- This topic has 43 replies, 11 voices, and was last updated 3 years, 6 months ago by

flyer.

-

AuthorPosts

-

May 28, 2021 at 4:49 PM #821918May 28, 2021 at 4:50 PM #821919

XBoxBoy

Participant[quote=The-Shoveler]IMO can’t discount the sugar high,

In the mid 80’s mortgage rates were in the 10’s housing was going up 15-20% a year in LA (defense spending boom sugar high).[/quote]

Undoubtedly we have had a number of sugar highs in the past, and probably will have more in the future. The problem with the sugar high though is that they don’t last.

May 28, 2021 at 4:57 PM #821920sdrealtor

Participant[quote=XBoxBoy][quote=sdrealtor]Correlation is not the same thing as causation[/quote]

True. However in this case I feel there is probably a causality at play. Feel free to disagree though.[/quote]

OK Let me amend that. 100% correlation is not 100% direct causation. There that’s better

May 28, 2021 at 10:08 PM #821921Reality

ParticipantWith inventory as low as it is is it possible San Diego is actually undervalued when interest rates and inflation explain most of the price difference from the past? What would prices have looked like 30 years ago with such scarce supply?

May 29, 2021 at 8:23 AM #821922 svelteParticipant

svelteParticipantXBoxBoy,

This is a truly impressive piece of work. I love your thought process and how you used that to drive what you research and how you present it.

There is no “but”, this work stands on its own and deserves kudos.

It is interesting to see how interest rates and inflation can account for darn near everything we see in San Diego housing prices, as your overlays clearly show. As others have pointed out there are other things that influence prices also, but most years that is in the noise while on rare occasion they truly do need to be factored in.

Again, congratulations. We’ll never get house prices down to an exact science because humans are emotional creatures, but it is fascinating to see how you can get into the ballpark by relating a few key facts.

Thank you!

May 29, 2021 at 10:06 AM #821923ParticipantInterest rates and inflation account for higher cost and price of just about everything everywhere. Devalue the dollar and flood with currency and prices will rise. I don’t think anyone would disagree with that.

For me the question is what explains the rest of it. Why do prices rise more and faster here than Cleveland? Why do single family homes rise more than condos. Why has beach area properties appreciated more than East County?

While he did an excellent job, I think it’s just showing how markets behave in general and I’m always looking for the exceptions that allow one to beat the market. Am I missing something?

May 29, 2021 at 10:53 AM #821924svelteParticipant[quote=sdrealtor]Interest rates and inflation account for higher cost and price of just about everything everywhere. Devalue the dollar and flood with currency and prices will rise. I don’t think anyone would disagree with that.

For me the question is what explains the rest of it. Why do prices rise more and faster here than Cleveland? Why do single family homes rise more than condos. Why has beach area properties appreciated more than East County?

While he did an excellent job, I think it’s just showing how markets behave in general and I’m always looking for the exceptions that allow one to beat the market. Am I missing something?[/quote]

I think the answer to all of your questions in the second paragraph boil down to one word: desirability. SD is more desirable than Cleveland (where the term “sunshine tax” came from), SFR are more desirable that condos, and beach property is more desirable that desert. Not sure there is much mystery in that. The question you may really be asking is how does one calculate how much more something is worth given that it is more desirable.

I’m not willing to pay more to live at the beach as I would probably hate it there (traffic, moisture, etc), but I’m willing to pay more to not live in the desert which is why I live about 11 miles from the coast. And I’m definitely willing to pay more for a SFR than a condo…a little more privacy is worth something to me, though I don’t need so much privacy that I need to move to the desert! 🙂

