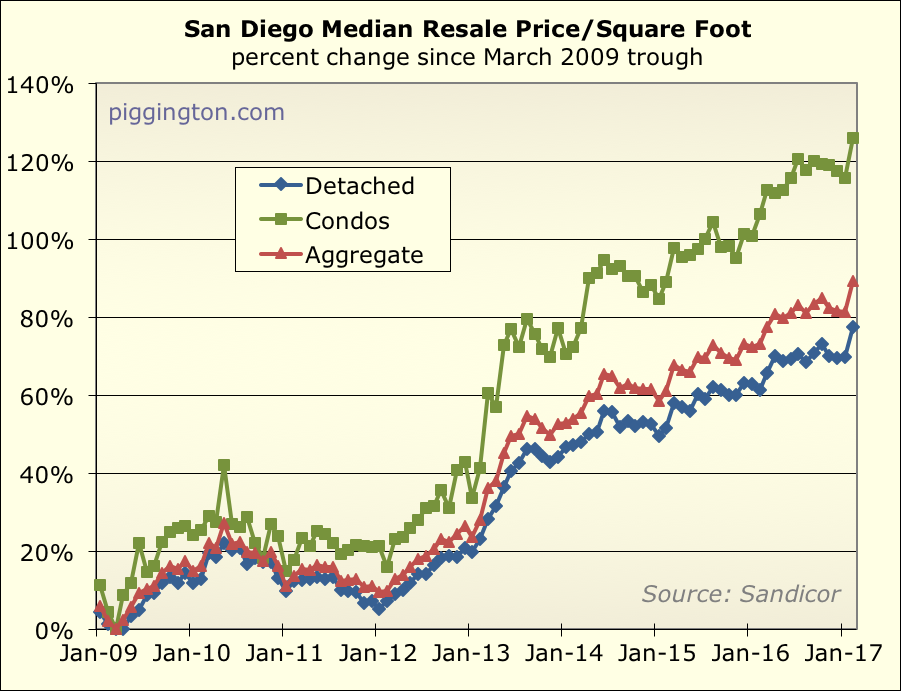

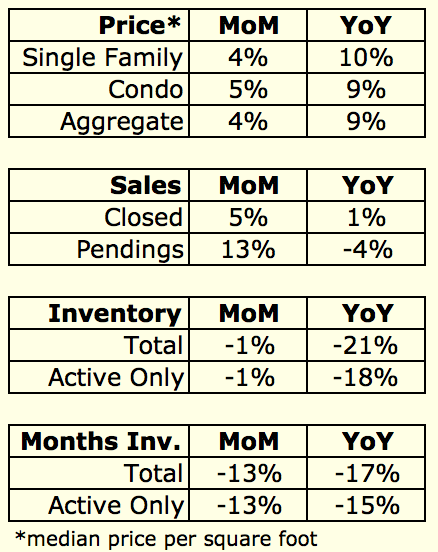

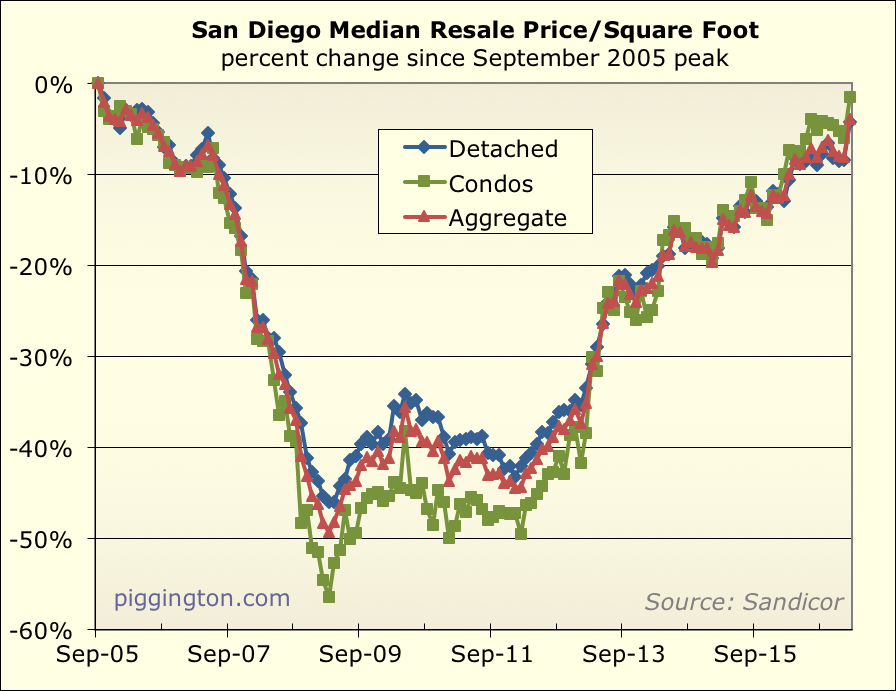

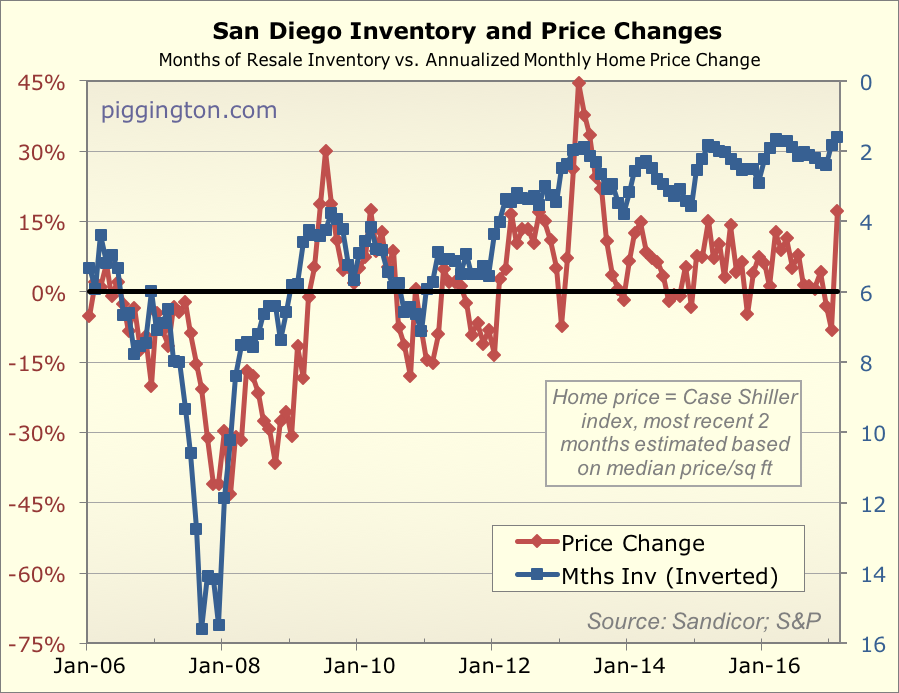

The median price per square foot surged in February:

This level of price increase is in some sense what should be expected

given the pretty severe lack of inventory, but to see prices go up so much in a single month is unusual:

Here’s a summary chart for the month, showing that price per square

foot for single family homes (much more reliable than condos) popped by

4%:

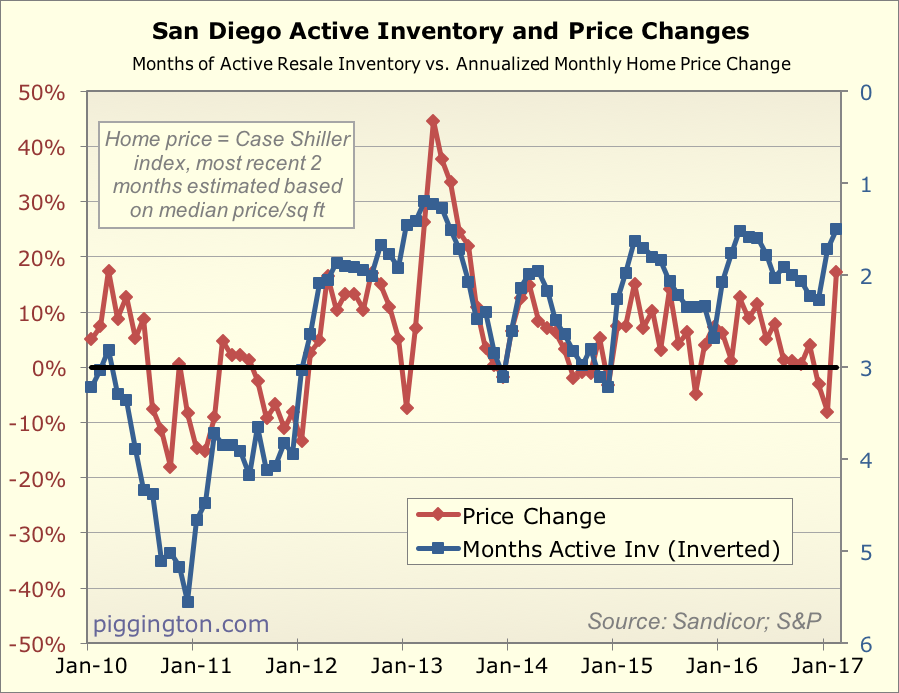

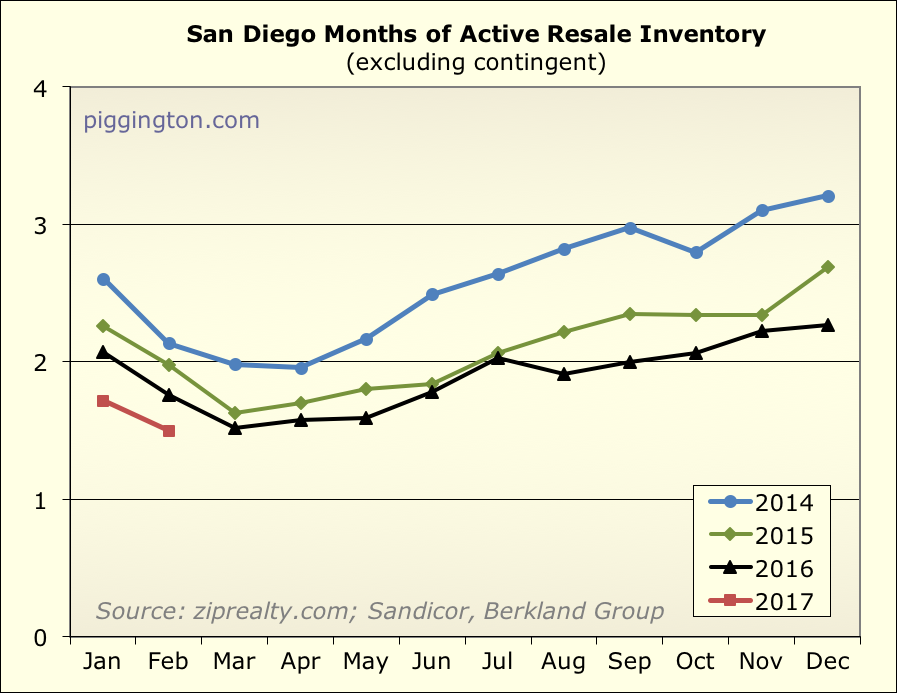

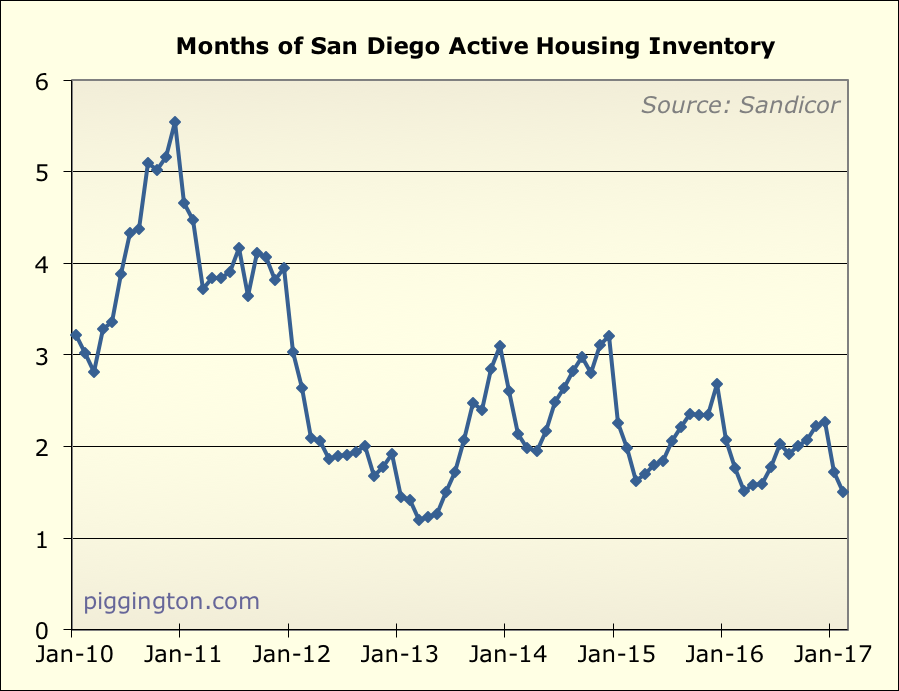

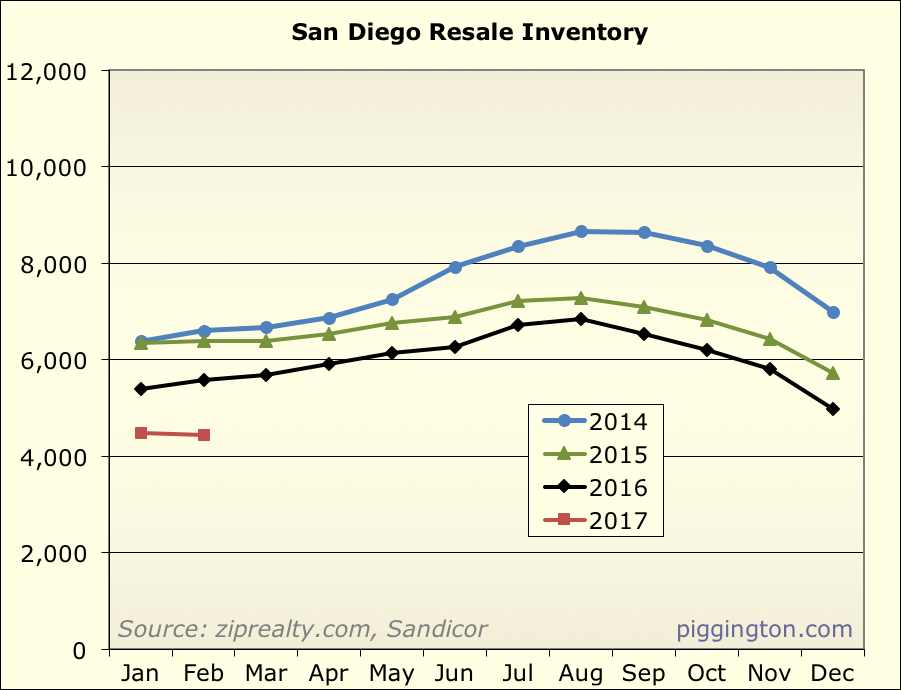

