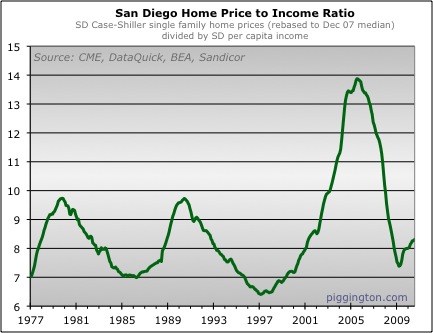

The continued rise in San Diego home prices has pushed valuation ratios

northward — but according to the home price-to-per capita income

ratio, prices are still fairly reasonable:

The price-to-income ratio is just 2% over its long-term median.

Of course the median was pulled upward by the protracted period of high

prices this decade, so another way to compare with past valuations is

to note how far below past housing cycle peaks we are. I am

referring here to the peaks in 1979 and 1990. Valuations during

this decade’s bubble were driven into the stratosphere by a frenzy of

reckless lending that won’t be repeated in our lifetimes, so that’s not

really a good comparison. But the similar (to one another) peaks

in 1979 and 1990 suggest an upper limit to how high valuations can get

in the absence of ubiquitous neg-am, no-doc loans. Even by this

measure, the price-to-income ratio is not raising any red flags —

July’s figure was a comfortable 17% below the 1979 and 1990 peaks.

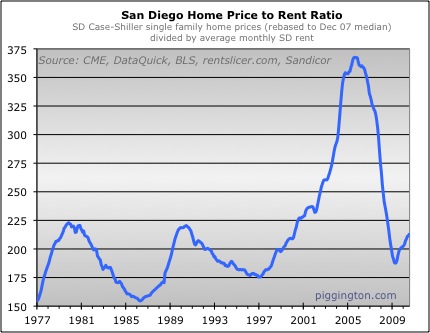

The price-to-rent ratio is telling a bit of a different story. While

only 6% above its median, this ratio is just 4% below the average peak

value in 1979 and 1990. If you cover up the wild 2000s ride with

your hand, you can see that valuations by this measure are approaching

what had formerly been housing boom peaks back in the old days.

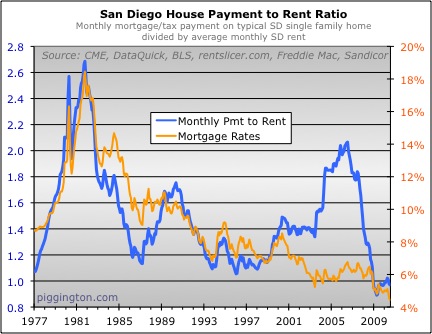

Ultra-low mortgage rates are no doubt playing a role in pushing prices

up. The charts below show that the monthy payment-based ratios

are still near all-time lows thanks to mortgage rates that are at all time lows during the time

period measured.

As I always point out in these updates, the mortgage rate level may be

of paramount interest to an individual buyer who is locking in a

long-term loan rate, but it’s just not all that relevant in determining

what is a long-term sustainable level of housing valuation. This

is because rates exert an ephemeral influence, while income and rent

levels (short of undergoing big changes in nominal growth rates due to

a seismic economic shift) are here to stay. The relative

unimportance of rates to this question is evident in the fact that the

payment ratios tended historically to move up

and down with mortgage rates, at least until the subprime frenzy came

into being.

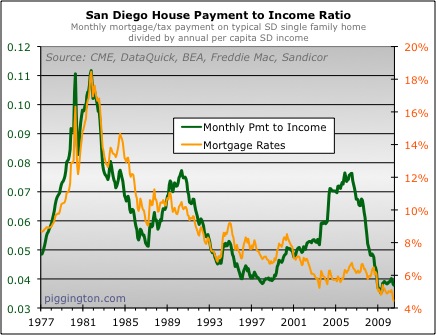

All standard disclaimers about aggregating a diverse county’s worth of

homes into a single figure or two apply. These numbers describe

what’s going on in the market as a whole. And even at that level

we are getting a mixed bag of results. Payment ratios suggest

homes are dirt cheap, but these are the far less meaningful

metrics. The price-to-income ratio indicates

slightly-above-typical but still reasonable pricing, while the

price-to-rent ratio suggests that homes are once again flirting with

overvaluation. Unfortunately all we can tell for sure is that San

Diego housing in aggregate is neither outlandishly expensive nor

excessively cheap.

