaotic-gop-debate

an honest outsider and math-centric weirdo might just see the giant lie at the center of the economy… by just PAYING ATTENTION!

[quote=NPR]

After the stock market crash of 1929, the agencies began to also rate bond investments for banks — at the request of the U.S. government. But things began to change in the 1960s and 1970s. Instead of charging investors for their ratings information, the agencies began to charge the bond issuers themselves for the ratings.“People were quite critical of this and said it could create a conflict of interest,” Partnoy says. “You can imagine what the difference between ratings of restaurants and movies might be if instead of the Michelin Guide or the Zagat guide, if the restaurants or movie companies themselves were paying the raters to be rated, it’s an obvious conflict of interest. And now it’s very commonplace that companies and GOVERNMENTS — anyone who wants to borrow money — THEY ARE THE ONES WHO ARE PAYING FOR THE RATING.”

http://www.npr.org/2011/08/17/139675717/rating-the-wall-street-ratings-agencies

[/quote][quote=TIMESOFSANDIEGO.COM]

Financial Outlook Shows San Diego’s Revenue Will GrowRevenues to the city of San Diego are projected to “modestly improve” over the next five fiscal years, while expenses will continue to rise, according to a financial outlook to be delivered Thursday to the City Council’s Budget Committee.

The five-year outlook, released annually in November by the mayor’s financial staff, projects steadily increasing general fund surpluses through Fiscal Year 2021.

The anticipated surpluses begin at $200,000 for the next fiscal year, and grow in subsequent years to $7.9 million, $25.1 million, $46.4 million, and $73.7 million.

THE PROJECTIONS DON’T INCLUDE FACTORS THAT OCCASIONALLY POP UP, like increases in contributions to the employee pension system.

[/quote][quote=LATIMES.COM]

PUBLIC “Pension liabilities must be included on the balance sheets of the agencies responsible for funding their employees’ pensions. Until now liabilities have been buried in arcane footnotes that few read and even fewer understood”http://articles.latimes.com/2014/apr/09/opinion/la-oe-fritz-pension-liability-california-20140410

[/quote] [/quote]June 18, 2016 at 12:24 PM #798763CoronitaParticipant

[/quote]June 18, 2016 at 12:24 PM #798763CoronitaParticipantI have the vanguard intermediate term ca fund for a few years. Its alright. I personally wouldnt do the long term one. But what do I know. Nothing particularly exciting.

June 18, 2016 at 12:26 PM #798819CoronitaParticipant[quote=ocrenter][quote=flu][quote=ocrenter]Would just buy the individual muni bonds, why buy the funds? What’s the rate?[/quote]

http://www.morningstar.com/funds/XNAS/VCAIX/quote.html%5B/quote%5D

Not bad, not bad at all[/quote]

Forgot to mention, it holds many ca bonds…. So it’s unlikely an individual can duplicate that sort of diversification. Maybe you can, but I sure can 🙂

Top holding include UC Regents bond, LA Unified, CA Dept of Water, Bay Area Toll Revenue, etc

https://personal.vanguard.com/us/funds/snapshot?FundId=0100&FundIntExt=INT#tab=2

holdings (many of the same bonds at different periods in time, but even so, pretty widespread)

June 18, 2016 at 2:37 PM #798817CoronitaParticipant[quote=phaster][quote=FormerOwner]

What does everyone think of municipal bond funds? I’ve got a financial advisor that has recommended a number of municipal bond funds, such as PIMAX and VCLAX; a mix of high-yield/lower credit quality muni funds and lower-yield/higher credit quality muni funds. Overall, the performance looks a heck of a lot better than the 1% I’m getting on my CD’s. I can leave the money there for several years at least, so short-term volatility wouldn’t really be a problem. Any thoughts would be appreciated.

[/quote]just wondering if your financial advisor has pondered how “municipal bond funds” he recommended are going to be affected by an accounting rule which was just put in place (which explicitly states pension liabilities must be included on the balance sheets)

[quote=phaster]FlyerInHi,

I guess its up to me warn of the economic danger(s) since none of the old hands on this forum were able to connected the dots to paint the big picture of a parallel situtation as described in the big short prologue

…long story short

“public pensions and muni bonds” have mutated into a monstrosity that could chaotically collapse the economy and very, very, vary few of the experts, leaders or talking heads in the wider world seem to have a clue

I’m guessing most of you still don’t know what most likely will happen AND truth be told its impossible to predict the future w/ 100% accuracy

yeah you might have some soundbite you repeat so you don’t sound dumb about the state of public finance, but come on (is it actually possible for the “average” taxpayer to trust/verify the figures?)

