Remember when housing started to falter back in 2006, and the

mainstream economists’ version of bearish tough talk was to predict

that prices might just go up slightly less quickly in the future?

Tim of the always amusing Seattle Bubble blog recently dug

up a prime example of that very thing, wherein Forbes magazine sternly

informed readers:

“Get used to it–the seller’s market is closing up shop.”

…and:

“Now the question is more how hard is it going to land…”

Wow, that’s some fairly bearish-sounding rhetoric. I guess that’s

why Forbes’ teamed up with Moody’s to determine that prices would…

pretty much just keep going up. (Fun graphs after the jump…)

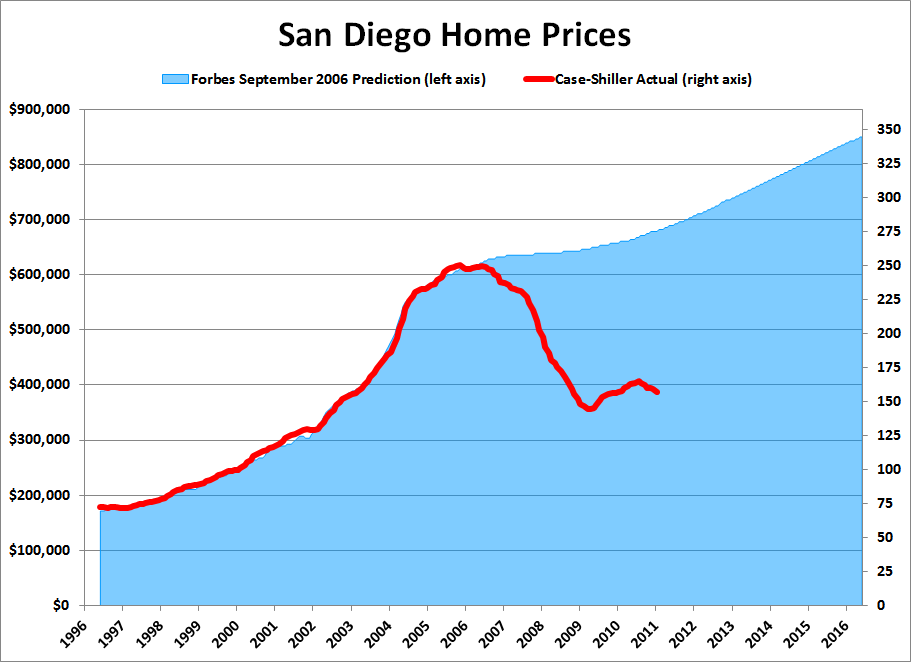

Here’s their San Diego prediction as of late 2006. Note that

prices are predicted to flatten out for what appears to be 3 months

(even that probably earned them thousands of hate emails from the

permabulls) after which it’s onwards and upwards as San Diego

proceeds smoothly into affordability oblivion:

Tim’s recently put up a post revisiting

the

Forbes

article and charting actual Seattle home prices over

their predictions. As a favor to us San Diegans, he was kind

enough to do the same for their San Diego chart. Click the chart

for a bigger version. Thanks Tim! And thanks to Moody’s and

Forbes for the entertainment.

those were the good ole days.

those were the good ole days.

now we are left arguing about how someone’s Thomas Guide in 1884 showed the land 4S sits on was colored white instead of yellow…

really, it seems like almost

really, it seems like almost anyone who bought after 02 is underwater or has marginal equity.

Anyone who did HELOC or cash out, or bought later is wildly underwater.

patb wrote:really, it seems

[quote=patb]really, it seems like almost anyone who bought after 02 is underwater or has marginal equity.

Anyone who did HELOC or cash out, or bought later is wildly underwater.[/quote]

Hmmm… Most people who bought after ’02 were simply selling one place and buying another, so they funded the insanely high price on the purchase with an insanely high price on the sale. It’s only first-time buyers who bought after ’02 who are truly underwater.

As for those who HELOC’d or cashed out, they got the sweetest deal of all – they got to spend money that they never earned, and that they never have to pay back.

