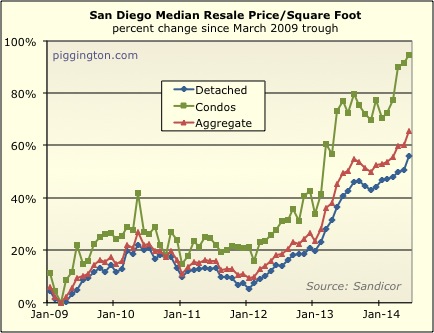

Well now… the median price per square foot for single family homes

(which is the best real-ish time price indicator) surged by 3.3%

last month:

I didn’t see that one coming. I suspect there is a good amount

of “noise” involved, and that last month’s surge will be smoothed

out in the months ahead. Nonetheless, it’s indicative of

continued upward price pressure. (Condos were up too, for what

it’s worth).

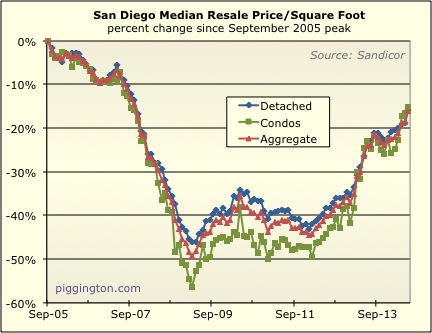

Same thing from the bubble peak:

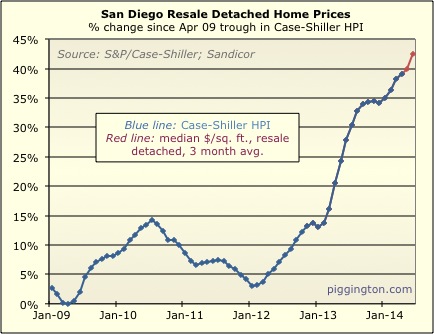

Last month’s increase gave a nice boost to the estimated/modeled

Case-Shiller index… if there was indeed a lot of “noise,” however,

the real Case-Shiller number should fix it, as it is a much more

reliable price measure than the median price per square foot.

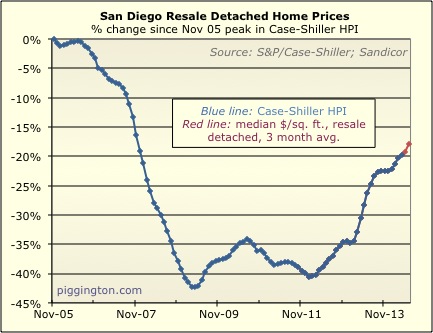

And… same thing from the peak:

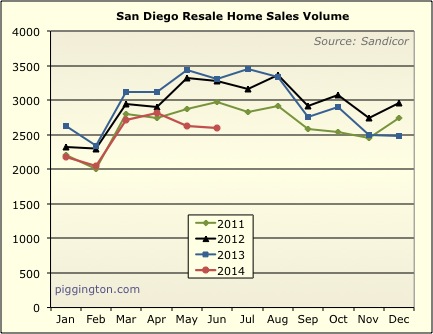

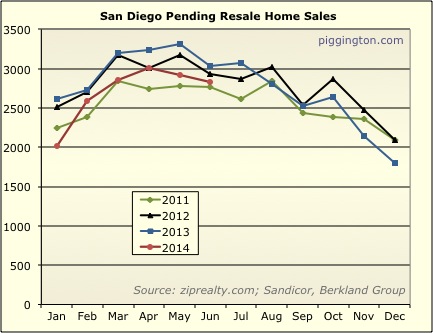

Onto supply and demand. Closed sales were anemic again:

And pendings also declined. Both are weaker than this time

last year.

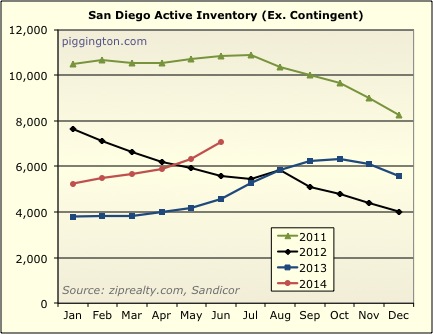

Inventory continued its recent rise:

But this chart shows that the rise in inventory hasn’t made a huge

dent in absolute terms:

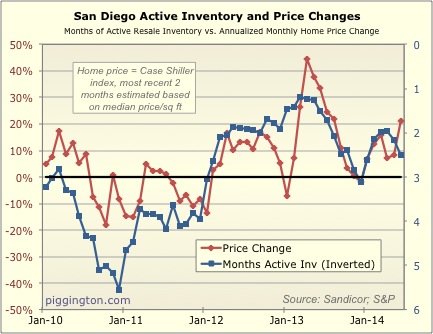

If we look only at active inventory, that’s risen a lot more.