May 29, 2021 at 12:13 PM #821926 Rich ToscanoKeymaster

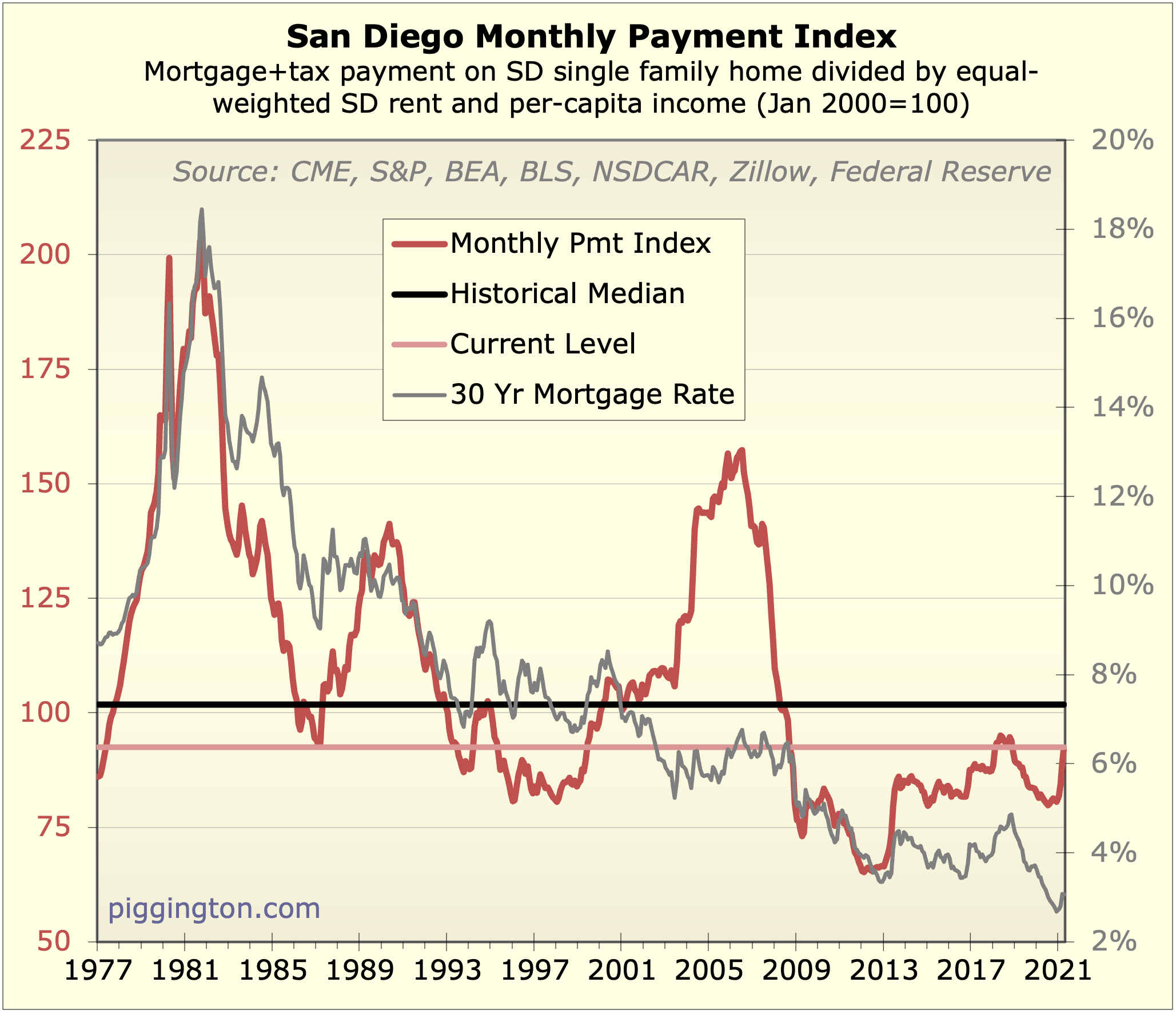

Rich ToscanoKeymasterI’ve been thinking about your results in the context of my monthly payment chart:

My interpretation of this chart has always been that it shows that rates haven’t had a ton of influence on home valuations. If they had, then the red line would mean revert around a pretty flat line across the whole chart. In other words, monthly payments would be the constraint, and home prices/valuations would move up or down to accommodate a pretty constant monthly payment (as a % of income).

But that’s definitely not happening in this chart. In the 70s and 80s, valuations didn’t plummet to accommodate high rates. Instead, prices hung in there, and people paid a much higher monthly payment (as a % of incomes or rents).