I have been following your

I have been following your blog since 2007 and I have to say, you are the best source for San Diego housing trends I have seen, ever. Keep up the good work! Looking to buy a house this year…..

Thanks loutran… good luck!

Thanks loutran… good luck!

loutran wrote:I have been

[quote=loutran]I have been following your blog since 2007 and I have to say, you are the best source for San Diego housing trends I have seen, ever. Keep up the good work! Looking to buy a house this year…..[/quote]

Thanks you for the reply.

These are great graphs. But

These are great graphs. But I admit I’m a little confused about the disparity between the price-to-income vs price-to-rent ratios.

The only explanation I could come to is that landlords haven’t been raising rents, so rents are lower compared to income now than historically speaking. So, the denominator in the second graph is smaller than it should be (compared to other decardes).

Thoughts?

permabear wrote:…

The only

[quote=permabear]…

The only explanation I could come to is that landlords haven’t been raising rents, so rents are lower compared to income now than historically speaking. …

[/quote]

I think this is indeed the case (based not only on the numbers but also on observation of rents during last years). I would say there has not been noticable increase in rents since 2005. I wonder if there are other explanations, though…

Yep, that’s pretty much it…

Yep, that’s pretty much it… per capita incomes have risen more than rents in recent years. This actually makes sense: a huge building boom accompanied the housing bubble, so the ratio of homes to people rose in SD. Makes sense that rents would go down in comparison to incomes.

Rich Toscano wrote:Yep,

[quote=Rich Toscano]Yep, that’s pretty much it… [/quote]

Right. I can see that.

It is interesting if this flatnness in rents may mean that the rents will start going up substantially at some point… Is there any insight into it?

Thanks again for your update

Thanks again for your update and insights, Rich. I’d have to agree with your conclusion: houses are neither cheap nor overly expensive especially when taking into consideration these low interest rates.

Rich Toscano wrote:Yep,

[quote=Rich Toscano]Yep, that’s pretty much it… per capita incomes have risen more than rents in recent years. This actually makes sense: a huge building boom accompanied the housing bubble, so the ratio of homes to people rose in SD. Makes sense that rents would go down in comparison to incomes.[/quote]

Professor, do you have any historical data on SD rents that, say, goes back to the 1990s? I’m very curious as to how SD rents have fared relative to the national average over the last 15-20 years.

As a side note, I’m downtown and I think rents have declined from the peak by about 10% on average, and maybe 15% in some buildings. They appear to have stabilized, however, for the moment. But I think there are several projects (think Vantage Point and a few other buildings) that haven’t put all of their rental units on the market yet.

Howdy davelj — You can get

Howdy davelj — You can get rent info for SD or the whole country (sounds like you need both for your analysis) by going here and querying on “Rent of Primary Residence”:

http://data.bls.gov:8080/PDQ/outside.jsp?survey=cu

I’m not sure if I’m reading

I’m not sure if I’m reading this correctly, is the chart saying that the average list price is more than 8x the average gross income in San Diego?

I’d be interested in what the average price to income ratio of sold homes is. If we are looking to buy a home 2 – 2.5 x our gross income, are we extending ourselves more or less on average?

1. These are sale prices, not

1. These are sale prices, not list prices.

2. Since you said “our,” I assume you mean you have a two income family. The above charts use average income per person.

3. The per capita income used is that of everyone in SD, renter and owner alike. There is no data for per capita or household income among homeowners, which would obviously be higher than that of non-homeowners. So these graphs don’t really address your question… their purpose is to measure how expensive housing is compared to the past, not to map to an idealized ratio between a household’s income and its purchase price.

pjwal wrote:I’m not sure if

[quote=pjwal]I’m not sure if I’m reading this correctly, is the chart saying that the average list price is more than 8x the average gross income in San Diego?

