- This topic has 33 replies, 11 voices, and was last updated 9 years, 8 months ago by

spdrun.

-

AuthorPosts

-

May 12, 2016 at 8:08 PM #21967May 13, 2016 at 6:16 AM #797536

The-Shoveler

ParticipantIn SoCal At Least it is more a classic housing shortage IMO.

May 13, 2016 at 7:24 PM #797557spdrun

ParticipantThe gyrations of the housing market in the last ~5 years aren’t accounted for by population trends, though.

May 17, 2016 at 6:43 AM #797637moneymaker

ParticipantWhat is the PE for the DOW now compared to then? Unemployment was actually higher in 1982 than right after the BB (bubble burst). Think when everything is considered we are on the precipice of something big, especially when you throw in Trump and government spying/TSA

May 17, 2016 at 8:04 AM #797643ctr70

ParticipantIf house prices are to keep going up or even stay flat, rates must stay in a very low and tight range for a very long time.

Let’s be honest with ourselves, probably at least 50% of all the housing price recovery since 2011 has been due to one thing, artificially low mortgage rates manipulated by Fed. Not due to fundamentals in the economy like good jobs and rising incomes. The 50 year average of 30 yr fixed mortgage interest rates is 7-8%, that is where they should be. If they had not been pushed to ridiculously artificially low levels (30 yr fixed in the 3% range are you kidding me?), there is no way prices would be where they are today. Where do you think prices would be in SD if the 30 yr fixed was 7%? So this is all the proof you need this is a Fed engineered housing recovery, not a housing recovery based on real fundamentals.

With that said, rates could still fall further if we get bad economic news or stocks fall. 30 yr fixed rates could fall to 3.00% or in the 2% range, and housing may be stimulated once again. But ask yourself is all this healthy? Is it healthy for economies around the world to get addicted to low rates and QE vs. real growth? Is it healthy for the Fed to keep inflating assets? I mean we are in the 7th year since the end of the recession and rates are basically still at zero! There is something not quite right with that picture.

May 17, 2016 at 9:15 AM #797647ParticipantMaybe zero rates is the first step to getting rid of money all together like on Star Trek ☺ . The big bear hiding in the closet is that these low rates are costing the government money, not exactly sure how but nothing is free, not even artificial low rates. Does it contribute to the national debt?

May 17, 2016 at 10:13 AM #797649FlyerInHi

GuestWhat makes you think that today’s rates are artificially low? What is artificial and real?

Money is just a human created means of exchange in commerce. There should be no reason for money to automatically make money on money, such as when rates are high.

Maybe we are just smarter in managing the money supply?

May 17, 2016 at 10:48 AM #797650Participant[quote=FlyerInHi]What makes you think that today’s rates are artificially low? What is artificial and real?

Money is just a human created means of exchange in commerce. There’s should be no reason for money to automatically make money on money, such as when rates are high.

Maybe we are just smarter in managing the money supply?[/quote]

Rates are artificially low because they are 100% driven by the Fed and not the free market. 95% of all mortgages originated today are Gov’t backed. This is far higher % than this has been in most of U.S. history. Do you really think if the mortgage market were more balanced with private investors that these private investors would take the risk for 3.5% return on a 30 yr fixed mortgage? The only reason rates are at 3.5% is because the Fed (aka tax payers) is guaranteeing 95% of all mortgages, and billions in Mortgage Backed Securities were purchased with Gov’t printed QE money helping to keep rates down.

It doesn’t seem healthy to me that the world economy is driven more and more by central Fed planning, rate manipulation, money printing, and more & more debt vs. true fundamentals, rising incomes, and good jobs.

I’m not smart enough to know how this all works out. Maybe it all works out and fixes itself. But there is no doubt we are in uncharted waters with this global monetary policy experiment that has been going on the past 8 years.

May 17, 2016 at 2:45 PM #797669mixxalot

ParticipantThe real estate prices do not pencil out to average incomes. It is foreign buyers, low inventory and institutional wall street firms jacking up prices.

May 17, 2016 at 3:13 PM #797670Participant[quote=mixxalot]The real estate prices do not pencil out to average incomes. It is foreign buyers, low inventory and institutional wall street firms jacking up prices.[/quote]

And mortgage rates the last few years being the lowest they have ever been in the 240 year history of the United States.

Super low rates especially juice the prices in expensive coastal areas. 3.5% vs. say 6.5% on a $700k mortgage in CA has a much bigger impact than 3.5% vs. 6.5% on a $100k mortgage in Nebraska.

May 17, 2016 at 3:40 PM #797671bearishgurl

Participant[quote=ctr70][quote=mixxalot]The real estate prices do not pencil out to average incomes. It is foreign buyers, low inventory and institutional wall street firms jacking up prices.[/quote]

And mortgage rates the last few years being the lowest they have ever been in the 240 year history of the United States.