Thus my conclusion that you can’t really value housing based off rates.

However, if you take a closer look at my graph, there are really 2 regimes there. In the 70s/80s, home prices weren’t influenced so much by rates. However, starting in the 90s, we DO see that more flat trend line where (with the exception of the bubble), monthly payments tended to stick to a somewhat constant level.

And that fits in perfectly with your conclusions — prices really have followed rates pretty closely. But if we were to extend your study back in time, we’d find that this wasn’t nearly so much the case.

What do we make of this? Well, it happens that this is actually a fairly controversial topic in finance generally.

One camp claims that lower rates justify higher stock valuations, pointing back to 30-40 years of a clear correlation there. The other camp points out that prior to that period, there was no such correlation! (Here is an article exploring some of the long term data). There are other arguments as well, such as: if low rates are such a benefit, why are stock valuations in Europe and Japan much lower than the US, while their rates are ALSO lower? IE, it seems that this relationship has only taken place in the US, which undermines the idea of a causal relationship.So I just wanted to put that out as a note of caution here. xbox’s analysis happened to cover the period where there was an unusually strong relationship between rates and the prices of RE and risk assets generally. But, this relationship is not written in stone.

Now, let’s say the relationship does remain intact. xbox’s results jibe with my general view that even through prices look high, when you consider interest rates, they aren’t nearly so bad.

However, based on these charts I’ve refined my view a bit. Looking at my monthly payment charts, I was thinking, we’re still below the historical (post-1977) median. But that includes the prior regime. If we only look at the 90s+ regime, with that tight relationship between rates and prices, then we ARE in fact overvalued even considering how low rates are. xbox’s charts do a good job of showing that. But, it’s a reasonable level of valuation, part of the normal ebb and flow, and nothing I’d consider remotely bubble-like. (Of course I mean overvalued based on this model… there are of course things going on outside the model, eg long term supply and demand changes, which could impact fair value.)

The other thing to consider is that if the rate/price relationship remains intact, this doesn’t tell you much about future prices anyway, UNLESS you want to posit that you know what rates are going to be. It’s my view that rates (and inflation, which heavily influence nominal rates) are poorly understood, and that the world’s most preeminent economists and asset managers disagree on what the course of rates will be. IE, I don’t think anyone can really make a high confidence forecast on rates. So IF the rate/price relationship remains intact, it is a fact that any home price forecast has an embedded interest rate forecast.

May 29, 2021 at 12:17 PM #821927ParticipantExactly where I was going. Desirability but there’s no way to measure that so one must relie on anecdotes. That something cannot be measured does not mean it’s not a vital part of the equation and should be dismissed

May 29, 2021 at 12:36 PM #821928svelteParticipant“Mortgage/tax payment on SD single family home divided by equal-weighted SD rent and per-capita income”

Appears to mean (SD SFR mortgage payment / SD SFR tax payment) / (SD rent payment + per-capita income).

Or does it mean

(SD SDR Mortgage + tax payment) / (SD rent payment + per-capita income)I’m not sure how that correlates to XBoxBoy’s data on house prices. I guess you could argue that house prices correlate to mortgage payments, but I’m not sure that’s true. And what any of that has to do with rent or income I’m not sure.

May 29, 2021 at 12:42 PM #821929Rich ToscanoKeymaster[quote=svelte]”Mortgage/tax payment on SD single family home divided by equal-weighted SD rent and per-capita income”

Appears to mean (SD SFR mortgage payment / SD SFR tax payment) / (SD rent payment + per-capita income).

Or does it mean

(SD SDR Mortgage + tax payment) / (SD rent payment + per-capita income)I’m not sure how that correlates to XBoxBoy’s data on house prices. I guess you could argue that house prices correlate to mortgage payments, but I’m not sure that’s true. And what any of that has to do with rent or income I’m not sure.[/quote]

It’s the latter. It correlates because it’s measuring monthly payments vs. “inflation” (xbox was using CPI, I use wages and rents) so should come up with similar results.