I’d be interested in what the average price to income ratio of sold homes is. If we are looking to buy a home 2 – 2.5 x our gross income, are we extending ourselves more or less on average?[/quote]

I am guessing by our you mean household income. I don’t have exact data on this, but based on what I have seen – if you are buying 2 – 2.5x household income your are definitely not extending yourself and most folks tend to extend themselves much more than that. In this case if your household income is 150K, you are trying to buy in the 300 – 375K range. I think normally would qualify for a lot more than that and people in SD tend by about 3x or 4x household income even now, which of course depends on the amount of cash they have.

Fantastic. Many thanks,

Fantastic. Many thanks, Professor.

Here are the results.

According to the BLS, rents in San Diego increased 4.5% annually between 1995 and 2010 (using first half data for 2010). Rents in the U.S. as a whole increased 3.1% annually between 1995 and 2010 (again, using first half data for 2010).

Consequently, rents in San Diego rose by a cumulative 23% greater than rents in the U.S. as a whole over the last 15 years. The crude implication (“crude” being the operative word) is that the attractiveness of San Diego as a place to live – to the average citizen of the Republic – has risen by 23% more than the rest of the US as a whole since 1995 (since folks have been willing to accept a 23% increase in rents relative to the rest of the US in order to live here).

Now, this says nothing about absolute home values. But it does have implications for the RELATIVE increase in home values in San Diego versus the rest of the country since 1995, which has been a debate here at the Pigg in certain threads recently.

Good stuff, thanks davelj.

Good stuff, thanks davelj.

Rich,

I think we discussed in

Rich,

I think we discussed in the past the difference between median household and per capita income. I couldn’t find much data on SD median income so I took a look at US income. In the data I pulled up a while back I noticed a significant difference b/t US per capita and household income. I think the US household tracked closer to inflation. Since 1975, US per capita increased by x 6.74 and the US household income increased by x 4.26. I’m not use to pulling this data so maybe there is an error in the data I have. Anyway, just something that I noticed that I thought I would pass along.

Ed

[img_assist|nid=13835|title=Income|desc=|link=node|align=left|width=100|height=75]

davelj wrote:Fantastic. Many

[quote=davelj]Fantastic. Many thanks, Professor.

Here are the results.

According to the BLS, rents in San Diego increased 4.5% annually between 1995 and 2010 (using first half data for 2010). Rents in the U.S. as a whole increased 3.1% annually between 1995 and 2010 (again, using first half data for 2010).

Consequently, rents in San Diego rose by a cumulative 23% greater than rents in the U.S. as a whole over the last 15 years. The crude implication (“crude” being the operative word) is that the attractiveness of San Diego as a place to live – to the average citizen of the Republic – has risen by 23% more than the rest of the US as a whole since 1995 (since folks have been willing to accept a 23% increase in rents relative to the rest of the US in order to live here).

Now, this says nothing about absolute home values. But it does have implications for the RELATIVE increase in home values in San Diego versus the rest of the country since 1995, which has been a debate here at the Pigg in certain threads recently.[/quote]

That’s a good point, davelj. Okay, so housing prices should have risen 23%+inflation since 1995. I’ll go for that. 😉

CA renter wrote:davelj

[quote=CA renter][quote=davelj]Fantastic. Many thanks, Professor.

Here are the results.

According to the BLS, rents in San Diego increased 4.5% annually between 1995 and 2010 (using first half data for 2010). Rents in the U.S. as a whole increased 3.1% annually between 1995 and 2010 (again, using first half data for 2010).

