Forum Replies Created

-

AuthorPosts

-

October 1, 2007 at 4:55 PM in reply to: Fairbanks Ranch vs. Santaluz vs. Cielo vs. rest of Rancho Santa Fe #86642

Eugene

ParticipantSpeaking of which, where do people buy their groceries or go to the mall if they live in FBR, Cielo, Santaluz etc?

I may be mistaken but I think most people who live in FBR Cielo etc. don’t really buy groceries, they have servants/butlers/maids who do it for them.

If you have 3 mil to spend on a house, you can certainly afford a $50k/year servant to take care of the house, water the lawn, wash your Aston Martin, and buy groceries.

Participant“if you are married AND don’t mind the wife knowing”

You can get 200k in an account that’s yours but payable on death to your wife.

ParticipantIt’s a buyer’s market, in all likelihood you’re the only bidder on the property, and he’s bluffing to make you pay more than he’s willing to take for the property.

Pull the offer, resubmit a new one for $50k below previously agreed price with 72 hour deadline. If it expires, go away and wait.

Participantescalating the cost of these goods and reducing consumption is exactly the point. difference between american levels of consumption and production is what ultimately drives this devaluation.

ParticipantMission of the Fed is to ensure orderly functioning of the economy. If gradual devaluation of the dollar is what it takes, than that’s what it takes. There are worse things in life than devaluation. If you had to choose between $2 euro and 25% unemployment, what would you prefer?

Devaluation of the dollar is an unfortunate necessity. Many serious economists (e.g. Paul Krugman) warned that we had it coming for a few years. Basically, the story is that our current state of affairs (large trade deficits financed by foreigners buying low yield dollar-denominated debt) results in artificially overpriced dollar and is not sustainable indefinitely. Trade deficits must close, that can happen either through gradual currency devaluation or through sudden dollar collapse (aka “Wile E. Coyote Moment” – google it).

kicksavedave: rates are spiking because foreign investors are coming to realize that investing in the dollar is risky and they are demanding higher interest rates to protect them against devaluation. Interest rates will increase (maybe substantially, to 10% or more) and they will only come back down when dollar is sufficiently devalued and balance of trade is restored. Rate increase may help in the short run but the real underlying problem is long-term and it seems that the genie is out of the bottle.

ParticipantMy thoughts.

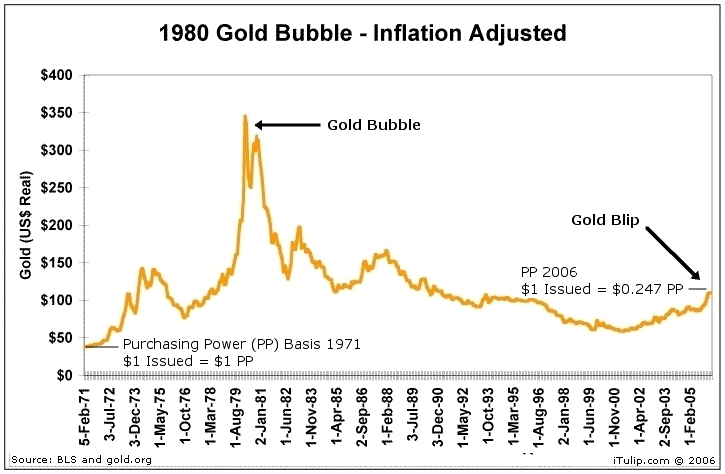

On gold: yes, gold has the tendency to get bubbly. But it’s nowhere near as expensive as it might be.

http://www.itulip.com/images/goldReal.jpg

And even 1980 peak is not the limit. We have almost a billion of people living in the Western world, and all these people are conditioned to believe that their dollars and euros and pounds maintain their value well. Imagine what happens if things start going haywire, America hyperinflates, Europe follows by lowering rates, and all these people lose their trust in fiat currencies. Also, imagine what happens if some country ends up going back to gold standard. There’s surprisingly little gold in the world. Total value of all gold ever mined is somewhere around $3 trillion at current prices. For comparison, total liquid net worth of all Americans is $30 trillion.

On TIPS: they are not as bad as people think. Government has been trying to keep some price increases from showing up in CPI, but it’s been mostly successful in delaying the effects. For example, they hid the housing bubble from CPI by using rent figures and excluding house prices. Guess what, now we’re looking at accelerated increases in rents nationwide as house prices are going down and former “homeowners” end up back in the rental market.

Overall, TIPS and gold are on two opposite ends of risk/reward specturm. TIPS are low risk (guaranteed not to lose any money) but low reward. Foreign currencies are in the middle. Gold is high risk (what if it falls back to $200?) but very high profit potential if you time the bubble and sell at the peak.

Participantyeah. moral questions aside, this is not going to make heck of a lot of difference. they are not rising debt to income ratio limits, that’s the important part.

Participantso to summarize

Most 30-year fixed loans are tied to 10-year treasury. Today 10-year treasuries profoundly ignored the rate cut and closed 0.01% higher than yesterday. If 50 point cut triggers a run on the dollar, 10-year treasuries will go through the roof.