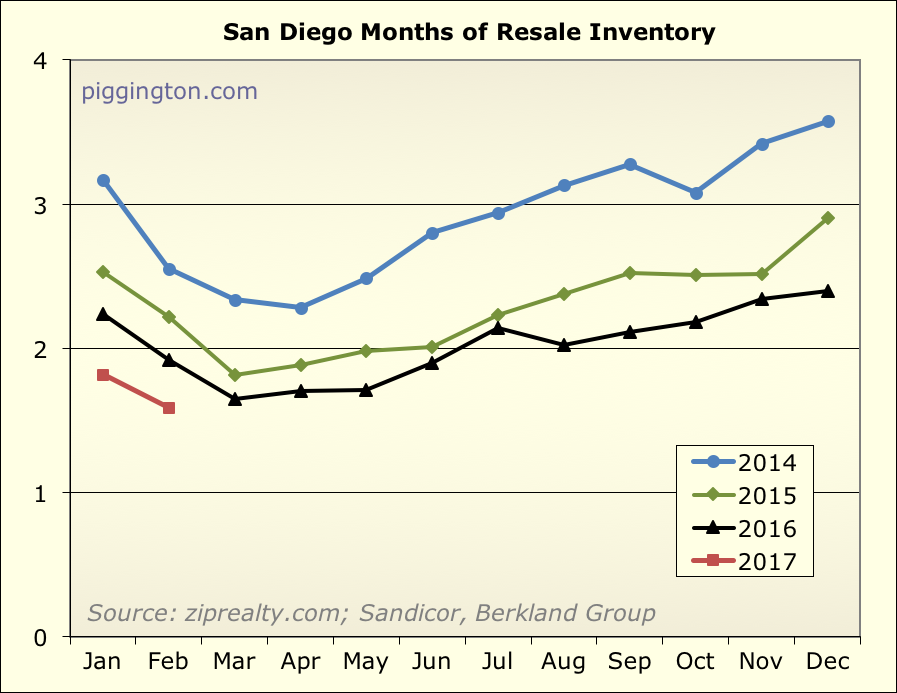

Note that months of inventory is 13% below last year’s

already-pretty-low level. Here’s how that metric looks over the

past few years:

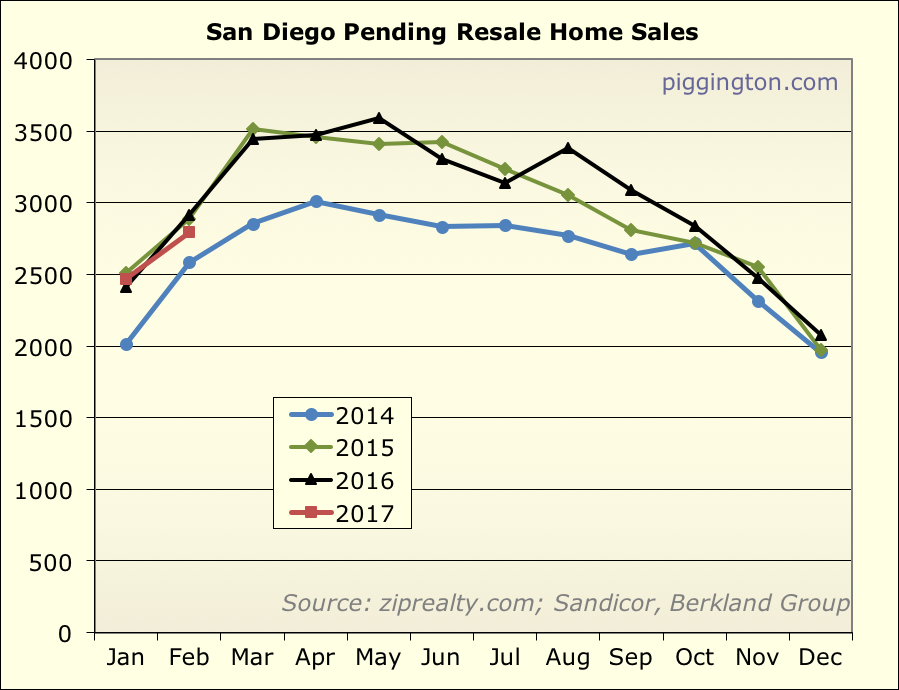

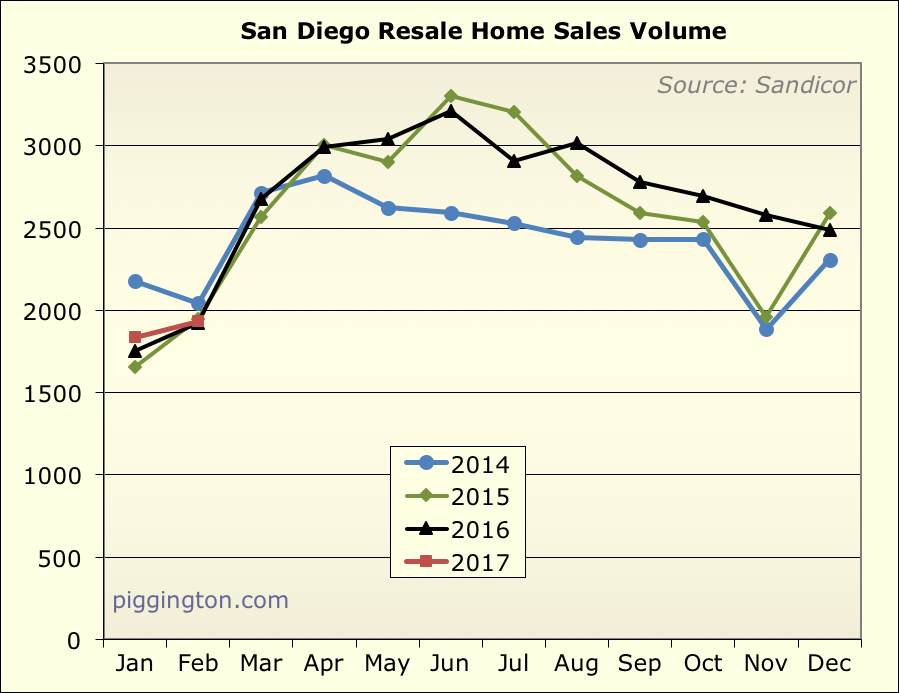

This is less a results of sales volume, which is healthy but very

normal for recent years:

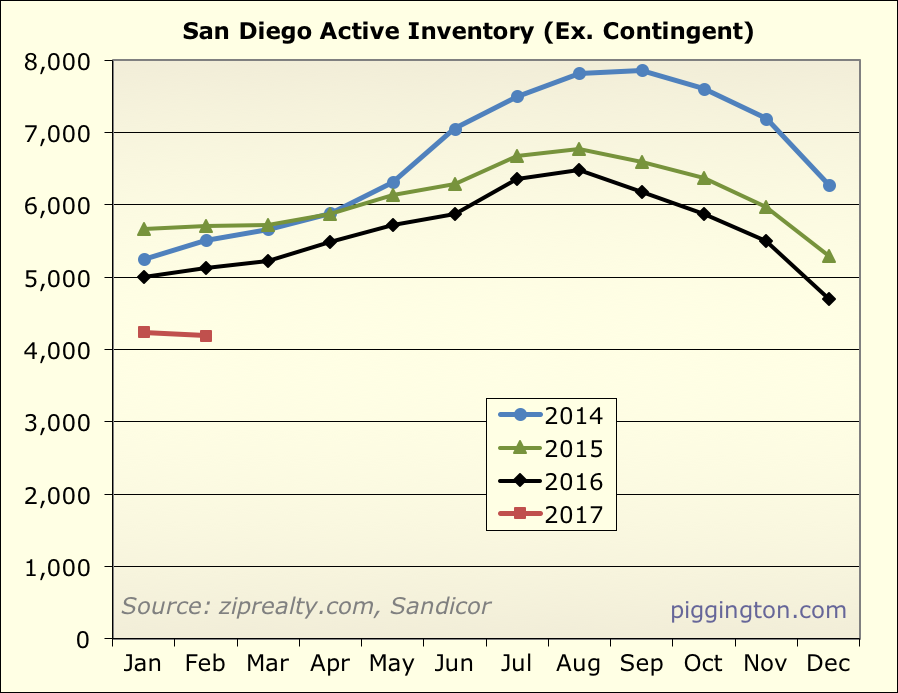

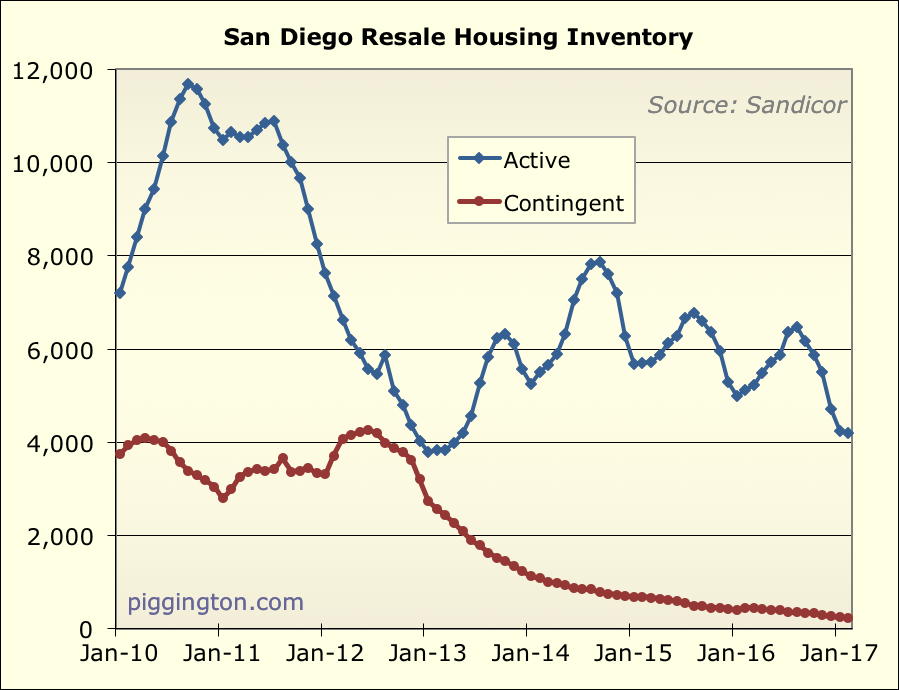

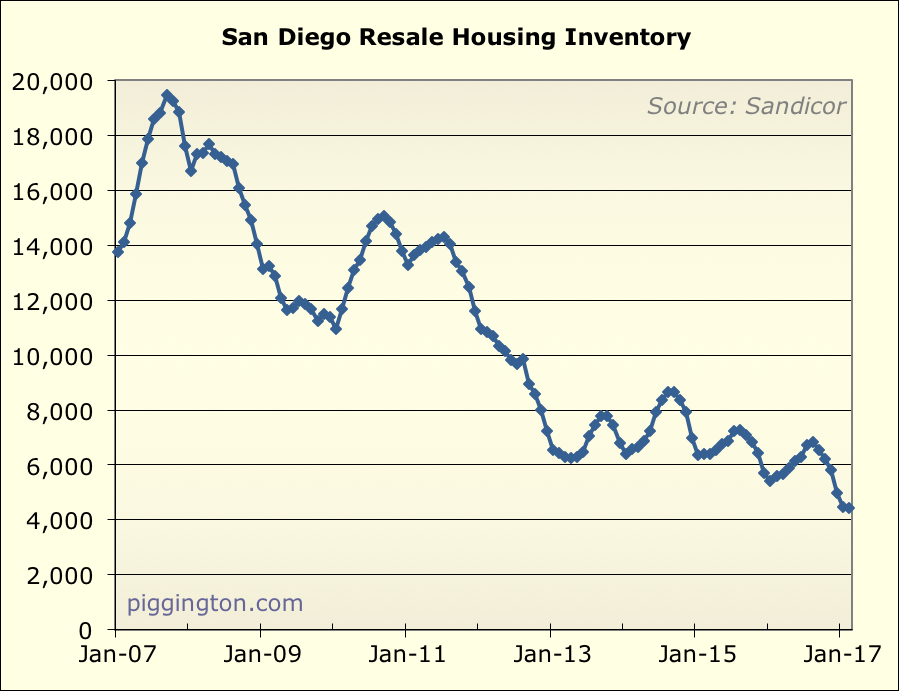

…and more a result of the severe lack of homes for sale:

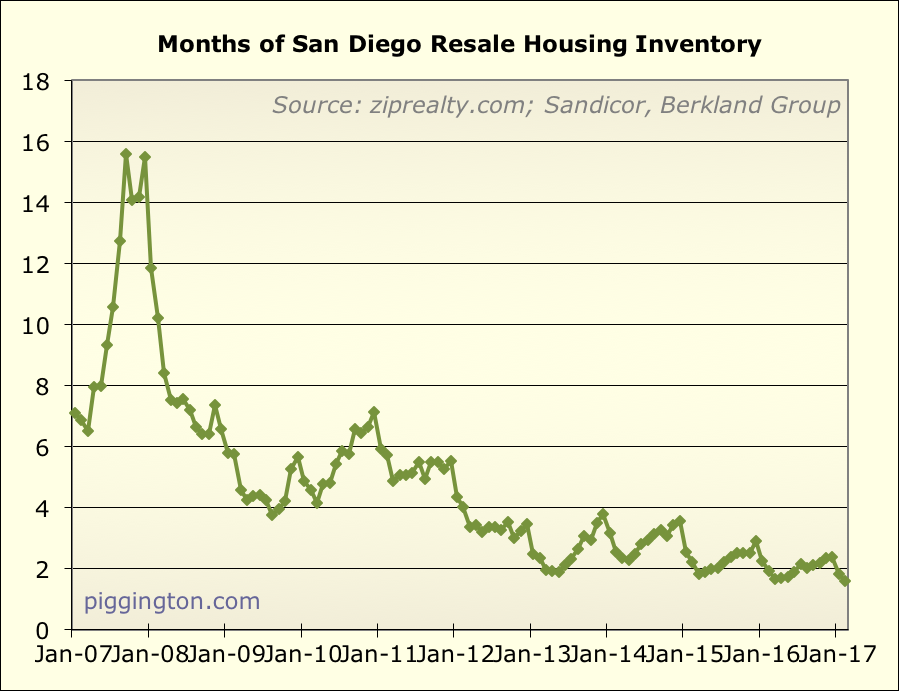

In fact, in terms of active inventory, we are approaching early-2013

levels of scarcity.

And we know what happened then! (In case your memory needs

jogging: SD Case-Shiller rose almost 19% between January and September

of that year).

If more supply doesn’t hit the market soon, things could get

interesting…

More graphs below:

Case Shiller inflation

[img_assist|nid=26273|title=Case Shiller inflation adjusted|desc=We might hit the nominal peak from 2005 by the end of the year. I much prefer the Case-Shiller index adjusted for inflation:|link=node|align=left|width=100|height=66]

Rich, Thanks for doing this.

Rich, Thanks for doing this. That lack of inventory is indeed rather unsettling. Interestingly, from what I see, the top end of the market (over 3 million) is actually much slower. Few houses going pending and price increases have come to a halt. Inventory is not that tight either. I doubt that changes much of anything for those under 1-2 million. (And alas, I can’t provide real data to back up my observations like your charts so who knows maybe I’m completely wrong.)

Sentiment here is 90% bullish

Sentiment here is 90% bullish — does this mean the market is going to turn … 🙂 When the shoeshine guy starts talking about investing, perhaps it’s time to run…

North County coastal has been

North County coastal has been WAY above 2005-07 peak for a year or two already.