[quote=CA renter]“Standard And Poor’s Gives San Diego County Its Highest Rating

San Diego County has earned the highest possible rating from all three of the top credit agencies—Fitch, Moody’s, and Standard and Poor’s.”so while most in this country are distracted by political horse$hit (i.e. soap opera media coverage of TRUMP for president)

http://www.npr.org/2016/03/04/469149226/trump-attacked-from-all-sides-in-bitter-chaotic-gop-debate

an honest outsider and math-centric weirdo might just see the giant lie at the center of the economy… by just PAYING ATTENTION!

[quote=NPR]

After the stock market crash of 1929, the agencies began to also rate bond investments for banks — at the request of the U.S. government. But things began to change in the 1960s and 1970s. Instead of charging investors for their ratings information, the agencies began to charge the bond issuers themselves for the ratings.“People were quite critical of this and said it could create a conflict of interest,” Partnoy says. “You can imagine what the difference between ratings of restaurants and movies might be if instead of the Michelin Guide or the Zagat guide, if the restaurants or movie companies themselves were paying the raters to be rated, it’s an obvious conflict of interest. And now it’s very commonplace that companies and GOVERNMENTS — anyone who wants to borrow money — THEY ARE THE ONES WHO ARE PAYING FOR THE RATING.”

http://www.npr.org/2011/08/17/139675717/rating-the-wall-street-ratings-agencies

[/quote][quote=TIMESOFSANDIEGO.COM]

Financial Outlook Shows San Diego’s Revenue Will GrowRevenues to the city of San Diego are projected to “modestly improve” over the next five fiscal years, while expenses will continue to rise, according to a financial outlook to be delivered Thursday to the City Council’s Budget Committee.

The five-year outlook, released annually in November by the mayor’s financial staff, projects steadily increasing general fund surpluses through Fiscal Year 2021.

The anticipated surpluses begin at $200,000 for the next fiscal year, and grow in subsequent years to $7.9 million, $25.1 million, $46.4 million, and $73.7 million.

THE PROJECTIONS DON’T INCLUDE FACTORS THAT OCCASIONALLY POP UP, like increases in contributions to the employee pension system.

[/quote][quote=LATIMES.COM]

PUBLIC “Pension liabilities must be included on the balance sheets of the agencies responsible for funding their employees’ pensions. Until now liabilities have been buried in arcane footnotes that few read and even fewer understood”http://articles.latimes.com/2014/apr/09/opinion/la-oe-fritz-pension-liability-california-20140410

[/quote][/quote][/quote]If you have to worry about everything that could happen, then the only thing you should do is leave your money in a 1%CD, never buy a house, and never buy any other sort of investment that isn’t guaranteed …..

Also, I think you’re glossing over all types of CA munibonds…..There’s many different ones, and unlikely all will be defaulting all at the same time….

Anyway I’m not suggesting to go all in in bonds.A little moderation everywhere, seemed to worked out ok. Definitely better than camping out in a 1%CD for the past few years…

June 21, 2016 at 7:23 AM #798921Participant[quote=livinincali][quote=henrysd]I have owned Vanguard long term CA muni bond fund since 2009. The fund is so called long term, but it is actually in high spectrum of intermediate term bond fund as the average duration is only 6.4 years. There were many good times to buy it like any time from 2009-2012. The best time was when “star analyst” Whitney called for massive default in muni bond which never happened. True star manager like Bill Gross added massive position in muni bond after Whitney made the call which causeed big selloff in muni bond. My entry point was about 4% YTM and with the yield down to 1.8% now, there is significant risk of losing value when interest goes up. I personally feel it is too late to jump into the boat. Be careful when tempted to the 1.8% yield using bank saving rate as reference.

I am still holding the position, and if Fed raise fed fund rate to 1% (likely in 3 baby steps), I’ll dump the fund and change position to CA muni money fund.[/quote]

The math says that eventually some muni bonds will be defaulted on. The problem is when and where. That’s what Whitney got wrong, the timing. It’s obvious that at some point Chicago is going to default on their muni bonds. They are currently paying the bond holders and defaulting on their contractors. CA sort of did the same thing with IOUs in the depths of the recession. You do have somewhat of a cushion because cities seems to value paying the bond holders before some of their other bills.[/quote]