Most ARMs are tied to LIBOR. LIBOR is generally correlated with Federal funds rate, but it does not have to be. We’ll see soon if it drops anywhere near 50 bps.

Many adjustable-rate credit cards and HELOCs are tied to “prime” rate, which is typically Federal funds rate + 3%.

ParticipantI live in RB and work in UTC. I can get from my house to my job using public transportation (one bus connection, 20->31, if i remember correctly). There are bus stops next to my house and next to the office where I work.

There’s just one problem. The same trip that takes me 20 min with my car (25 in rush hour) takes 1 hour 50 min with the bus. That includes 20 min wait on a bus stop somewhere in Mira Mesa.

Oh and the bus ticket ($2.25 last i checked) costs more than gasoline burned by my relatively fuel inefficient car during 15-mile trip.

Any wonder why i prefer to drive?

September 16, 2007 at 9:36 PM in reply to: possible rate cut this tuesday;will it boost home sales & prices? #84767ParticipantLower fed rates may affect RE if they translate into lower interest rates on fixed-rate mortgages. Short term (6-12 months) lower interest rates won’t matter. Long term (2-5 years) lower interest rates mean that bottom is formed sooner.

There’s doubt that fed rate matters much in RE any more. Too much rate cutting – weakening dollar – global investors stop buying US Treasuries – Treasury yields go up – mortgage rates follow.

Participant” I still don’t see that 17% were leveraged to 90%. You are assuming that every one of those 123,000 was ??

What month is that 123,000 through ? Recent sales haven’t dropped as much.In any case, well over 80% probably don’t have any problem.

Over 95,000 homes have no mortgage at all.”123,000 is from January 2005 to July 2007. If national averages apply to SD, they were, on average, leveraged to 91%. I think San Diego should be higher simply because San Diego prices are much higher. In any case, 40% of 123,000 got interest-only or negative amortization loans and I don’t imagine many of those putting any money down at all.

I think the situation is this –

20% of people have their houses paid off completely

40-50% have a lot of equity

15-25% are at risk of going under water (negative equity) if prices decline another 20%

15% are under water alreadyand “under water” is DEEP under water, because prices are so high. If someone buys a median house with 0 down interest-only at the peak and that house depreciates just 20%, that person is under water for about 2x average annual household income in San Diego. Have things ever gotten so bad during 90’s?

P.S. I screwed up, 123k is 22% of 550k.

P.P.S. There’s also Temecula and Murrieta. That’s where things are really fun. Around 20k new and existing houses sold in 2005-2007 vs. total housing stock of 40-50k houses.

ParticipantHLS

“In San Diego county, I think that it would be a HUGE stretch to say that 10% of homes are leveraged over 90% even at todays price.

I don’t know how many homes there are in the county.”It is considerably more than 10%.

According to http://www.city-data.com there are around 550k owner-occupied houses and condos in the county.

According to bubbletracking.blogspot.com, 93k new and existing houses and condos were sold since 07/2005. Estimate 30k more houses sold during 1st half of 2005. Most likely, every one of these houses is worth less than they were paid for. 123k is 17% of all housing stock.

What mortgages did those buyers take?

* Around 80% were ARMs, more than 40% were interest-only or negative amortization

* Around 50% put 5% or less down out-of-pocket (CLTV >95%)

* Average nationwide CLTV was 91% in 2006, can’t find data for San Diego but it’s gotta be higherSo here you have 17% of houses that were leveraged to 90+% (average) back when they were bought. I’m not counting houses that were bought in 2004 and financed for 100% down; and I’m not counting houses that were refinanced in 2005-2006.

So, the correct statement would be “10% of homeowners are in negative equity land even at todays price.” Each one of these 10% is a foreclosure candidate. If prices were to fall further, this 10% can grow. It’s a vicious circle.

That’s the big problem we have today. When housing prices peaked in 2005, public did not yet accept the reality of the housing bubble, and lenders did not cut down on exotic mortgages. We were given 2+ years to build up a huge inventory of houses that were bought at sky-high prices for little or no money down, whose new owners won’t think twice about foreclosing if market corrects even by 20%.

Participant“Tell that to the people that bought gold in 1980 :)”

What I really meant is – gold coins don’t depreciate simply because you bought them. If you buy a Gucci handbag, or a Rolex watch, or even a diamond necklace, can you sell it back to the same dealer who sold it to you, without significant loss? No you can’t. Even a car will depreciate 10% the moment you drive it off the lot.

If you buy gold bullion coins online at kitco.com or onlygold.com, you can turn around and sell them back and only lose 5% of the price.

Participantit’s a good way to diversify, and it’s an OK way to prop up your self esteem if you have too much money (compared with what people do when they want to feel filthy rich). If I were rich, I’d rather have a stack of pretty gold bullion coins on my desk than a Rolex watch or a designer handbag for my wife. At least gold coins don’t depreciate.

Gold works best if you have a way to hide it from the government. Last time United States were in a major financial crisis (1929-1933), government ended up trying to confiscate all gold held by private citizens. If you had gold in a safe deposit box in your bank, you were screwed.

-

AuthorPosts

{kind=link}