Consequently, rents in San Diego rose by a cumulative 23% greater than rents in the U.S. as a whole over the last 15 years. The crude implication (“crude” being the operative word) is that the attractiveness of San Diego as a place to live – to the average citizen of the Republic – has risen by 23% more than the rest of the US as a whole since 1995 (since folks have been willing to accept a 23% increase in rents relative to the rest of the US in order to live here).

Now, this says nothing about absolute home values. But it does have implications for the RELATIVE increase in home values in San Diego versus the rest of the country since 1995, which has been a debate here at the Pigg in certain threads recently.[/quote]

That’s a good point, davelj. Okay, so housing prices should have risen 23%+inflation since 1995. I’ll go for that. ;)[/quote]

You mean mortgage payment should have risen 4.5% annually since 1995? How many people do you know pay cash for their house?

Well, if we take interest

Well, if we take interest rates into consideration, we’re probably below that. However, are we on the up side of a cycle, or are we on the down side? From my recollection, things looked a whole lot rosier in 1995 than they do today, and that’s why I think prices (and payments) are going down. We have a LOT more debt now, and fewer resources to pay it off. We have structural problems now that we were only thinking about then. IMHO, we are finally being hit with all the things many have been trying to warn about for at least a couple of decades (globalization, immigration, unsustainable debt/unfunded long-term liabilities, too much leverage, etc.). We’ve been living on credit for a long, long time; and the time is coming when we’ll finally have to pay for it.

CA renter wrote:…We’ve been

[quote=CA renter]…We’ve been living on credit for a long, long time; and the time is coming when we’ll finally have to pay for it.[/quote]

Agree, but I don’t think that time is in the next couple of years. I think it’s much further down the road. That’s just my uneducated guess.

You could very well be right,

You could very well be right, AN. That’s the problem, though; none of us knows for sure what’s coming next, we can only make (somewhat) educated guesses, and there is so much manipulation, the picture is muddied even further.

[quote=CA renter] From my

[quote=CA renter] From my recollection, things looked a whole lot rosier in 1995 than they do today [quote]

We were actually looking to buy in San Diego in 1995 and ultimately closed in Spring 1996. The defense industry in the region had been gutted. NODs and NOTS were still near peak levels.

The real estate market was hardly rosy (except maybe for the few buyers like me). We must have toured 30 houses. REOs were everyhere and sellers were happy just to have someone show up with an offer. We were able to buy with a 90-day escrow (to allow us to save up the remainder of the down payment).

Only in retrospect with rising prices from 1996 onward does 1995 look rosy. At the time, it did not.

FormerSanDiegan][quote=CA

[quote=FormerSanDiegan][quote=CA renter] From my recollection, things looked a whole lot rosier in 1995 than they do today [quote]

We were actually looking to buy in San Diego in 1995 and ultimately closed in Spring 1996. The defense industry in the region had been gutted. NODs and NOTS were still near peak levels.

The real estate market was hardly rosy (except maybe for the few buyers like me). We must have toured 30 houses. REOs were everyhere and sellers were happy just to have someone show up with an offer. We were able to buy with a 90-day escrow (to allow us to save up the remainder of the down payment).

Only in retrospect with rising prices from 1996 onward does 1995 look rosy. At the time, it did not.[/quote]

Yes, we had layoffs and lots of people scramblng for work, but it seems to me that housing prices and rents were more affordable to regular working people back then. In many industries and occupations, nominal wages are just barely higher today than they were in the mid-90s (in some industries, like construction, they have been flat or declining since the 80s); but housing prices and rents have since skyrocketed. While the more educated/skilled workers have done alright (not stellar, mind you), there is a vast portion of our population that has seen their standard of living decline greatly over the past two or three decades, but they’ve been masking this reality with tons of debt that can never be paid back.

I also think that the public sector (and private entities who do business directly or indirectly with the govt) will be hit next, and that pain is going to reverberate throughout our economy.

It doesn’t matter if rates are at zero, the debt burden is still too great for the vast majority of working people, IMHO. We need prices to fall to match what’s been happening to wages over the past few decades.