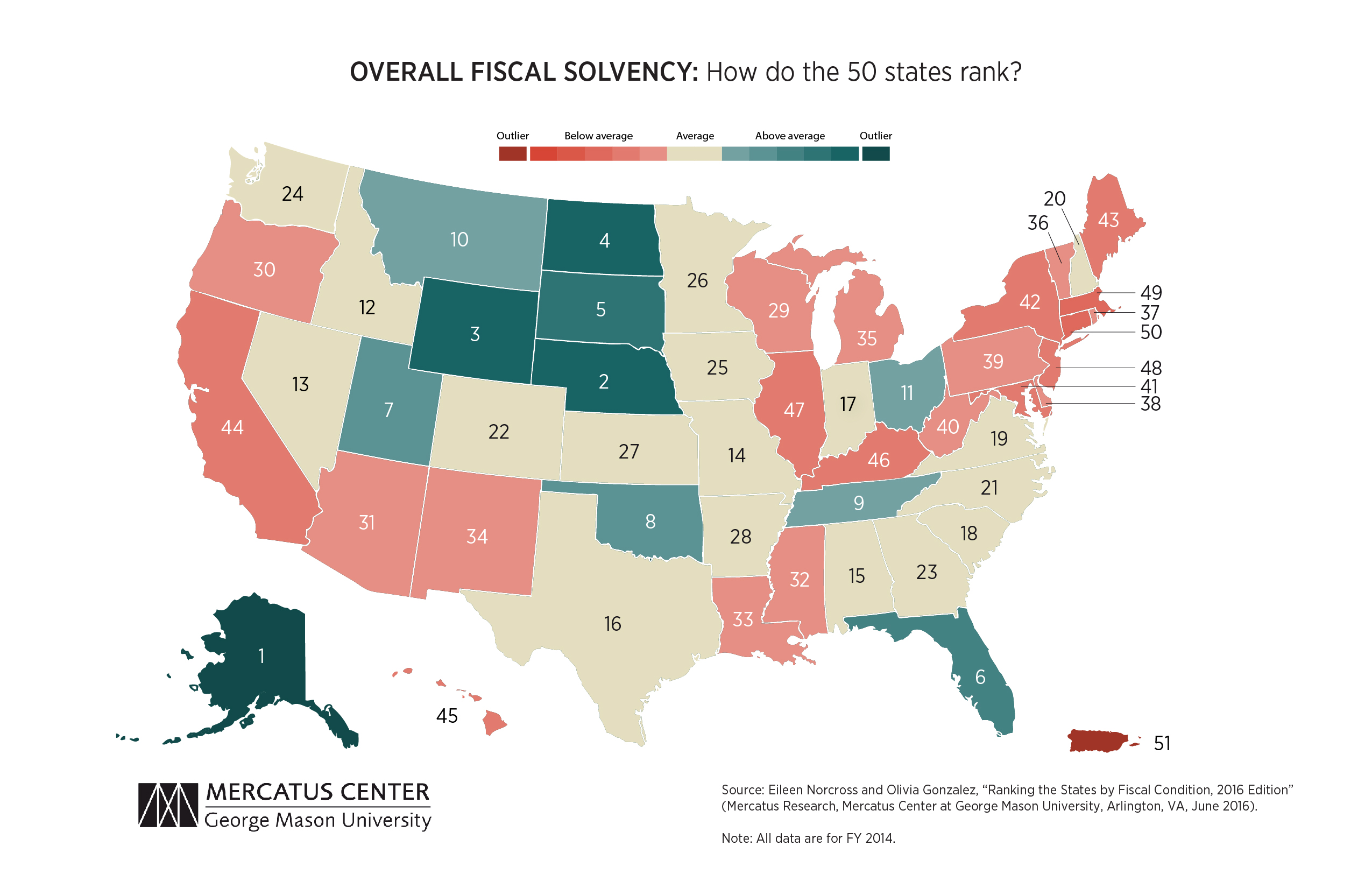

[quote=mercatus.org]

A new study for the Mercatus Center at George Mason University ranks each US state’s financial health based on short- and long-term debt and other key fiscal obligations, such as unfunded pensions and healthcare benefits.

#44 California

#45 Hawaii

#46 Kentucky

#47 Illinois

#48 New Jersey

#49 Massachusetts

#50 Connecticut

#51 Puerto Ricohttp://mercatus.org/statefiscalrankings

[/quote][quote=flu]

Also, I think you’re glossing over all types of CA muni bonds…..There’s many different ones, and unlikely all will be defaulting all at the same time….