Active inventory is 55% higher than it was last year!

This chart shows contingents in red and actives in blue… the

decline in the former having offset the rise in the latter,

somewhat:

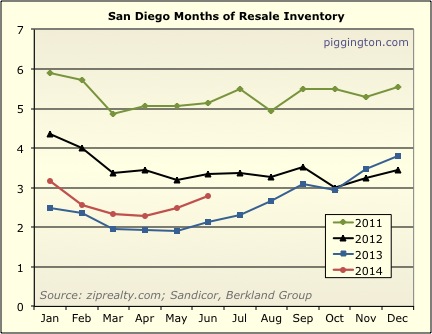

Here’s months of inventory (including contingents). This

continues upward from a historically very low level.

Here’s a linear look:

And here are the same things looking only at months of active

inventory. Months of active inventory is up 66%(!) year over

year…

But still on the low side, historically speaking:

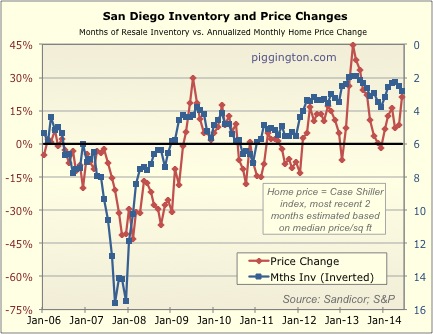

Here are the two measures of months of inventory (active +

contingent, and active only) graphed over the monthly change in home

prices. Months of inventory is inverted to better show the

relationship… ie, a declining line signifies rising inventory:

You can probably see why last month’s price jump was a surprise (to

me, anyway). Both measures of months of inventory have been

trending up (down on the chart)… inventories are still low, and

commensurate with upward price pressure, but given the upward trend

in inventories I would have expected price appreciation to be

decelerating. Instead, prices surged. Maybe it’s noise,

or maybe prices legitimately rose due to some other factor (the

recent decline in rates?). I suppose the months ahead will

give us a better idea.

What is considered a balanced

What is considered a balanced inventory? The value seems to jump around all over the place. 3 months seems low, but I haven’t seen any values prior to 2007.

Bewildering, when I first did

Bewildering, when I first did the original chart, 6 months was about the level that tended to mark the threshold between rising and falling prices. Interestingly, this is spot on with the “6 months of inventory is a balanced market” rule of thumb I’ve occasionally thrown around.

They didn’t even break out contingent inventory until more recently, so it’s tougher to know what is balanced if we are looking at active only. The huge presence of contingent inventory, and its subsequent disappearance, have both distorted things so that it’s harder to tell what’s going on…

UT San Diego recently had and

UT San Diego recently had and article on the return of 0-down loans:

http://www.utsandiego.com/news/2014/Jul/11/zero-percent-down-mortgages-return-loans-homes/?#article-copy

Sounds like 0-down loans are limited to a few credit unions, but are lending standards going down again more generally? Could that contribute to the increasing prices? Or would you expect increasing number of sales if that were that case?

This article says that 0%

This article says that 0% down was brought back in 2010 by NFCU. With QM coming into force this past January, there’s next to no secondary market for 0% down loans. I seriously doubt that this is a big factor, especially since sales aren’t rising like during the last bubble.

I’d suggest interest rates

I’d suggest interest rates are a big factor here. The 10-year bond interest rate is down 1/2 % so far this year, and mortgage rates track this instrument pretty closely. Plus, credit standards are reportedly being relaxed of late for home buyers.

The interest rate decline is surprising everyone, since the forecasts at the end of last year were for higher rates. Blame that on weak GNP growth (actually minus 2.9% rate in the first quarter) so far this year. With economists rapidly lowering their growth forecasts, low mortgage rates may be with us for some time.

US bond yields are high

US bond yields are high compared to international bond yields. Irish 10-year bond yields are now 2.23 – US are 2.45. Weird considering Irish yields were above 10 a few years ago…

Japan and Swiss 10-year yields are 0.6. Is this the future for the US 10-year bond yield?

I can’t imagine US yields going higher in this international market. So mortgage rates might be heading even lower.

Prices have been all over the

Prices have been all over the map in the past five years, even with low mortgage rates. You’re ascribing some sort of rationality to the market. Perhaps geopolitics will be good for a scare.