“Yes, we had layoffs and lots

“Yes, we had layoffs and lots of people scramblng for work, but it seems to me that housing prices and rents were more affordable to regular working people back then. In many industries and occupations, nominal wages are just barely higher today than they were in the mid-90s (in some industries, like construction, they have been flat or declining since the 80s); but housing prices and rents have since skyrocketed. While the more educated/skilled workers have done alright (not stellar, mind you), there is a vast portion of our population that has seen their standard of living decline greatly over the past two or three decades, but they’ve been masking this reality with tons of debt that can never be paid back. ”

CAR, the potential flaw in your logic is that you see that some people have had stagnant wages and that some people used their houses as ATM’s and lived beyond their means and then you go on to conclude that everyone is in that boat. I personally know of a few people in the boat you suggest but then I also know people that are in a far different boat. These are people perhaps similar to yourself that watched all the mania from the sidelines and lived below their means for the last decade. I know people whose wages skyrocketed who bought a house in La Costa Valley to raise their family in, paid cash, and still have 1M in other assets. If I know several people like this myself then perhaps there are more people out there like that? I know people who are thriving in this economy by buying cash flow properties at dirt cheap interest rates in places such as Vista which by the way is a pretty darn nice place to raise a family as well.

At this point, you are likely competing with other folks such as yourself who managed to avoid the temptation of the last decade and have money saved and ready to spend. Are there enough folks out there to sustain the current price levels and the cream of the crop locations? Who knows but I think the housing ATM junkies and people who lost their jobs are pretty much sidelined for now.

pemeliza,

There’s no doubt

pemeliza,

There’s no doubt that some people are doing well, as I alluded to in my prior post. There issue is whether or not a critical mass is needed to prop up housing prices in the aggregate over the long term.

CA renter

[quote=CA renter]pemeliza,

There’s no doubt that some people are doing well, as I alluded to in my prior post. There issue is whether or not a critical mass is needed to prop up housing prices in the aggregate over the long term.[/quote]

I agree with you totally. Unless you work in the financial sector or your money came or is coming from the previous bubble real estate sector and now the real estate sector that is being flooded with Federal monies in countless ways, your income barely tracked inflation.

Being that the financial sector became such a large portion of the economy, as did realestate, the “average incomes” are heavily skewed by a small percentage.

When I was in my 20’s just about everyone I knew could buy a house if they just handled their money right and many did. Today, I know only a handful of people who could afford to buy.

Exactly, sobmaz.

Exactly, sobmaz.

CA renter wrote:Well, if we

[quote=CA renter]Well, if we take interest rates into consideration, we’re probably below that. However, are we on the up side of a cycle, or are we on the down side? From my recollection, things looked a whole lot rosier in 1995 than they do today, and that’s why I think prices (and payments) are going down. We have a LOT more debt now, and fewer resources to pay it off. We have structural problems now that we were only thinking about then. IMHO, we are finally being hit with all the things many have been trying to warn about for at least a couple of decades (globalization, immigration, unsustainable debt/unfunded long-term liabilities, too much leverage, etc.). We’ve been living on credit for a long, long time; and the time is coming when we’ll finally have to pay for it.[/quote]

These things are true, but… you’re really arguing for a long future of low interest rates (not unlike Japan). Japan’s got a crapload of debt and still-overvalued real estate (although Japan’s bubble wasn’t even in the same ballpark as ours – it was a magnitude larger) and interest rates have been near zero for 15 years.

My point is that some of this stuff is self-correcting. Debt blows up, debt must be serviced (out of dollars otherwise used for consumption and investment), growth flattens or declines, interest rates fall, serving debt gets cheaper (even though there’s a mountain of it). Eventually the cycle reverses.

So, yes, we have a shitload of debt. Too much of it for sure. But the cost of servicing that debt is actually quite reasonable right now (taking into account both balance and rate) because rates are low… because of all the issues you mention above.

Thank you for posting this.

Thank you for posting this.