[/quote]i’ll admit i’ve got ZERO formal education in economics or finance, and because of that fact instead have to rely on common sense (AND knowledge of math) to try and make sense of the complex economic forces that produced the bubble(s) w/ internet stocks and “housing”

perhaps not having formal education in economics or finance may actually be an advantage because conventional wisdom missed all the various warnings of “crazy shit” that went down before the crash!

WRT the housing bubble, in the opening scenes of the movie “the big short” the point was made that at the time people always pay mortgages… so it made sense when Lewis Ranieri of Salomon Brothers began packaging mortgage loans into mortgage-backed securities, BUT as we know these BONDS “mutated into a monstrosity that collapsed the world’s economy”

no doubt you’ve heard the expression “a rising tide lifts all boats” when describing the economy,… well my reading of the tea leaves and using common sense math, tells me the public pension system is unsustainable and eventually will result in something akin to a receding tide in the muni bond market

using a building analogy, imagine a crap building foundation onto which a big ass sky scraper is built with fancy inlaid wood floored work spaces and marble floored bathrooms w/ gold plated bathroom fixtures, etc.

http://www.idesignarch.com/inside-donald-and-melania-trumps-manhattan-apartment-mansion/

what I’m trying to point out is as long as the structure (i.e. system supporting the “muni bond”) isn’t too stressed, its possible for the structure to remain standing, but if a structure becomes too top heavy for a weak foundation, the whole thing comes crashing down!

so looking at a “real world” example, we see some parts of the local government are diligently building infrastructure to deal with the problem(s) associated w/ the drought, (like investing 3+ billion for a DeSal plant, building more space for water storage, etc.)

http://piggington.com/ucsd_econ_roundtable

BUT there is also a reported 2+ billion unfunded public pension debt, which is the akin to a “crap” economic foundation onto which a “solid” water infrastructure is built!

http://piggington.com/how_will_unfunded_pensions_affect_economy?page=7#comment-264991

[quote=damfailures.org]

Case Study: St. Francis Dam (California, 1928)

…Multiple instances of poor judgment by Mulholland and several of his subordinates significantly contributed to the cause of the failure of St. Francis Dam.

[/quote]I don’t have any muni bond funds w/ in my own portfolio, but given the fractal nature (i.e. patterns repeat at ALL levels) of things like, governments fiscal/political corruption/(mis)management

(here at the local level for example…)

[quote=kpbs.org]

City’s Development System A Major Fraud Risk, Says Auditorhttp://www.kpbs.org/news/2012/jul/03/citys-development-system-major-fraud-risk-says-aud/

[/quote][quote=kpbs.org]

Illegal Campaign Cash Tied To 4 Prominent San Diego Politicians

http://www.kpbs.org/news/2014/jan/21/tech-ceo-and-former-sdpd-detective-accused-funneli/

[/quote][quote=nbcsandiego.com]

Lawsuit Opposes Destruction of Old San Diego City Hall EmailsOn Feb. 27, 2014, interim Mayor Todd Gloria announced the adoption of a policy, known as “AR 90.67,” that would authorize the destruction of city emails that are more than one year old…

“Had someone not leaked the interim mayor’s announcement to the press, the public would not have found out about AR 90.67 until long after the email communications had been destroyed,”

[quote=wsj.com]

San Diego Pension Dials Up the Risk to Combat a Shortfallhttp://www.wsj.com/articles/san-diego-pension-dials-up-the-risk-to-combat-a-shortfall-1407974779

[/quote][quote=sandiegouniontribune.com]

A troubling mess at the City Attorney’s Officehttp://www.sandiegouniontribune.com/news/2016/apr/22/city-attorney-botched-cases-goldsmith/

[/quote][quote=sandiegouniontribune.com]

Azano’s son charged in campaign donations caseSAN DIEGO — The prosecution of Mexican businessman José Susumo Azano Matsura, accused of orchestrating illegal donations to the campaigns of San Diego politicians, has widened to include his son.

http://www.sandiegouniontribune.com/news/2016/mar/04/edward-susu-azano-charged-campaign-donations/

[/quote]and god only know what other “political” horse$hit is out there

so given the uncertainty I’d think it prudent to investigate “investment yield alternatives” along with a hedge strategy against the risk of systemic economic failure (i.e. TSHTF) before “investing” in CA muni bonds,… because a voice (seemly everywhere) that tells me…

[quote=washingtonpost.com]

“There’s something going on,” Trump said. “It’s inconceivable. There’s something going on.”June 21, 2016 at 7:36 AM #798923CoronitaParticipantyawn

-

AuthorPosts

- You must be logged in to reply to this topic.