May 29, 2021 at 3:33 PM #821930Participant[quote=sdrealtor]For me the question is what explains the rest of it. Why do prices rise more and faster here than Cleveland? Why do single family homes rise more than condos. Why has beach area properties appreciated more than East County?

While he did an excellent job, I think it’s just showing how markets behave in general and I’m always looking for the exceptions that allow one to beat the market. Am I missing something?

[/quote]It’s important to keep in mind that the above charts and data do not answer most the questions you are asking. These charts and data are really only about the cause of the rise in house prices over the last 30 some years in a broad area. (San Diego in this case) And as you have pointed out previously, that relationship might not be causal.

Additionally, this data and charts do not explain any of the deviations from the expected price such as the housing bubble we saw in early 2000’s. So, clearly the relationship between interest rates, inflation, and house prices doesn’t hold true at all times.

I could make some speculative guesses as to why prices didn’t rise as fast in Cleveland, and why they rose even faster in Silicon Valley, but without data, they would just be guesses. But in this thread I’m trying to stay within Piggington’s motto: “In God we Trust, Everyone Else Bring Data.” (Although admittedly I do think that question could be a really interesting discussion. But it probably needs its own thread.)

May 29, 2021 at 3:52 PM #821931ParticipantGotcha and I agree interest rates and inflation are a big influence on home prices. To me it’s like saying water is wet because it’s obvious they influence all asset prices. However there are not the sole cause. There are other significant forces which can’t be so easily measured but none the less are very powerful. I took exception to the inference that inflation and interest rates explained all or nearly all of the price changes.

And I’ve been having that discussion for years but others refuse to acknowledge that which I provide evidence of though not perfect statistical data as it does not exist because it can’t be measured

May 29, 2021 at 4:39 PM #821932gzz

ParticipantYou have some places with expected rent and demand for housing generally expected to decrease over time. That completely changes the PV of housing, especially when rates are low.

This is very good work xbox.

May 30, 2021 at 3:04 PM #821933ParticipantI’ve got some new data from Rich that I want to share, and I’ve been working with the charts and trying to develop some insight into what I’m seeing.

Here’s the same chart as I used above but with data from Jan. 1977 through April 2021.

The orange is the CaseShiller price and the blue is the price I would anticipate based on interest rate and inflation. (From here on out I’m going to refer to the anticipated price based on interest rate and inflation as the XValue, just because that’s easier to type.) There are two things to notice before jumping to any conclusions about this chart.

One of the first insights I had when looking at this chart is that the vast majority of the time house prices were overvalued in the last 45 years. Then I realized that this chart assumes that the Case Shiller and XValue are equally valued in January 1977. But the chart has very few times that is true. Simply because my data starts on January 1977 doesn’t mean the Case Shiller and the XValue would be equal at that time. So, let’s take a look at the chart with the Case Shiller undervaluing the XValue by 30% at January 1977.

Now we see about an equal amount of overvalue and undervalue.

This also lead me to realize that without some anchor to tell me that houses were fairly priced on a specific date, it becomes very difficult to use these charts to tell if currently (or at any specific time) housing is overpriced or underpriced.

Previously I claimed that over the long term the vast majority of house price rise could be explained by interest rate changes and inflation. (Short term that isn’t so true, but long term it is) Now that I have more data I think that claim still holds up very well. To help see that, I can fit a second order polynomial to each data series to find the slope.

Here we see a purple line which is the fit for the Case Shiller, and the yellow line which is a fit for the XValue.

The next issue is that as prices go up, price increase look bigger than they are when measured in percent. Imagine this scenario: You buy two houses, one for $500k and the other for $200k. Twenty years later the first house is worth $1.5m and the second house is worth only $600k. So the first house has appreciated $1m and the second house has appreciated $400k. Which one has a better return? The answer is neither, they both tripled in price. But the higher the starting price the bigger the increase should be numerically. So, when we look at the above chart, the most recent years look like a lot more appreciation but as a percent not so much. To compensate for this it’s important to work with log scale on the charts if you want to talk about growth rates. So, here’s the same chart but with a log scale on the Y axis and no slope lines.

And now with the slope lines.

-

AuthorPosts

- You must be logged in to reply to this topic.