Is the main difference

Is the main difference between your numbers and the median price discussed in the following article, that yours takes into account ppsf, instead of just median?

http://www.sandiegouniontribune.com/business/real-estate/sd-fi-corelogic-feb-20170320-story.html

If there were more smaller, “starter” homes, which I think have had a disproportionately higher increase, that could explain part of the jump/noise?

biggoldbear wrote:Is the main

[quote=biggoldbear]Is the main difference between your numbers and the median price discussed in the following article, that yours takes into account ppsf, instead of just median?

http://www.sandiegouniontribune.com/business/real-estate/sd-fi-corelogic-feb-20170320-story.html

If there were more smaller, “starter” homes, which I think have had a disproportionately higher increase, that could explain part of the jump/noise?[/quote]

Yes on both counts…

Wow great news, thanks for

Wow great news, thanks for compiling and graphing all this data.

About half the price spike seems to be just correcting the unexplained lack of growth in Q4 2016. Even then, we are now above the trend line of the past three years.

These strong February prices will be useful in setting higher comps for the spring and summer selling season.

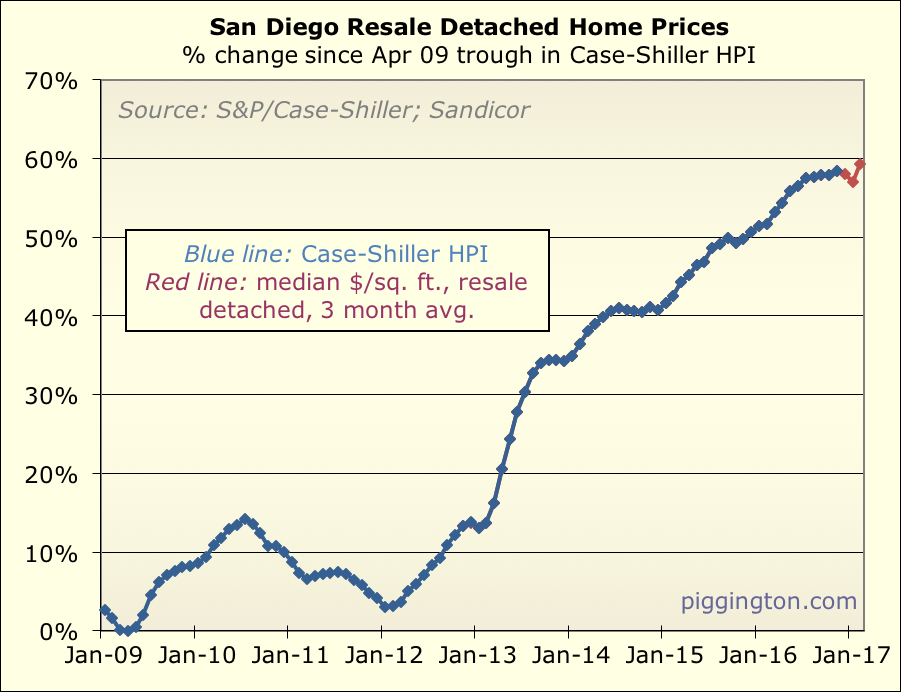

The bonkers price spike of 2012-13 started when inventory was double current levels.

I can’t wrap my head around

I can’t wrap my head around it … why is inventory so low now? I am going to guess that 5-6 years ago there weren’t that many units being built either. Population has mostly always been on a rising trend – or not?. Is it short term rental explosion? Higher rate of out of state immigration? Foreign buyers? I believe it’s been a few years of about 30% investor bought units, perhaps post bubble investor racked up a ton of units? Help?

Onateag wrote:I can’t wrap my

[quote=Onateag]I can’t wrap my head around it … why is inventory so low now? I am going to guess that 5-6 years ago there weren’t that many units being built either. Population has mostly always been on a rising trend – or not?. Is it short term rental explosion? Higher rate of out of state immigration? Foreign buyers? I believe it’s been a few years of about 30% investor bought units, perhaps post bubble investor racked up a ton of units? Help?[/quote]

“Lower inventory begets lower inventory; a downward pressure cycle continues. If one cannot find properties to move up to, they will not list or sell their current homes.”

There are a list of reasons in this article: http://www.inman.com/2015/04/02/why-is-housing-inventory-so-low/

1. Exceeding capital gains exclusion on primary residence.

2. Sustained low-rate environment for almost 7 years.

3. Value disruption/reset after 2008. Cash buyers are holding on to lucrative rental properties.

4. Values not at peak levels across the country. A portion of homeowners are still underwater in San Diego in ‘real’ value.

5. Sense that values will continue to climb. Why sell now when prices will rise?

6. Where would I go?

7. Stunted new development since 2007.

8. Investor bought units

Also – from that other thread. Some numbers on San Diego wealth increases (in real value) that shocked me:

From 2010 – 2015, detached housing in San Diego county grew by just over 8800 units.

In that same period, households in San Deigo county making more than $200K/yr grew by 15,400 households. Household making $150K-$199k grew by 8900 households.

bewildering wrote:

6. Where

[quote=bewildering]

6. Where would I go?

[/quote]

This is a big one. Even if you feel your home is overpriced, it’s not like it’s always easy to sell, move your family, and rents are sky high too. Someone paying $1600 for their mortgage won’t want to turn around and rent for $2000/mo.