“As for those who HELOC’d or

“As for those who HELOC’d or cashed out, they got the sweetest deal of all – they got to spend money that they never earned, and that they never have to pay back.”

I’m not sure where you’re getting that idea. HELOC loans are exempt from California’s no recourse laws. The only way people who took those are going to avoid having to pay the money back is if they file bankrupcy and lose everything or can get a short sale approved by both the lenders of their original mortage and of the HELOC.

“HELOC loans are exempt from

“HELOC loans are exempt from California’s no recourse laws. ”

Not if the HELOC was a purchase loan, which was very common among post-2002 first time buyers such as myself. Purchase HELOCs are non-recourse. However, if you took out a HELOC after purchase, then you are out of the “no recourse” statute.

I’m a prime example. Bought first home/condo in the summer of 2005, interest only 0% down. $290k first mortgage and $70k HELOK. The place is now worth less than $160k, based on recent identical unit sales. But because my loans were purchase money, I am protected by the statute and can walk away with only my credit harmed (small price to pay to get out of $200k hole).

wooga wrote:”HELOC loans are

[quote=wooga]”HELOC loans are exempt from California’s no recourse laws. ”

Not if the HELOC was a purchase loan, which was very common among post-2002 first time buyers such as myself. Purchase HELOCs are non-recourse. However, if you took out a HELOC after purchase, then you are out of the “no recourse” statute.

I’m a prime example. Bought first home/condo in the summer of 2005, interest only 0% down. $290k first mortgage and $70k HELOK. The place is now worth less than $160k, based on recent identical unit sales. But because my loans were purchase money, I am protected by the statute and can walk away with only my credit harmed (small price to pay to get out of $200k hole).[/quote]

Regarding Heloc recourse:

The one way to take a non-purchase money loan and make it non-recourse is to use it to improve the property.

Of course that will probably require an attorney’s letter.

Regarding your situation:

With the exception of some credit unions, most lenders will let you short sell.

While missing payments will still damage your credit, a short will keep you from being part of the 10 year moratorium on home lending.

Good luck.

Actually there is a one

Actually there is a one action rule in CA that can effectively make a recourse loan a non-recourse loan. An example of this would be a case where you have a large 2nd and a first that isny underwater. Let’s say you have 300K 1st and 250K 2nd but your house is only worth 350K. You could keep paying your first and stop paying your 2nd. That would force the 2nd to foreclose to get anything. Once they foreclosed they would give up their right to recourse.

This is not to say this scenario is common but rather to point out that the laws are not so simple and straight forward. Each situation can be different and anyone with udnerwater loans should speak to someone that knows what they are doing not just some realtor who decided to claim they were a short sale expert on their business card or website. There are plenty who do so without having compelted a single short sale transaction and who have no idea of what the intracacies are in the CA foreclosure laws.

sdrealtor wrote:Actually

[quote=sdrealtor]Actually there is a one action rule in CA that can effectively make a recourse loan a non-recourse loan. An example of this would be a case where you have a large 2nd and a first that isny underwater. Let’s say you have 300K 1st and 250K 2nd but your house is only worth 350K. You could keep paying your first and stop paying your 2nd. That would force the 2nd to foreclose to get anything. Once they foreclosed they would give up their right to recourse.

This is not to say this scenario is common but rather to point out that the laws are not so simple and straight forward. Each situation can be different and anyone with udnerwater loans should speak to someone that knows what they are doing not just some realtor who decided to claim they were a short sale expert on their business card or website. There are plenty who do so without having compelted a single short sale transaction and who have no idea of what the intracacies are in the CA foreclosure laws.[/quote]

sdr and I know a few of those.

BTW sdr, sorry for hanging up quickly today.

I had people walking in while I was talking to you.

urbanrealtor wrote:sdrealtor

[quote=urbanrealtor][quote=sdrealtor]Actually there is a one action rule in CA that can effectively make a recourse loan a non-recourse loan. An example of this would be a case where you have a large 2nd and a first that isny underwater. Let’s say you have 300K 1st and 250K 2nd but your house is only worth 350K. You could keep paying your first and stop paying your 2nd. That would force the 2nd to foreclose to get anything. Once they foreclosed they would give up their right to recourse.