Super low rates especially juice the prices in expensive coastal areas. 3.5% vs. say 6.5% on a $700k mortgage in CA has a much bigger impact than 3.5% vs. 6.5% on a $100k mortgage in Nebraska.[/quote]Agree with this except in the most coveted coastal areas (where the majority of buyers pay all cash). Some coastal areas (usually within one mile of the coast) have truly proven to be “bubble-proof” as land on the coastal strip is a finite resource.

And you may be surprised in places like NE (or states with even cheaper RE) it isn’t uncommon for a buyer to pay all cash, as well, especially if it is a vacation home or home purchased for relatives to live in. It’s also not uncommon for first-time buyer-residents of states with cheaper residential RE to pay off the home within ~5 years of purchasing it. In these areas, mortgage interest rates aren’t as sensitive as they would be to purchasers of garden variety tract homes in more expensive locales.

Nice to see you back here posting, ctr70. Are you still living/working up in the PNW?

May 17, 2016 at 4:29 PM #797673GuestCtr70 , I think we will have low rates for a long time because of excess capacity. unlimited things can be produced for cheap.

We need money circulating to soak up capacity, that’s why central banks are acting. Not only the Fed, but ECB, China, Japan.

Ideally, governments need to tax and spend and put money in people’s pockets. But that’s politically hard to do.

I’m watching China’s pivot to a consumer economy. The government built a lot of modern infrastructure. They are now building a social safety net to encourage consumers to spend. We will see how it works out in the next few decades

Now is the 50th anniversary of China’s cultural revolution. I was reading that, at the time, people were starving and had nothing. The period since then has been the greatest creation of wealth in the history of capitalism.

May 17, 2016 at 9:14 PM #797683 Rich ToscanoKeymaster

Rich ToscanoKeymasterThanks OP, glad to see Grantham and GMO getting some attention here. They are as good as it gets when it comes to identifying and analyzing bubbles. FYI – you have to register to access their stuff but it’s free and well worth the small effort.

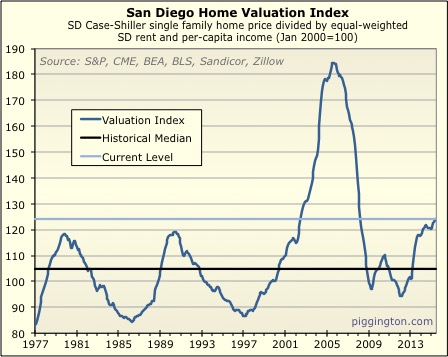

My own version of the graph looks a little different as, unlike US-wide prices, SD prices have been a lot more volatile.

So the US-wide overvaluation is more unusual than the SD level of valuation, for what that’s worth.

All due respect to Grantham (who is literally my investing hero — btw I got to meet him once, it was awesome </fanboy raving>) — I don’t see it so much as an echo bubble, as just a response to low rates. Rates are extremely low and even at these price levels, buying can pencil out. So it’s more like high housing prices are a rational response to (irrationally?) high bond prices.

But that’s just my feeling on it. When in doubt, listen to Grantham.

(Fortunately, the question of whether the “bubble” label fits or not is not all that important –and I’m sure my man JG would agree with that. The important issue is that housing is expensive, whatever the reason may be, and prospective risk/returns should be evaluated accordingly).

May 17, 2016 at 9:24 PM #797684Rich ToscanoKeymaster[quote=FlyerInHi]What makes you think that today’s rates are artificially low? What is artificial and real?

Money is just a human created means of exchange in commerce. There should be no reason for money to automatically make money on money, such as when rates are high.

Maybe we are just smarter in managing the money supply?[/quote]

I don’t really think your money supply thing explains it. That might explain low inflation, but it doesn’t explain why real rates are negative. (I actually think the whole premise is questionable, but even if we allow it, it doesn’t explain the negative real rates).

Let’s avoid the word “artificial” — that has a lot of implications. What we can say is that rates are very, very low. Lower than inflation, which has never historically lasted, and with good reason.

I suppose it’s possible that rates stay this low, but I think that people who are depending on that (unprecedented) outcome are taking a huge risk. There’s a difference between allowing for it, and depending on it… and many (maybe most) investors seem to be doing the latter as far as I can tell.

May 18, 2016 at 8:29 AM #797691natesactm

ParticipantRich – Re-reading your “Shambling Towards Affordability, Mid-Year 2015” post, the influence is pretty clear. GMO has been a newer find for me, but have since devoured their free content. So much good stuff in there!

-

AuthorPosts

- You must be logged in to reply to this topic.