My street has a lot of retirees who bought in the 70s, and it does seem like these prices are motivating them to finally downsize and sell.

I have the impression that

I have the impression that the valuation time series is less of a Markov chain and more like something with a long term memory. For example, if lower inventory and high price are due to the bubble busting and low interest rates ending after that, then their effect will be persistent in today’s and future price as long as: a) who bought at bubble price isn’t forced to divest its home equity due to other market or societal forces; b) investors have no enticing alternative to their cash flow fueled by the low mortgage rates locked in with multiple refinances and high rents.

I wonder what kind of incentives to higher density housing construction would be effective in this environment.

By the same argument,

By the same argument, wouldn’t the bubble-burst prices also be “sticky?”

I’ll bet that it’s more like an under-damped system.

Some things are stickier than

Some things are stickier than others. And I was focusing on inventory and not price.

Bewildering’s article has

Bewildering’s article has factors explain rising prices very welll than low inventory.

We are going up less than during the bubble despite tighter inventory that is at or below historical records. “It is a tight seller’s market” does not explain this. Something else has changed.

My theories are prices are below normal “market clearing” prices, leading to a shortage. My evidence is very low monthly payments make homes cheap, but banks sre reluctant to loan money more than 10% above comps from the prior 12 months. As we learned in econ 101, prices below the market equilibrium mean a shortage.

Another trend that has been going on for a while that partially explains this is internet listings allow everyone interested in a property to view it the same week it is listed. If it is priced right, that is all the time it will take. So inventory that is properly priced may leave the market in a week rather than 5 or 6 weeks it might have taken 20 years ago.

(1) Prices are not below

(1) Prices are not below equilibrium everywhere in the county. Not while crappy 2-bedroom condos in places like Escondido, Chula Vista, and Vista are approaching $200k, and those same condos rent in the mid-$1000s. (Say $1600/mo).

Subtract HOA, mortgage, insurance, tax and you don’t get much saving vs renting if any. Contrast that to other world cities (even NYC), where the spread between rents and costs in secondary areas (say central to eastern Queens or Staten Island) is much bigger.

(2) It’s psychologically driven. People think that because inventory is low, they have to buy now, further driving up prices. Anything happens to flatten prices, the urgency will be gone and the demand will shrink quickly.

It’s not a bubble driven by easy credit and flipping, but the fact that there’s a psychological driver (low inventory, expectation of rising prices) is the same.

(3) Internet sales listings were also around in 2010 to 2013, in fact, just as available as today.

SPD, buy v rent depends on

SPD, buy v rent depends on tax bracket. Someone renting a “crappy” 2 bedroom in a working class distant suburb may be better renting, but such people are not much driving the SD market. Also, with payment ratios near record lows and incomes growing, buy v rent is better than most of San Diego’s history.

Well, let’s hope Trump keeps

Well, let’s hope Trump keeps “winning” and that the original predictions of the results of his win come true 🙂

(a) opportunity

(b) we won’t see another Repub in the White House till 2036, and that would be a lovely thing

Where are these “very low

Where are these “very low monthly payments” you all speak off? A good 4bd is >$700k, even with 20% down you’re approaching $4k/month, how is that low?

The 4 bedroom I purchased in

The 4 bedroom I purchased in 2015 is rented for $4200 and the payment is $3600, most of which is tax deductible or reducing my debt, so really is more like $2400 Add in lost interest on my DP and that makes my cost to own about $2700.

Prices and rates are higher now, but that still leaves a whole lot of room for buying to beat renting. And that is without any assumption of further appreciation.

Can you point to recent sales that don’t pencil out as better than renting for a primary residence for a couple making 100,000 to 250,000? There might be some out there, but the still-large share of cash buyers indicates to me that a lot of people see SD prices as pretty low relative to expected rents. Which is exactly what Rich’s payment ratio chart says.

gzz wrote:The 4 bedroom I

[quote=gzz]The 4 bedroom I purchased in 2015 is rented for $4200 and the payment is $3600, most of which is tax deductible or reducing my debt, so really is more like $2400 Add in lost interest on my DP and that makes my cost to own about $2700.

Prices and rates are higher now, but that still leaves a whole lot of room for buying to beat renting. And that is without any assumption of further appreciation.

Can you point to recent sales that don’t pencil out as better than renting for a primary residence for a couple making 100,000 to 250,000? There might be some out there, but the still-large share of cash buyers indicates to me that a lot of people see SD prices as pretty low relative to expected rents. Which is exactly what Rich’s payment ratio chart says.[/quote]

HUH? His charts say exactly the opposite of that:

http://www.voiceofsandiego.org/wp-content/uploads/2016/10/san-diego-home-expensiveness101116.png

That is not the payment ratio

That is not the payment ratio chart.

Show’s over millennials, you

Show’s over millennials, you are priced out.

Millennials are not priced

Millennials are not priced out. Monthly payments on a house are much lower than the historical average compared to rents and incomes. Down payments can be an issue, but 5% downpayments still exist for people with good income and credit. I am a millennial and just got my third property a few months ago, all nice places 2-4 blocks from the beach.

The trends of small family size and delayed children also mean millennials will have more help with down payments than prior generations. For California natives, growing up middle class generally means your parents are sitting on half a million or more of home equity that can be tapped for a down payment gift, and this happens all the time.