This is not to say this scenario is common but rather to point out that the laws are not so simple and straight forward. Each situation can be different and anyone with udnerwater loans should speak to someone that knows what they are doing not just some realtor who decided to claim they were a short sale expert on their business card or website. There are plenty who do so without having compelted a single short sale transaction and who have no idea of what the intracacies are in the CA foreclosure laws.[/quote]

sdr and I know a few of those.

BTW sdr, sorry for hanging up quickly today.

I had people walking in while I was talking to you.[/quote]

No problem and thanx for the tip. We should catch a concert together sometime and you will see that I am not as musically challenged as you once thought;)

Well, if I ever have a

Well, if I ever have a compelling need to see REO Speedwagon (which is what I wanted to call the foreclosure bus tour) then we will see.

Only time I ever saw them was

Only time I ever saw them was at the first Live Aid concert in Philly. Dont think I’ll be seeing them again;)

“they got to spend money that

“they got to spend money that they never earned, and that they never have to pay back.”

They didn’t have to pay income taxes on it either 🙂

Hi Rich and assorted Piggies

Hi Rich and assorted Piggies :), would anyone be able to guide me to the Case-Shiller index, presented similar to the red curve in the charts above, for the Inland Empire area, particularly the primary cities of San Bernardino County? The IE area is, ‘sigh’, my area of abode and interest, alas.

On a side note, it is so comforting coming back to Piggington, 5 years on from that fateful day when I first surfed to the website, and seeing piggies, old and new. You all feel like my extended family, even though I’ve never met any Piggie in person. Such is the pull of the piggie!-Calidesigner

Thanks cali

Thanks cali d…

Unfortunately there’s no CS index for any Inland Empire cities, that I know of.

While I find these types of

While I find these types of posts kind of self-congratulatory and distasteful, there is something more troubling in this one.

Dr. Yun, the economist referenced in the Forbes piece, is not only still with the NAR, he is now the chief economist of NAR.

http://en.wikipedia.org/wiki/Lawrence_Yun

And for those of us who are giant collective action nerds, it is yet more troubling that he is a disciple of Mancur Olsen.

It is also important to recall that aside from a few skeptics and contrarians (Mr. R____ included among those) many of the seriously respected and reputable people who were paid to know what would happen were dead wrong.

Ben Bernanke in 2005

http://www.washingtonpost.com/wp-dyn/content/article/2005/10/26/AR2005102602255.html

David Lereah in 2005

http://www.amazon.com/Are-Missing-Real-Estate-Boom/dp/0385514344/ref=sr_1_1?ie=UTF8&s=books&qid=1197316917&sr=8-1

Rich and the perfesser in 2005

http://replay.web.archive.org/20050305004807/http://piggington.com/mania.php

Paul Krugman in 2005

http://www.nytimes.com/2005/08/08/opinion/08krugman.html?_r=1&scp=1&sq=krugman+hissing&st=nyt&oref=slogin

Mr. R___ himself has said that he did not expect the level of price retreat that came to pass.

http://lansner.ocregister.com/2009/03/13/blog-party-people-thought-i-was-a-complete-nut-job/16453/

My point is only that while determining that San Diego (or, for that matter, national) housing was a speculative bubble seems easy in retrospect, that is pure (or at least mostly) hindsight.

In 2005, many of us suspected that something was wrong. However, we were left with competing views.

On the one side we had the Federal Reserve and the NAR economists.

That said that we would see some cooling but that market fundamentals would avert any sort of real collapse.

The other side consisted of partisan columnists, non-economists, and bloggers who constantly made jokes about opium dens.

They said that the thing in which we held a large percentage of our net worth was soon going to lose (and thus our net worth would lose) more than 20% of nominal value.

Funny thing:

It became clear after not too long that the contrarian skeptics were right. And everyone else was wrong.

As the scope of that wrongness came into focus, we got a better idea of what we were looking at.

In sum:

It was clear something was unsustainable and problematic. However, it is understandable, given the context that few could accurately predict the direction things took (and continue to take).

Some humility is required when looking at the past mistakes of others.

Oh, and for those who forgot:

http://replay.web.archive.org/20050220094419/http://piggington.com/staff.php

urbanrealtor wrote:While I

[quote=urbanrealtor]While I find these types of posts kind of self-congratulatory and distasteful,

[/quote]

And there I was starting to type a rebuttal, when in the second half of the sentence you did it for me:

[quote=urbanrealtor]

there is something more troubling in this one.

Dr. Yun, the economist referenced in the Forbes piece, is not only still with the NAR, he is now the chief economist of NAR.

[/quote]

That’s the whole point. It’s not about being “self-congratulatory,” it’s about holding people accountable. People who are STILL in the same positions they were back then, and still being asked as experts to give guidance to people about important decisions. People are still listening to Bernanke and Forbes and Zandi and (less so, admittedly, although he is still constantly quoted in the press) Yun. That’s a problem.

It’s actually an outrage that there is so little accountability, and that a track record of being quoted a lot trumps a track record of not being constantly and abysmally wrong. But outrage is boring and kind of a downer. So I take it in the mockful direction instead. It’s multitasking.

I agree with you that humility is important because we are all wrong at times. But that doesn’t mean that you should give a pass to people who were horrifically wrong in a way that was PREVENTABLE had they actually taken the time (or in some cases, eg Yun, put aside their self interest) to take a peak at what I think were glaringly obvious fundamental indications that very clearly showed that they were wrong.

I’m sorry if you find it “distasteful” or if you incorrectly interpret it as “self-congratulatory.” And I know I’ve been wrong about some things and will be wrong again, and I’ve never pretended otherwise. But there is a difference between these two things:

1. sometimes being wrong in a market that is a chaotic system based on endless inputs, many of which are completely psychological or random

2. being totally incompetent and utterly missing out on the obvious as these people did despite the fact that it was their full time job to know what was up

So despite your objections I will continue to occasionally post a reminder of how totally badly some parties blew it during the bubble – ESPECIALLY when these parties to this day continue to be put on a pedestal of expertise.

BTW you didn’t have to go back to the wayback machine for that opium reference; it’s in the FAQ: http://piggington.com/frequently_asked_questions

I have been a sieve for

I have been a sieve for economic news since I was a kid back in the 70s.

Perhaps that is why I got into the gold sector in 02 and forsaw the bubble (as many of you here did) sold my California house in April of 04.

NOTE..

Selling my house to this day was a mistake. North Park has held up and from my estimation if the same house was for sale today I would pay about 5% more than I sold for and of course my tax base would be much much higher. I hope sometime soon that decision to sell ends up being the right one.

Anyway, regarding the economists. Over the years I have noticed that the majority of economists are wrong, it is usually the smallest minority that is right.

Right now most economists claim the economy will continue to grow and blah blah blah. The minority says a double dip is on its way.

I see evidence all over the place the economy is about to turn into recession.

1. despite the end of Monetary Printing number 2 (qee 2) long rates are declining. This defies logic unless it is telegraphing a slowing economy.

2. Oil and food prices are squeezing the consumer and is stalling consumer spending.

3. Despite sky rocketing commodity prices, the corresponding stock prices are refusing to set new highs.

4. Signs of stock market topping.

5. Demands of cut backs in Government spending. States cutting back and the end to numerous stimulative Governmental programs.

6. Despite Ben Shalom Bernanke’s refusal to raise rates to tame inflation, most large economies across the globe are beginning interest rate increases, slowing their growth, meaning they will buy less of our exports.

7. The biggest sign of all…….most economists have discounted the possibility of a double dip recession.

When the stock market starts tanking and the economy starts faltering later this year, Qe3 will be announced. Be sure to take advantage of the upcoming correction in the gold sector to protect your future..

Who would have guessed it

Who would have guessed it would end up looking like a classic bell curve?

The big long term question is if the 8% a year price increase can continue. This is approximately the rate at which the dollar has declined over the last century. Coincidence?